Cartoon – Prescription Plan Coverage

https://www.bloomberg.com/view/articles/2017-03-17/the-wrong-way-to-lower-health-insurance-premiums

For proponents of the American Health Care Act, perhaps the most encouraging nugget in the Congressional Budget Office’s otherwise critical analysis is that insurance premiums could fall by 10 percent on average by 2026. Even this prediction is more mirage than reality, however, in part because of an obscure concept known as “actuarial value.”

As many opponents of the Republicans’ Obamacare replacement legislation have already noted, for many people, the decline in premiums would be smaller than the cutback in their subsidies, so they would still end up paying more. And in any case, the predicted fall in premiums partly reflects a troubling rise in the share of older Americans without insurance, a change that would shift the enrollment pool to younger, less expensive beneficiaries.

Another factor, however, has received less attention, though it is hidden in plain sight in the CBO analysis: The premium reduction would occur in no small part because the insurance products wouldn’t be as good. In other words, their actuarial value would fall.

An insurance policy’s actuarial value is the share of total health-care costs paid by the plan rather than the policy holder, through deductibles and copayments. A plan with an actuarial value of 80 percent will pick up, on average, 80 percent of the cost of care. Plans with higher actuarial values have higher premiums, not surprisingly, because they provide deeper insurance. And if a plan’s actuarial value is very low, it may not really qualify as insurance at all.

The Affordable Care Act sets minimum actuarial values for each of the four tiers of plans that can be sold on the exchanges; the lowest, for bronze plans, is about 60 percent. The new legislation would repeal these minimums.

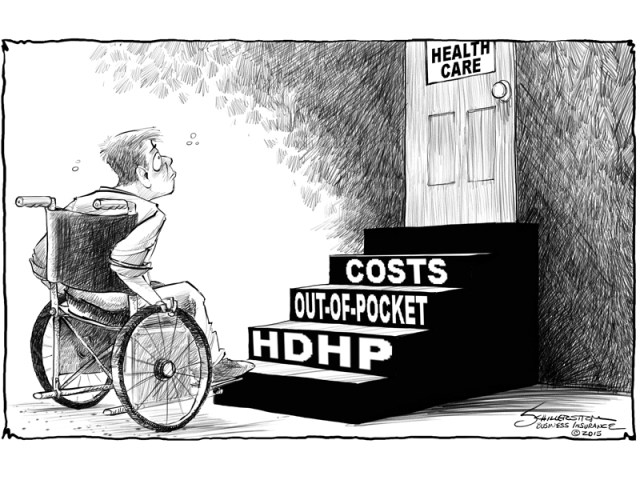

To see how big a deal this is, it is instructive to study the table toward the end of the CBO’s analysis, which calculates premiums under current law and under the AHCA. A 40-year-old single person could see his or her premium fall 7 percent — to $6,050, from $6,500. That’s only slightly less than the average 10 percent premium decline. Yet the actuarial value of the person’s plan would decline to 65 percent, from 70 percent or 87 percent, depending on his or her income.

To get some sense of what these lower actuarial values mean in terms of higher deductibles, we can look to the most recent Centers for Medicare and Medicaid Services calculator. It suggests that a plan with a $1,500 deductible, an 80 percent coinsurance rate (the plan pays 80 percent of costs above the deductible and below the maximum out-of-pocket threshold), and a $7,200 maximum out-of-pocket limit would have an actuarial value of 73 percent. The same plan with a $5,000 deductible would have an actuarial value of 61 percent. In other words, a decline in actuarial value of about 12 percentage points (not far from the average decline in the CBO examples) would raise the policy’s deductible by $3,500.

It’s no wonder that the premium for such a plan would be lower — in the same way that it’s no wonder a 12-ounce can of soda costs less than a 35-ounce bottle. It’s no great accomplishment to lower premiums by increasing other consumer costs.

As the CBO concluded, under the Republicans’ system, “individuals’ cost-sharing payments, including deductibles, in the nongroup market would tend to be higher than those anticipated under current law.” Indeed, according to an analysis from the Center for American Progress, average total costs to consumers would be significantly higher.

If you think that competition can fix this, note another problem that the CBO points out: Under Obamacare, the actuarial value requirements allow for easy comparison shopping; plan A can be directly compared with plan B. Under the Republican system, it would be harder to shop for a policy based on price.

Health-care reform is indeed complicated. Esoteric concepts like actuarial value have big effects on every family’s bottom line.

Senator Robert Byrd helped save the Affordable Care Act once already. In December 2009, the wizened West Virginia Democrat overcame fragile health to cast a crucial vote for the act’s passage. It was one of the last votes in the career of the Senate’s longest-serving member: Just weeks after President Obama signed the Affordable Care Act into law, Byrd died at age 92.

Now, nearly seven years after his death, Senator Byrd may ensure that the Affordable Care Act, also known as Obamacare, lives another day. One of Byrd’s many legislative accomplishments over a half-century in the Senate was the eponymous “Byrd rule,” which governs the process of budget reconciliation. Republicans on Capitol Hill are trying to use the reconciliation process to repeal and replace the Affordable Care Act. The Byrd rule stands in their way.

Reconciliation is a fast-track process that allows budget-related legislation to pass the Senate without the prospect of a filibuster. The Byrd rule prevents reconciliation from being used to pass any measure for which the budgetary effects — “changes in outlays or revenues” — are “merely incidental to the non-budgetary components.” Republicans know they lack the 60 votes to break a filibuster in the Senate, so they designed their repeal-and-replace bill to satisfy the Byrd rule’s requirements. Yet there is a surprising flaw in their design — one that has so far drawn little notice, but that Senate Democrats will surely seize on.

The flaw is found in a provision of the bill with the innocuous title “Encouraging Continuous Health Insurance Coverage.” Under that provision, individuals who go without coverage for more than two months must pay a penalty the next time they buy health insurance. The penalty is equal to 30 percent of their new plan’s premium. Significantly, individuals must pay this 30 percent penalty to their new insurer, not to the federal government.

And therein lies the problem. If the penalty were paid to the federal government, as with the individual mandate penalty under the Affordable Care Act, the provision would comply with the Byrd rule because it would have an obvious positive budgetary effect: Penalty payments would increase federal revenues. But the drafters of the repeal-and-replace bill chose not to adopt that approach, lest the penalty look too much like the Obamacare mandate. Instead, they are hoping that the threat of a future penalty averts an insurance market “death spiral,” in which healthy individuals run for the exits and the sick are left behind.

http://www.nejm.org/doi/full/10.1056/NEJMp1615696?query=featured_home&

Medicaid’s introduction also generated large benefits. Medicaid reduced mortality among infants and children, provided financial protection for their families, and led to better health, higher employment, and lower use of public benefits when they grew up. Moreover, by increasing tax revenue and reducing cash transfers, Medicaid currently saves federal and state governments $21 billion per year.5

How do these historical policies compare with today’s Medicaid-reform proposals? Ryan’s proposed caps apply only to Medicaid spending and recipients, since Medicaid was long ago decoupled from cash welfare. The cap amounts would initially equal average 2016 Medicaid spending by eligibility category and by state, rather than a single statutorily defined amount. Yet the caps would be “set to grow more slowly than under current law,” so over time they cease being related to actual Medicaid costs, thereby limiting the ability of states to adjust to rapid advances in technology, epidemics, or other unforeseen events. Nevertheless, as in the 1950s, discouraging Medicaid recipients from receiving costly care or keeping the highest-cost patients out of the program would be the clearest ways to limit state outlays. Toward that end, the Ryan plan would allow states to impose work requirements, charge premiums, offer a limited benefit package, shift beneficiaries into the individual insurance market, and create enrollment caps or waiting lists.

Medicaid creates a divisive relationship between the federal and state governments. Federal mandates and open-ended federal cost sharing are meant to provide incentives for state spending, but states often balk at the large costs. Both state and federal budgets would benefit if each Medicaid recipient cost less. Unfortunately, a per capita cap on federal Medicaid spending is unlikely to achieve this aim. Rather than “modernize” Medicaid, the historical experience in the United States suggests per capita caps would simply shrink the program.

What goes on the chopping block: Research into cancer or Alzheimer’s? A Zika vaccine or a treatment for superbugs?

Health groups say President Donald Trump’s proposal to slash funds for the nation’s engine of biomedical research would be devastating for patients with all kinds of diseases — and for jobs.

“It is possible that the next cure for some cancer is sitting there waiting to be discovered, and it won’t get to the table,” said Dr. Georges Benjamin, executive director of the American Public Health Association.

In his budget blueprint Thursday, Trump called for a cut of $5.8 billion from the National Institutes of Health. That’s a staggering 18 percent drop for the $32 billion agency that funds much of the nation’s research into what causes different diseases and what it will take to treat them.

It comes despite Trump recently telling Congress about the need to find “cures to the illnesses that have always plagued us.”

“All of us woke up this morning in a state of shock about this number,” said Dr. Blase Polite, a cancer specialist at the University of Chicago who chairs the American Society for Clinical Oncology’s government relations committee.

Trump’s proposal would roll back NIH’s 2018 budget to about what it was in 2003. The president called for a “major reorganization” of NIH to stress the “highest priority research,” but only specifically targeted for elimination the $69 million Fogarty International Center that focuses on global health and has played a big role in HIV research abroad.

Drops in deaths from cancer and heart disease, breakthroughs in genetics, and new ways to treat and prevent HIV and other infectious diseases all are credited to decades of NIH-funded basic research.

GOP’s 3-Bucket Strategy To Repeal And Replace Health Law Is Springing Leaks

Republicans in Washington working to overhaul the Affordable Care Act say their strategy consists of “three buckets.” But it appears that all three may be leaking.

The plan to dismantle and replace Obamacare emerged after the Republican congressional retreat in late January. The first bucket is a fast-track budget bill that needs only a simple majority to pass the Senate. Because of congressional rules, however, it can only address parts of the health law that have immediate impact on federal spending.

The second consists of changes to regulations and other policies put in place by the Obama administration that could theoretically be undone by new Health and Human Services Secretary Tom Price. And the third is separate legislation that would do things Republicans have been advocating for many years, such as imposing caps on medical malpractice damages and selling health insurance across state lines.

All three are proving problematic at this point — among Republicans.