Sign of the Times: High Deductible Health Care

https://mailchi.mp/c9e26ad7702a/the-weekly-gist-april-7-2023?e=d1e747d2d8

As the locus of care continues to shift from inpatient hospitals to outpatient centers, health system executives face a growing conundrum over pricing. The combination of “consumerism” and tougher reimbursement policies raises a question about how aggressively systems should discount services to compete in the ambulatory arena.

Site-neutral payment remains a goal for Medicare, and consumers are increasingly voting with their pocketbooks when it comes to choosing where to have procedures and diagnostics performed. “We know we’re going to have to give on price,” one CEO recently shared with us. “The question is how much, and how soon.”

Should hospitals proactively shift to match prices offered by freestanding centers, or should they try to defend their substantially higher “hospital outpatient department” (HOPD) pricing?

The former choice could help win—or at least keep—business in the system, but at the risk of turning that business into a money-losing proposition.

To compete successfully, hospitals will not only need to lower price, but also lower cost-to-serve—rethinking how operations are run, how overhead is allocated, and how services are staffed and delivered in ambulatory settings.

“We’ve got to get our costs down,” the CEO admitted. “Trying to run an ambulatory business with our traditional hospital cost structure is a recipe for losing money.”

And as a system CFO recently told us, “We can’t just trade good price for bad, for doing the same work. We have to be smart about where to discount services.” The future sustainability of many health systems will hinge on how they navigate this transition to an ambulatory-centric model.

Radio Advisory’s Rachel Woods sat down with Optum EVP Dr. Jim Bonnette to discuss the sustainability of modern-day hospitals and why scaling down might be the best strategy for a stable future.

Read a lightly edited excerpt from the interview below and download the episode for the full conversation.https://player.fireside.fm/v2/HO0EUJAe+Rv1LmkWo?theme=dark

Rachel Woods: When I talk about hospitals of the future, I think it’s very easy for folks to think about something that feels very futuristic, the Jetsons, Star Trek, pick your example here. But you have a very different take when it comes to the hospital, the future, and it’s one that’s perhaps a lot more streamlined than even the hospitals that we have today. Why is that your take?

Jim Bonnette: My concern about hospital future is that when people think about the technology side of it, they forget that there’s no technology that I can name that has lowered health care costs that’s been implemented in a hospital. Everything I can think of has increased costs and I don’t think that’s sustainable for the future.

And so looking at how hospitals have to function, I think the things that hospitals do that should no longer be in the hospital need to move out and they need to move out now. I think that there are a large number of procedures that could safely and easily be done in a lower cost setting, in an ASC for example, that is still done in hospitals because we still pay for them that way. I’m not sure that’s going to continue.

Woods: And to be honest, we’ve talked about that shift, I think about the outpatient shift. We’ve been talking about that for several years but you just said the change needs to happen now. Why is the impetus for this change very different today than maybe it was two, three, four, five years ago? Why is this change going to be frankly forced upon hospitals in the very near future, if not already?

Bonnette: Part of the explanation is regarding the issues that have been pushed regarding price transparency. So if employers can see the difference between the charges for an ASC and an HOPD department, which are often quite dramatic, they’re going to be looking to say to their brokers, “Well, what’s the network that involves ASCs and not hospitals?” And that data hasn’t been so easily available in the past, and I think economic times are different now.

We’re not in a hyper growth phase, we’re not where the economy’s performing super at the moment and if interest rates keep going up, things are going to slow down more. So I think employers are going to become more sensitized to prices that they haven’t been in the past. Regardless of the requirements under the Consolidated Appropriations Act, which require employers to know the costs, which they didn’t have to know before. They’re just going to more sensitive to price.

Woods: I completely agree with you by the way, that employers are a key catalyst here and we’ve certainly seen a few very active employers and some that are very passive and I too am interested to see what role they play or do they all take much more of an active role.

And I think some people would be surprised that it’s not necessarily consumers themselves that are the big catalyst for change on where they’re going to get care, how they want to receive care. It’s the employers that are going to be making those decisions as purchasers themselves.

Bonnette: I agree and they’re the ultimate payers. For most commercial insurance employers are the ultimate payers, not the insurance companies. And it’s a cost of care share for patients, but the majority of the money comes from the employers. So it’s basically cutting into their profits.

Woods: We are on the same page, but I’m going to be honest, I’m not sure that all of our listeners are right. We’re talking about why these changes could happen soon, but when I have conversations with folks, they still think about a future of a more consolidated hospital, a more outpatient focused practice is something that is coming but is still far enough in the future that there’s some time to prepare for.

I guess my question is what do you say to that pushback? And are there any inflection points that you’re watching for that would really need to hit for this kind of change to hit all hospitals, to be something that we see across the industry?

Bonnette: So when I look at hospitals in general, I don’t see them as much different than they were 20 years ago. We have talked about this movement for a long time, but hospitals are dragging their feet and realistically it’s because they still get paid the same way until we start thinking about how we pay differently or refuse to pay for certain kinds of things in a hospital setting, the inertia is such that they’re going to keep doing it.

Again, I think the push from employers and most likely the brokers are going to force this change sooner rather than later, but that’s still probably between three and five years because there’s so much inertia in health care.

On the other hand, we are hitting sort of an unsustainable phase of cost. The other thing that people don’t talk about very much that I think is important is there’s only so many dollars that are going to health care.

And if you look at the last 10 years, the growth in pharmaceutical spend has to eat into the dollars available for everybody else. So a pharmaceutical spend is growing much faster than anything else, the dollars are going to come out of somebody’s hide and then next logical target is the hospital.

Woods: And we talked last week about how slim hospital margins are, how many of them are actually negative. And what we didn’t mention that is top of mind for me after we just come out of this election is that there’s actually not a lot of appetite for the government to step in and shore up hospitals.

There’s a lot of feeling that they’ve done their due diligence, they stepped in when they needed to at the beginning of the Covid crisis and they shouldn’t need to again. That kind of savior is probably not their outside of very specific circumstances.

Bonnette: I agree. I think it’s highly unlikely that the government is going to step in to rescue hospitals. And part of that comes from the perception about pricing, which I’m sure Congress gets lots of complaints about the prices from hospitals.

And in addition, you’ll notice that the for-profit hospitals don’t have negative margins. They may not be quite as good as they were before, but they’re not negative, which tells me there’s an operational inefficiency in the not for-profit hospitals that doesn’t exist in the for-profits.

Woods: This is where I wanted to go next. So let’s say that a hospital, a health system decides the new path forward is to become smaller, to become cheaper, to become more streamlined, and to decide what specifically needs to happen in the hospital versus elsewhere in our organization.

Maybe I know where you’re going next, but do you have an example of an organization who has had this success already that we can learn from?

Bonnette: Not in the not-for-profit section, no. In the for-profits, yes, because they have already started moving into ambulatory surgery centers. So Tenet has a huge practice of ambulatory surgery centers. It generates high margins.

So, I used to run ambulatory surgery centers in a for-profit system. And so think about ASCs get paid half as much as a hospital for a procedure, and my margin on that business in those ASCs was 40% to 50%. Whereas in the hospital the margin was about 7% and so even though the total dollars were less, my margin was higher because it’s so much more efficient. And the for-profits already recognize this.

Woods: And I’m guessing you’re going to tell me you want to see not-for-profit hospitals make these moves too? Or is there a different move that they should be making?

Bonnette: No, I think they have to. I think there are things beyond just ASCs though, for example, medical patients who can be treated at home should not be in the hospital. Most not-for-profits lose money on every medical admission.

Now, when I worked for a for-profit, I didn’t lose money on every Medicare patient that was a medical patient. We had a 7% margin so it’s doable. Again, it’s efficiency of care delivery and it’s attention to detail, which sometimes in a not-for-profit friends, that just doesn’t happen.

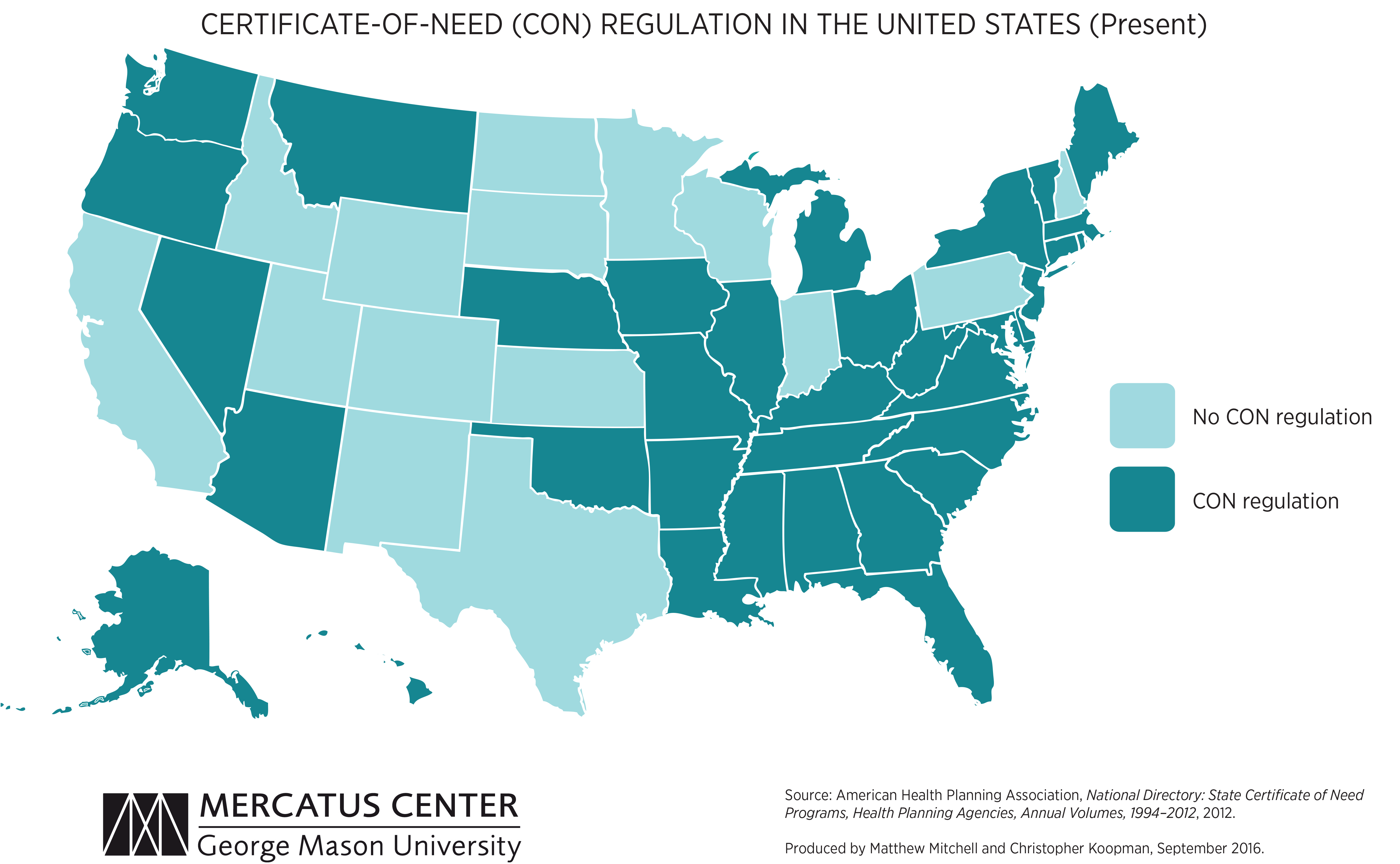

We’re picking up on a growing concern among health system leaders that many states with “certificate of need” (CON) laws in effect are on the cusp of repealing them. CON laws, currently in place in 35 states and the District of Columbia, require organizations that want to construct new or expand existing healthcare facilities to demonstrate community need for the additional capacity, and to obtain approval from state regulatory agencies. While the intent of these laws is to prevent duplicative capacity, reduce unnecessary utilization, and control cost growth, critics claim that CON requirements reduce competition—and free market-minded state legislators, particularly in the South and Midwest, have made them a target.

One of our member systems located in a state where repeal is being debated asked us to facilitate a scenario planning session around CON repeal with system and physician leaders. Executives predicted that key specialty physician groups would quickly move to build their own ambulatory surgery centers, accelerating shift of surgical volume away from the hospital.

The opportunity to expand outpatient procedure and long-term care capacity would also fuel investment from private equity, which have already been picking up in the market. An out-of-market health system might look to build microhospitals, or even a full-service inpatient facility, which would be even more disruptive.

CON repeal wasn’t all downside, however; the team identified adjacent markets they would look to enter as well. The takeaway from our exercise: in addition to the traditional response of flexing lobbying influence to shape legislative change, the system must begin to deliver solutions to consumers that are comprehensive, convenient, and competitively priced—the kind of offerings that might flood the market if CON laws were lifted.

https://mailchi.mp/b5daf4456328/the-weekly-gist-july-23-2021?e=d1e747d2d8

Two major policy developments emerged from this week’s release by the Centers for Medicare & Medicaid Services (CMS) of the FY22 proposed rule governing payment for hospital outpatient services and ambulatory surgical centers.

First, CMS proposes to dramatically increase the financial penalties assessed to hospitals that fail to adequately reveal prices for their services, a requirement first put in place by the Trump administration. According to a report by the consumer group Patient Rights Advocate, only 5.6 percent of a random sample of 500 hospitals were in full compliance with the transparency requirement six months after the regulation came into effect, with many instead choosing to pay the $300 per hospital per day penalty associated with noncompliance. The new CMS regulation proposes to scale the assessed penalties in accordance with hospital size, with larger hospitals liable for up to $2M in annual penalties, a substantial increase from the earlier $109,500 maximum annual fine. In a press release, the agency said it “takes seriously concerns it has heard from consumers that hospitals are not making clear, accessible pricing information available online, as they have been required to do since January 1, 2021.” In a statement, the AHA stated that it was “deeply concerned” about the proposal, “particularly in light of substantial uncertainty in the interpretation of the rules.” The penalty hike is a clear signal that the Biden administration plans to put teeth behind its new push for more competition in healthcare, which was a major focus of the President’s recent executive order. We’d expect to see most hospitals and health systems quickly move to comply with the transparency rule, given the size of potential penalties.

More heartening to hospitals was CMS’ proposal to roll back changes the Trump administration made, aimed at shifting certain surgical procedures into lower cost, ambulatory settings. The agency proposed halting the elimination of the Inpatient Only (IPO) list, which specifies surgeries CMS will only pay for if they are performed in an inpatient hospital. Citing patient safety concerns, CMS noted that the phased elimination of the IPO list, which began this year, was undertaken without evaluating whether individual procedures could be safely moved to an outpatient setting. Nearly 300 musculoskeletal procedures have already been eliminated from the list, and will now be added back to the list for 2022, keeping the rest of the list intact while CMS undertakes a formal process to review each procedure. Longer term, we’d anticipate that CMS will look to continue the elimination of inpatient-only restrictions on surgeries, as well as pursuing other policies (such as site-neutral payment) that level the playing field between hospitals and lower-cost outpatient providers.

For now, hospitals will enjoy a little more breathing room to plan for the financial consequences of that inevitable shift.

Hospitals lost 5,800 jobs in April, marking the fourth month of job loss this year, according to the latest jobs report from the U.S. Bureau of Labor Statistics.

The April count compares to 600 hospital jobs lost in March, 2,200 jobs lost in February and 2,100 jobs lost in January. Before January, the last job loss was in September, when hospitals lost 6,400 jobs.

Overall, healthcare lost 4,100 jobs last month — compared to 11,500 jobs added in March — and employment in the industry is down by 542,000 since February 2020.

Within ambulatory healthcare services, dentist offices saw 3,700 added jobs; physician offices saw 11,300 job gains; and home healthcare services lost 6,700 jobs in April.

Nursing and residential care facilities lost 19,500 jobs last month, compared to 3,200 jobs lost the month prior.

The U.S. gained 266,000 in April after gaining 916,000 jobs in March. The unemployment rate was 6.1 percent last month, compared to 6 percent in March.

To view the full jobs report, click here.

A key Medicare advisory panel is calling for a 2% bump to Medicare payments for acute care hospitals for 2022 but no hike for physicians.

The report, released Monday from the Medicare Payment Advisory Commission (MedPAC)—which recommends payment policies to Congress—bases payment rate recommendations on data from 2019. However, the commission did factor in the pandemic when evaluating the payment rates and other policies in the report to Congress, including whether policies should be permanent or temporary.

“The financial stress on providers is unpredictable, although it has been alleviated to some extent by government assistance and rebounding service utilization levels,” the report said.

MedPAC recommended that targeted and temporary funding policies are the best way to help providers rather than a permanent hike for payments that gets increased over time.

“Overall, these recommendations would reduce Medicare spending while preserving beneficiaries’ access to high-quality care,” the report added.

MedPAC expects the effects of the pandemic, which have hurt provider finances due to a drop in healthcare use, to persist into 2021 but to be temporary.

It calls for a 2% update for inpatient and outpatient services for 2022, the same increase it recommended for 2021.

The latest report recommends no update for physicians and other professionals. The panel also does not want any hikes for four payment systems: ambulatory surgical centers, outpatient dialysis facilities, skilled nursing facilities and hospices.

MedPAC also recommends Congress reduce the aggregate hospice cap by 20% and that “ambulatory surgery centers be required to report cost data to [Centers for Medicare & Medicaid Services (CMS)],” the report said.

But it does call for long-term care hospitals to get a 2% increase and to reduce payments by 5% for home health and inpatient rehabilitation facilities.

The panel also explores the effects of any policies implemented under the COVID-19 public health emergency, which is likely to extend through 2021 and could continue into 2022.

For instance, CMS used the public health emergency to greatly expand the flexibility for providers to be reimbursed for telehealth services. Use of telehealth exploded during the pandemic after hesitancy among patients to go to the doctor’s office or hospital for care.

“Without legislative action, many of the changes will expire at the end of the [public health emergency],” the report said.

MedPAC recommends Congress temporarily continue some of the telehealth expansions for one to two years after the public health emergency ends. This will give lawmakers more time to gather evidence on the impact of telehealth on quality and Medicare spending.

“During this limited period, Medicare should temporarily pay for specified telehealth services provided to all beneficiaries regardless of their location, and it should continue to cover certain newly-covered telehealth services and certain audio-only telehealth services if there is potential for clinical benefit,” according to a release on the report.

After the public health emergency ends, Medicare should also return to paying the physician fee schedule’s facility rate for any telehealth services. This will ensure Medicare can collect data on the cost for providing the services.

“Providers should not be allowed to reduce or waive beneficiary cost-sharing for telehealth services after the [public health emergency],” the report said. “CMS should also implement other safeguards to protect the Medicare program and its beneficiaries from unnecessary spending and potential fraud related to telehealth.”

https://www.businessinsider.com/walmart-slowing-healthcare-clinics-strategy-2021-2

In 2018, Walmart‘s board of directors approved a bold plan to scale to 4,000 clinics by 2029.

The timeline laid out a net investment of $3 billion, not counting profits from the clinics, and a rollout strategy, according to a February 2019 presentation to the board obtained by Insider.

The vision was backed by former Walmart US CEO Greg Foran, the health team’s biggest champion who left Walmart in 2019. And it was dreamed up by Sean Slovenski, who Foran asked to come up with a big idea in healthcare as Walmart’s biggest competitors were pushing deeper into the space.

Now those leaders have been replaced by a team with a different philosophy, and the strategy is in flux at the same time Walmart is dealing with the pandemic and focusing on e-commerce, Insider has learned through conversations with eight former and current employees.

One coalition inside Walmart is happy with the change of pace —the retailer has 20 clinics currently, with at least 15 slotted for 2021 — because healthcare is hard, and the clinics are a work in progress.

Another coalition is frustrated by what they see as a stark departure from the initial goal to provide inexpensive care for people around the US quickly as possible.

Walmart didn’t comment on whether the rollout was slowing, but said it continued to “experiment” with Walmart Health centers and that the pandemic had reaffirmed its commitment to healthcare. It pointed to the launch of pharmacy curbside delivery, COVID-19 testing sites, and vaccine administration as evidence.

Dubai is proud to introduce its impressive fleet of the “world’s largest ambulances,” or “Mercedes-Benz large-capacity ambulances” which were created to give rapid medical assistance in the event of major emergencies with large numbers of causalities. These new emergency vehicles offer a fully-equipped, mobile clinic with an intensive-care unit and an operating room.

Equipped with an X-ray unit and ultrasonic equipment for further evaluation, each super ambulance bus carries 12,000 liters of oxygen, which ensures a dependable supply for up to three days. With the press of a button, oxygen masks fall from special holders, and the oxygen flow to each mask can be individually controlled.

They’re also equipped with an ECG and an InSpectra shock monitor, which monitors the oxygen saturation in tissue-matter and warns doctors of the onset of shock minutes before it occurs. This unit can also detect and monitor internal bleeding. If an emergency caesarian birth is needed, essential obstetrical instruments, including an incubator, are on board.

https://www.healthcaredive.com/trendline/labor/28/#story-1

Hospitals are often the biggest employers in many towns and medium-sized cities, but their job creation has been uneven at best in recent months. According to an analyst note from Jefferies, employment by hospitals dropped by 2,000 on a seasonally adjusted basis, although that grew to a net 1,000 new jobs on an unadjusted basis.

By comparison, hospitals added a seasonally adjusted 9,000 new jobs in June, 25,000 on an unadjusted basis. However, much of that boost was created by the minting of new residents who just graduated from medical schools.

Hospital employment is still growing at a 1.8% annual clip (compared to 1.4% as of July 2018), although that’s down from the 2.1% rate reported in April.

“Overall, healthcare employment growth continues to demonstrate strong momentum, but hospital jobs growth appears to be moderating,” the analysts said. Inpatient providers account for more than 5.2 million jobs nationwide.

However, Jefferies’ analysts believe that healthcare will continue to be a big job engine for the foreseeable future.

“We believe the supply of clinical labor continues to struggle to keep pace with solid demand growth, resulting in tight clinician labor markets and strong demand for healthcare temp staffing services,” they said.

Although healthcare job growth has been extremely robust, wages have been stagnant in recent years, a phenomenon attributed in part to continued consolidation among industry players.

The ambulatory care segment has been growing rapidly in recent years. Its addition of 29,000 new jobs was up from 17,000 in June, and significantly outpaced the year-to-date average monthly growth of 22,000.

Home healthcare services added 11,000 new jobs last month alone — the highest rate since 2017. The segment’s annual growth rate is currently 5.3%, up from 3.2% in July 2018.

The nursing home segment added another 1,000 jobs.