-

Rural hospitals seen as among hardest hit by regulatory change

-

Technological shifts and urgent care reshaping industry

A growing number of health-care companies may face near-death experiences of their own.

“Smaller hospitals have already been struggling for years,” said Kristin Going, a partner in the New York office of Drinker, Biddle & Reath LLP. Both lawyers declined to discuss specific companies. Since 2010, a growing number of patients have enrolled in high-deductible health plans that force them to shoulder more of costs when they get treatment, according to the U.S. Centers for Disease Control and Prevention. That has translated into more bad debt from customers for hospitals and other providers.

Some publicly traded hospital companies that were already under pressure from high debt loads have been further buffeted by this year’s hurricanes. Community Health Systems Inc., with $1.9 billion in debt maturing in 2019, has suffered doctor revolts over crumbling, cash-strapped facilities, as well as losses linked to the storms in Texas and Florida earlier this year. A representative for Community Health didn’t return a call seeking comment.

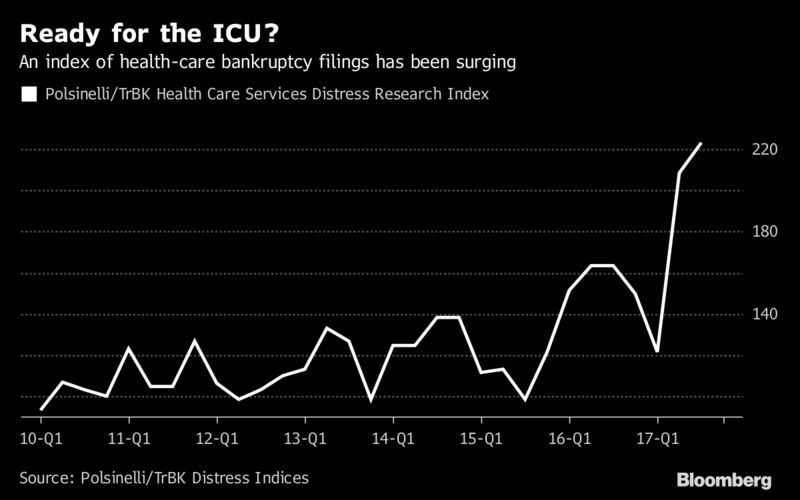

Signs of Distress

Jorian Rose, partner in the New York office of Baker & Hostetler LLP, said many health-care restructurings are already going on under the radar right now. Rose, Going and Neier are members of the Turnaround Management Association, a group for bankruptcy and restructuring professionals.

The Polsinelli Health Care Services Distress Research index, which tracks bankruptcy filings for companies with more than $1 million in assets, shows that activity has surged 123 percent since the fourth quarter of 2010. By comparison, the law firm said, the general index that tracks Chapter 11 filings in the U.S. is down nearly 58 percent from 2010. The Affordable Care Act, which Republican lawmakers have been looking to repeal, replace, defund, or otherwise change, was cited as one of the systemic changes rocking the sector.

Since 1997, health-care cases have made up only 5.25 percent of all U.S. bankruptcy filings, according to Bloomberg data. Year to date, they already comprise 7.25 percent of all filings. Emergency-room operator Adeptus Health, cancer-care provider 21st Century Oncology, and cancer treatment specialist California Proton Treatment are the largest filings. Those statistics exclude pharmaceutical company Concordia, which is restructuring in Canada, and Preferred Care Inc., one of the U.S.’s largest nursing home groups, operating 108 assisted living facilities.

Problems for the sector aren’t limited to U.S. companies. Israeli drugmaker Teva Pharmaceutical Industries Ltd., saddled with debt that’s more than double its market value, is putting together a “detailed restructuring plan” after the company has slashed its profit forecasts, cut its dividend, signaled it may sell new shares, and reduced its goal for paying down debt this year. It announced a management shakeup on Monday.

Distress among health-care companies can spread to other parts of the economy. Quality Care Properties Inc., for example, is a real estate investment trust with a struggling tenant, HCR Manorcare Inc. Moody’s Investors Service said in an October report that if HCR Manorcare files for bankruptcy, Quality Care could also need to amend the terms of its own debt. Representatives for HCR Manorcare and Quality Care didn’t return calls seeking comment.