Reproduced from Kaiser Family Foundation analysis of the 2016 Survey of Consumer Finance; Note: Liquid assets include the sum of checking and saving accounts, money market accounts, certificates of deposit, savings bonds, non-retirement mutual funds, stocks and bonds; Chart: Axios Visuals

A lot of low-income families can’t afford even a moderate deductible, yet deductibles continue to rise in almost all forms of insurance, Kaiser Family Foundation president Drew Altman writes in his latest Axios column.

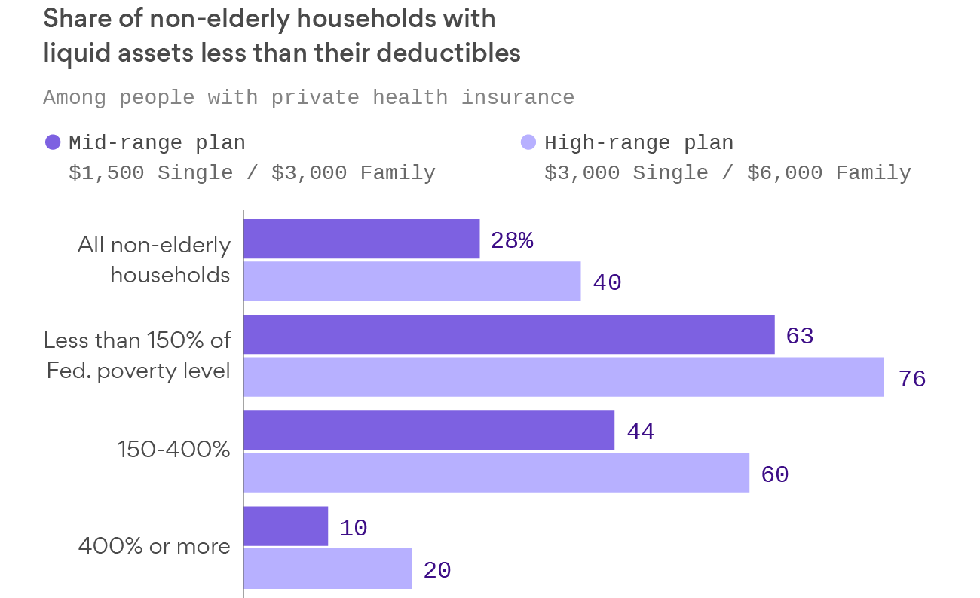

- Roughly 40% of all non-elderly households don’t have enough liquid assets to cover a high deductible ($3,000 for an individual or $6,000 for a family).

- Among families whose income makes them eligible for the ACA’s premium subsidies, 60% don’t have enough liquid assets to cover a high deductible and 44% couldn’t cover the deductible for a mid-range plan ($1,500 for an individual or $3,000 for a family).

Why it matters: High deductibles are everywhere, and they’re only getting higher. Many ACA plans have relatively big deductibles and Republicans’ alternatives would push them higher. They’ve been getting bigger and bigger in employer plans, too.

- “For many families, even if they have insurance, any significant illness could wipe out all their savings, making impossible to fix a broken car to get to work, or pay for school, or make a rent or mortgage payment,” Altman says.