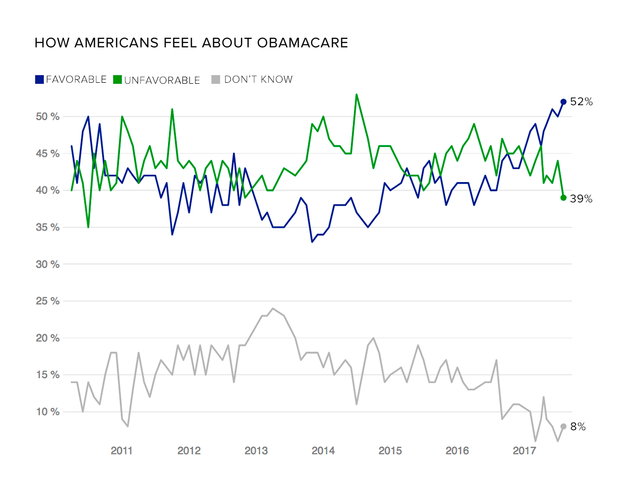

The Trump administration said on Thursday that it would slash spending on advertising and promotion for the Affordable Care Act, but it has already been waging a multipronged campaign against it.

Despite several failed efforts by Republican lawmakers to repeal it, the Affordable Care Act remains the law of the land. But the Department of Health and Human Services — an agency with a legal responsibility to administer the law — has used taxpayer dollars to oppose it.

Legal experts say that while it is common for a new administration to reinterpret an existing law, it is unusual to take steps to undermine it. Here are three ways the health department has campaigned against Obamacare.

1. REDIRECTING PROMOTIONAL FUNDING

Instead of using its outreach budget to promote the Affordable Care Act, the department made videos critical of the law.

In June, the health department posted 23 video testimonialson YouTube from people who said they had been “burdened by Obamacare,” including families, health care professionals and small business owners.

While it’s not certain where the money for the videos came from, several former health officials who worked in the Obama administration said that they suspect it came from the budget meant to promote the Affordable Care Act.

“There’s no other budget that makes sense,” said Lori Lodes, who oversaw outreach efforts under Mr. Obama.

The Trump administration defended the videos, saying that they were produced to inform Americans about the need for change so that people would have access to affordable health care.

“As evidenced by these important and educational testimonials, the status quo has made that impossible for millions of Americans,” a department spokeswoman, Alleigh Marré, said in July. “The administration is committed to reforming the current health care system to bring down the cost of coverage, expand health care choices, and strengthen the safety net for generations to come.”

The Daily Beast reported in July that one of the participants in the videos said he felt he was being pushed “for a harder line against Obamacare.”

While the health department refers to these testimonials as “educational videos” produced to inform Americans on the need to overhaul health care, some experts question whether they fit that definition.

“The lines between what is partisan, what is propaganda, and what is educational are nightmarish and subjective,” said Michael Eric Herz, a professor at the Cardozo School of Law in New York who has written about social media and the government.

2. ATTACKING THE LAW

The department targeted the Affordable Care Act with a marketing campaign as Republicans in Congress tried to repeal the legislation.

In addition to the YouTube videos, the department has used Twitter and news releases to try to discredit the health law. Since being sworn in as health secretary on February 10, Tom Price has posted on Twitter 48 infographics advocating against Obamacare, all of which bear the health department’s logo.

“Here, it’s an agency trying to destroy its own program because it opposes it,” said Kathleen Clark, a law professor at Washington University who is an expert on government ethics. “It is inconsistent with the constitutional duty to take care that the law is faithfully executed.”

The bulk of Mr. Price’s Twitter posts were from late June to mid-July, when Senate Republicans were trying to pass a bill to repeal and replace the Affordable Care Act. Once, Mr. Price tweeted five infographics in a single day.

Around the same time, the Trump administration ended $23 million worth of contracts with companies that help people sign up for coverage.

In August, five congressional Democrats wrote a letter to Mr. Price demanding detailed information about his plans for marketing and outreach. “Rather than encouraging enrollment in the marketplaces, the administration appears intent on depressing it,” the letter said.

3. DELETING INFORMATION ONLINE

The department removed useful guidance for consumers about the Affordable Care Act from its website.

Under the Obama administration, the health department’s website contained information to help consumers learn about the Affordable Care Act and how to obtain coverage through the health insurance marketplaces. Much of that information is now gone. Some was removed within hours of President Trump’s inauguration.

A link to a page about the Affordable Care Act disappeared from the health department’s home page the evening of the inauguration, according to a comparison of the sites, shown below.