Hospital monopolies get the headlines – but new research shows health insurance markets are highly concentrated in every state, giving insurers more pricing power than most policymakers realize.

Hospital consolidation dominates the discussion on health care costs – with good reason. There is overwhelming evidence that it raises prices. But every hospital must ultimately negotiate rates with insurers, yet the consolidation story in the health insurer market has only gotten a tiny fraction of the attention. This is a mistake. While the insurer market is not as highly consolidated as the hospital market, it is still highly concentrated by any reasonable antitrust standard, and a major (and under-estimated) driver of cost growth.

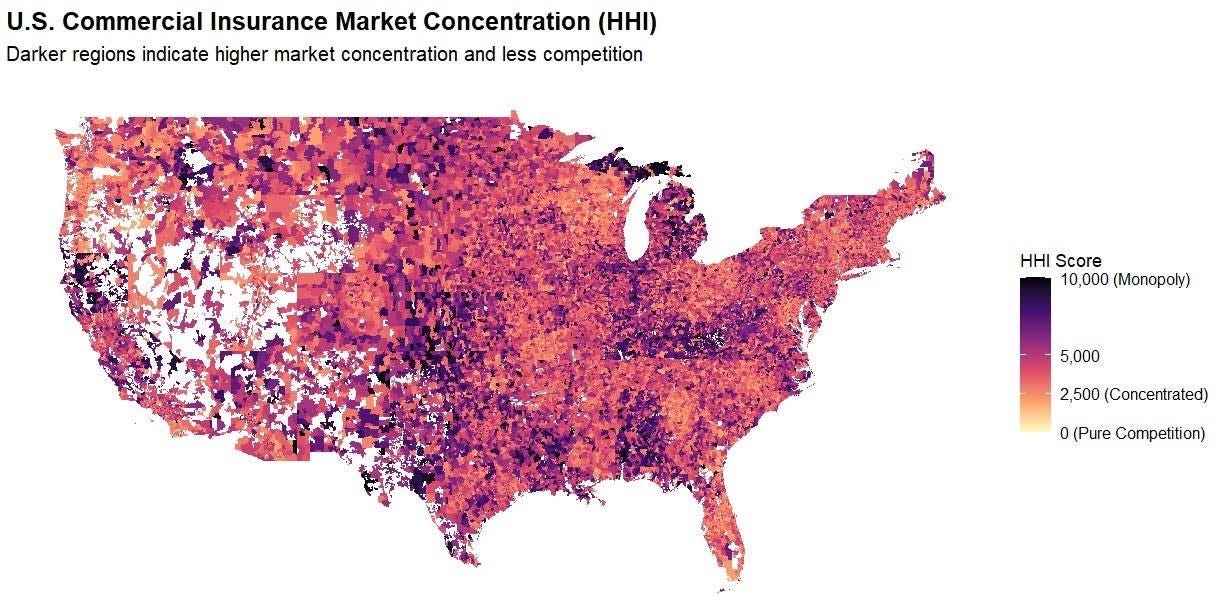

The Department of Justice (DOJ) and Federal Trade Commission (FTC) use the Herfindahl Hirschman Index (HHI) to measure market concentration, where >1,800 is highly concentrated, 5,000-7,500 is where a few firms hold substantial market power, and >7,500 is a near monopoly, where a single firm holds absolute (or near absolute) price-setting autonomy. The hospital market is heavily concentrated and has an average HHI score of 5,273, with 97% of markets being at least heavily concentrated and 64% being near or complete monopolies.

By comparison, our recent work similarly shows a high degree of consolidation among insurers. (Figure 1) We found that the state-level average HHI score in the commercial insurance market was 4,458, with 50 of 50 states (100%) at least heavily concentrated, comparable to hospital markets. This means that in almost every state, health insurers hold pronounced power in price-setting, a key component of the health care cost crisis roiling the country. The most competitive states (although still very highly concentrated) were Oregon (2,870), New York (3,203), and Georgia (3,222), whereas Kentucky (6,752) and Alabama (6,988) are near monopolies.

We find that insurers are even more consolidated than previously reported by the American Medical Association (AMA). Yet the market power of insurers, in combination with hospitals, is a vastly under-appreciated and under-studied driver of costs.

There are several reasons why it is important.

1. Vertical integration

Vertical integration is rapidly accelerating the ability of insurers to consolidate power and redefining what an insurer even is (UnitedHealth/Optum, CVS/Aetna, Cigna/Express Scripts, Elevance/Carelon, BCBSA/Ascendiun). This means that traditional plan-level data (such as that used by researchers and the DOJ/FTC) underestimates the true market power of insurers, and the shadowy network of MSOs, banks, and vendors makes it very difficult to quantify, absent new reporting or regulatory requirements

2. Geography

Where you live is important since it determines where you receive care and buy insurance. In some states, the average competition tells the story, e.g. Louisiana, Kentucky, Alabama, since certain insurers dominate the metro areas and everything in between. In others, the reassuring state averages (CA, NY) mask the variance, and hide the pockets of very uncompetitive markets, particularly in rural areas. Understanding this issue at a market level is important for creating transparency and accountability, to ensure that everyone has options and access to affordable health insurance.

3. Competition

Competition among insurers and hospitals matters, as power asymmetry and/or collusion create dysfunctional markets where costs are “optimized” for the purposes of power and profits, not to make health care more affordable for consumers. It is also important to look at competition among insurers. Market dominance confers advantages that have little to do with delivering better care, such as leverage over providers, captive employer relationships, and pricing power insulated from competition.

While insurer markets aren’t as concentrated as hospital markets, they’re concentrated enough to matter, and the structure of that concentration makes it a distinct and important part of the cost problem. In our next piece, we will show which carriers hold dominant positions and where, and why the answer surprised us.

This research was made possible by the support of Arnold Ventures.

HHI scores weighted according to zip-level and policy volume. Concentration levels: Red – Extreme; Orange – Severe; and Yellow – Very High.