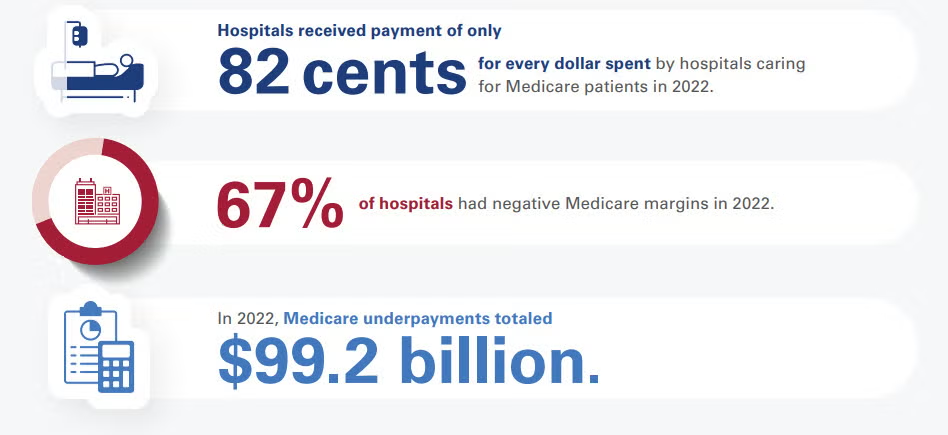

Medicare reimburses hospitals at an average of 82% to 87% of the actual cost of providing patient care. According to long-term data from the American Hospital Association (AHA) and the Congressional Budget Office (CBO), this means hospitals face a shortfall, receiving roughly 82 to 87 cents for every dollar they spend caring for Medicare beneficiaries.

Financial Impact and Hospital Margins

Because Medicare reimbursement rates are fixed by the federal government, they often fail to keep pace with the rising costs of labor, drugs, and supplies:

- Negative Profit Margins: The Medicare Payment Advisory Commission (MedPAC) reported that hospitals experienced an average -12% margin on fee-for-service Medicare services, with projections remaining deeply negative at -10%. [1]

- Widespread Losses: Approximately 67% of all U.S. hospitals operate at a net financial loss specifically on their Medicare patient population. [1]

- Aggregate Underpayments: This payment-to-cost deficit translates to roughly $99.2 billion in annual underpayments that hospitals must absorb or offset through other revenue streams.

How Hospitals Balance the Deficit

To remain financially viable while absorbing underpayments from Medicare and Medicaid, hospitals rely on cost-shifting to the private sector:

- Commercial Insurance Rates: Private, employer-sponsored health plans pay hospitals significantly more to subsidize public program shortfalls. On average, commercial insurers reimburse hospitals at 196% to 199% of Medicare rates.

- Payer Mix Vulnerability: Hospitals located in regions with high concentrations of elderly or low-income residents are at higher financial risk. At 96% of U.S. hospitals, government programs (Medicare and Medicaid) account for more than half of all inpatient days.

If you are tracking hospital financials or healthcare policy, would you like to see how Medicaid reimbursement rates compare, or look closer at the differences between inpatient and outpatient Medicare payment structures?

Medicaid reimburses hospitals at an average of 88% to 90% of the actual cost of care, but this figure heavily relies on supplemental government funding. Without these extra state and federal payments, standard Medicaid base rates only cover roughly 58% to 65% of hospital costs.

Because Medicaid is jointly funded by federal and state governments, the exact payment-to-cost ratio varies wildly by state, fluctuating between 49% and 169% of Medicare benchmarks.

The Core Components of Medicaid Payments

Medicaid hospital payment structures are highly complex and divided into two primary tiers:

- Base Rates (Severe Shortfalls): Standard Fee-For-Service (FFS) base rates and Managed Care Organization (MCO) plans pay well below actual expenditures. According to industry data published by the American Hospital Association (AHA), standard MCO plans cover just 65 cents on the dollar, while FFS base payments plummet to 58 cents on the dollar.

- Supplemental Payments (The Lifeline): To minimize this gap, states issue extra payments to hospitals. These account for over 52% of total Medicaid hospital spending nationwide and are broken down into:

- Disproportionate Share Hospital (DSH) Payments: Extra funds legally required for safety-net hospitals serving high volumes of low-income or uninsured patients.

- Non-DSH Supplemental Payments: Upper Payment Limit (UPL) adjustments and state-directed payments meant to artificially boost base rates closer to commercial or Medicare levels.

Operational Impacts on Hospitals

The gap between Medicaid base reimbursement and actual cost strains hospital systems in several distinct ways:

- Widespread Financial Loss: Even after accounting for all safety-net supplemental payments, roughly 62% of U.S. hospitals operate at a net loss on their Medicaid patient populations.

- Aggregate Underfunding: The total nationwide Medicaid underpayment deficit adds up to approximately $24.8 billion annually that hospitals must absorb.

- The Commercial Subsidy: Because public programs underpay, hospitals shift costs onto employer-sponsored health plans. As a result, private insurers are charged nearly double (up to 200%) what Medicare and Medicaid pay for the exact same medical services.