I know plenty of people who are politically right-of-center – and they want to rein in Big Insurance just as much as people to the left.

Some of my closest family and friends have nearly polar opposite political beliefs than mine. And these are not family members I’m only with on holidays (like during Thanksgiving dinner later this week) or friends I only see on Facebook. These are people I love and communicate with weekly — sometimes daily. They’re my people.

And I’d say that my people largely fall into two distinct right-of-center sub groups:

The first group:

USDA grass-fed Trump supporters who like Jeanine Pirro and Blue Lives Matter bumper stickers.

And the second group:

Nonpolitical and anti-establishment 20-30 somethings who make their own beef-tallow.

(And both groups are patient enough to keep a Bernie-t-shirt-owning-lib, who listens to The Daily (like myself) in their lives.)

We don’t all agree on vaccines. We don’t all agree on the Gulf of America. And none of them agree with my mullet. But what we all do agree on is that through backroom deals and moneyed influence, big corporations pull Washington’s levers and squeeze American families at every chance they get – all to make their Wall Street investors and executives richer. And, as readers of HEALTH CARE un-covered undoubtedly know, Big Insurance may be the perfect example of those deals and influence.

That’s where my people and I meet in our venn diagram. While we have many sticking points, Big Insurance is not one of them.

And this is not just qualitative on my end. Poll after poll proves that my people are not the exception to the rule. An October KFF poll showed that a majority of Republicans who align with the MAGA movement (57%) said Congress should have extended the enhanced premium tax credits for Affordable Care Act (ACA) plans, and a new study by Undue Medical Debt found that 62% of Republicans blame health insurance companies the most for the medical debt crisis in the country.

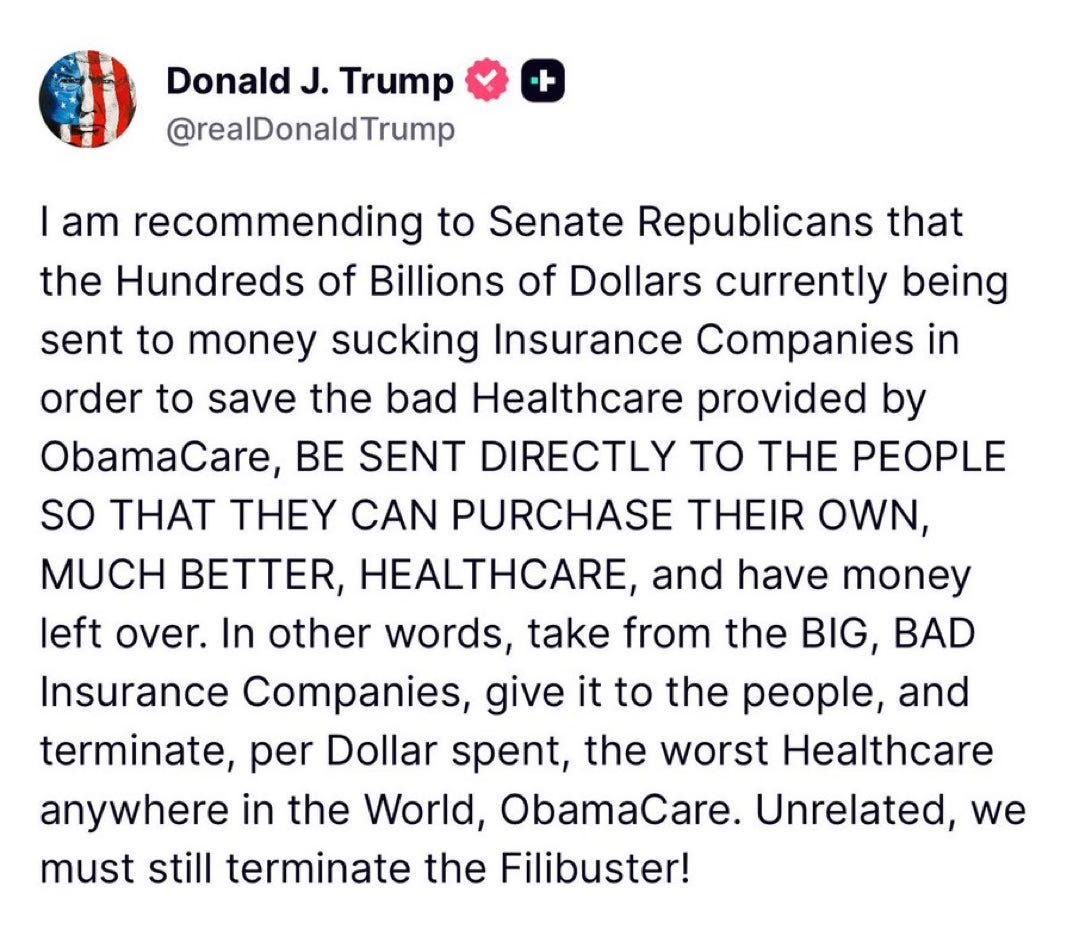

The deeds of the health insurance industry have grown so rotten and their stench so unavoidable that even the President has caught a whiff. On Truth Social last month, President Trump posted about “BIG,” “BAD” and “Money sucking” health insurance companies. His message reverberated in the media and on Wall Street and helped bring this issue even more to the forefront.

But here’s the thing: Trump’s post isn’t the tip of the spear but rather the caboose following a long train of Republicans (and their voters) who as of late have begun to focus on Big Insurance. In the last six months, we’ve seen Representative Marjorie Taylor Green call on Republicans to take on Big Insurance, former Representative Mark Green (R-TN) introduce legislation to crack down on Big Insurance’s prior authorization tactics, and Pam Bondi’s Department of Justice open a criminal investigation into UnitedHealth Group’s Medicare Advantage business – all moves that have been historically uncharacteristic of their political bents but nonetheless are, in one way or another, raising the heat on Big Insurance.

If the latest news out of Washington tells us anything, it’s that conservatives are largely on the same side as many of the most liberal voices when it comes to health insurance reforms.

While my people may not speak the same health care language or advocate the exact same solutions that many health care reform advocates or left-of-center folks would raise, the differences are largely just in the terminology used. For instance, my people are not going to mention Medicare for All or a public option as an answer to our country’s health care woes. Those phrases have been carefully tarred and feathered by the insurance industry as “socialism” to hold back both centrist and Republican voters and policymakers from putting guardrails in place that would cut into the industry’s immense profits. But again, it’s the terminologies that have been discredited – not the sentiment behind them.

On more than one occasion, when talking with my people about health insurers, they have straight-up volunteered that they think “insurance companies should be outlawed.” That belief, last time I checked, was to the left of even Senators Elizabeth Warren and Bernie Sander’s proposals to finally establish universal coverage for every American by expanding Medicare to cover all of us.

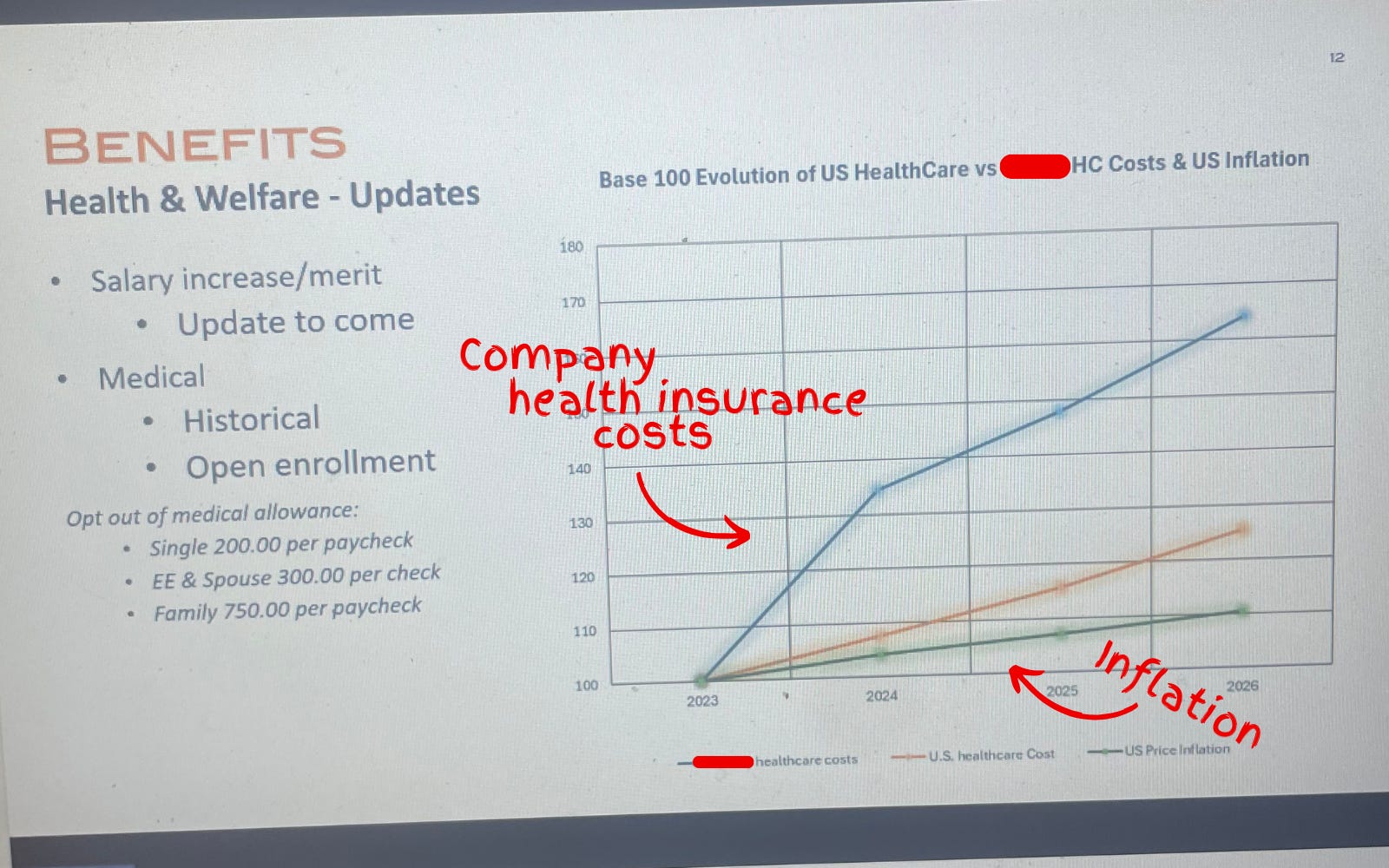

Another one of my people, who handles financials for the North American-sector of a sizable global company in the home-technology space, FaceTimed me last week to show me his computer screen while he was crunching the companies’ health care costs.

In anticipation for a company-wide town hall, he had to make a slide showing that the health insurance costs for his company’s U.S.-side had increased (on average) 20% over the past several years – including a projected 25% jump in 2026. He couldn’t believe it. “Show this to Wendell,” he said.

And that’s the thing:

Nobody can believe how out-of-control Big Insurance has become.

Where my people and I meet

It’s fair to say that I think more about health care policy than the average bear. And it’s true that my people have had me in their ear talking about these issues for nearly a decade. But as I noted above, polling shows that while certain solutions may not be as popular, the desire for action is clear and exists sans my yapping.

Over years of conversations, there have been some major themes that have stuck. I will list them below:

- Big Insurance is the villain in health care: With its army of slick lobbyists and spokesmen on TV, Big Insurance is the epitome of the D.C.-swamp monster that so many Americans disdain. Between 2014 and 2024, just seven for-profit health insurers amassed $543.4 billion in profits (of which they spent $618 million on lobbying during that time) all while 100 million Americans owe $220 billion in medical debt and Americans’ life expectancy is ranked 48th in the world.

- Big Insurance and it’s cushy government handouts: Nearly all of Big Insurance’s growth has come from contracts it engineers with the federal and state governments in the form of managing Medicaid, Medicare Advantage and some Veteran health services. These contracts are not the invisible hand of the free market but rather cushy government handouts that have allowed just seven for-profit health insurance conglomerates to capture $10.192 trillion in revenues between 2014 and 2024.

- Big Insurance’s business practices: Health insurance companies like UnitedHealth Group, Cigna and Aetna deploy rigid artificial intelligence (AI) programs to sideline doctors and automate denials, offshore jobs and employ folks in India and the Philippines to deny American’s care while they use American’s premium and tax dollars to boost million dollar C-suite compensation packages and buy back their own stocks.

- Big Insurance has grown too big: Big Insurance companies are buying up the entire health care landscape – from physician practices to pharmacies. That is why independent physicians are an endangered species and why an independent pharmacy closes nearly every day in this country.

- Big Insurance hurts the little guy: American small businesses often see double-digit yearly increases in health insurance costs that stifle Main Street America’s growth and stop Americans from being entrepreneurs altogether. And, not to mention, if businesses weren’t being raked over the coals for more premium dollars year after year, more money could be paid to workers.

I included this list because I think we are at a watershed moment in the health care debate and reforming Big Insurance is no longer a wedge issue. It’s a bridge issue.

I don’t know what comes next

Because the long standoff between Republicans and Democrats to open the government finally came to an end this month – without the ACA subsidy extensions – Big Insurance reform (and health care reform broadly) has become an unaddressed priority in American politics.

In the current moment, if Republican electeds were smart, they’d read the writing on the wall and focus on rooting out an actual source of widespread waste, fraud and abuse found in health insurance companies’ private Medicare Advantage, Medicaid and military businesses. That’s an issue that polls incredibly well with conservatives. Just tackling Medicare Advantage, for example, could save taxpayers somewhere between $80 and $140 billion annually. For reference, the DOGE website claims it has only clawed back $214 billion in total since January.

Republicans could also work with their political opposites (and fulfill a campaign promise) to pass a worthwhile health insurance reform package that builds on (or possibly replace) the consumer protections of ACA and fills the loopholes of well-intended rules that have been exploited and manipulated by Big Insurance.

And it wouldn’t be a one-party trick. For what it’s worth, I think most Democrats in Washington would be on board with anything that lessens the corporate grip Big Insurance has on our country’s public programs and improves the ACA. In the last year, we’ve already seen Democrats link with the country’s current controlling party to introduce bills that would bring meaningful change to Big Insurance:

- Senators Elizabeth Warren (D-MA) and Josh Hawley (R-MO) introduced legislation that would stop health insurance companies from owning pharmacy benefit managers (PBMs);

- Senators Jeff Merkley (D-OR) and Bill Cassidy, M.D. (R-LA) introduced the No UPCODE Act to curb taxpayer-sponsored overpayments to health insurers; and

- Representatives Nannette Barragan (D-CA) and Mariannette Miller-Meeks, M.D. (R-IA) (among other legislators) reintroduced The DRUG Act to stop insurance companies from driving up drug prices.

These unlikely partnerships in Washington are happening because what my people (and all people) want is a health insurance system that guarantees comprehensive coverage for all of us, without forcing folks to choose between biopsies or groceries. Everybody I know – left, right and in between – wants a health care system that doesn’t bury families under mountains of medical bills or force them to attend unnecessary funerals. And all rational people want an insurance system that doesn’t buy off its buddies in Washington to serve their Wall Street daddies.

I want to scream from the mountaintops that health insurance reform is not just a moral or economic issue. It’s a winning issue.

Americans have had it. Most of Washington seems motivated. And now is the time for health care, patient and consumer advocates to change their tune and stop (just) preaching to the choir. Advocates for reform need to get their message to the corners of the country that they may have written off — or found too difficult to bridge — because the ground for health care reform is fertile for change. And I think all people are ready.

Thanksgiving is in a few days. And in times of heightened political polarization, the dinner table – filled with folks sharing a myriad of different opinions – can become a battleground between courses of mashed potatoes and pumpkin pie. But if I can gleam anything from what I see as a bi-partisan kumbaya against Big Insurance, it’s that even with all the reported divisiveness, we have one less thing to argue about.

And because of that – I don’t know what comes next – but what I do know is that the 2026 midterms and the 2028 presidential election will be about health insurance reform. And whichever political party takes that seriously is going to seize the day.