1917 Hospital Ambulance

https://www.medpagetoday.com/publichealthpolicy/healthpolicy/69102?pop=0&ba=1&xid=fb-md-pcp

The market economy fails when applied to healthcare.

That healthcare expenditures in the US are high and rising rapidly is nothing new, but this study appearing in the Journal of the American Medical Association identifies the exact components of healthcare that are driving those soaring costs. As F. Perry Wilson, MD points out in this 150 Second Analysis, the data suggest traditional economic forces break down in the US healthcare market.

The US spends the most of any country in the world on healthcare in terms of percent of GDP, sitting around 18% as of the most recent data.

But to address the issue, we need to understand what is driving this increase, and a new study appearing in the Journal of the American Medical Association does the best job yet in decomposing the factors behind the rising costs.

The year 2017 marked a turning point in the implementation of the Affordable Care Act. Republicans in Congress attempted to repeal and replace the Affordable Care Act numerous times, ultimately failing but promising to try again. In addition, the Trump administration significantly cut funding for outreach and enrollment activities during 2018’s open enrollment period for the marketplaces, and disrupted markets by declining to pay insurers money owed to them for providing cost-reduced plans for lower-income enrollees. In December, Senate Republicans passed a tax bill that included a provision to repeal the ACA’s individual mandate penalties, paid by most people who do not have health insurance. Given these developments, many Americans are confused about the ACA’s status, which could reduce the number of people who enroll in health plans for the coming year, despite strong enrollment thus far.

It is useful to assess the changes in coverage and access that happened across states under the law before this tumultuous year. Between 2013, the year before the ACA’s major coverage expansions took effect, and the end of 2016, the number of uninsured Americans under age 65 fell by an estimated 17.8 million.1 Uninsured rates declined in every state and the District of Columbia (Exhibit 1).

In this issue brief, we examine the extent to which health care access and affordability improved from 2013 to 2016 for residents in each of the 50 states and D.C. We use six indicators: uninsured rates for working-age adults and for children, three measures of adults’ access to care, and the percentage of individuals under age 65 with high out-of-pocket medical costs relative to their income (Exhibit 2). These measures align with those reported in the Commonwealth Fund’s ongoing series of Health System Performance Scorecards.

After three years of the ACA’s major coverage expansions, the number of uninsured working-age adults and children in the United States had fallen to a record low. This historic decline was accompanied by widespread reductions in cost-related access problems and improvements in access to routine care for at-risk adults, particularly in states that expanded Medicaid. If the 19 states that have not yet expanded Medicaid decided to expand, they could see similar positive effects for their residents.

There is no deadline for adopting the Medicaid expansion. In November, Maine residents voted to expand Medicaid under a citizen-initiated ballot referendum, indicating that popular support for expanding the program may exist in states where elected officials have rejected it. While implementation in Maine could face hurdles because of opposition from the state’s governor, similar efforts are now under way in other nonexpansion states.

Actions at the federal level could, however, jeopardize the gains made under the ACA. Recent actions by the Trump administration, including a shortened open enrollment period for marketplace coverage and deep cuts in advertising and outreach, could reduce enrollment for 2018.10 In addition, Congress has yet to extend funding for the Children’s Health Insurance Program, which expired at the end of September. In the absence of an extension, more than half of states are projected to run out of federal CHIP dollars by March 2018.11 The result could be a loss of coverage for millions of children.12

Further, the tax bill passed by Senate Republicans included a repeal of the ACA’s individual mandate penalties, which would mean a cancellation of the penalties owed by people who do not take up insurance. The Congressional Budget Office estimated that repealing the penalties would reduce the number of Americans with health insurance by 13 million by 2027 and significantly increase premiums for plans purchased in the individual market. This is because healthy individuals would be the most likely to forgo coverage, leaving sicker people (who are more expensive to insure) in the risk pool.13

People who buy their own coverage on the individual market and who have incomes above 400 percent of the federal poverty level (about $48,200 for an individual and $98,400 for a family of four) — the threshold for ACA premium subsidies — would face the brunt of the premium increase.14 A recent Commonwealth Fund analysis estimates that a 40-year-old buying unsubsidized individual market coverage in one of the 39 states that uses the federally facilitated marketplace would face an average dollar increase in premiums ranging from $556 in North Dakota to $1,264 in Nebraska (Exhibit 10).15

Rather than defining addiction as destructive, compulsive behavior, this ideology focuses on physical dependence. If you need a drug to avoid being physically ill, you are considered addicted. So Prozac would be considered addictive, but not cocaine, because quitting Prozac abruptly can cause flulike symptoms while stopping cocaine doesn’t, even though it elicits extreme craving.

In the 1980s, crack cocaine made clear just how addictive cocaine could be, even without physical withdrawal symptoms. Today, both the National Institute on Drug Abuse and the Diagnostic and Statistical Manual of Mental Disorders reject the idea that addiction is synonymous with dependence. Unfortunately, many clinicians, including doctors, haven’t caught up.

What is addiction, then? The root problem is craving, which drives a compulsion to use drugs despite the harm they cause. That’s what makes crack addictive, while Prozac can be therapeutic.

Because methadone and buprenorphine are opioids themselves, it’s easy to assume that using them is “substituting one addiction for another.” However, the pattern of taking the same dose every day at the same time means that there is no high or intoxication. Patients on maintenance doses are able to nurture a baby, drive, work and be a loving spouse.

In these patients, addiction is replaced by physical dependence. And that’s not a problem for those who have health care coverage: It’s no different from needing antidepressants or insulin. When a drug’s benefits outweigh its risks, continued use is healthy, not addictive.

Sadly, though, there’s another reason for widespread skepticism about addiction medication. It comes from the fact that many patients will continue to misuse opioids. Medication reduces relapse more than abstinence does — but relapse is still common, as in Mr. Thompson’s case. In abstinence treatment, however, relapsers drop out and are invisible; with medication, they often remain in treatment.

And remaining in treatment is important because it cuts overdose risk, even during relapse. Many highly traumatized people also need the continued health care support before they are able to quit street drugs.

When we fail to understand that these medications can be used both to reduce harm and stabilize people in recovery, we risk letting the perfect be the enemy of the good. For some, medication is a way to reduce risk while drug use continues. For others, it’s a path to rapid recovery. Often, people will need to take the first route to survive long enough to reach the second.

For harm reduction to work, maintenance drugs need to be almost as accessible as street drugs. Whenever people take buprenorphine rather than heroin, their risk of dying is lowered, especially since so much heroin these days is tainted with deadly strong fentanyl. For stabilization, people need empathetic counseling that doesn’t view dependence as continuing addiction.

Change will require innovative measures. The government should stop funding and insurers should stop covering any program that does not use all the F.D.A.-approved anticraving medications and does not provide informed consent about their effectiveness. While abstinence can work for some, we need many options. We also need to rethink our regulations for methadone and buprenorphine prescribing.

Then we need to publicly recognize that recovery on medication is every bit as valid as any other treatment. What matters is whether, as Freud put it, you can love and work, not the chemical content of your brain or urine.

Earlier this week, Amazon.com Inc., JPMorgan Chase & Co., and Berkshire Hathaway Inc. jolted Wall Street with their announcement of a joint venture designed to reduce health care costs for their combined one million US employees. It is exciting to see innovative private sector companies lend their intellectual and financial capital to a seemingly intractable issue that has plagued the American economy for decades. About 18 percent of our nation’s financial output is now devoted to health care. For decades, health care costs have outpaced overall economic growth, and the gap is projected to remain to remain at three percentage points a year.

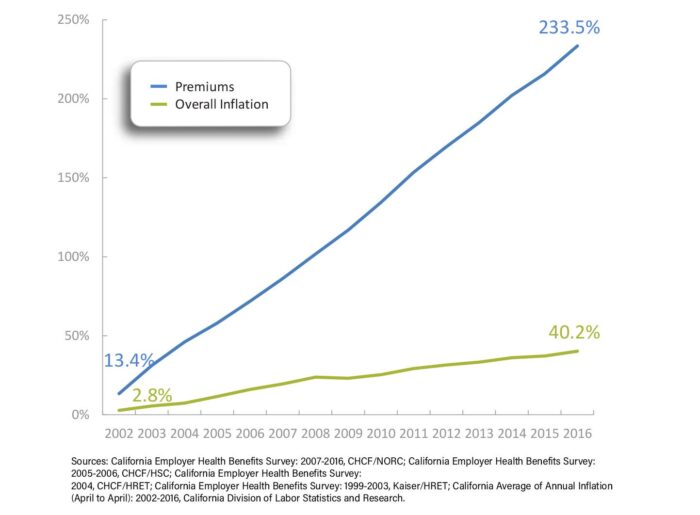

Employees directly and indirectly shoulder these costs. The average premium that employers and their workers pay for a family plan in California now exceeds $1,600 a month. Employer-based family health insurance premiums in the state have increased by 234% over the last 15 years, nearly six times the increase in the state’s overall inflation rate. Every dollar spent on health care is a dollar unavailable for something else, such as education, affordable housing, and environmental protection.

Sixty-six percent of working California families face a deductible of $2,000 or more for their employer-based coverage, including many without high-deductible health plans linked to tax-advantaged health savings accounts.

Increasingly, health care is unaffordable for all of us—not just businesses like Amazon and its workers, but for retirees, the self-employed, people seeking employment, and low-income Californians who aren’t eligible for public coverage. The Affordable Care Act (ACA) attempted to address the cost burden for those with employer coverage by creating disincentives for employers to simply pass on unaffordable premiums, and by capping the share of premiums health plans spent on overhead and profit. For people who shop for insurance coverage on the individual market, the ACA provided federal tax credits to offset premium and cost sharing.

While these and other efforts have helped, more work is needed. Too many families still struggle to afford health care. In 2017, 37% of Americans with health insurance found it difficult to afford premiums each month. Forty-three percent said it was hard to meet their deductibles before coverage kicked in. Among California workers with an aggregate family deductible, 66% faced a deductible of $2,000 or more in 2016.

At least 40% of adults say they worry about being able to afford health care services, losing their insurance, or being able to afford prescription drugs.

Addressing the affordability of care in California and throughout the country requires lowering the underlying cost of care across market segments. Many efforts are already underway. Health insurance companies, large self-funded employers, and public purchasers of care often deploy management strategies to reduce the use of expensive tests, high-cost prescription drugs, and duplicative services. The most common strategies include prior authorization, patient education for better clinical decisionmaking, chronic disease initiatives, and pushing the cost to employees through deductibles and other cost-sharing tools.

To date, the results of these initiatives have been mixed. The findings are consistent with a growing body of academic research that suggests the real driver of health care costs is price, not increased demand. If that is the case, the solution might be to create a market that rewards high-value providers and cost-effective drugs. This type of strategy would rely on tools like reference pricing (individual drugs are grouped by therapeutic class and payment is limited to the price of the cheapest drugs in each class), value-based insurance design (copayments are reduced or eliminated for the most efficient, effective services), or high-deductible health plans.

Unfortunately, consumer-driven approaches have also had limited impact. While companies like Amazon might develop new technologies to enable patients to easily compare, shop for, and purchase health care services in a competitive marketplace, to date these types of tools have not succeeded in reducing costs or changing provider behavior in California. More to the point, introducing blunt consumer-facing financial incentives may run counter to the overall goal of affordability. Everyone should have access to the care they need at a price they can afford and not face care that is rationed by their ability to pay for it.

Perhaps the biggest advantage of the new joint venture is its size and reach. The most promising solutions today are found in large, integrated delivery systems. They have consistently shown that the best approach is to give providers simple, strong financial incentives to make care more efficient and effective. Because this type of model works best on a large scale, the ideal approach is for multiple public and private purchasers of care to come together to align quality reporting requirements, reward value, and support investments in improving health outcomes across entire groups of people. We are already seeing this happen in California and other states.

No one group or slice of the private health care market has the power to really drive down health care costs for everyone. It will take many, many players in the private and public sectors working together to align their efforts. The foundation of payment and delivery reform laid by the Affordable Care Act is a good place to start. Technology is critical and necessary – but it is not by itself sufficient. Leaders also need to pull policy levers, fix payment systems, and spark collaboration between purchasers. Innovators like Amazon, JPMorgan Chase, and Berkshire Hathaway will no doubt make material contributions. Their leadership, in tandem with that of other large purchasers, offers a prime opportunity to make care more affordable for everyone.