A recent survey of bank officers shows U.S. institutions are tightening their lending standards and raising rates on commercial loans and credit cards.

Details:Bankers say they have increasing concern about future economic growth, despite continued U.S. labor market strength and solid economic fundamentals. The data banks are seeing runs contrary to the overall narrative of a strong U.S. economy.

Driving the news: Credit card delinquency rates in Q1 hit the highest level since 2012, driven in part by a spike in overdue payments by people ages 18–29, according to a report out this week from the New York Federal Reserve.

What’s happening: In addition to the inability to make credit card payments, the rise in younger borrowers’ delinquency rates — by far the highest among all age groups — reflects the cohort jumping into the credit card market at a faster rate, as well as the eagerness of banks to latch on to younger consumers. Still, the delinquency rate remains well below that seen during the financial crisis.

More young people are opening credit cards now than they did in the the past decade — about 52% in 2018 verses 46% in 2008, per the New York Fed — pushing up the likelihood of more delinquencies.

Credit card accounts among young borrowers fell in 2009 following the passage of the Card Act, which added new rules for consumers under 21 looking to borrow and limited how much banks could advertise to young people.

“There has been some recovery in credit card prevalence in recent years, consistent with increased issuance in card accounts,” according to the Fed.

Why it matters: After the financial crisis, young people had been largely debt-averse — particularly with credit cards — as a result of the the Great Recession. But that trend looks to be reversing.

“Banks were a little concerned going forward and [expect to] tighten standards,” David Norris, head of U.S. credit at TwentyFour Asset Management, tells Axios.

“I think from the viewpoint of the marketplace, if that’s going to continue … it works its way into consumer spending habits, consumer attitudes, and that can affect the demand side of the economy.”

That move comes as U.S. debt is $1 trillion higher than its previous record…

The N.Y. Fed’s latest report shows that total household debt increased by $124 billion in Q1. It was the 19th consecutive quarter with an increase, and household debt is now $993 billion higher than the previous peak of $12.68 trillion in the third quarter of 2008.

Between the lines: Delinquency rates are trending up again, and not just for younger consumers.

The report found that seriously delinquent credit card balances have also risen for consumers aged 50–69.

For borrowers aged 50–59 and 60–69, the 90-day delinquency rate increased by nearly 100 basis points each.

“People are probably extending themselves too much,” said TwentyFour’s David Norris, also noting that the headline numbers for Q1 U.S. GDP were a bit misleading.

“Banks are seeing this currently and they’re beginning to get concerned about credit quality and the quality of borrowers and they’re trying to tighten standards. This is a signal that we need to watch out for.”

A deeper look at the credit card delinquencies that are steadily rising…

In the Fed’s latest U.S. bank senior loan officers survey, which provided data from the fourth quarter of 2018, loan officers predicted more delinquencies this year as a result of the growth of “non-prime” borrowers. They’ve cited that as a reason for an anticipated pullback in credit and an increase in rates.

U.S. card holders are expected to pay $122 billion just in interest charges this year. That’s 50% more than what they paid just 5 years ago.

Financial challenges, including increasing costs, shaky Medicaid reimbursement, reductions in operating costs and bad debt, ranked No. 1 on the list of hospital CEO worries in 2018, according to an American College of Healthcare Executives poll.

Government mandates and patient safety and quality tied for second place in ACHE’s survey of top issues facing health systems. Workforce shortages came in third.

A little more than 350 execs responded to the survey and ranked 11 concerns their facilities faced last year. Behavioral health and addiction issues, patient satisfaction, care access, physician-hospital relations, tech, population health management and company reorganization filled in the remaining slots.

Dive Insight:

No matter which cog in the healthcare system one blames for the skyrocketing costs of healthcare (big pharma inflating the list prices of drugs; hospitals for upmarking services; insurers for leaving gaps in care resulting in surprise bills) consumers’ pocketbooks aren’t the only ones affected.

A separate American Hospital Association-backed study predicted health systems will lose $218 billion in federal payments by 2028, and private payers (whose dollars would normally help hospitals make up the difference) have been curtailing reimbursements as well.

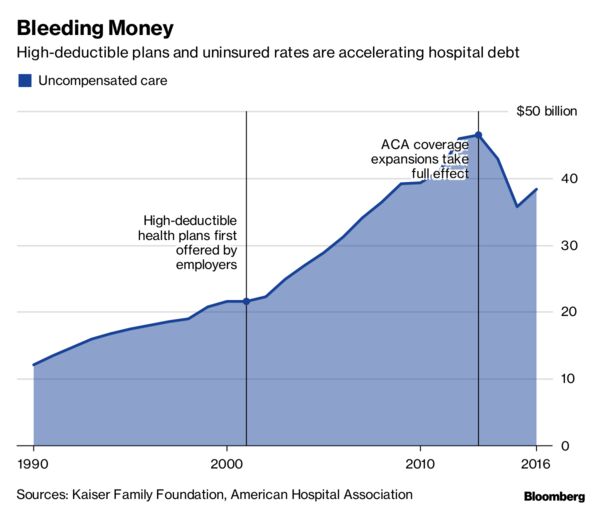

Bad debt was another fear in the ACHE report. Uncompensated care costspeaked in 2013 at $46.4 billion and, though the figures have decreased slightly since then, hospitals shelled out $38.3 billion in 2016. Wisconsin alone was on the hook for $1.1 billion in uncompensated care in fiscal year 2017.

“The survey results indicate that leaders are working to overcome challenges of balancing limited reimbursements against the rising costs of attracting and retaining talented staff to provide that care, among other things,” ACHE president and CEO Deborah Bowen said in a statement.

Other financial concerns included competition, government funding cuts, the transition to value-based care, revenue cycle management and price transparency.

And 70% of hospital CEOs were worried about shifting CMS regulations in 2018, along with regulatory/legislative uncertainty (61%) and cost of demonstrating compliance (59%) — unsurprising, given the current administration’s track record of unpredictability.

Patient safety and quality of care was also top of mind for health system CEOs, with over half of respondents anxious about the high price of medications, involving physicians in the culture of quality and safety and getting them to reduce unnecessary tests and procedures.

Also of interest was the high rank given to addressing behavioral health and addiction issues, according to Bowen, which ranked fifth in its first year of being included in the survey. The topic has been front and center in the industry of late, in line with the increasing recognition of social determinants of health and the breakdown in silos of care.

Ranking of the issues has remained largely constant since 2016, though in 2017 more hospital CEOs were concerned about personnel shortages than patient safety and quality.

Moody’s Investors Service has issued a negative outlook on the nonprofit healthcare and hospital sector for 2019. The outlook reflects Moody’s expectation that operating cash flow in the sector will be flat or decline and bad debt will rise next year.

Moody’s said operating cash flow will either remain flat or decline by up to 1 percent in 2019. Performance will largely depend on how well hospitals manage expense growth, according to the credit rating agency.

Moody’s expects cost-cutting measures and lower increases in drug prices to cause expense growth to slow next year. However, the credit rating agency said expenses will still outpace revenues due to several factors, including the ongoing need for temporary nurses and continued recruitment of employed physicians.

Hospital bad debt is expected to grow 8 to 9 percent next year as health plans place greater financial burden on patients. An aging population will increase hospital reliance on Medicare, which will also constrain revenue growth, Moody’s said.

Highlighting a key implication of the rise in high-deductible health plans, both on the ACA exchanges and in employer-sponsored insurance, the article describes a question now commonly faced by doctors and hospitals—how best to collect their patients’ portion of the fees they charge? As one Texas doctor tells Bloomberg, reflecting the experience of the Maldonados from the other side of the equation, “If [patients] have to decide if they’re going to pay their rent or the rest of our bill, they’re definitely paying their rent.” He reports that the number of people dodging his calls to discuss payment has increased “tremendously” since the passage of the ACA. Another Texas doctor reports that his small practice had to add an additional full-time staff member just to collect money owed by patients, adding further overhead to his practice’s costs and making it more likely that he, like many other doctors, will eventually seek shelter by being employed by a larger delivery organization. That trend, as has been repeatedly shown, further increases the cost of care, exacerbating the increase in insurance costs for families like the Maldonados. This Gordian knot of increasing costs, rising deductibles, and growing premiums has left us with a healthcare system that’s forcing difficult decisions at every turn, for patients and providers.

Physicians, hospitals and medical labs are grappling with the rise in high-deductible insurance.

Doctors, hospitals and medical labs used to be concerned about patients who didn’t have insurance not paying their bills. Now they’re scrambling to get paid by the ones who do have insurance.

For more than a decade, insurers and employers have been shifting the cost of care onto their workers and customers, tamping down premiums by raising patients’ out-of-pocket costs. Last year, almost half of privately insured Americans under age 65 had annual deductibles ranging from $1,300 to as high as $6,550, government data show.

Now, instead of getting paid by insurance companies on a predictable schedule, health-care providers have to engage in an awkward dance. One moment they’re removing a pre-cancerous skin mole. The next, they’re haranguing patients to pay what’s become a growing portion of the total medical bill.

“It’s harder to collect from the patient than it is from the insurance,” said Amy Derick, a doctor who heads a dermatology practice outside Chicago. “If the plans change to a higher deductible, it’s harder to get the patients to pay.”

Independent physicians cited reimbursement pressures as their biggest concern for staying in business, according to a report by Accenture Plc in 2015.

“If they have to decide if they’re going to pay their rent or the rest of our bill, they’re definitely paying their rent,” said Gerald “Ray” Callas, president of the Texas Society of Anesthesiologists, whose Beaumont, Texas, practice treats about 40,000 people annually. “We try to work with the patient, but on the other hand, we can’t do it for free because we still maintain a small business.”

Accenture

In 2016, Callas introduced payment options that allow patients with expensive plans to pay a portion of the bill upfront or on a monthly basis over several years. Even so, Callas said the number of people avoiding his calls after surgery has increased “tremendously” each year since the Affordable Care Act passed in 2010.

Derick instituted a “time-out” option a few years back that gives patients the billing codes before a procedure, allowing them to call their insurance companies for estimates. Even with the program, collection rates are slower, especially at the beginning of the year when insurance plan deductibles reset.

Even large medical companies with national operations are facing the problem. Quest Diagnostics Inc., the lab-testing giant, said 20 percent of services billed to patients in the third quarter of this year went unpaid, costing the company about $80 million in lost revenue.

“We certainly have a high bad-debt rate for the uninsured,” Chief Financial Officer Mark Guinan said in a telephone interview. “But really the biggest driver is people with insurance. It’s their coinsurance and their high deductibles, and they don’t always pay their bills.”

Another testing company, Laboratory Corp. of America Holdings, reported its first year-over-year uptick in unpaid bills in the first quarter of 2016. At the time, Chief Executive Officer David King said high-deductible plans, higher copays and greater incidences of non-covered services led to more dollars being shifted to patients. LabCorp declined requests for comment.

Northwell Healthcare Inc., a network of more than 700 hospitals and outpatient facilities, lost $106.9 million to unpaid services in 2015. Others have reported the same: Acute-care and critical-access hospitals reported$55.9 billion in bad debt for 2015, according to data compiled by the American Hospital Directory Inc.

“High-deductible plans have had a very big impact,” said Richard Miller, Northwell’s chief business strategy officer.

Kaiser Family Foundation, American Hospital Association

When it comes to reimbursement, a common denominator across the health-care industry is the archaic process through which bills are processed — a web of medical records, billing systems, health insurers and contractors.

High deductibles only add to the red tape. Providers don’t have real-time, fully accurate information on patient deductibles, which fluctuate based on how much has already been paid. That forces providers to constantly reach out to insurance companies for estimates.

Tarek Fakhouri, a Texas surgeon specializing in skin cancer, had to hire an additional staff member just to reason through bills with patients and their insurers, a big expense for an office of six or seven employees. About 10 percent of Fakhouri’s patients need payment plans, delay their skin-cancer surgeries until they’ve met their deductibles, or have to choose an alternative treatment.

According to a study earlier this year by the Journal of American Medical Association, primary-care physicians at academic health-care systems lose about 15 percent of their revenue to billing activities like calling insurance companies for estimates.

“It’s an unnecessary added cost to the health-care system to have to hire staff just to sit there on hold with insurance companies to find out what a patient’s deductible status is,” said Fakhouri.

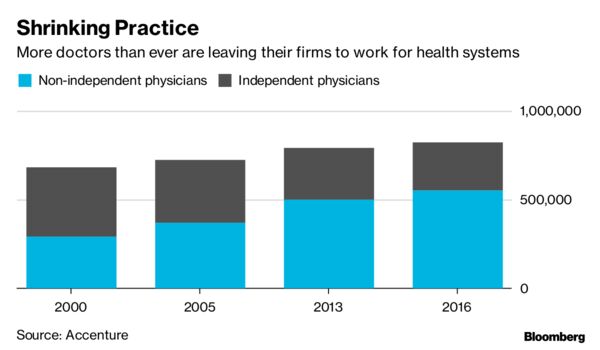

Callas, Derick, and Fakhouri said they all know physicians who have left private practice altogether, some for the sole purpose of ending their dual roles as bill collectors. According to a study by the American Medical Association, less than half of doctors were self-employed as of 2016 — the lowest total ever. Many left their own practices in favor of hospitals and large physician groups with more resources.

To cope with the challenge, labs and hospitals are investing millions in programs designed to help patients understand what they owe at the point of care. Northwell has been implementing call centers and facilities where patients can ask questions about their bills.

“There’s a burden on both sides,” said Callas. “But health-care providers get caught in the middle.”

A lack of OON benefits leads to never-ending financial obligations for patients and a greater likelihood of bad debt for providers.

Surprise, sky-high medical bills have been irking patients and legislators a lot lately, but as the number of patients with out-of-network (OON) benefits shrinks, the problem of high bills will continue to grow, according to research from the Robert Wood Johnson Foundation.

A lack of OON benefits leads to never-ending financial obligations for patients and a greater likelihood of bad debt for providers, according to Katherine Hempstead, PhD, senior policy adviser at the Robert Wood Johnson Foundation.

Hempstead authored the new analysis, which looked at trends in OON benefits in the individual and small group markets.

“Out of network benefits have become much less common, especially in the individual market, where the proportion of plans with OON benefits has declined from 58% in 2015 to 29% in 2018 in the individual market,” she tells HealthLeaders via email.

“In the small group market, the decline was smaller: 71% to 64%,” she says.

However, even plans that do offer OON benefits increasingly have very high deductibles and maximum out-of-pocket (MOOP) caps.

For instance, in the individual market, the median OON deductible is approximately $12,000, the analysis shows. Some are even higher.

“A sizable share of plans in the individual markets have OON deductibles that exceed $20,000, and have no MOOP, meaning that patient obligations can continue infinitely,” Hempstead says.

For hospitals and health systems, all of this adds up to more patients who will be unable to pay their bills.

“The takeaway for revenue cycle managers is that most customers in the individual and small group market have little or no out-of-network coverage,” Hempstead says.

Because of this lack of OON coverage, hospitals and health systems should do some investigating beforehand.

“It will be important to ascertain in-network status before providing services, or the likelihood of bad debt will be high,” Hempstead says.

That’s something that hospitals and health systems can feasibly do, “especially if they have a price estimator tool,” says Donella J. Lubelczyk, RN, BSN, ACM-RN, CRC, CRCR, executive director of revenue cycle at Catholic Medical Center in Manchester, New Hampshire.

“They would need to do this with the patient and make sure the patients understand their out-of-network costs prior to selecting the service(s),” Lubelczyk says via email.

Patients also have a responsibility to know which providers are in and out of their networks.

A recent HealthSparq survey shows that 40% of patients who received a surprise bill said they could have done more to better understand their benefits and healthcare processes.

“Patients really need to understand their in-network plans, but most people do not and need to get assistance,” Lubelczyk says.

Maine’s Republican governor is publicly laying out a proposed tax hike on hospitals to pay for voter-approved Medicaid expansion.

Gov. Paul LePage’s office says Medicaid expansion will offset a tax hike by decreasing charity care and bad debt. Maine’s hospital tax rate is 2.23 percent, and Rabinowitz said Maine could go up to six percent.

Maine Hospital Association lobbyist Jeffrey Austin previously told The Associated Press that Maine hospitals pay $100 million in annual taxes and would oppose an increase.

Mainers voted last fall to expand Medicaid to 80,000 low-income adults.

LePage’s administration is fighting litigation by advocates calling on the governor to stop blocking expansion. LePage vetoed legislation funding Maine’s share of expansion with surplus and tobacco settlement funds after he argued lawmakers must fund expansion without raising taxes.

The trend even includes Medicare bad debt, which results when hospitals exhaust efforts to collect from beneficiaries and must be paid back.

Hospitals continue to face financial challenges as the landscape shifts, and the challenge posed to hospitals by patient balances after insurance, or PBAI, is growing. That’s according to a new TransUnion Healthcare analysis that showed PBAI rose from 8 percent of the total bill responsibility during the first quarter of 2012 to 12.2 percent during the same quarter in 2017.

Commercially insured patients experienced a PBAI increase of 67 percent from $467 to $781, the analysis showed. The rising trend fueled an 88 percent increase in total hospital revenue attributed to PBAI over the 5-year period.

As patients take on more risk and shoulder more of their own healthcare costs, uncompensated care is also rising. TransUnion cited the American Hospital Association’s 2017 Hospital Fact Sheet, which said uncompensated care increased by $2.6 billion dollars in 2016, the first increase in three years. Rising PBAI has no doubt amplified bad debt for providers, contributing to that rise.

Jonathan Wiik, principal for healthcare strategy at TransUnion, said he expects the figure to have risen in 2017 and again in 2018.

The analysis also indicated that Medicare Bad Debt, which happens when Medicare patients don’t pay their deductibles and coinsurance, rose from $3.14 billion in 2012 to $3.69 billion in 2016, a 17 percent increase. If a hospital feels it has exhausted all efforts to get money from a Medicare beneficiary who has an outstanding copay coinsurance or deductible, and they have documented their efforts to collect, Medicare will actually pay the hospital back though not dollar-for-dollar. Wiik said Medicare pays about 65 cents on the dollar for that payback so the hospital still loses some money, about a third of the bill to be exact.

“A great example of that is a hip surgery patient that has Medicare, has a $1,000 deductible and never paid it,” Wilk said. “The hospital would have gotten $650 back but lost $350.”

The trend indicates that hospitals continue to experience reimbursement pressure that can be tied directly to the increase in how much of their own medical cost patients are now taking on

“That’s a very scary thing. For the average elective surgery the number used to be 10 percent, now it’s 30. Patients are great volume for hospitals but they are horrible payers compared to insurance companies. They cost twice as much to collect from and they take three times as long to pay. That’s an administrative burden for the hospital-cost to collect – it’s significantly higher to collect from a patient than from a insurer,” Wilk said.

To show just how much the payer landscape has shifted for hospitals, patients are now generally ranked as a top tier payer for hospitals, right after Medicare and Medicaid. Then comes PBAI and then commercial, according to Wiik. And with patients in the top of a hospital’s AR ranking, he’s seeing some clinics do deductible holds in which they delay their claim while a related hospital claim processes. They don’t send it in until the patient meets the deductible through the hospital. Once it is met then the clinic will send in their claim and get paid right away because the payer is paying, not the patient.

A big part of the problem is a huge gap in benefits literacy for patients coupled with the driving force of consumerism.

“They don’t understand the magnitude of the costs they they are going to get hit with. A relatively simple elective surgery will blow a $2,500 dollar deductible out of the water almost every time. Patients don’t realize that until it happens so hospitals should be engaging them early and putting patient-facing estimates in front of them. And it’s really not about collecting money from patients anymore it’s about getting them financing,” Wiik said.

That means proactively setting up payment plans to spread debt out over time, which protects not only the patient experience but also the hospital’s revenue. Plus it’s a more pleasant conversation to have. If patients are a higher ranking payer, hospitals should be putting into place more policies to deal with their needs and requirements, treating them like the force they are becoming.

“Imagine if you were going in for knee surgery and your hospital sent you a text that said here’s your payment plan would you like to start that now. I think a lot of patients would appreciate that. It doesn’t happen. But it should. The technology is there. You can buy groceries online now and go pick them up. It’s all billed electronically now.”

It can be hard to do estimates and set up payment plans early because medical costs cost can vary so much, but patients want that kind of experience. They put it on the hospitals to figure out how to get them a bill that is at least close to what they were expecting, and set them up to pay for it.

“They are going to go somewhere where that experience is frictionless. That’s what hospitals have to be aware of,” Wilk said. “The market is highly competitive when it comes to that type of stuff and the ones who are innovating and engaging patients are going to get those millennials and the folks that live paying their bills online.”

More than 4 million people have lost coverage in the past two years, including many lower-income adults. That could prove problematic for safety net hospitals in the near future.

The ongoing efforts to destabilize the Affordable Care Act will adversely affect the operating margins of not-for-profit healthcare providers, according to a new analysis from S&P Global.

S&P analyst Allison Bretz said that over time, “a growing uninsured population could be a credit negative for not-for-profit hospitals and health systems, as these facilities would likely see an uptick in self-pay patients, charity care and bad debt.”

Two years into the Trump administration’s efforts to roll back the ACA, the uninsured population has risen from about 12.7% in 2016 to 15.5% in 2018.

A study by The Commonwealth Fund estimates that 4 million people have lost health insurance since 2016, and that the uninsured rate among lower-income adults rose from 21% in 2016 to 25.7% this spring.

“This will be most acute at safety-net providers and other providers with a high concentration of Medicaid patients, as that population is most vulnerable to many of these changes,” Bretz said in remarks accompanying the report.

Beth Feldpush, senior vice president of policy and advocacy for America’s Essential Hospitals, said the report “underscores concerns we’ve had since last year’s attempts to repeal the ACA and, now, with piecemeal changes that have weakened the law.”

“Many of the people who lose coverage seek care at our hospitals, which adds to uncompensated costs and puts more pressure on our members’ already low operating margins,” Feldpush said. “Because essential hospitals, by their mission, turn no one away, this could prove financially unsustainable for some.

Although active efforts to repeal the ACA in Congress have slowed in the past year, it is facing one of its greatest threats, as a federal judge in Texas hears a lawsuit brought by 20 states that challenges the constitutionality of the sweeping healthcare law.

For-profit, Payer Outlook Stable

While the rising uninsured rate could prove challenging for not-for-profit providers, S&P analyst David Peknay said it should have little effect on for-profit providers.

“The for-profit companies we rate have been reporting some increase in uninsured patients, consistent with national trends, but the impact on ratings is also currently immaterial,” he said.

The losses in covered lives for health insurance companies is offset by other factors, said S&P analyst Joseph Marinucci.

“A key contributing factor is the sustained migration of the government-sponsored insurance segments toward coordinated care (Medicare Advantage and managed Medicaid), which is expanding the market opportunity for health insurers,” Marinucci said.

“We expect ratings in the insurance sector to remain relatively stable in the near term despite the growth in the number of working-age uninsured individuals,” he said.

President Trump is expected to soon address the nation about the rising cost of prescription drugs. But Americans are worried about more than drug prices. New findings from the Commonwealth Fund Affordable Care Act Tracking Survey show that consumers’ confidence in their ability to afford all their needed health care continues to decline.

Last week, we reported that the survey indicated a small but significant increase in the uninsured rate among working-age adults since 2016. In this post, we look at people’s views of the affordability of their health care. The Affordable Care Act Tracking Survey is a nationally representative telephone survey conducted by SSRS that tracks coverage rates among 19-to-64-year-olds, and has focused in particular on the experiences of adults who have gained coverage through the marketplaces and Medicaid. The latest wave of the survey was conducted between February and March 2018.1

Findings

Confidence in Ability to Afford Health Care Continues to Decline

In each wave of the survey, we’ve asked respondents whether they have confidence in their ability to afford health care if they were to become seriously ill. In 2018, 62.4 percent of adults said they were very or somewhat confident they could afford their health care, down from a high of nearly 70 percent in 2015 (Table 1). Only about half of people with incomes less than 250 percent of poverty ($30,150 for an individual) were confident they could afford care if they were to become very sick, down from 60 percent in 2015 and about 20 percentage points lower than the rate for adults with higher incomes. There were also significant declines in confidence among young adults, those ages 50 to 64, women, and people with health problems. Declines were significant among both Democrats and Republicans.

People in Employer Plans Have the Greatest Confidence in Their Insurance

We asked people with health insurance how confident they were that their current insurance will help them afford the health care they need this year. Majorities of adults were somewhat or very confident in their coverage; those with employer coverage were the most confident. More than half (55%) of adults insured through an employer were very confident their coverage would help them afford their care compared to 31 percent of adults with individual market coverage and 41 percent of people with Medicaid (Table 2). The least confident were adults enrolled in Medicare. Working-age adults enrolled in Medicare were the sickest among insured adults and the second-poorest after those covered by Medicaid (data not shown).2

One-Quarter of Adults Said Health Care Became Harder to Afford

We asked people whether, over the past year, their health care, including prescription drugs, had become harder for them to afford, easier to afford, or if there had been no change. The majority (66%) said there had been no change, one-quarter (24%) said it had become harder to afford, and 8 percent said it had become easier (Table 3). People with individual market coverage were significantly more likely than those with employer coverage or Medicaid to say health care had become harder to afford. About one-third of adults with deductibles of $1,000 or more said health care had become harder to afford, twice the share of those who had no deductible. About one-third of those enrolled in Medicare and 41 percent who were uninsured also reported that their health care had become harder to afford.

Only About Half of Americans Would Have Money to Pay for an Unexpected Medical Bill

Accidents and other medical emergencies can leave both uninsured and insured people with unexpected medical bills, which usually require prompt payment. We asked people if they would have the money to pay a $1,000 medical bill within 30 days in the case of an unexpected medical event. Nearly half (46%) said they would not have the money to cover such a bill in that time frame (Table 4). Women, people of color, people who are uninsured, those covered by Medicaid or Medicare, and those with incomes under 250 percent of poverty were among the most likely to say they couldn’t pay the bill.

Health Care Is Among People’s Top Four Greatest Personal Financial Concerns

Fourteen percent of adults said that health care was their biggest personal financial concern, after mortgage or rent (23%), student loans (17%), and retirement (17%) (Table 5). Those most likely to cite health care as their greatest financial concern were people who could potentially face high out-of-pocket costs because they were uninsured or had high-deductible health plans.

Policy Implications

Uninsured adults are the least confident in their ability to pay medical bills. But the risk of high out-of-pocket health care costs doesn’t end when someone enrolls in a health plan. The proliferation and growth of high-deductible health plans in both the individual and employer insurance markets is leaving people with unaffordable health care costs. Many adults enrolled in Medicare for reasons of disability or serious illness also report unease about their health care costs. An estimated 41 million insured adults have such high out-of-pocket costs and deductibles relative to their incomes that they are effectively underinsured. As this survey indicates, the nation’s health care cost burden is felt disproportionately by people with low and moderate incomes, people of color, and women.

The ACA’s reforms to the individual insurance market have doubled the number of people who now get insurance on that market to an estimated 17 million, with approximately half receiving subsidies through the ACA marketplaces. The ACA also has made it possible for people who were regularly denied coverage by insurers — older Americans and those with health problems — to get insurance. They are now entitled by law to an offer should they want to buy a plan.

But as this survey suggests, the ACA’s reforms did not fully resolve the individual market’s relatively higher costs for all those enrolled, compared to employer coverage or Medicaid. Moreover, recent actions by Congress and the Trump administration, including the repeal of the individual mandate penalty and loosened restrictions on plans that don’t comply with the ACA, are expected to exacerbate those costs for many. In the survey, people with individual market coverage are more likely than those with employer coverage or Medicaid to say that their health care, including prescription drugs, has become harder to afford in the past year. They express less confidence than those with employer coverage that their insurance will help them afford their care this year. As explained in the first post, there are a number of policy options that Congress can pursue that would improve individual market insurance’s affordability and cost protection. In the absence of bipartisan Congressional agreement on legislation, several states are currently pursuing their own solutions. But if current trends continue, the federal government will likely confront growing pressure to provide a national solution to America’s incipient health care affordability crisis.

HHS issued a proposed rule on Tuesday that expands the availability of short-term health insurance by allowing the purchase of plans providing coverage for up to 12 months, the latest in the Trump administration’s plans to weaken the Affordable Care Act. The action builds off a request for information by HHS last June on ways to increase affordability of health insurance.

The current maximum period for such plans is less than three months, a change made by the Obama administration in 2016. The proposed rule would mark a return to the pre-2016 era, but CMS noted that it is seeking comment on offering short-term plans for periods longer than 12 months.

Short-term plans are not required to comply with federal rules for individual health insurance under the ACA, so the plans could charge more for those with preexisting conditions and not provide what the ACA deemed essential health benefits like maternity care.

Dive Insight:

The proposed rule builds off of an executive order President Donald Trump signed in October, which instructed the federal government to explore more access to association health plans, expanding short-term limited duration plans and changes to health reimbursement arrangements or HRAs.

Consumers buying these short-terms plans could lose access to certain healthcare services and providers and experience an increase in out-of-pocket expenditures for some patients, according to the proposal.

The short-term plans “would be unlikely to include all the elements of ACA-compliant plans, such as the preexisting condition exclusion prohibition, coverage of essential health benefits without annual or lifetime dollar limits, preventive care, maternity and prescription drug coverage, rating restrictions and guaranteed renewability,” according to the proposed rule.

The Trump administration argues that expanding access to short-term plans is increasingly important due to rising premiums in the individual markets.

But if young and healthy people leave the individual market for short-term plans, it could contribute to an unbalanced risk pool. HHS itself states that the exodus of young and healthy exchange members could contribute to rising premiums within the ACA exchange markets.

“If individual market single risk pools change as a result, it would result in an increase in premiums for the individuals remaining in those risk pools,” the proposed rule stated.

But when asked about concerns that the idea might hurt the stability of the ACA marketplaces by siphoning healthy people away, CMS Administrator Seema Verma argued there would be little impact.

“No, we don’t think there’s any validity to that — based on our projections only a very small number of healthy people will shift from the individual market to these short-term limited duration plans. Specifically, we estimate that only 100,000 to 200,000 people will shift. And this shift will have will have virtually no impact on the individual market premiums,” Verma said on a press call.

But the insurance lobby cautioned that the action could increase insurance prices for the most vulnerable.

The American Hospital Association and Association for Community Affiliated Plans also slammed the short-term plans, saying they would increase the cost of comprehensive coverage.

“Short-term, limited-duration health plans have a role for consumers who experience gaps in coverage. They are not unlike the small spare tire in a car: they get the job done for short periods of time, but they have severe limitations and you’ll get in trouble if you drive too fast on them,” ACAP CEO Margaret Murray said in a statement.

“While we are reviewing the proposed rule to understand its impact on the people we serve, we remain concerned that expanded use of short-term policies could further fragment the individual market, which would lead to higher premiums for many consumers, particularly those with pre-existing conditions,” said Kristine Grow, SVP of communications at America’s Health Insurance Plans.

HHS anticipates most individuals switching from individual market plans to short-term coverage plans would be relatively young or healthy and not eligible to receive ACA’s premium tax credits.

CMS said the proposal is one to help the 28 million Americans without health insurance, pointing to the 6.7 million who chose to pay the individual mandate penalty in 2015 as evidence that ACA-compliant plans are too expensive.

“In a market that is experiencing double-digit rate increases, allowing short-term, limited-duration insurance to cover longer periods gives Americans options and could be the difference between someone getting coverage or going without coverage at all,” Verma said in a statement.

Senate HELP Committee Chair Lamar Alexander, R-Tenn., praised the action, but cautioned that states still have a responsibility to protect consumers.

“Millions of Americans who are between jobs and who pay for their own insurance will welcome this extended option for lower-cost, short-term policies. States will have the responsibility for making sure these policies benefit consumers,” Alexander said in a statement.

Democrats largely oppose the move, arguing it will further destabilize the market for millions of Americans in the ACA exchanges. “Widespread marketing of these bare bones, junk plans will further destabilize health insurance markets, and will lead to higher premiums for everyone,” a group of House Democrats said in a joint statement.

As Republicans are not likely to take up ACA repeal again any time soon, the Trump administration has been working to pare back the law in the past several months. It halved the enrollment period and stopped paying cost-sharing reduction payments to insurers. Also, the recent tax overhaul included a repeal of the law’s requirement that most people have coverage.