The hospital had already transferred out most of its patients and lost half its staff when the CEO called a meeting to take inventory of what was left. Employees crammed into Tina Steele’s office at Fairfax Community Hospital, where the air conditioning was no longer working and the computer software had just been shut off for nonpayment.

“I want to start with good news,” Steele said, and she told them a food bank would make deliveries to the hospital and Dollar General would donate office supplies.

“So how desperate are we?” one employee asked. “How much money do we have in the bank?”

“Somewhere around $12,000,” Steele said.

“And how long will that last us?”

“Under normal circumstances?” Steele asked. She looked down at a chart on her desk and ran calculations in her head. “Probably a few hours,” she said. “Maybe a day at most.”

The staff had been fending off closure hour by hour for the past several months, ever since debt for the 15-bed hospital surpassed $1 million and its outside ownership group entered into bankruptcy, beginning a crisis in Fairfax that is becoming familiar across much of rural America. More than 100 of the country’s remote hospitals have gone broke and then closed in the past decade, turning some of the most impoverished parts of the United States into what experts now call “health-hazard zones,” and Fairfax was on the verge of becoming the latest. The emergency room was down to its final four tanks of oxygen. The nursing staff was out of basic supplies such as snakebite antivenin and strep tests. Hospital employees had not received paychecks for the past 11 weeks and counting.

The only reason the hospital had been able to stay open at all was that about 30 employees continued showing up to work without pay, increasing their hours to fill empty shifts and essentially donating time to the hospital, understanding what was at stake. Some of them had been born or had given birth at Fairfax Community. Several others had been stabilized and treated in the emergency room after heart attacks or accidents. There was no other hospital within 30 miles of two-lane roads and prairie in sprawling Osage County, which meant Fairfax Community was the only lifeline in a part of the country that increasingly needed rescuing.

“If we aren’t open, where do these people go?” asked a physician assistant, thinking about the dozens of patients he treated each month in the ER, including some in critical condition after drug overdoses, falls from horses, oil field disasters or car crashes.

“They’ll go to the cemetery,” another employee said. “If we’re not here, these people don’t have time. They’ll die along with this hospital.”

“We have no supplies,” Steele said. “We have nothing. How much longer can we provide quality care?”

As emergencies rise across rural America, a hospital fights for its lifeAs emergencies rise across rural America, a hospital fights for its life

From reimbursement landscape challenges to dwindling patient volumes, many factors lead hospitals to file for bankruptcy.

Here are 12 hospitals that filed for bankruptcy since Jan. 1, beginning with the most recent:

1. De Queen (Ark.) Medical Center filed for Chapter 11 bankruptcy on April 3. The hospital, owned by an affiliate of Kansas City, Mo.-based EmpowerHMS, entered bankruptcy after facing financial challenges for months. Electricity was temporarily shut off in some parts of the hospital in February due to nonpayment, and the hospital subsequently stopped providing patient care.

2. Prague (Okla.) Community Hospital, owned by an affiliate of EmpowerHMS, entered Chapter 11 bankruptcy on March 21. A judge allowed a new company to take over management of Prague Community Hospital in early March after the hospital experienced payroll issues and lacked funds for supplies.

3. I-70 Community Hospital in Sweet Springs, Mo., filed for Chapter 11 bankruptcy on March 21. The bankruptcy filing came after CMS ended its provider agreement with the hospital, which voluntarily suspended its license for 90 days on Feb. 15. I-70 Community Hospital is owned by an affiliate of EmpowerHMS.

4. Haskell County Community Hospital in Stigler, Okla., filed for Chapter 11 bankruptcy on March 17. The hospital, owned by an affiliate of EmpowerHMS, entered bankruptcy with less than $50,000 in assets and at least $1 million in liabilities.

5. Drumright (Okla.) Regional Hospital, owned by an affiliate of EmpowerHMS, filed for Chapter 11 bankruptcy on March 17. The hospital entered bankruptcy with less than $50,000 in assets and upward of $10 million in estimated liabilities.

6. Oswego (Kan.) Community Hospital entered Chapter 11 bankruptcy on March 17. The bankruptcy filing came after the hospital, owned by an affiliate of EmpowerHMS, abruptly closed Feb. 14.

7. Fairfax (Okla.) Community Hospital, owned by an affiliate of EmpowerHMS, filed for Chapter 11 bankruptcy March 17. The hospital entered bankruptcy with less than $50,000 in assets and at least $1 million in liabilities.

8. Horton (Kan.) Community Hospital entered Chapter 11 bankruptcy March 14, just two days after it closed. In its bankruptcy petition, the hospital said it has less than $50,000 in assets and liabilities of between $1 million and $10 million. Horton Community Hospital is owned by an affiliate of EmpowerHMS.

9. Hillsboro (Kan.) Community Hospital, owned by an affiliate of EmpowerHMS, filed for Chapter 11 bankruptcy on March 13. According to documents filed in the bankruptcy case, the hospital has at least $10 million in assets and at least $10 million in liabilities. The hospital owes more than $334,000 in real estate taxes, making the Marion County (Kan.) Treasurer the unsecured creditor with the largest claim against the hospital.

10. Lauderdale Community Hospital in Ripley, Tenn., filed for Chapter 11 bankruptcy on March 8. The hospital, owned by an affiliate of EmpowerHMS, has faced financial challenges for months, and a federal judge appointed a receiver to oversee the hospital’s finances in February.

11. Washington County Hospital in Plymouth, N.C., entered bankruptcy in February after creditors filed an involuntary Chapter 7 bankruptcy petition. The hospital, owned by an affiliate of EmpowerHMS, missed payroll Feb. 8 and suspended all medical services Feb. 14.

12. Penobscot Valley Hospital, a 25-bed critical access hospital in Lincoln, Maine, filed for Chapter 11 bankruptcy Jan. 29. “We have made tremendous strides over the last three years in bringing our operational costs in line with revenue,” Hospital CEO Crystal Landry said in a press release. “Legacy debt is the issue here, and Chapter 11 allows us to restructure that debt so we can keep our doors open and ensure that our community continues to have a hospital close to home.”

It’s staggering to think of the challenges that CAHs face. Now OIG is calling for a re-examination of a program that it says has overpaid CAHs billions of dollars to provide skilled nursing services using hospital swing beds.

They’re called “Critical Access Hospitals” for a reason. These tiny healthcare outposts provide “critical access” to people who live in remote areas.

That was the intent of the legislation that created CAHs in 1997 at a time when rural hospitals were shuttering at an alarming rate. Congress understood that rural America needed extra Medicare dollars to keep the doors open at hospitals that serve an older, sicker and poorer patient mix.

It’s staggering to think of the challenges that CAHs face:

Because of their location and size, CAHs have few economies of scale, little leverage with vendors or payers, or a sufficiently large patient mix or volume of commercial payers to help cover costs.

CAHs are often limited in their ability to provide some of the more lucrative services that are cash cows for larger hospitals in urban areas.

Recruiting clinicians to rural areas is a slog.

And because of all those challenges, it’s also more difficult to merge or collaborate with other healthcare providers from such an isolated perch. It’s surprising to learn that only 40% of CAHs operate in the red.

Unfortunately, some people in Washington, DC have short institutional memories.

For the past couple of years, reports from the Office of the Inspector General at the Department of Health and Human Services have made it clear that they believe the CAH designation and funding scheme should be overhauled.

In its latest shot across the bow, OIG this week called for a re-examination of the swing bed program that allows CAHs to provide long-term care. The OIG audit claimed that the federal government has overpaid CAHs $4.1 billion over the past six years for services that could have cost less in relatively nearby skilled nursing and long-term care facilities.

Tavenner Pushes Back

Rural healthcare advocates rallied around the reply to the OIG recommendations from former Centers for Medicare & Medicaid Services Administrator Marilyn Tavenner, who challenged the OIG findings and recommendations in her formal response, and suggested that auditors don’t understand healthcare delivery in rural areas.

In that same response to OIG, however, Tavenner said the Obama 2016 budget has called for reducing the Medicare reimbursement that CAHs receive from 101% to 100% of allowable costs, and reassessing and eliminating CAH status for hospitals that are within 10 miles each other.

Highlighting a key implication of the rise in high-deductible health plans, both on the ACA exchanges and in employer-sponsored insurance, the article describes a question now commonly faced by doctors and hospitals—how best to collect their patients’ portion of the fees they charge? As one Texas doctor tells Bloomberg, reflecting the experience of the Maldonados from the other side of the equation, “If [patients] have to decide if they’re going to pay their rent or the rest of our bill, they’re definitely paying their rent.” He reports that the number of people dodging his calls to discuss payment has increased “tremendously” since the passage of the ACA. Another Texas doctor reports that his small practice had to add an additional full-time staff member just to collect money owed by patients, adding further overhead to his practice’s costs and making it more likely that he, like many other doctors, will eventually seek shelter by being employed by a larger delivery organization. That trend, as has been repeatedly shown, further increases the cost of care, exacerbating the increase in insurance costs for families like the Maldonados. This Gordian knot of increasing costs, rising deductibles, and growing premiums has left us with a healthcare system that’s forcing difficult decisions at every turn, for patients and providers.

Physicians, hospitals and medical labs are grappling with the rise in high-deductible insurance.

Doctors, hospitals and medical labs used to be concerned about patients who didn’t have insurance not paying their bills. Now they’re scrambling to get paid by the ones who do have insurance.

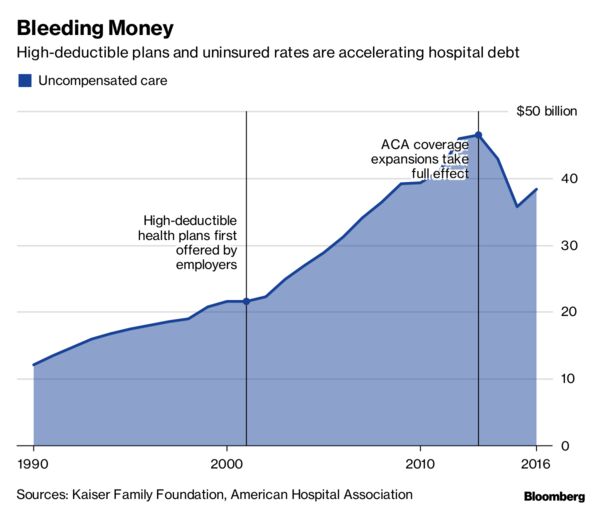

For more than a decade, insurers and employers have been shifting the cost of care onto their workers and customers, tamping down premiums by raising patients’ out-of-pocket costs. Last year, almost half of privately insured Americans under age 65 had annual deductibles ranging from $1,300 to as high as $6,550, government data show.

Now, instead of getting paid by insurance companies on a predictable schedule, health-care providers have to engage in an awkward dance. One moment they’re removing a pre-cancerous skin mole. The next, they’re haranguing patients to pay what’s become a growing portion of the total medical bill.

“It’s harder to collect from the patient than it is from the insurance,” said Amy Derick, a doctor who heads a dermatology practice outside Chicago. “If the plans change to a higher deductible, it’s harder to get the patients to pay.”

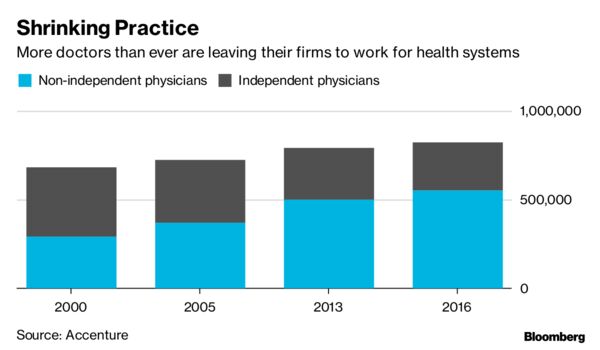

Independent physicians cited reimbursement pressures as their biggest concern for staying in business, according to a report by Accenture Plc in 2015.

“If they have to decide if they’re going to pay their rent or the rest of our bill, they’re definitely paying their rent,” said Gerald “Ray” Callas, president of the Texas Society of Anesthesiologists, whose Beaumont, Texas, practice treats about 40,000 people annually. “We try to work with the patient, but on the other hand, we can’t do it for free because we still maintain a small business.”

Accenture

In 2016, Callas introduced payment options that allow patients with expensive plans to pay a portion of the bill upfront or on a monthly basis over several years. Even so, Callas said the number of people avoiding his calls after surgery has increased “tremendously” each year since the Affordable Care Act passed in 2010.

Derick instituted a “time-out” option a few years back that gives patients the billing codes before a procedure, allowing them to call their insurance companies for estimates. Even with the program, collection rates are slower, especially at the beginning of the year when insurance plan deductibles reset.

Even large medical companies with national operations are facing the problem. Quest Diagnostics Inc., the lab-testing giant, said 20 percent of services billed to patients in the third quarter of this year went unpaid, costing the company about $80 million in lost revenue.

“We certainly have a high bad-debt rate for the uninsured,” Chief Financial Officer Mark Guinan said in a telephone interview. “But really the biggest driver is people with insurance. It’s their coinsurance and their high deductibles, and they don’t always pay their bills.”

Another testing company, Laboratory Corp. of America Holdings, reported its first year-over-year uptick in unpaid bills in the first quarter of 2016. At the time, Chief Executive Officer David King said high-deductible plans, higher copays and greater incidences of non-covered services led to more dollars being shifted to patients. LabCorp declined requests for comment.

Northwell Healthcare Inc., a network of more than 700 hospitals and outpatient facilities, lost $106.9 million to unpaid services in 2015. Others have reported the same: Acute-care and critical-access hospitals reported$55.9 billion in bad debt for 2015, according to data compiled by the American Hospital Directory Inc.

“High-deductible plans have had a very big impact,” said Richard Miller, Northwell’s chief business strategy officer.

Kaiser Family Foundation, American Hospital Association

When it comes to reimbursement, a common denominator across the health-care industry is the archaic process through which bills are processed — a web of medical records, billing systems, health insurers and contractors.

High deductibles only add to the red tape. Providers don’t have real-time, fully accurate information on patient deductibles, which fluctuate based on how much has already been paid. That forces providers to constantly reach out to insurance companies for estimates.

Tarek Fakhouri, a Texas surgeon specializing in skin cancer, had to hire an additional staff member just to reason through bills with patients and their insurers, a big expense for an office of six or seven employees. About 10 percent of Fakhouri’s patients need payment plans, delay their skin-cancer surgeries until they’ve met their deductibles, or have to choose an alternative treatment.

According to a study earlier this year by the Journal of American Medical Association, primary-care physicians at academic health-care systems lose about 15 percent of their revenue to billing activities like calling insurance companies for estimates.

“It’s an unnecessary added cost to the health-care system to have to hire staff just to sit there on hold with insurance companies to find out what a patient’s deductible status is,” said Fakhouri.

Callas, Derick, and Fakhouri said they all know physicians who have left private practice altogether, some for the sole purpose of ending their dual roles as bill collectors. According to a study by the American Medical Association, less than half of doctors were self-employed as of 2016 — the lowest total ever. Many left their own practices in favor of hospitals and large physician groups with more resources.

To cope with the challenge, labs and hospitals are investing millions in programs designed to help patients understand what they owe at the point of care. Northwell has been implementing call centers and facilities where patients can ask questions about their bills.

“There’s a burden on both sides,” said Callas. “But health-care providers get caught in the middle.”

Hospitals across the U.S. are being battered by financial headwinds, and rural hospitals are vulnerable because they don’t have capital or diversified services to fall back on when the going gets rough. Between 2013 and 2017, 64 rural hospitals closed due to financial distress and changing healthcare dynamics, more than twice the number in the previous five years, a new Government Accountability Office analysis shows.

Rural hospital closures disproportionately occurred in the South, among for-profit hospitals and among organizations with a Medicare-dependent hospital payment designation.

One potential lifeline was Medicaid expansion. According to GAO, just 17% of rural hospital closures occurred in states that had expanded Medicaid as of April 2018.

Dive Insight:

Declining inpatient admissions and reimbursement cuts have taken a toll on rural hospitals. Since 2010, 86 rural hospitals have closed, and 44% of those remaining are operating at a loss — up from 40% in 2017.

CMS Administrator Seema Verma released a rural health strategy in May aimed at improving access and quality of care in rural communities. Among its objectives are expanding telemedicine, empowering patients in rural areas to take responsibility for their health and leveraging partnerships to advance rural health goals.

The agency also expanded its Rural Community Hospital Demonstration from 17 to 30 hospitals. The program reimburses hospitals for the actual cost of inpatient services rather than standard Medicare rate, which could be as little as 80% of actual cost.

Such initiatives can be helpful, but if a hospital can’t make ends meet on its Medicare and Medicaid businesses and has only a modicum of privately insured patients, “that’s just not a balance that works financially,” Diane Calmus, government affairs and policy manager at the National Rural Health Association, told Healthcare Dive recently.

In all, 49 rural hospitals closed in the South, or 77% of rural hospital closures from 2013 through 2017, according to GAO. Texas had the most closures with 14, followed by Tennessee with eight and Georgia and Mississippi, each with five. By contrast, there were eight rural hospital closures in the Midwest and four each in the West and Northeast.

GAO also looked at closures by Medicare rural hospital payment designation. Critical access hospitals made up 36% of rural hospital closures, 30% were hospitals receiving Medicare standard inpatient payment, 25% had Medicare-dependent hospital designation and 9% were sole community hospitals.

To aid rural hospitals and ensure access for patients, NRHA has urged CMS to adopt a common sense approach to the “exclusive use” standard and lobbied lawmakers to pass legislation eliminating the 96-hour condition of payment requirement, two policies that are particularly hard on rural providers.

Another bill, theSave Rural Hospitals Act, would reverse reimbursement cuts to rural hospitals, provide other regulatory relief and establish the community outpatient hospital, a new provider type offering 24/7 emergency services plus outpatient and primary care.

From reimbursement landscape challenges to dwindling inpatient volumes, many factors lead hospitals to file for bankruptcy.

Here are six hospitals that have filed for bankruptcy protection since Jan. 1:

1. Rockdale, Texas-based Little River Healthcare, its parent company and several of its affiliated entities entered Chapter 11 bankruptcy July 24. One of the hospitals included in the bankruptcy filing, Crockett, Texas-based Timberlands Hospital, closed in 2017.

2. Florence (Ariz.) Hospital at Anthementered Chapter 11 bankruptcy in late May after it failed to contest an involuntary bankruptcy petition from creditors within the required 21-day timeline.

3.Gilbert (Ariz.) Hospital, which is affiliated with Florence Hospital at Anthem, entered Chapter 11 bankruptcy May 24.

4. The Miami Medical Center, a 67-bed hospital that suspended services in October 2017, filed for Chapter 11 bankruptcy protection March 9. The hospital was sold in auction in late June.

5.Iron County Medical Center, a critical access hospital in Pilot Knob, Mo., filed for Chapter 9 bankruptcy Feb. 21. The hospital is owned by the Iron County Hospital District.

6. Surprise Valley Health Care District, which operates 26-bed Surprise Valley Hospital in Cedarville, Calif., filed for Chapter 9 bankruptcy Jan. 4.

CMS ended its provider agreement with Blackfoot-based Idaho Doctors’ Hospital July 20.

Under rules enacted last September, a healthcare facility must average at least two inpatients per day and an at least two-night average length of stay to be considered an inpatient hospital for Medicare reimbursement. In April, CMS determined Doctors’ Hospital is not primarily engaged in providing care to inpatients and does not meet the new federal requirements for Medicare participation. The agency subsequently sent Doctors’ Hospital a Medicare termination notice.

“To go from being OK just 18 months ago, when we had our last survey, to now being told that we don’t meet the CMS conditions of participation because of new interpretations of the regulations is just difficult to comprehend,” Dave Lowry, administrative manager at Idaho Doctors’ Hospital, told KIFI earlier this month. “Like any business that is regulated by government agencies, we fully expect there to be changes to rules and their interpretations, but this drastic level of change just goes to show how much uncertainty there is in healthcare right now.”

After receiving the termination notice from CMS, Doctors’ Hospital sent letters to all patients affected by the contract termination, a spokesperson told Becker’s Hospital Review.

“We have worked with other area hospitals who provide the same services, and our staff provides this information for any patients who call with questions on where to go for care,” the Doctors’ Hospital spokesperson said.

The final rule will also allow for higher payment when Medicare beneficiaries receive certain procedures in outpatient departments.

Several groups representing U.S. hospitals on Wednesday said they plan to sue the Centers for Medicare and Medicaid Services over a hospital outpatient prospective payment system final rule released Wednesday that reduces what hospitals are paid under the 340B drug program.

The rule lowers the cost of prescription drugs for seniors and other Medicare beneficiaries by reducing the payment rate to hospitals for certain Medicare Part B drugs purchased through the 340B program. The existing rule would have paid hospitals 6 percent above the sale price of drugs, but the final rule instead pays hospitals 22.5 percent less than sale prices, amounting to a $1.6 billion cut.

“CMS’s decision in today’s rule to cut Medicare payments to hospitals for drugs covered under the 340B program will dramatically threaten access to health care for many patients, including uninsured and other vulnerable populations,” AHA Executive Vice President Tom Nickels said in a statement. “We strongly urge CMS to abandon its misguided 340B rule, and instead take direct action to halt the unchecked, unsustainable increases in the cost of drugs.”

America’s Essential Hospitals CEO Bruce Siegel said the organization saw no reasonable rationale for diverting Medicare Part B reimbursement from hospitals in the 340B drug pricing program that are in the greatest need of support to providers not eligible for 340B discounts. CMS has no evidence that the policy will combat rising drug prices, he said.

“Congress clearly intended that the 340B program help hospitals that care for many vulnerable patients; this new policy subverts that goal,” Siegel said. “Essential hospitals operate with an average margin less than half that of other hospitals and depend on 340B program savings to stretch resources for patient care and community services. Given their fragile financial position, essential hospitals will not weather this policy’s 27 percent cut to Part B drug payments without scaling back services or jobs.”

340B Health said the rule is a backdoor effort to undermine an important drug discount program.

“Responding to a survey earlier this year, 340B hospitals were unanimous in saying implementation of the CMS rule would cause them to cut back services. For example, Genesis Healthcare System in Zanesville, Ohio, estimates a loss of $3 million in Medicare payments could force it to cancel critical services such as substance abuse treatment, cancer treatment, and behavioral health programs.The MetroHealth System Cancer Center in Cleveland, Ohio, estimates an $8 million loss would raise patients’ costs and reduce access to needed services including transportation and care navigation that are supported by 340B savings,” said 340B Health CEO Ted Slafsky.

However, the AIR340B Coalition said it would continue to advocate for regulatory action to better align the program with its original intent of helping vulnerable patients.

“We applaud the Administration for taking action to help address one aspect of the 340B program that has been leading to higher costs for Medicare and its beneficiaries,” the AIR340B Coalition said.

Areas of change it supports include clearly defining a 340B eligible patient, examination of hospital and satellite clinic eligibility criteria, and a more rational and legally supportable policy on contract pharmacy arrangements.

CMS said the savings will be reallocated equally to all hospitals paid under the hospital outpatient prospective payment system. Children’s hospitals, certain cancer hospitals, and rural sole community hospitals will be excluded from these drug payment reductions.

CMS will work with Congress for additional considerations on 340B for safety net hospitals, said CMS Administrator Seema Verma.

Consumers would save an estimated $320 million in copayments in 2018 under the new payment rule that gives Medicare beneficiaries the benefit of discounts hospitals receive under the 340B program, according to Verma.

“As part of the president’s priority to lower the cost of prescription drugs, Medicare is taking steps to lower the costs Medicare patients pay for certain drugs in the hospital outpatient setting,” Verma said.

The final rule will also allow outpatient payment to be made when Medicare beneficiaries receive certain procedures in a lower cost setting, the outpatient department. The new availability of the higher OPPS payment applies to six procedures, including total knee replacements, a common and costly Medicare surgical procedure, CMS said.

Starting in January 2018, Medicare beneficiaries undergoing any of the six procedures can opt to have them performed in a lower cost setting when a clinician believes such a setting is appropriate.

Additionally, the final rule provides relief to rural hospitals by placing a two-year moratorium on the direct physician supervision requirements for rural hospitals and critical access hospitals.

“CMS understands the importance of strengthening access to care, especially in rural areas,” Verma said. “This policy helps to ensure access to outpatient therapeutic services for seniors living in rural communities and provides regulatory relief to America’s rural hospitals.”

In a home health prospective payment system final rule, CMS is not finalizing the home health groupings model and will take additional time to further engage with stakeholders.

Over recent years, numerous rural health insurance markets have teetered on the brink of collapse. Rural areas have long posed a special challenge to health care policymakers, but a poorly-designed system of subsidies for rural hospital care has turned this into a crisis. It has fostered a rural hospital market structure that has crippled the ability of private insurers to negotiate reasonable payment rates, without fully securing the provision of essential care. By refocusing federal assistance on emergency care, it should be possible to restore rural insurance markets to health, while improving the affordability and access to care available to residents.

Warren Buffett once famously observed that “you only find out who is swimming naked when the tide goes out.” As the Affordable Care Act’s reforms have placed the nongroup market for health insurance under acute strain, it is rural areas that have been most exposed. Of 650 counties that have only a single insurer offering plans on their exchange, 70 percent are rural. For Medicare Advantage, despite total revenues roughly twice as large as the individual market, the situation is even worse—with 140 (mostly rural) counties lacking private insurance coverage options altogether.

It is more challenging to deliver healthcare services in sparsely populated areas. Small communities are unable to support full-time physicians for many medical specialties, and the fixed costs of multi-million-dollar hospital equipment cannot be spread across so many patients. As only 24 percent of rural residents can reach a top trauma center within an hour, rural areas suffer 60 percent of America’s trauma deaths, despite having only 20 percent of the nation’s population.

During the 1990s, economic pressures forced 208 rural hospitals to close. As a result, Congress established the Flex program to boost Medicare payments to isolated rural hospitals. Facilities designated as Critical Access Hospitals under the Flex program were intended to be more than 35 miles by major road from other facilities, but states were allowed to waive that requirement. As a result, the number of such hospitals grew from 41 in 1999 to more than 1,300 in 2011 – covering a quarter of U.S. hospitals, before Congress eliminated the states’ waiver power. By that time, 800 facilities exceeding the 35-mile requirement had been designated as CAHs, and these were grandfathered in.

What makes CAH status so attractive to hospitals? Instead of being paid standard Medicare rates for services, CAHs are allowed to claim reimbursement for whatever costs they incur in the delivery of covered inpatient, outpatient, post-acute and laboratory services to Medicare beneficiaries. Medicare pays more to facilities with the most expensive cost structures and eliminates incentives to control expenses – encouraging all to increase spending on new infrastructure and equipment.

Eighty-one percent of CAHs now have MRI scanners, for which they bill Medicare an average of $633 per scan—double the normal fee schedule rates. From 1998 to 2003, payments per discharge for acute care at CAHs rose by 21 percent, while post-acute care costs per day almost quadrupled. This upward pressure on costs has compounded over time: The longer a hospital has been a CAH, the more its costs have grown.

To check the capacity of CAHs to inflate their overheads, Medicare rules limit them to 25 beds. This has transformed the rural hospital landscape. In 1997, 85 percent of rural hospitals had more than 25 beds; by 2004 only 55 percent did. This makes it very difficult for the best-managed and most cost-effective facilities to win market share and has eliminated whatever competitive forces may have constrained costs. Nonetheless, excess capacity remains enormous: occupancy rates were only 37 percent in small rural hospital in 2014, compared with 64 percent in urban hospitals. Insurers covering care at such facilities must pay for equipment that is often unused and skilled physicians who spend much of their time idle.

Medicare Advantage (MA) plans have been hit hardest by this arrangement. MA plans usually attract enrollees by providing supplemental benefits and reduced out-of-pocket costs, funded by preventing unnecessarily costly hospitalizations. But, as CAHs are able to claim unconstrained reimbursement for Medicare beneficiaries directly from the government, they have little reason to agree to reasonable fees with MA plans, who may constrain their claims or steer enrollees to cheaper sites of care. Even under relatively loose network adequacy requirements, MA plans can, therefore, be effectively locked out of states dominated by CAHs. While 56 percent of Medicare beneficiaries in Minnesota are enrolled in MA plans, only 3 percent of those in Wyoming and 1 percent in Alaska are covered.

Low volumes and the absence of competition have also resulted in a lower quality of care. CAHs are more poorly-equipped than other hospitals, fall short on standard processes of care and have higher 30-day mortality rates for critical conditions. As a result, patients are increasingly willing to travel longer distance for treatments, with rural residents receiving 48 percent of elective care beyond their local providers. This bypass of rural provider networks is particularly common for surgeries on eye, musculoskeletal and digestive systems and for complex procedures more generally.

Although CAH status gives each hospital an average additional $500,000 of revenues, falling volumes of inpatient procedures and the increased costs entailed by this arrangement nonetheless leaves many facilities struggling. According to the National Rural Health Association, 55 rural hospitals closed between 2010 and 2015, while 283 were on brink of closure.

Can the $2 billion total annual cost of additional hospital subsidies provided by the Medicare Flex program not be better spent to support essential care in rural areas?

MedPAC, the agency established by Congress to advise it on Medicare payment policy, has argued that CAHs are “not the best solution”, as “many small towns do not have the population to support efficient, high-quality inpatient services.” MedPAC has proposed that Congress provide lump-sum payments to cover the overheads needed to provide 24/7 emergency care at geographically isolated outpatient-only facilities and suggested that Medicare reimbursement be extended to care provided by standalone emergency departments.

This would focus subsidies to secure emergency services, which must be delivered locally, while leaving elective care to be located efficiently according to market demand. Such a reform would give emergency rural hospital care a firmer financial foundation while restoring payment rules for elective care that would make it possible for insurers to re-enter the rural marketplace.

Consolidation remains a major trend in the healthcare industry, especially among hospitals. In 2016, there were 102 announced partnership and transaction deals, compared to 66 in 2010, according to a Kaufman, Hall & Associates analysis. In the current climate of declining reimbursements and greater emphasis on value-based care, many hospital executives see mergers as a necessary way of reigning in costs and benefiting from economies of scale. Yet, a significant number of acute care hospitals remain independent and even thrive. A recent article highlighted Marin General Hospital, which separated from Sutter in 2008 but has performed well enough on its own to fund construction of a new $400 million replacement hospital. What do high-performing independent hospitals have in common? An analysis of Definitive Healthcare data suggests independent hospitals with consistently strong operating margins have limited competition from other facilities, high discharge volumes, and a greater proportion of private payers.

Under the analysis, a high-performing hospital was classified as a facility with a median operating margin of at least four percent during a five-year period from 2011 to 2015, as four percent is often cited as the traditional minimum necessary for a hospital to be able to raise capital effectively. 143 out of around 1,450 independent hospitals met this condition, according to Definitive Healthcare data. Of them, 67 were non-profit, 56 were proprietary (for-profit) companies, and 30 were government owned.

A favorable payor mix and higher-than-average discharge volume appear to be the most common characteristics among the selected hospitals. The median payor mix for independent hospitals was 38 percent private/other, 6 percent Medicaid, and 51 percent Medicare, compared to 50 percent private, 6 percent Medicaid, and 41 percent Medicare at hospitals with median margins over four percent. The greater percentage of private payors means higher reimbursement rates per procedure and can reflect the presence of a more affluent patient base. The larger volume of discharges compared to the overall median, 1,662 to 792, also helps explain their higher margins. Despite the trend towards outpatient treatment, inpatient care is still necessary and tends to be more profitable for hospitals. Some facilities actually witnessed discharge increases from 2011 to 2015, possibly indicating a growing area population, but they were the minority and the trend did not always coincide with a stable operating margin.

Geography also appears to be an important factor. Isolated hospitals with limited competition have a natural advantage, being the only source of inpatient care within the immediate area. Some independent critical access hospitals, which by definition are geographically isolated, do have strong margins, but so do many regular acute care hospitals. Of the top 10 non-critical access facilities by median operating margin, eight are located at least 15 miles from the next-closest hospital, making them the primary destinations in terms of convenience and emergency care for local residents.

The company status of independent hospitals is also associated with high profitability. While proprietary hospitals constituted only around 10 percent of all independent hospitals, they were 37 percent of all those with median margins over four percent. In addition, they tended to have the highest margins overall. Of the top 30 hospitals by median margin, only three identified as non-profits or government-owned hospitals. Nearly all were specialty hospitals, which are generally more profitable than acute-care hospitals as they usually have more favorable payor mixes and focus on a single high-margin specialty, such as surgery or orthopedics. Non-profits came next, while government-owned facilities were the least likely to have strong margins. Of course, the margin of a government-owned hospital is less significant due to its ability to leverage tax revenues to support operations.

While financially strong independent hospitals appear to benefit largely from circumstances beyond their control, such as patient income, insignificant competition, and fundamental organizational structure, they are not a guarantee of success. Previous research, such as that here, has identified other characteristics that are equally if not more critical to an independent hospitals’ fortunes. Among them are strong business and clinical planning, high levels of cooperation with both local providers and national institutions (such as those covering specialty consults and clinical trials access), and capable leadership. Obviously, such qualities are easier described than achieved, but if attained, could be enough to create a strong, thriving hospital even in spite of unfavorable geography, payor mixes, or organization type.