In breaking news that will infinitely complicate the already difficult process of attempting to resuscitate a patient, cardiopulmonary resuscitation (or CPR) will now require prior authorization.

The prevailing reaction to this news is best captured by Felicia Martin-Lowry, MD, a critical care physician at James Monroe University Hospital in Washington, as she crumbled into a burbling mess of defeat: “No … no … NOOOOOOOO!!!!”

Much like prior authorization requests for medications or other services, health care professionals will only learn about the need for a prior authorization right when CPR is initiated. The insurer will block CPR from continuing and the health care professional will need to go through the lengthy prior authorization process.

“We need to make sure that the health care team tried some other interventions before jumping straight into CPR,” explained a spokesperson for a major national health insurance company, who insisted on anonymity. “Expect us to ask questions like, did you try oxygen? Did you try IV fluids? Did you try an antibiotic? Did you try bicarb?”

The spokesperson went on to say that the checklist of questions will border on somewhere between 700 and 800 questions.

Insurance companies understand that CPR can be a life-saving measure. For that reason, if the insurer finds that all the appropriate steps were taken prior to the patient’s death, then they will be sure to expedite the prior authorization as an urgent request and make the decision on whether or not to approve CPR in no less than 14 days.

“Time is of the essence,” the spokesperson added, before reminding everyone that prior authorizations for CPR will only take place weekdays from 9 a.m. to 5 p.m.

In other news, Gomerblog has learned that insurers will soon require prior authorizations before physical exams and IV placement.

Once again, this post is from GomerBlog, a satirical site about healthcare.

Astria Health, a three-hospital health system based in Sunnyside, Wash., filed for Chapter 11 bankruptcy protection on May 6.

Astria plans to use the bankruptcy process to restructure its finances, enter into a plan of reorganization with its creditors and replace its billing company, according to TV station KIMA.

In a press release issued May 6, the health system said it is facing a significant shortfall in cash flow due to issues with the company it contracted with to manage its billing in August 2018. Astria said the unidentified company failed to process a significant number of accounts receivable, leading to a backlog of unpaid claims, according to the Yakima Herald-Republic.

“Although hospital leadership has actively managed the supply chain to ensure necessary supplies for patient care, this delay in cash collections has now become severe enough to potentially disrupt the organization’s ability to pay for crucial items in a timely matter,” Astria Health wrote in its news release, according to the Yakima Herald-Republic.

Astria said it has secured debtor in possession financing and the bankruptcy filing will not affect operations at its hospitals or clinics. They will remain open as the health system moves through the bankruptcy process.

“As one of the largest healthcare providers and employers in the Yakima Valley, we believe this step was necessary in order to protect the Valley’s hospitals and its local economies,” Astria Health President CEO John Gallagher told KIMA. “We believe it will protect and sustain the three hospitals for the future.”

Astria aims to emerge from bankruptcy by the end of 2019.

Financial challenges, including increasing costs, shaky Medicaid reimbursement, reductions in operating costs and bad debt, ranked No. 1 on the list of hospital CEO worries in 2018, according to an American College of Healthcare Executives poll.

Government mandates and patient safety and quality tied for second place in ACHE’s survey of top issues facing health systems. Workforce shortages came in third.

A little more than 350 execs responded to the survey and ranked 11 concerns their facilities faced last year. Behavioral health and addiction issues, patient satisfaction, care access, physician-hospital relations, tech, population health management and company reorganization filled in the remaining slots.

Dive Insight:

No matter which cog in the healthcare system one blames for the skyrocketing costs of healthcare (big pharma inflating the list prices of drugs; hospitals for upmarking services; insurers for leaving gaps in care resulting in surprise bills) consumers’ pocketbooks aren’t the only ones affected.

A separate American Hospital Association-backed study predicted health systems will lose $218 billion in federal payments by 2028, and private payers (whose dollars would normally help hospitals make up the difference) have been curtailing reimbursements as well.

Bad debt was another fear in the ACHE report. Uncompensated care costspeaked in 2013 at $46.4 billion and, though the figures have decreased slightly since then, hospitals shelled out $38.3 billion in 2016. Wisconsin alone was on the hook for $1.1 billion in uncompensated care in fiscal year 2017.

“The survey results indicate that leaders are working to overcome challenges of balancing limited reimbursements against the rising costs of attracting and retaining talented staff to provide that care, among other things,” ACHE president and CEO Deborah Bowen said in a statement.

Other financial concerns included competition, government funding cuts, the transition to value-based care, revenue cycle management and price transparency.

And 70% of hospital CEOs were worried about shifting CMS regulations in 2018, along with regulatory/legislative uncertainty (61%) and cost of demonstrating compliance (59%) — unsurprising, given the current administration’s track record of unpredictability.

Patient safety and quality of care was also top of mind for health system CEOs, with over half of respondents anxious about the high price of medications, involving physicians in the culture of quality and safety and getting them to reduce unnecessary tests and procedures.

Also of interest was the high rank given to addressing behavioral health and addiction issues, according to Bowen, which ranked fifth in its first year of being included in the survey. The topic has been front and center in the industry of late, in line with the increasing recognition of social determinants of health and the breakdown in silos of care.

Ranking of the issues has remained largely constant since 2016, though in 2017 more hospital CEOs were concerned about personnel shortages than patient safety and quality.

Vertical integration is all the rage in healthcare these days, with Aetna, Cigna and Humana making notable plays.

If the proposed CVS-Aetna, Cigna-Express Scripts and Humana-Kindred deals are cleared by regulators, the tie-ups will have to immediately face UnitedHealth Group’s Optum, which has been ahead of the curve for years and built out a robust pharmacy benefit manager (PBM) business already along with a care services unit, employing about 30,000 physicians and counting.

UnitedHealth formed Optum by combining existing pharmacy and care delivery services within the company in 2011. Michael Weissel, Group EVP at Optum, told Healthcare Dive the company began by focusing on three core trends in the industry: data analytics, value-based care and consumerism.

Since then, the company has been on an acquisition spree to position itself as a leader in integrated services.

“For the longest time, the market assumed that they were building the Optum business [to spin it out] and what is interesting in the evolution of the industry is that that combination has now set a trend,” Dave Windley, managing director at Jefferies, told Healthcare Dive.

“United has now set the industry standard or trend … to be more vertically integrated and it seems less likely now that United would spin this out … because many of their competitors are now mimicking their strategy by trying to buy into some of the same capabilities,” he said.

Weissel said Optum will continue to push on the three identified trends in the next three to five years, with plans to invest heavily in machine learning, AI and natural language processing.

The question will be whether and how the company can keep its edge.

What Optum is

Optum is a company within UnitedHealth Group, a parent of UnitedHealthcare. Optum’s sister company UnitedHealthcare is perhaps more well known within the industry and with consumers.

However, Optum, a venture that encompasses data analytics, a PBM and doctors,has been gradually building its clout at UnitedHealth Group.

In 2017, the unit accounted for 44% of UnitedHealth Group’s profits.

In 2011, UnitedHealth Group brought together three existing service lines under one master brand. Services are delivered through three main businesses within a business within a business:

OptumHealth – the care delivery and ambulatory care capabilities of OptumCare, as well as the care management, behavioral health, and consumer offerings of Optum;

OptumInsight – the data and analytics, technology services and health care operations business; and

OptumRx – its pharmacy benefit service.

The company focuses on five core capabilities, including data and analytics, pharmacy care services, population health, healthcare delivery and healthcare operations. Services include but are certainly not limited to OptumLabs (research), OptumIQ (data analytics), Optum360 (revenue cycle management), OptumBank (health savings account) and OptumCare (care delivery services).

The Eden Prairie, MN-headquartered company has recently expanded its care delivery services, with much of the growth coming from acquisitions. The past two years have seen Optum expand its footprint into surgical care (Surgical Care Affiliates), urgent care (MedExpress) and primary care (DaVita Medical Group).

It’s a wide pool, but the strategy affords UnitedHealth the opportunity to grab more revenue by expanding its market presence. For example, the DaVita acquisition, which is still pending, allows OptumCare to operate in 35 of 75 local care delivery markets the company has targeted for development, Andrew Hayek, OptumHealth CEO, said on an earnings call in January.

Optum’s strategy of meeting patients where they are and deploying more ambulatory, preventative care services works in concert with its sister company UnitedHealthcare’s goal of reducing high-cost, unnecessary care services, when applicable. If Optum succeeds in creating healthier populations that use lower levels of care more often, that benefits the parent company UnitedHealth Group as UnitedHealthcare spends less money and time on claims processing/payout.

The strategy has been paying off so far.

Three charts that show UnitedHealth’s financial health as it relates to Optum

Optum’s presence has grown as it has steadily increased its percentage of profits for UnitedHealth Group.

Credit: Healthcare Dive / Jeff Byers

In 2011, the first year Optum was configured as it looks today, the company contributed 14.8% of total earnings through operations to UnitedHealth Group with $1.26 billion. That’s about 29 percentage points lower than in 2017, when Optum brought in $6.7 billion in profits on $83.6 billion in revenue.

Broken down, it’s clear that pharmacy services make up the lion’s share of the company’s revenue. In 2017, OptumRx earned $63.8 billion in revenue, fulfilling 1.3 billion prescriptions. OptumRx’s contributions to the company took off in 2015 when Optum acquired pharmacy benefit manager Catamaran.

Credit: Healthcare Dive / Jeff Byers

In recent years, OptumHealth has grown due to expansion in care delivery services, including consumer engagement and behavioral and population health management. The care delivery arm served 91 million people last year, up from 60 million in 2011.

OptumInsight has grown largely due to an increase in revenue cycle management and operations services in recent years.

On Wall Street, UnitedHealth Group is performing well and has seen healthy growth since 2008. The stock peaked in January and took a dive when Amazon, J.P. Morgan and Berkshire Hathaway — industry outsiders yet financial giants — announced they would create a healthcare company.

Credit: Healthcare Dive / Jeff Byers

While these charts suggest a dominant force, the stock activity shows that investors believe there’s still more room for competition, if the new entrants play their cards right.

Where Optum could lock out and rivals could cut in on competition

UnitedHealth started down this strategic path many years ago and the rest of the industry just now seems to be catching up.

“Optum’s been the leader in showing how a managed care organization with an ambulatory care delivery platform and a pharmacy benefit manager all in house can lower or maintain and bend cost trend and then drive better market share gains in their health insurance business,” Ana Gupte, managing director of healthcare services at Leerink, told Healthcare Dive. “I think they have been the impetus in the large space for the Aetna-CVS deal.”

Because the company is multi-dimensional, Optum’s competition will be varied. If all the mergers making news — including the Walmart’s rumored buyout of Humana — close, here’s what competition could look like:

Perhaps oddly, its largest revenue contributor, OptumRx, seems to have the largest vulnerability for competition in the coming years.

Optum’s competitive advantage in the PBM space is driven largely by already realized integration. Merging data across IT systems is no easy task, and Optum has spent years harmonizing pharmacy data across platforms to assist care managers in OptumCare to see medical records for United members.

Anyone with experience implementing EHR systems can tell you such integration doesn’t happen over night.

If the Cigna-Express Scripts deal closes, the equity can compete with OptumRx, but the technology investment needed to harmonize data and embed Cigna’s service and pharmacy information into Express Scripts servers will take time, Windley said. Optum, on the other hand, has invested in the effort and integration for years.

Gupte says the encroaching organizations in the PBM space have the ability to realize the efficiencies and savings and the integrated medical that Optum has been realizing across OptumRx and the managed care organization.

Optum’s leg up in PBM space could last two to three years over the competition, she said.

On the care delivery side, OptumHealth has been purchasing large physician groups for a variety of services. There are only so many large physician groups putting themselves on the market, and Optum has been making bids for them.

There’s still a bit of white space to fill in its 75 target markets, but analysts note Optum may have the competition on lock in this space

Even if CVS-Aetna closes, OptumCare is a $12 billion business with many urgent and surgery care access points. If CVS-Aetna is finalized, the company will have about 1,100 MinuteClinics capable of realizing efficiencies with Aetna, but, as Windley notes, they likely won’t have primary care or surgery care elements.

There’s also a lot of time and capital needed for building out and retrofitting retail space to medical areas.

On the surgical care services, “I don’t see either Cigna, Aetna or Humana getting into that business,” Gupte said. “That will be one element of their footprint on care delivery that will be unique and differentiated for them.”

Urgent care has the potential for outsider competition, she added. However, Optum is using its MedExpress business to treat higher acuity conditions and have an ER doctor on staff in each center. Compared to the typical types of conditions treated in retail clinics or those that would be feasible over time, Gupte believes services that could be seen in CVS or Walmart would be lower acuity, chronic care management services.

“[Optum has] been so proactive and so strategic I don’t think there’s going to be a lot of reactive catchup they have to do,” Gupte said. “I think it’s going to be hard for the other entities to play catch up, outside of the PBM.”

One potential issue will be harmonizing the disparate businesses so patients can be effectively managed across the various organizations, Trevor Price, founder and CEO of Oxean Partners, told Healthcare Dive.

“I think the biggest challenge for Optum is operationalizing the combined platform,” Price said. “The biggest question is do they continue to operate as individual businesses or do they merge into one.”

What’s next?

Optum will continue to explore ground in the three core trends it has identified.

Out of the three, consumerism has the longest path to maturity in healthcare, Weissel said, adding he believes consumerism is going to change healthcare more than any other trend over the next decade.

“There is a wave coming, and this expectation that we will move there,” he said. “Increasingly, this aging of people who become very comfortable in a different modality is going to tip the balance with how people will want to interact with healthcare. I know there’s pent up demand already.”

That means the company is putting bets into the marketplace around consumer building and segmentation models as well as thinking about how to connect data to allow patients to schedule appointments, view health records, sign up for insurance, search for providers or renew prescriptions online.

Consumer-centric projects currently underway include digital weight loss programs — including streaming fitness classes — and maternity programs to track pregnancy. The company is also experimenting with remote patient monitoring to understand the impacts on those with heart disease or asthma and to search for service opportunities.

Optum will pursue investments as well as acquisitions to push into the consumer space.

“When it comes to acquisitions to Optum overall, we’re always in the marketplace looking to extend our capabilities, to extend our reach in the care management space to fill in holes or gaps that we have,” Weissel said. “That’s a constant process in our enterprise.”

According to the DOJ, this is the ninth consecutive year that the organizations’ civil healthcare fraud settlements and judgments have exceeded $2 billion.

As part of the federal government’s increasing focus on issues of healthcare fraud, particularly in the Medicare space, the U.S. Department of Justice recovered $2.5 billion in settlements and judgments from False Claims Act Cases over the past year.

According to the DOJ, this is the ninth consecutive year that the organizations’ civil health care fraud settlements and judgments have exceeded $2 billion.

While the $2.5 billion number represents federal losses, the DOJ also said it also helped recover significant funds for state Medicaid programs

“Every year, the submission of false claims to the government cheats the American taxpayer out of billions of dollars,” Principal Deputy Associate Attorney General Jesse Panuccio said in a statement.

“In some cases, unscrupulous actors undermine federal healthcare programs or circumvent safeguards meant to protect the public health … The nearly three billion dollars recovered by the Civil Division represents the Department’s continued commitment to fighting fraudsters and cheats on behalf of the American taxpayer.”

The False Claims Act has its roots in groups trying to defraud the military during and after the Civil War and was significantly strengthened since 1986 when Congress increased incentives for whistleblowers to file lawsuits alleging false claims.

In healthcare, organizations across the industry were hit with False Claims cases including drug companies, medical device manufacturers, payer organizations and healthcare providers.

The single largest recovery over the past year was a $625 million settlement paid by drug wholesaler AmerisourceBergen to resolve a number of claims including that the company illegally repackaged injectable cancer drugs into pre-filled syringes and billing multiple doctors for individual drug vials.

The DOJ also brought cases against drug companies who increased drug prices by funding Medicare co-payments meant to serve as a check on healthcare costs.

One major case against Massachusetts-based medical device company Alere resulted in a $33.2 million settlement over allegations that it sold unreliable diagnostic devices meant to detect acute coronary syndromes, heart failure, drug overdose and other serious conditions.

When it comes to health plans, the government’s case against UnitedHealth Group over allegations that it knowingly obtained inflated risk adjustment payments for its Medicare Advantage beneficiaries is still ongoing.

Allentown, Pa.-based Coordinated Health and its founder and CEO Emil DiIorio, MD, have entered into an agreement with the federal government to settle False Claims Act allegations, according to the Department of Justice.

The settlement resolves allegations that Coordinated Health inflated payments from federal payers by unbundling claims for reimbursement for orthopedic surgeries, including many for total joint replacement, from 2007 through mid-2014.

Instead of stopping the illegal unbundling, Dr. DiIorio changed how he wrote operative reports to enable Coordinated Health billers to maximize improperly unbundled reimbursements, according to the Justice Department.

Two outside coding consultants identified the improper unbundling during audits in 2011 and 2013 and told top Coordinated Health executives about the problem. “Motivated by its bottom line, Coordinated Health simply ignored the consultants’ recommendations and continued abusing Modifier 59 to improperly unbundle orthopedic surgery claims until mid-2014,” states a Justice Department press release.

Coordinated Health will pay $11.25 million and Dr. DiIorio will pay $1.25 million to settle the allegations. In addition to the monetary settlement, Coordinated Health entered into a corporate integrity agreement with HHS that will require monitoring of its billing practices for five years.

Regarding the settlement, Coordinated Health released the following statement: “We are pleased to have come to a resolution with the federal government regarding allegations of our past use of a specific Medicare billing modifier, involving a complex Centers for Medicare and Medicaid Services rule, which does not relate to the quality of patient care. We have already updated our billing practice to resolve the issue in question, and have taken a number of decisive actions to reduce the potential for issues in the future. Our focus has been and always will be providing the best possible patient care in the communities we serve.”

Without a workable revenue cycle management system, 82 percent of the hospitals plan to go blind with value-based reimbursement and 85 percent may seek consulting services.

Approximately one-quarter of US hospitals (26 percent) do not have an effective healthcare revenue cycle management solution in place, according to a new Black Book survey.

Black Book surveyed over 4,640 individuals from 522 hospitals and healthcare delivery networks on their use of 165 revenue cycle management technology services and solutions. The survey showed that revenue cycle management improvement is happening, but a significant portion of hospitals still do not have workable solutions.

While 26 percent of hospitals do not have a plan to optimize or replace legacy revenue cycle management systems, the proportion of hospitals without a transition plan is down compared to six years ago. In 2012, 35 percent of all hospitals did not have a revenue cycle management strategy in place to improve or replace their solutions.

The most recent survey results show that about 400 hospitals implemented a viable, effective revenue cycle management optimization or replacement plans over the past six years.

However, the opportunity to improve healthcare revenue cycle management remains. Of the 1,600 hospitals without a revenue cycle management optimization plan, about 82 percent expect to make value-based reimbursement decisions in 2019 without the use of an advanced software or outsourced partner, the survey showed.

Value-based reimbursement is overtaking the traditional fee-for-service system. The proportion of healthcare payments tied to an alternative payment model is rising, reaching 29 percent of healthcare payments by 2016, the Health Care Payment Learning and Action Network (LAN) recently reported.

The number of payments linked to value-based reimbursement is only going to increase as private and public payers implement alternative payment models to lower costs and improve care quality. And hospitals will be expected to take on the clinical and financial risks associated with the models.

Effective revenue cycle management solutions can help hospitals make the transition to value-based reimbursement.

“What providers absolutely must have are really powerful analytics that are able to take clinical and outcomes data, a lot of which resides in clinical systems, and combine it with financial data to accurately measure where we improve quality based on outcomes results,” Deanna Kasim, Research Director of Payer Health IT at IDC Health Insights, toldRevCycleIntelligence.com.

“There is an absolute need that if this is going to be successful in terms of changing reimbursements and care delivery models, payers need to get providers and the consumers to the table and there has to be the next generation of analytics applications to support these efforts.”

Without a viable, effective revenue cycle management solution, hospitals could lose revenue during the transition to value-based reimbursement.

In light of the challenge, 85 percent of Black Book respondents said they would partner with a revenue cycle management consultant or advisory company for short-term direction.

For the long-term, however, hospitals will need to partner with a third-party vendor to implement an optimized revenue cycle management solution that can deliver value-based reimbursement results.

Black Book explained that hospitals can invest in core, platform, and/or point solutions, which cover enterprise-wide functions. Or hospitals can implement bolt-on solutions that automate specific components of the healthcare revenue cycle.

At this stage in the market, hospitals are currently turning to bolt-on solutions to complement their legacy financial and clinical systems. About 45 percent of large and community hospitals in a recent Black Book survey plan to use multiple bolt-on solutions for revenue cycle management in 2019.

Few hospitals expect to use one core legacy vendor for a software solution. Only 23 percent of small hospital staff, 15 percent of community hospital staff, and 17 percent of large hospital staff stated that relying on a core solution was their organization’s revenue cycle management strategy for 2019.

Hospitals are investing in more bolt-on solutions versus core software because of staffing concerns, Black Book reported in the most recent survey. The five-month polling process revealed that staffing concerns were the top challenge hospitals faced with implementing new revenue cycle management solutions or improving legacy software.

Finding skilled revenue cycle management human resources for new solutions was a major obstacle to optimizing or replacing legacy systems. Therefore, outsourcing core functions or implementing bolt-on services was a short-term alternative, hospitals leaders said.

“If hospitals are to maximize revenue and reduce claims take-backs, it is imperative that those still behind the curve find a way to dedicate appropriate resources toward implementing an effective RCM system,” the market research firm concluded.

West Reading, Pa.-based Tower Health reduced charges by an average of 30 percent at nearly all of its hospitals after reviewing a third-party report on costs at other regional hospitals, according to WFMZ.

The cost reductions affect a wide array of services, procedures, tests and medications at Tower’s hospitals in Brandywine, Chestunt Chestnut Hill, Jennersville, Phoenixville and Pottstown, all in Pennsylvania. They went into effect Dec. 1.

The prices at Reading (Pa.) Hospital will not change, as the independent report found that its charges were already in line with local competitors.

Highlighting a key implication of the rise in high-deductible health plans, both on the ACA exchanges and in employer-sponsored insurance, the article describes a question now commonly faced by doctors and hospitals—how best to collect their patients’ portion of the fees they charge? As one Texas doctor tells Bloomberg, reflecting the experience of the Maldonados from the other side of the equation, “If [patients] have to decide if they’re going to pay their rent or the rest of our bill, they’re definitely paying their rent.” He reports that the number of people dodging his calls to discuss payment has increased “tremendously” since the passage of the ACA. Another Texas doctor reports that his small practice had to add an additional full-time staff member just to collect money owed by patients, adding further overhead to his practice’s costs and making it more likely that he, like many other doctors, will eventually seek shelter by being employed by a larger delivery organization. That trend, as has been repeatedly shown, further increases the cost of care, exacerbating the increase in insurance costs for families like the Maldonados. This Gordian knot of increasing costs, rising deductibles, and growing premiums has left us with a healthcare system that’s forcing difficult decisions at every turn, for patients and providers.

Physicians, hospitals and medical labs are grappling with the rise in high-deductible insurance.

Doctors, hospitals and medical labs used to be concerned about patients who didn’t have insurance not paying their bills. Now they’re scrambling to get paid by the ones who do have insurance.

For more than a decade, insurers and employers have been shifting the cost of care onto their workers and customers, tamping down premiums by raising patients’ out-of-pocket costs. Last year, almost half of privately insured Americans under age 65 had annual deductibles ranging from $1,300 to as high as $6,550, government data show.

Now, instead of getting paid by insurance companies on a predictable schedule, health-care providers have to engage in an awkward dance. One moment they’re removing a pre-cancerous skin mole. The next, they’re haranguing patients to pay what’s become a growing portion of the total medical bill.

“It’s harder to collect from the patient than it is from the insurance,” said Amy Derick, a doctor who heads a dermatology practice outside Chicago. “If the plans change to a higher deductible, it’s harder to get the patients to pay.”

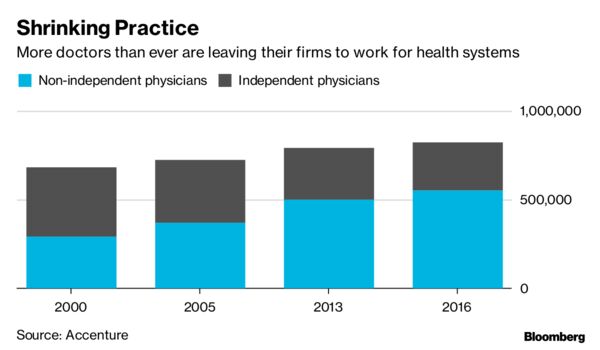

Independent physicians cited reimbursement pressures as their biggest concern for staying in business, according to a report by Accenture Plc in 2015.

“If they have to decide if they’re going to pay their rent or the rest of our bill, they’re definitely paying their rent,” said Gerald “Ray” Callas, president of the Texas Society of Anesthesiologists, whose Beaumont, Texas, practice treats about 40,000 people annually. “We try to work with the patient, but on the other hand, we can’t do it for free because we still maintain a small business.”

Accenture

In 2016, Callas introduced payment options that allow patients with expensive plans to pay a portion of the bill upfront or on a monthly basis over several years. Even so, Callas said the number of people avoiding his calls after surgery has increased “tremendously” each year since the Affordable Care Act passed in 2010.

Derick instituted a “time-out” option a few years back that gives patients the billing codes before a procedure, allowing them to call their insurance companies for estimates. Even with the program, collection rates are slower, especially at the beginning of the year when insurance plan deductibles reset.

Even large medical companies with national operations are facing the problem. Quest Diagnostics Inc., the lab-testing giant, said 20 percent of services billed to patients in the third quarter of this year went unpaid, costing the company about $80 million in lost revenue.

“We certainly have a high bad-debt rate for the uninsured,” Chief Financial Officer Mark Guinan said in a telephone interview. “But really the biggest driver is people with insurance. It’s their coinsurance and their high deductibles, and they don’t always pay their bills.”

Another testing company, Laboratory Corp. of America Holdings, reported its first year-over-year uptick in unpaid bills in the first quarter of 2016. At the time, Chief Executive Officer David King said high-deductible plans, higher copays and greater incidences of non-covered services led to more dollars being shifted to patients. LabCorp declined requests for comment.

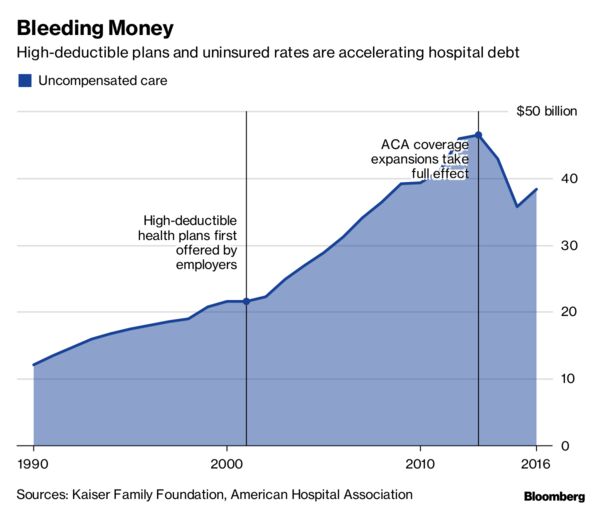

Northwell Healthcare Inc., a network of more than 700 hospitals and outpatient facilities, lost $106.9 million to unpaid services in 2015. Others have reported the same: Acute-care and critical-access hospitals reported$55.9 billion in bad debt for 2015, according to data compiled by the American Hospital Directory Inc.

“High-deductible plans have had a very big impact,” said Richard Miller, Northwell’s chief business strategy officer.

Kaiser Family Foundation, American Hospital Association

When it comes to reimbursement, a common denominator across the health-care industry is the archaic process through which bills are processed — a web of medical records, billing systems, health insurers and contractors.

High deductibles only add to the red tape. Providers don’t have real-time, fully accurate information on patient deductibles, which fluctuate based on how much has already been paid. That forces providers to constantly reach out to insurance companies for estimates.

Tarek Fakhouri, a Texas surgeon specializing in skin cancer, had to hire an additional staff member just to reason through bills with patients and their insurers, a big expense for an office of six or seven employees. About 10 percent of Fakhouri’s patients need payment plans, delay their skin-cancer surgeries until they’ve met their deductibles, or have to choose an alternative treatment.

According to a study earlier this year by the Journal of American Medical Association, primary-care physicians at academic health-care systems lose about 15 percent of their revenue to billing activities like calling insurance companies for estimates.

“It’s an unnecessary added cost to the health-care system to have to hire staff just to sit there on hold with insurance companies to find out what a patient’s deductible status is,” said Fakhouri.

Callas, Derick, and Fakhouri said they all know physicians who have left private practice altogether, some for the sole purpose of ending their dual roles as bill collectors. According to a study by the American Medical Association, less than half of doctors were self-employed as of 2016 — the lowest total ever. Many left their own practices in favor of hospitals and large physician groups with more resources.

To cope with the challenge, labs and hospitals are investing millions in programs designed to help patients understand what they owe at the point of care. Northwell has been implementing call centers and facilities where patients can ask questions about their bills.

“There’s a burden on both sides,” said Callas. “But health-care providers get caught in the middle.”