Nurses who work for staffing agencies are much more satisfied than their counterparts who serve hospitals, health systems, home healthcare providers and senior living facilities, according to an Oct. 18 report from MIT Sloan Management Review.

Researchers identified 200 of the largest healthcare employers in the U.S., and calculated how highly nurses rate the organization and senior leadership on Glassdoor from the beginning of COVID-19 through June 2023 (view their ranking here).

The five highest-ranked employers in the sample were staffing agencies, according to the report — and higher compensation only accounts for part of nurses’ satisfaction. Researchers analyzed the free text on Glassdoor to determine how positively nurses spoke about 200 topics, and found that nurses spoke more highly of staffing agencies on issues other than pay.

Overall, 75% of nurses’ comments about staffing agencies were positive, compared with 23% of nurses’ comments about health systems.

Staffing agencies have other healthcare employers beat in problem resolution, the researchers found. Seventy-three percent of nurses said staffing agencies resolved problems efficiently, compared to 31% of nurses employed by hospitals and health systems. The difference was even greater when it came to resolving problems effectively — 55% of nurses say staffing agencies do this, compared to 9% of nurses at hospitals and health systems.

Nurses also rated staffing agencies more highly on several measures related to honesty, according to the report. Three-quarters of nurses employed by staffing agencies spoke highly of their organizations’ speed in replying to inquiries; less than one-quarter of nurses employed by hospitals and health systems praised their organization on timely replies. Staffing agencies scored 41 percentage points higher on transparency, 36 points higher on trust and 46 points higher on honesty than their hospital and health system counterparts.

Although nurses employed by staffing agencies also ranked their compensation and work-related stress levels significantly better than nurses employed by hospitals and health systems, the latter took the lead in some metrics. Nurses prefer hospitals and health systems for health and retirement benefits, learning and development opportunities, and connection with colleagues: all “important aspects of organizational life,” according to the report.

“Healthcare systems can learn from staffing agencies, but they can also leverage their own distinctive advantages to attract and retain nurses,” the report says. “Healthcare systems should invest in their comparative advantages and emphasize them when communicating their value proposition to potential and current employees.”

Hospitals in California are being warned not to violate state law on staffing levels or face fines. New state policy narrows the circumstances under which hospitals can claim “unpredictable circumstances” for violating the mandate.

The California Department of Public Health this week, in a notice to hospitals, warned that noncompliance can result in a $15,000 fine for a first violation and $30,000 for a second.

The state conducts periodic, unannounced inspections to enforce compliance.

New policy by Governor Newsom narrows the circumstances under which hospitals will not be penalized for violations due to “unpredictable circumstances,” requiring them to document efforts to maintain safe staffing and that such instances be truly unforeseen.

In an advisory letter to hospitals, the public health department said, “Situations that are not considered unpredictable, unknown or uncontrollable include consistent, ongoing patterns of understaffing. Facilities are expected to maintain required nurse-to-patient ratios at all times, including but not limited to, weekends, holidays, leaves of absences, among others.”

WHY THIS MATTERS

Minimum staffing ratios have been law in California since nurses and healthcare workers fought to pass AB 394, the nation’s first nurse-patient staffing ratio law in 1999.

In addition, SB 227, which passed in 2019, requires the state to assess administrative fines on hospitals that violate the safe staffing law. Law AB 1422 requires public comment before the public health department grants waivers to the critical care program flexibility requests.

THE LARGER TREND

Nurse staffing ratios are controversial and California remains the only state to have enacted them.

A study reportedly commissioned by the Centers for Medicare and Medicaid Services said there was “no single staffing level that would guarantee quality care.”

The NIH looked at survey data from 22,336 hospital staff nurses in California, Pennsylvania and New Jersey in 2006 and state hospital discharge databases. California hospital nurses cared for one less patient on average than nurses in the other states and two fewer patients in medical and surgical units, the NIH research said.

The study found that lower ratios were associated with significantly lower mortality. When nurses’ workloads were in line with California-mandated ratios in all three states, nurses’ burnout and job dissatisfaction were lower, and nurses reported consistently better quality of care, the NIH said.

Also, the hospital nurse staffing ratios in California were associated with better nurse retention than in the other states.

ON THE RECORD

“Patients in California are safer today because nurses and healthcare workers demanded that hospitals be held accountable for violating safe-staffing laws,” said Leo Pérez, RN and president of SEIU 121RN. “The COVID-19 pandemic taught us that our state’s health depends on supporting and listening to those who are on the front lines of patient care – a lesson we should never forget. Today’s action is the result of SEIU’s relentless vigilance. We applaud the step CDPH has taken to enforce laws that keep patients safe.”

Working as a travel nurse in the early days of the Covid pandemic was emotionally exhausting for Reese Brown — she was forced to leave her young daughter with her family as she moved from one gig to the next, and she watched too many of her intensive care patients die.

“It was a lot of loneliness,” Brown, 30, said. “I’m a single mom, I just wanted to have my daughter, her hugs, and see her face and not just through FaceTime.”

But the money was too good to say no. In July 2020, she had started earning $5,000 or more a week, almost triple her pre-pandemic pay. That was the year the money was so enticing that thousands of hospital staffers quit their jobs and hit the road as travel nurses as the pandemic raged.

Two years later, the gold rush is over. Brown is home in Louisiana with her daughter and turning down work. The highest paid travel gigs she’s offered are $2,200 weekly, a rate that would have thrilled her pre-pandemic. But after two “traumatic” years of tending to Covid patients, she said, it doesn’t feel worth it.

“I think it’s disgusting because we went from being praised to literally, two years later, our rates dropped,” she said. “People are still sick, and people are still dying.”

The drop in pay doesn’t mean, however, that travel nurses are going to head back to staff jobs. The short-lived travel nurse boom was a temporary fix for a long-term decline in the profession that predates the pandemic. According to a report from McKinsey & Co., the United States may see a shortage of up to 450,000 registered nurses within three years barring aggressive action by health care providers and the government to recruit new people. Nurses are quitting, and hospitals are struggling to field enough staff to cover shifts.

Nine nurses around the country, including Brown, told NBC News they are considering alternate career paths, studying for advanced degrees or exiting the profession altogether.

“We’re burned out, tired nurses working for $2,200 a week,” Brown said. People are leaving the field, she said, “because there’s no point in staying in nursing if we’re expendable.”

$124.96 an hour

Travel nursing seems to have started as a profession, industry experts say, in the late 1970s in New Orleans, where hospitals needed to add temporary staff to care for sick tourists during Mardi Gras. In the 1980s and the 1990s, travel nurses were often covering for staff nurses who were on maternity leave, meaning that 13-week contracts become common.

By 2000, over a hundred agencies provided travel contracts, a number that quadrupled by the end of the decade. It had become a lucrative business for the agencies, given the generous commissions that hospitals pay them. A fee of 40 percent on top of the nurse’s contracted salary is not unheard of, according to a spokesperson for the American Health Care Association, which represents long-term care providers.

Just before the pandemic, in January 2020, there were about 50,000 travel nurses in the U.S., or about 1.5 percent of the nation’s registered nurses, according to Timothy Landhuis, vice president of research at Staffing Industry Analysts, an industry research firm. That pool doubled in size to at least 100,000 as Covid spread, and he says the actual number at the peak of the pandemic may have far exceeded that estimate.

By 2021, travel nurses were earning an average of $124.96 an hour, according to the research firm — three times the hourly rate of staff nurses, according to federal statistics.

That year, according to the 2022 National Health Care Retention & RN Staffing Report from Nursing Solutions Inc., a nurse recruiting firm, the travel pay available to registered nurses contributed to 2.47% of them leaving hospital staff jobs.

But then, as the rate of deaths and hospitalizations from Covid waned, the demand for travel nurses fell hard, according to industry statistics, as did the pay.

Demand dropped 42 percent from January to July this year, according to Aya Healthcare, one of the largest staffing firms in the country.

That doesn’t mean the travel nurses are going back to staff jobs.

Brown said she’s now thinking about leaving the nursing field altogether and has started her own business. Natalie Smith of Michigan, who became a travel nurse during the pandemic, says she intends to pursue an advanced degree in nursing but possibly outside of bedside nursing.

Pamela Esmond of northern Illinois, who also became a travel nurse during the pandemic, said she’ll keep working as a travel nurse, but only because she needs the money to retire by 65. She’s now 59.

“The reality is they don’t pay staff nurses enough, and if they would pay staff nurses enough, we wouldn’t have this problem,” she said. “I would love to go back to staff nursing, but on my staff job, I would never be able to retire.”

The coronavirus exacerbated issues that were already driving health care workers out of their professions, Landhuis said. “A nursing shortage was on the horizon before the pandemic,” he said.

According to this year’s Nursing Solutions staffing report, nurses are exiting the bedside at “an alarming rate” because of rising patient ratios, and their own fatigue and burnout. The average hospital has turned over 100.5% of its workforce in the past five years, according to the report, and the annual turnover rate has now hit 25.9%, exceeding every previous survey.

There are now more than 203,000 open registered nurse positions nationwide, more than twice the number just before the pandemic in January 2020, according to Aya Healthcare.

An obvious short-term solution would be to keep using travel nurses. Even with salaries falling, however, the cost of hiring them is punishing.

LaNelle Weems, executive director of Mississippi Hospital Association’s Center for Quality and Workforce, said hospitals can’t keep spending like they did during the peak of the pandemic.

“Hospitals cannot sustain paying these exorbitant labor costs,” Weems said. “One nuance that I want to make sure you understand is that what a travel agency charges the hospitals is not what is paid to the nurse.”

Ultimately, it’s the patients who will suffer from the shortage of nurses, whether they are staff or gig workers.

“Each patient added to a hospital nurse’s workload is associated with a 7%-12% increase in hospital mortality,” said Linda Aiken, founding director of the University of Pennsylvania’s Center for Health Outcomes and Policy Research.

Nurses across the country told NBC News that they chose the profession because they cared about patient safety and wanted to be at the bedside in the first line of care.

“People say it’s burnout but it’s not,” Esmond said about why nurses are quitting. “It’s the moral injury of watching patients not being taken care of on a day-to-day basis. You just can’t take it anymore.”

As RNs struggle to work through staffing shortages, their job satisfaction has sharply declined, with 67% saying they plan to leave their jobs within the next few years, according to a survey from the American Association of Critical-Care Nurses (AACN) published in Critical Care Nurse.

RNs cite poor work environments

For the survey, AACN collected responses from 9,862 nurses, 9,335 of which met the study criteria of being currently practicing RNs, in October 2021. The mean age was 46.5 years, and the mean years of experience was 17.8 years.

Of the participants, 78.3% worked in direct care, and 19.4% worked in a Beacon unit, meaning that their unit had been recognized by an AACN Beacon Award for Excellence. Half of the participants said they spent 50% or less of their time caring for Covid-19 patients, while the other half said they spent 50% or more.

To measure the health of a work environment, AACN looked at six standards:

Skilled communication

True collaboration

Effective decision-making

Meaningful recognition

Authentic leadership

Appropriate staffing

Overall, AACN found that nurses’ perceptions of quality on these six measures had declined across the board since the organization’s 2018 survey.

In particular, appropriate staffing was the lowest rated of all the standards at 2.33 out of 4, which is the lowest rating the standard has received since AACN first began the survey in 2006. Only 24% of RNs said their units had the right number of nurses with the right knowledge and skills more than 75% of the time—down from 39% who said the same in 2018.

In addition, there was a significant decline in how RNs rated the quality of care in their organizations and their units. Only 16% rated their organizations’ quality of care as excellent (compared to 24% in 2018), and 30% rated their units’ quality of care as excellent (compared to 44% in 2018). Over 50% of nurses said quality of care in their organization or unit has gotten somewhat or much worse over the last year.

Many nurses also reported difficulties with their physical and psychological well-being in the survey. For example, less than 50% of RNs said they felt their organization values their health and safety, a significant decline from 68% who said the same in 2018.

In addition, 40% of participants reported that they were not emotionally healthy. The percentage of RNs who reported experiencing moral distress also doubled from 11% in 2018 to 22% in 2021.

A significant portion of RNs also reported experiencing verbal abuse, physical abuse, sexual harassment, or discrimination over the past year. Of the 7,399 RNs who answered this question, 72% said they had experienced at least one negative incident, with verbal abuse being the most common at 65%, followed by physical abuse at 28%.

RN job satisfaction

Only 40% of RNs said they were “very satisfied” with their job, down from 62% who said the same in 2018. Further, a significant number of RNs in the survey reported planning to leave their jobs within the next few years.

Overall, 67% of RNs said they planned to leave their current position within the next three years, compared to 54% in 2018. Of this group, 36% said they planned to leave within the next year, with 20% planning to leave within the next six months.

According to the respondents, the top factors that could lead them to reconsider their decision to leave their job were a higher salary and more benefits (63%), better staffing (57%), and more respect from administration (50%).

“Without improvements in the work environment, the results of this study indicate that nurses will continue to exit the workforce in search of more meaningful, rewarding, and sustainable work,” the survey’s authors wrote. “It is time for bold action, and this study shows the way.” (Firth, MedPage Today, 8/3; Ulrich et al., Critical Care Nurse, 8/1)

Hard truths on the current and future state of the nursing workforce

Concerns about an imbalance in supply and demand in the nursing workforce have been around for years. The number of nursing professionals nationally may be healthy, but many nurses are not in the local areas, sites of care, or roles where they’re needed most. And many of today’s nurses don’t have the specialized skills they need, widening the existing gap between nurse experience and job complexity.

As a result, gaping holes in staffing rosters, prolonged vacancies, unstable turnover rates, and unchecked use of premium labor are now common.

Health care leaders need to confront today’s challenges in the nursing workforce differently than past cyclical shortages. In this report, we present six hard truths about the nursing workforce. Then, we detail tactics for how leaders can successfully address these challenges—stabilizing the nursing workforce in the short term and preparing it for the future.

Hospitals are experiencing significant increases in expenses for workforce, drugs and medical supplies

Introduction

For over two years since the outset of the COVID-19 pandemic, America’s hospitals and health systems have been on the front lines caring for patients, comforting families and protecting communities.

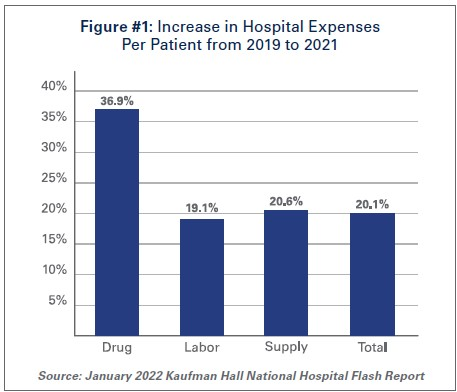

With over 80 million cases1, nearly 1 million deaths2, and over 4.6 million hospitalizations3, the pandemic has taken a significant toll on hospitals and health systems and placed enormous strain on the nation’s health care workforce. During this unprecedented public health crisis, hospitals and health systems have confronted many challenges, including historic volume and revenue losses, as well as skyrocketing expenses (See Figure #1).

Hospitals and health systems have been nimble in responding to surges in COVID-19 cases throughout the pandemic by expanding treatment capacity, hiring staff to meet demand, acquiring and maintaining adequate supplies and personal protective equipment (PPE) to protect patients and staff and ensuring that critical services and programs remain available to the patients and communities they serve. However, these and other factors have led to billions of dollars in losses over the last two years for hospitals, and over 33% of hospitals are operating on negative margins.

The most recent surges triggered by the delta and omicron variants have added even more pressure to hospitals. During these surges, hospitals saw the number of COVID-19 infected patients rise while other patient volumes fell, and patient acuity increased. This drove up expenses and added significant financial pressure for hospitals. Moreover, hospitals did not receive any government assistance through the COVID-19 Provider Relief Fund (PRF) to help mitigate rising expenses and lost revenues during the delta and omicron surges. This is despite the fact that more than half of COVID-19 hospitalizations have occurred since July 1, 2021, during these two most recent COVID-19 surges.

At the same time, patient acuity has increased, as measured by how long patients need to stay in the hospital. The increase in acuity is a result of the complexity of COVID-19 care, as well as treatment for patients who may have put off care during the pandemic. The average length of a patient stay increased 9.9% by the end of 2021 compared to pre-pandemic levels in 2019.4

As hospitals treat sicker patients requiring more intensive treatment, they also must ensure that sufficient staffing levels are available to care for these patients, and must acquire the necessary expensive drugs and medical supplies to provide high-quality care. As a result, overall hospital expenses have experienced considerable growth.

Data from Kaufman Hall, a consulting firm that tracks hospital financial metrics, shows that by the end of 2021, total hospital expenses were up 11% compared to pre-pandemic levels in 2019. Even after accounting for changes in volume that occurred during the pandemic, hospital expenses per patient increased significantly from pre-pandemic levels across every category. (See Figure #1)

The pandemic has strained hospitals’ and health systems’ finances. Many hospitals operate on razorthin margins, so even slight increases in expenses can have dramatic negative effects on operating margins, which can jeopardize their ability to care for patients. These expense increases have been more challenging to withstand in light of rising inflation and growth in input prices. In fact, despite modest growth in revenues compared to pre-pandemic levels, median hospital operating margins were down 3.8% by the end of 2021 compared to pre-pandemic levels, according to Kaufman Hall. Further exacerbating the problem for hospitals are Medicare sequestration cuts and payment increases that are well below increases in costs. For example, an analysis by PINC found that for fiscal year 2022, hospitals received a 2.4% increase in their Medicare inpatient payment rate, while hospital labor rates increased 6.5%.5

These levels of increased expenses and declines in operating margins are not sustainable. This report highlights key pressures currently facing hospitals and health systems, including:

Each of these issues separately presents significant challenges to the hospital field. Taken together, they represent conditions that would be potentially catastrophic for most organizations, institutions and industries. However, the fact that the nation’s hospitals and health systems continue to serve on the front lines of the ongoing pandemic is a testament to their resiliency and steadfast commitment to their mission to serve patients and communities around the country.

Hospitals and health systems are the cornerstones of their communities. Their patients depend on them for access to care 24 hours a day, seven days a week. Hospitals are often the largest employers in their community, and large purchasers of local services and goods. Additional support is needed to help ensure hospitals have the adequate resources to care for their communities.

I. Workforce and Contract Labor Expenses

The hospital workforce is central to the care process and often the largest expense for hospitals. It is no surprise then that even before the pandemic, labor costs — which include costs associated with recruiting and retaining employed staff, benefits and incentives — accounted for more than 50% of hospitals’ total expenses. Therefore, even a slight increase in these costs can have significant impacts on a hospital’s total expenses and operating margins.

As the pandemic has persisted for over two years, the toll on the health care workforce has been immense. A recent survey of health care workers found that approximately half of respondents felt “burned out” and nearly a quarter of respondents said they anticipated leaving the health care field.6

This has been mirrored by a significant and sustained decline in hospital employment, down approximately 100,000 employees from pre-pandemic levels.7 At the height of the omicron surge, approximately 1,400 hospitals or 30% of all U.S. hospitals reporting data to the government, indicated that they anticipated a critical staffing shortage within the week.8This high percentage of hospitals reporting a critical staffing shortage stayed relatively consistent throughout the delta and omicron surges.

The combination of employee burnout, fewer available staff, increased patient acuity and higher demand for care especially during the delta and omicron surges, has forced hospitals to turn to contract staffing firms to help address staffing shortages.

Though hospitals have long worked with contract staffing firms to bridge temporary gaps in staffing, the pandemic-driven-staffing-shortage has created an expanded reliance on contract staff, especially contract or travel registered nurses. Travel nurses are in particularly high demand because they serve a critical role in delivering care for both COVID-19 and non-COVID-19 patients and allow the hospital to meet the demand for care, especially during pandemic surges.

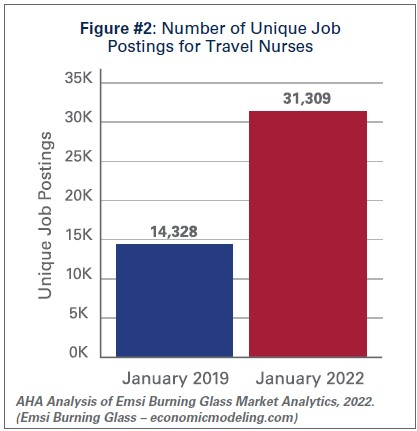

According to a survey by AMN Healthcare, one of the nation’s largest health care staffing agencies, 95% of health care facilities reported hiring nurse staff from contract labor firms during the pandemic.9Staffing firms have increased their recruitment of contract or travel nurses, illustrating the significant growth in their demand. According to data from EMSI/Burning Glass, there has been a nearly 120% increase in job postings for contract or travel nurses from pre-pandemic levels in January 2019 to January 2022. (See Figure #2)

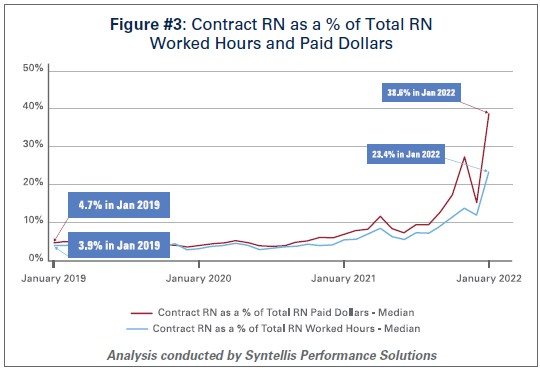

Similarly, the hours worked by contract or travel nurses as a percentage of total hours worked by nurses in hospitals has grown from 3.9% in January 2019 to 23.4% in January 2022, according to data from Syntellis Performance Solutions. (See Figure #3) In fact, a quarter of hospitals have experienced nearly a third of their total nurse hours accounted for by contract or travel nurses.

As the share of contract travel nurse hours has grown significantly compared to before the pandemic, so too have the costs of employing travel nurses compared to pre-pandemic levels. In 2019, hospitals spent a median of 4.7% of their total nurse labor expenses for contract travel nurses, which skyrocketed to a median of 38.6% in January 2022. (See Figure #3) A quarter of hospitals — those who have had to rely disproportionately on contract travel nurses — saw their costs for contract travel nurses account for over 50% of their total nurse labor expenses. In fact, while contract travel nurses accounted for 23.4% of total nurse hours in January 2022, they accounted for nearly 40% of the labor expenses for nurses. (See Figure #3) This difference has grown considerably compared to pre-pandemic levels in 2019, suggesting that the exorbitant prices charged by staffing companies are a primary driver of higher labor expenses for hospitals.

Data from Syntellis Performance Solutions show a 213% increase in hourly rates charged to hospitals by staffing companies for travel nurses in January 2022 compared to pre-pandemic levels in January 2019. This is because staffing agencies have exploited the situation by increasing the hourly rates billed to hospitals for contract travel nurses more than the hourly rates they pay to travel nurses. This is effectively the “margin” retained by the staffing agencies. During pre-pandemic levels in 2019, the average “margin” retained by staffing agencies for travel nurses was about 15%. As of January 2022, the average “margin” has grown to an astounding 62%. (See Figure #4)

These high “margins” have fueled massive growth in the revenues and profits of health care staffing companies. Several staffing firms have reported significant growth in their revenues to as high as $1.1 billion in just the fourth quarter of 202110, tripling their revenues and net income compared to 2020 levels.11

The data indicate that the growth in labor expenses for hospitals and health systems was in large part due to the exorbitant rates charged by contract staffing firms. By the end of 2021, hospital labor expenses per patient were 36.9% higher than pre-pandemic levels, and increased to 57% at the height of the omicron surge in January 2022.12 A study looking at hospitals in New Jersey found that the increased labor expenses for contract staff amounted to $670 million in 2021 alone, which was more than triple what their hospitals spent in 2020.13High reliance on contract or travel staff prevents hospitals and health systems from investing those costs into their existing employees, leading to low morale and high turnover, which further exacerbates the challenges hospitals and health systems have been facing.

II. Drug Expenses

Prescription drug spending in the U.S. has grown significantly since the pandemic. In 2021, drug spending (including spending in both retail and non-retail settings) increased 7.7%14, which was on top of an increase of 4.9%15 in 2020. While some of this growth can be attributed to increased utilization as patient acuity increased during the pandemic, a significant driver has been the continued increase in prices of existing drugs as well as the introduction of new products at very high prices. A study by GoodRx found that in January 2022 alone, drug companies increased the price of about 810 brand and generic drugs that they reviewed by an average of 5.1%.16 These price increases followed massive price hikes for certain drugs often used in the hospital such as Hydromorphone (107%), Mitomycin (99%), and Vasopressin (97%).17 For another example, the drug manufacturer of Humira, one of the most popular brand drugs used to treat rheumatoid arthritis, increased the price of the drug by 21% between 2019 and 2021.18 A study by the Kaiser Family Foundation found that in Medicare Part B and D markets, half of all drugs in each market experienced price increases above the rate of inflation between 2019 and 2020 – in fact, a third of these drugs experienced price increases of greater than 7.5%.19 At the same time, according to a report by the Institute for Clinical and Economic Review (ICER), eight drugs with unsupported U.S. drug price increases between 2019 and 2020 alone accounted for an additional $1.67 billion in drug spending, further illustrating that drug companies’ decisions to raise the prices of their drugs are simply an unsustainable practice.20

As hospitals have worked to treat sicker patients during the pandemic, they have been forced to contend with sky-high prices for drugs, many of which are critical and lifesaving for their patients. For example, in 2020, 16 of the top 25 drugs by spending in Medicare Part B (hospital outpatient settings) had price increases greater than inflation — two of the top three drugs, Keytruda and Prolia — experienced price increases of 3.3% and 4.1%, respectively.21

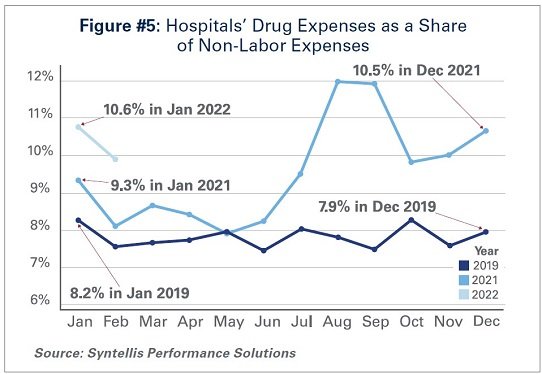

As a result of these price increases, hospital drug expenses have skyrocketed. By the end of 2021, total drug expenses were 28.2% higher than pre-pandemic levels.22 When taken as a share of all non-labor expenses, drug expenses have grown from approximately 8.2% in January 2019, to 9.3% in January 2021, and to 10.6% in January 2022. (See Figure #5) Even when considering changes in volume during the pandemic, drug expenses per patient compared to pre-pandemic levels in 2019 saw significant increases, with a 36.9% increase through 2021.

While continued drug price increases by drug companies have been a major driver of the growth in overall hospital drug expenses, there also are other important driving factors to consider:

Drug Treatments for COVID-19 Patients:Remdesivir, one of the primary drugs used to treat COVID-19 patients in the hospital, has become the top spend drug for most hospitals since the pandemic. This drug alone accounted for over $1 billion in sales in the fourth quarter of 2021.23 Priced at an average of $3,12024, Remdesivir’s cost was initially covered by the federal government. However, hospitals must now purchase the drug directly.

Limitation of 340B Contract Pharmacies: The 340B program allows eligible providers, including hospitals that treat many low-income patients or treat certain patient populations like children and cancer patients, to buy certain outpatient drugs at discounted prices and use those savings to provide more comprehensive services to the patients and communities they serve. Since July 2020, several of the largest drug manufacturers have denied 340B pricing to eligible hospitals through pharmacies with whom they contract, despite calls from the Department of Health and Human Services that such actions are illegal. Because of these actions, many 340B hospitals, especially rural hospitals who disproportionately rely on contract pharmacies to ensure access to drugs for their patients, have lost millions in 340B drug savings.25 In addition, these manufacturers have required claim-level data submissions as a condition of receiving 340B discounts, which has increased costs to deliver the data as well as staff time and expense to manage that process. The loss of 340B savings coupled with increased burden of providing detailed data to drug companies have contributed to increasing drug expenses.

Health Plans’/Pharmacy Benefit Managers’ (PBMs’) “White Bagging” Policies: Health plans and PBMs have engaged in a tactic that steers hospital patients to third-party specialty pharmacies to acquire medication necessary for clinician-administered treatments, known as “white-bagging.” This practice disallows the hospital from procuring and managing the handling of a drug — typically drugs that are infused or injected requiring a clinician to administer in a hospital or clinic setting — used in patient care. These policies not only create serious patient safety concerns, but create delays and risks in patient care; add to administration, storage and handling costs; and create important liability issues for hospitals.

Taken together, these factors increase both drug expenses and overall hospital expenses.

III. Medical Supply and PPE Expenses

The U.S., like most countries in the world, relies on global supply chains for goods and services. This is especially true for medical supplies used at hospitals and other health care settings. Everything from the masks and gloves worn by staff to medical devices used in patient care come from a large network of global suppliers. Prior to the global pandemic, hospitals had established relationships with distributors and other vendors in the global health care supply chain to deliver goods as necessitated by demand. After the pandemic hit, many factories, distributors and other vendors shut down their operations, leaving hospitals, which were on the front lines facing surging demand, to fend for themselves. In fact, supply chain disruptions across industries, including health care, increased by 67% in 2020 alone.26

As a result, hospitals turned to local suppliers and non-traditional suppliers, often paying significantly higher rates than they did prior to the pandemic. Between fall 2020 and early 2022 costs for energy, resins, cotton and most metals surged in excess of 30%; these all are critical elements in the manufacturing of medical supplies and devices used every day in hospitals.27 As COVID-19 cases surged, demand for hospital PPE, such as N95 masks, gloves, eye protection and surgical gowns, increased dramatically causing hospitals to invest in acquiring and maintaining reserves of these supplies. Further, downstream effects from other global events such as the war in Ukraine and the energy crisis in China, as well as domestic issues, such as labor shortages and rising fuel and transportation costs, have all contributed to drive up even higher overall medical supply expenses for hospitals in the U.S.28 For instance, according to the Health Industry Distributors Association, transportation times for medical supplies are 440% longer than pre-pandemic times resulting in massive delays.29

Compared to 2019 levels, supply expenses for hospitals were up 15.9%30 through the end of 2021. When focusing on hospital departments involved most directly in care for COVID-19 patients − primarily hospital intensive care units (ICUs) and respiratory care departments − the increase in expenses is significantly higher. Medical supply expenses in ICUs and respiratory care departments increased 31.5% and 22.3%, respectively. Further, accounting for changes in volume during surge and non-surge periods of the pandemic, medical supply expenses per patient in ICUs and respiratory care departments were 31.8% and 25.9% higher, respectively. (See Figure #6) These numbers help illustrate the magnitude of the impact that increases in supply costs have had on hospital finances during the pandemic.

IV. Impact of Rising Inflation

Higher economy-wide costs have serious implications for hospitals and health systems, increasing the pressures of higher labor, supply, and acquisition costs; and potentially lower consumer demand. Inflation is defined as the general increase in prices and the decrease in purchasing power. It is measured by the Consumer Price Index (CPI-U). In April 2021, the Bureau of Labor Statistics (BLS) reported that the CPI-U had the largest 12-month increase since September 2008. The CPI-U hit 40-year highs in February 2022.31 Overall, consumer prices rose by a historic 8.5% on an annualized basis in March 2022 alone.32

As inflation measured by consumer prices is at record highs, below are key considerations on the potential impact of higher general inflation on hospital prices:

Labor Costs and Retention: Labor costs represent a significant portion of hospital costs (typically more than 50% of hospital expenses are related to labor costs). As the cost-of-living increases, employees generally demand higher wages/total compensation packages to offset those costs. This is especially true in the health care sector, where labor demands are already high, and labor supply is low.

Supply Chain Costs: Medical supplies account for approximately 20% of hospital expenses, on average. As input/raw good costs increase due to general inflation, hospital supplies and medical device costs increase as well. Furthermore, shortages of raw materials, including those used to manufacture drugs, could stress supply chains (i.e., medical supply shortages), which may result in changes in care patterns and add further burden on staff to implement work arounds.

Capital Investment Costs: Capital investments also may be strained, especially as hospitals have already invested heavily in expanding capacity to treat patients during the pandemic (e.g., constructing spaces for testing and isolation of COVID-19 patients). One of the areas that has seen the largest increase in prices/shortages is building materials (e.g., lumber). Additionally, a historically large increase in inflation has resulted in increases in interest rates, which may hamper borrowing options and add to overall costs.

Consumer Demand: Higher inflation also may result in decreases in demand for health care services, specifically if inflation exceeds wage growth. Specifically, higher costs for necessities (food, transportation, etc.) could push down demand for health care services and, in turn, dampen hospital volumes and revenues in the long run.

Health care and hospital prices are not driving recent overall inflation increases. The BLS has cited increases in the indices for gasoline, shelter and food as the largest contributors to the seasonally adjusted all items increase. The CPI-U increased 0.8% in February on a seasonally adjusted basis, whereas the medical care index rose 0.2% in February. The index for prescription drugs rose 0.3%, but the hospital index for hospital services declined 0.1%.33

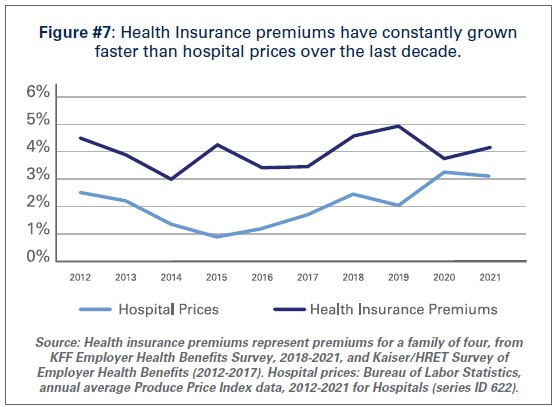

This is consistent with pre-pandemic trends. Despite persistent cost pressures, hospital prices have seen consistently modest growth in recent years. According to BLS data, hospital prices have grown an average 2.1% per year over the last decade, about half the average annual increase in health insurance premiums. (See Figure #7) More recently, hospital prices have grown much more slowly than the overall rate of inflation. In the 12 months ending in February 2022, hospital prices increased 2.1%. In fact, even when excluding the artificially low rates paid to hospitals by Medicare and Medicaid, average annual price growth has still been below 3% in recent years.34

Conclusion

While we hope that our nation is rounding the corner in the battle against COVID-19, it is clear that the pandemic is not over. During the week of April 11, there have been an average of over 33,000 cases per day35 and reports suggest that a new subvariant of the virus (Omicron BA.2) is now the dominant strain in the U.S.36As a result, the challenges hospitals and health systems are currently facing are bound to last much longer.

As COVID-19 infections and hospitalizations are decreasing in some parts of the U.S. and increasing in others, hospitals and health systems continue to care for COVID-19 and non-COVID-19 patients. With additional surges potentially on the horizon, the massive growth in expenses is unsustainable. Most of the nation’s hospitals were operating on razor thin margins prior to the pandemic; and now, many of these hospitals are in an even more precarious financial situation. Regardless of potential new surges of COVID-19, hospitals and health systems continue to face workforce retention and recruitment challenges, supply chain disruptions and exorbitant expenses as outlined in this report.

Hospitals appreciate the support and resources that Congress has provided throughout the pandemic; however, additional support is needed now to keep hospitals strong so they can continue to provide care to patients and communities.

Stanford Health Care and Lucile Packard Children’s Hospital administrators have notified union leaders that its nurse members who strike later in April risk losing pay and health benefits, according to Palo Alto Weekly.

The Committee for Recognition of Nursing Achievement, a union at Stanford Health Care and Stanford Children’s Health that represents about 5,000 nurses, has scheduled a strike to begin April 25. The nurses’ contract expired March 31.

If the strike moves forward, Stanford Health Care and the Lucile Packard Children’s Hospital, both based in Palo Alto, Calif., are prepared to continue to provide safe, quality healthcare, according to a statement from Dale Beatty, DNP, RN, chief nurse executive and vice president of patient care services for Stanford Health Care, and Jesus Cepero, PhD, RN, senior vice president of patient care and chief nursing officer for Stanford Children’s Health.

But the statement, which was shared with Becker’s, said nurses who choose to strike will not be paid for shifts they miss.

“In addition, employer-paid health benefits will cease on May 1 for nurses who go out on strike and remain out through the end of the month in which the strike begins,” Drs. Beatty and Cepero said.

The leaders quoted from Committee for Recognition of Nursing Achievement’s “contingency manual” that the union provided to nurses: “If a strike lasts beyond the end of the month in which it begins and the hospitals discontinue medical coverage, you will have the option to pay for continued coverage.”

Drs. Beatty and Cepero said nurses who strike may pay to continue their health coverage through the Consolidated Omnibus Budget Reconciliation Act.

In a separate statement shared with Becker’s, Committee for Recognition of Nursing Achievement President Colleen Borges called Stanford and Packard management’s move regarding nurses’ health benefits “cruel” and “immoral.”

“Health benefits should not be used against workers, especially against the very healthcare professionals who have made Stanford a world-class health system,” said Ms. Borges, who is also a pediatric oncology nurse at Lucile Packard Children’s Hospital. “We have spent our careers caring for others and putting others first — now more than ever we need solutions that will ensure sustainability, safe staffing and strong benefits to retain nurses. But instead of taking our proposals seriously, hospitals are spending their time and energy weaponizing our medical benefits. We refuse to be intimidated from standing up for the fair contracts that we need in order to continue delivering world-class patient care.”

The union has organized a petition to tell Stanford not to cut off medical benefits for nurses and their families during the strike. As of April 19, the petition had more than 25,150 signatures.

Sacramento-based Sutter Health said nurses who went on strike April 18 will not be allowed to return to work until the morning of April 23, the San Francisco Chronicle reported.

The strike affected nurses and healthcare workers at Sutter Health facilities in Northern California. The nurses are members of the California Nurses Association, and the other workers are members of the Caregivers and Healthcare Employees Union, an affiliate of the California Nurses Association.

More than 8,000 registered nurses and healthcare workers were expected to participate in the strike, according to an April 18 news release from the unions.

In a statement shared with Becker’s, Sutter Health said the organization conducted strike contingency planning, which included “securing staff to replace nurses who have chosen to strike, and those replacement contracts provide the assurance of five days of guaranteed staffing amid the uncertainty of a widespread work stoppage.”

“As always, our top priority remains safe, high-quality patient care and nurses may be reinstated sooner based on operational and patient care needs,” the statement said.

The California Nurses Association described Sutter Health’s decision as retaliatory, as well as “completely unnecessary and vindictive.”

“Nurses who are regularly scheduled to work during this lockout period will lose those days of pay,” the union said in a statement shared with Becker’s. “We urge Sutter to respect the nurses’ strike and let all nurses return to work.”

Sutter Health workers authorized a strike in March, and union officials announced an official strike notice April 8. Union members cited lack of transparency about the stockpile of personal protective equipment supplies and contact tracing as a reason for the strike. They also said they seek a contract that will help retain experienced nurses and provide sufficient staffing and training.

Nurses have been in contract negotiations since June.

Businesses who suffered from the Great Resignation, in which large numbers of workers voluntarily resigned during the pandemic looking for more fulfilling work or higher wages, are now hoping the “Great Regret” might bring workers back. According to recent surveys, over 70 percent of workers who switched employment during the pandemic found that their new jobs didn’t live up to their expectations, and nearly half wish they had their old job back.

After scores of nurses left hospital positions for travel roles, health system leaders are seeing some nurses return. One physician told us about a favorite nurse on his oncology unit who returned from over a year as a traveler, ready to settle down and be closer to family.

A chief nursing officer relayed that her system was seeing nurses who took agency positions to work toward personal financial goals, like earning a down payment for a house, wanting to come back now that they’ve reached it: “Travel roles are intense, and most nurses can’t do them forever”.

But other nursing leaders caution that they’re preparing for agency nurses to become a permanent fixture in the workforce: “More nurses will see travel as an option for different points in their career, when they have personal flexibility or need the extra money”.

The “Great Regret” might help some hospitals lessen their reliance on agency nursing in the short-term. But building a stable clinical workforce will require addressing underlying structural challenges, through changes in education, rethinking job roles and care models, and finding ways to build individualized job flexibility and customization.

UPDATE: April 14, 2022: Nurses will begin striking April 25 if they are unable to reach a deal with the system by then, according to a Wednesday statement from the union. The two sides have met with a federal mediator three times, and the strike would be open-ended.

Dive Brief:

Unionized nurses at Stanford hospitals in California voted in favor of authorizing a strike Thursday, meaning more than 4,500 nurses could walk off the job in a bid for better staffing, wages and mental health measures in new contracts.

Some 93% of nurses represented by the Committee for Recognition of Nursing Achievement voted in favor of the work stoppage, though the union did not set a date, according to a union release. It must give the hospitals 10 days notice before going on strike.

Nurses’ contracts expired March 31 and the union and hospital have engaged in more than 30 bargaining sessions over the past three months, including with a federal mediator, according to the union.

Dive Insight:

As the COVID-19 pandemic has worsened working conditions for nurses, some unions have made negotiating contracts a priority. Better staffing is key, along with higher wages and other benefits to help attract and retain employees amid ongoing shortages.

The California nurses’ demands in new contracts focus heavily on recruitment and retention of nursing staff “amid an industry-wide shortage and nurses being exhausted after working through the pandemic, many in short-staffed units,” the union said in the release.

They’re also asking for improved access to time off and more mental health support.

Nurses say their working conditions are becoming untenable and relying on travel staff and overtime shifts is not sustainable, according to the release.

The hospitals are taking precautionary steps to prepare for a potential strike and will resume negotiations with the union and a federal mediator Tuesday, according to a statement from Stanford.

But according to CRONA, nurses have filed significantly more assignment despite objections documents from 2020 to 2021 — forms that notify hospital supervisors of assignments nurses take despite personal objections around lacking resources, training or staff.

And a survey of CRONA nurses conducted in November 2021 founds that as many as 45% were considering quitting their jobs, according to the union.

That’s in line with other national surveys, including one from staffing firm Incredible Health released in March that found more than a third of nurses said they plan to leave their current jobs by the end of this year.

The CRONA nurses “readiness to strike demonstrates the urgency of the great professional and personal crisis they are facing and the solutions they are demanding from hospital executives,” the union said in the release.

No major strikes among healthcare workers have occurred so far this year, though several happened in 2021 and in 2020, the first year of the pandemic.

The Great Nursing Resignation, and hospitals’ growing reliance on expensive agency labor (a.k.a. “travelers”) has grabbed headlines, for good reason. But lately we’ve heard a couple of anecdotes from health system leaders about the second-order impacts of the phenomenon that are worth considering as well.

First, as the ranks of agency nurses at hospitals have swelled, full-time employed nurses’ morale has plummeted—tenured nurses are having to orient their new temporary co-workers, then watch them earn up to three times as much money for the same work.

At the same time, willingness to work overtime among employed nurses has dropped. That’s not just because of burnout—it turns out that the nurses who were most likely to take overtime shifts are also more likely to have chosen to leave full-time employment to become travelers, where they are even more richly rewarded for working extra shifts. So, the “productivity” of the remaining corps of staff nurses has dropped, even as caseloads have increased.

One other implication we’ve heard about recently: the economic impact of “observation” cases, where patients are held in a staffed bed but not admitted—already a bad bargain for hospitals—has gotten worse. That’s because the cost of deploying staff to care for those patients has gone up, due to wage inflation and use of travelers. It’s hard to overstate the level of staffing crisis at most hospitals today, and the rapid growth in reliance on temporary staff will have consequences lasting well beyond the current surge.