Cartoon – Kissed-up to all the Right People

Maryland Gov. Larry Hogan signed a contract with the federal government on Monday to enact the state’s unique all-payer health care model, which he said will create incentives to improve care while saving money.

Hogan signed the five-year contract along with the administrator of the federal Centers for Medicare and Medicaid Services, Seema Verma.

“The Maryland Model provides incentives across the health system to provide greater coordinated care, expanded patient-care delivery and collaboration of chronic-disease management … all while improving the quality of care at lower cost to the consumer,” Hogan said.

He said the model emphasizes the quality of care over the quantity of care.

The Hogan administration said the new contract is expected to provide an additional $300 million in savings a year by 2023, totaling $1 billion in savings over five years.

Maryland is the only state that can set its own rates for hospital services, and all payers must charge the same rate for services at a given hospital. The policy has been in place since the 1970s, though Maryland modernized its one-of-a-kind Medicare waiver about four years ago to move away from reimbursing hospitals on a fee-for-service basis to a fixed budget.

Because that change focused on hospitals only, the federal government required the state to develop a new model that would provide comprehensive coordination across the entire health care system.

Under the agreement, Maryland will be relieved of federal restrictions and red tape that the other 49 states face in the Medicare program. However, the state will have to meet benchmarks of improving access to health care while improving quality and reducing costs.

Verma said the model is the first involving the Centers for Medicare and Medicaid Services that holds the state “fully at risk for total Medicare costs for all residents.”

“The state and CMS have agreed on the goals, and now our job is to get out of the way and give the state the maximum flexibility to achieve success.”

Maryland health secretary Robert Neall says if successful, the plan could be replicated around the country to address financial strain on Medicare. Neall described the model as being “less transactional and more just taking care of the total person.”

“The incentives are going to be aligned so that it’s right place, right time, right purpose, right price, instead of, ‘Come back and see me in two weeks, and we’ll run the same set of tests on you,'” Neall said.

https://commonwealthmagazine.org/opinion/the-real-driver-of-health-care-spending/

An inefficiency gap is boosting costs — and profits

THE HEALTH CARE DEBATES that occurred in Washington over the past year were largely irrelevant to what’s happening in the health care marketplace. Republicans couldn’t repeal the Affordable Care Act but they made some changes that weakened it. Those changes will increase insurance premiums in the individual market but they do nothing to address the most significant trends that are evolving across the system. To understand the important trends, one must look elsewhere.

In March, three researchers from the Harvard T. H. Chan School of Public Health published a study in JAMA analyzing the well-known reality that the United States spends dramatically more on health care than other wealthy countries. They compared the US, where health care consumes 17.8 per cent of gross domestic product, to 10 comparable nations where the mean expenditure is 11.5 percent. Despite spending much less, the other countries provide health insurance to their entire populations and have outcomes equal to or better than ours. The researchers found that this inefficiency gap is primarily driven by two characteristics of the US system: the high cost of pharmaceuticals and inordinate administrative expenses.

The high administrative spending derives in large part from the fact that 55 percent of the people in the US are covered by private health insurers who embed their own billing requirements, expenses, and profit into the system. The next highest country in this regard is Germany, where 10.8 percent of the population is covered by private insurers. In many countries, there are no such middlemen.

Coincidentally, when the JAMA study was published, the large publicly traded health care companies that dominate the US market had just finished disclosing their 2017 financial results. Examining those results provides additional insight into the economic forces that make our system so expensive and inefficient. The scale of the money involved is sometimes hard to grasp. The largest health care corporations, those included in the S&P 500, had almost $2 trillion in revenue last year. (Table 1)

Most of these enormous companies are engaged in one of two businesses: they’re either selling drugs or they’re selling health insurance. The excess costs reported by the Harvard researchers serve mainly to support the revenue of the companies in those fields.

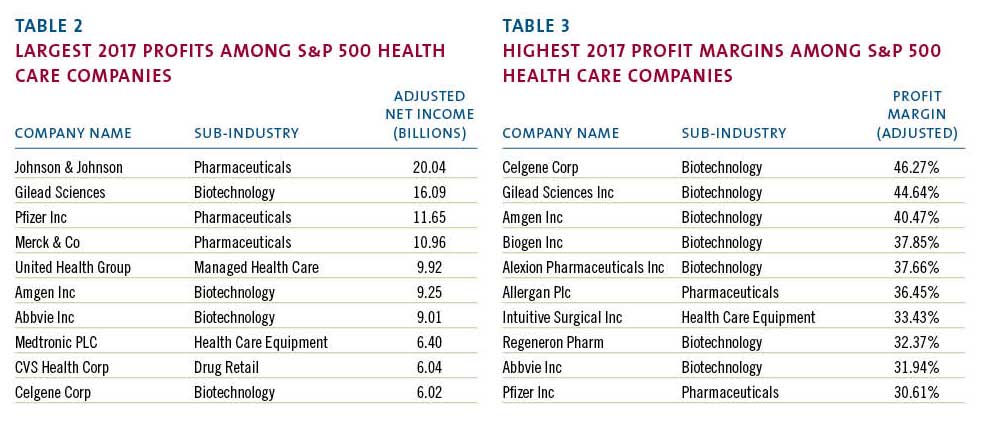

The 2017 reporting of corporate profits was complicated by the passage of the new tax bill. But most companies also reported “adjusted net income,” which shows their normalized profits after accounting for the one-time impact of the tax law. The chart below (Table 2) uses the adjusted numbers to show the largest annual profits among S&P health care companies.

Health insurers such as United Health and retailers such as CVS have enormous revenue and impressive profits but, when profit is measured as a percentage of revenue, they can’t compete with biotech and pharma. The highest relative profitability, using the same reported adjusted results, is in the chart below. (Table 3)

These profit margins show that there are many situations where between a third and a half of every dollar spent on a prescription drug falls to the bottom line of the of the company that made it. This profit derives in large part from the enormous difference in drug prices in the US versus other countries where such prices are more effectively controlled.

The high administrative cost of the US system stems from the large portion of the market dominated by insurance companies looking to maximize their profits. Notwithstanding many news stories about turmoil in the insurance markets, 2017 was a banner year for the largest health insurers. The big players all had significant increases in annual profitability in 2017.

Note that Humana did not report “adjusted” numbers even though its profit was swollen by unusual events. A major distortion was a huge break-up fee the company received from a failed merger. That accounted for approximately $630 million in after-tax profit. Even discounting that, it was a very good year.

The revenue and profitability of these corporations support the proposition that high pharmaceutical prices and insurance-related administrative costs account for much of the extraordinary expense of our system. US health policy, or the absence thereof, has enabled these businesses annually to drive costs up for the benefit of their bottom line. That effect will continue. Not surprisingly, the big health care companies are developing new strategies to enhance their businesses and drive their profits going forward.

The term now heard often among health care giants is “vertical integration,” which means combining upstream suppliers with downstream buyers to control the flow of business. If this strategy persists, health care delivery will evolve significantly although it is unlikely to become less expensive. The most prominent current example of vertical integration is the planned $68 billion acquisition of Aetna by CVS.

How would these companies work together? A Wall Street analyst recently described the vision as a way to “identify high risk patients and preemptively get them into a Minute Clinic.” Thus, your health insurer could send you to a local store for diagnosis, treatment, drugs, and anything else you might need from the shelves. This will keep even more of the health care dollar under their control.

Similarly, Cigna is in the process of acquiring Express Scripts, a huge pharmacy benefits manager, for $54 billion, another attempt to bring more services under one roof. The combined company would have annual revenue of $142 billion and, presumably, enough leverage with drug companies to improve profits although not necessarily to lower costs to patients. United Health, a leader of vertical integration, previously bought a pharmacy benefit manager but co-pays and deductibles for its patients have continued to climb. United has aggressively acquired physician practices in recent years and is now in the process of buying DaVita Medical Group, which operates nearly 300 clinics and outpatient surgical centers.

More striking are reports of a potential but unsigned merger of Walmart and Humana, a combined company that would have revenue of $550 billion. Walmart is a large operator of retail pharmacies inside its stores and the logic is similar to the Aetna-CVS deal. Humana, a huge insurer, is separately in the process of acquiring a large home health business from Kindred so this could represent yet another level of vertical integration.

If this course continues, the health care system will evolve quickly, giving fewer and larger companies even more market leverage. Integration of this kind benefits the large corporations that initiate it but there is no evidence it will lead to lower costs, improved access, or enhanced quality. These changes are driven by highly focused corporate financial interests and are occurring without reference to public policy. That’s because there is no coherent public policy to guide these changes.

On May 11, President Trump made a long-awaited speech to reveal what he described as “the most sweeping action in history to lower the price of prescription drugs for the American people.” His typically firebrand language struck at “drug makers, insurance companies, distributors, pharmacy benefit managers, and many others” who contributed to “this incredible abuse.” His attack seemed to target the large public companies that have benefited from the abuse. Unsurprisingly, his speech did not include specifics. His staff then released tepid policy details, which immediately generated a significant upward spike in the biotech stock index as well as the stock prices of other large health care companies. For all the presidential bombast, investors saw Trump’s policy for what it is: indifference to the current path and no threat to high prices.

It is not in the interest of huge profit-making corporations to restrain the overall cost of the US health care system. In fact, their interest is served by driving health care expenditures higher. When combined with the spending analysis provided by researchers, the financial data disclosed by public corporations point to a path that the country must follow to make our system more coherent and less costly. Any progress will require driving down pharmaceutical pricing and reducing administrative costs imposed by middlemen. We are not doing that yet but, ultimately, we must.

Nearly half are operating with negative margins, according to new research, which says a high rate of uninsured patients is among the reasons.

With healthcare services being concentrated more and more among major health systems and larger providers, rural hospitals are struggling.

A new study from Chartis Group and iVantage Health Analytics sheds light on the scope of the problem. About 41 percent of rural hospitals faced negative operating margins in 2016, the report found.

If those hospitals were located in a state that elected not to expand Medicaid under the Affordable Care Act, those margins were generally worse than those of their peers, suggesting that such expansion had a mitigating effect on financial pressures.

Due to those financial pressures, 80 rural hospitals closed from 2010 to 2016, indicating that the rural health safety net has seen better days.

One of the key factors behind this was a high rate of uninsured patients, and a payer mix heavy on public insurers with lower claims reimbursement rates. More patients are seeking care outside rural areas, which isn’t helping, and many areas see a dearth of employer-sponsored health coverage due to lower employment rates. Many markets are also besieged by a shortage of primary care providers, and tighter payer-negotiated reimbursement rates.

Demographics aren’t helping rural hospitals, either. Patients in rural markets are generally more socioeconomically disadvantaged, with many patients over 65 years old and suffering from multiple health disparities, which lead to higher general healthcare costs.

To make matters worse, there’s a shortage of physicians in rural communities as well, with only about 39.8 physicians per 100,000 people. By contrast, the ratio in non-rural areas is 53.3 physicians per 100,000 people.

All this comes at a time when the shift from fee-for-service payment models to value-based reimbursement is in full swing, putting pressure on all hospitals to reduce costs — which is especially problematic for rural hospitals given that their demographic and staffing challenges have a tendency to drive costs up, not down.

The researchers pointed to the Graves-Loebsack Save Rural Hospital Act as a possible means of mitigating the problem. The bill, introduced by the House in 2015, would create a payment structure whereby 105 percent of “reasonable” costs would be reimbursed; 100 percent of bad debt would be reimbursed; and rural hospitals would be exempt from 2 percent of sequestration of payments.

The authors suggested revisiting the bill, which would also establish the Community Outpatient Hospital Program, a measure aimed at preserving emergency and outpatient care for rural markets. It would also recoup $5.4 billion in lost Medicare reimbursement among rural hospitals over 10 years.

A look at the financial, branding and cultural considerations when deciding to acquire or merge with another hospital.

Mergers and acquisitions are common occurrences in healthcare. The impetus behind consolidation can range from shifting patient demographics to new and disruptive technologies, but financial concerns are almost always at the root — which means the acquiring entities always assume some modicum of risk when pulling the trigger on these deals.

Oftentimes, the acquirer will subsume members, who then become part of the larger system. This brings risk if the hospital being acquired is distressed. These hospitals either don’t have the in-house expertise or aren’t willing to hire outside expertise, or they take shortcuts with physicians and kickbacks, according to Roger Strode, a partner with Foley and Lardner, who said he has seen it time and time again.

“They tend to be so cash-strapped, and they’re in such dire need, that they’ll take risks that other systems won’t take,” said Strode. “You might not have a pool of indemnification, so it takes a lot to get these deals done. The other risk is that they’ve brought on a base of employees so you’ve got cultural risk.”

Cash-strapped hospitals, for instance, are likely to operate under a different culture than organizations that have the financial means to pay for strong leadership. And then there’s the risk of how the healthcare provider is going to be perceived in the community. Will they be looked at as the hero swooping in to rescue the struggling hospital, and keep its promises, like maintaining services in the community? There’s risk if the acquirer hasn’t done its due diligence and realizes only after the fact they they can’t keep all the services it said they would. The health of a company’s branding is on the hook.

There’s a tremendous amount of diligence to keep in mind when making these deals, said Strode. There are lawyers and outside accountants to hire. There’s understanding the material contracts. And there’s hashing out what the five-to-10-year financial plan is going to be.

“There’s a certain amount of mission-driven thinking that goes into this,” said Strode. “If you’ve seen one of these deals, you’ve seen one of these deals. Healthcare is local, markets are different, so every deal is a little bit different. Some feel that if they don’t grab it now, their competitors will grab it, so they’ll fix the problems after they get it. Sometimes there’s a concern they’ll go to bankruptcy, and then it’s really difficult to acquire them.”

Rob Fraiman, president of Cain Brothers, sees most merger and acquisition activity taking place among nonprofit entities, more so than in the investor-owned world. There’s certainly some of the latter — Tenet and Universal Health come to mind — but they’re generally the exception, and structurally, most of these nonprofit transactions are outright sales of a hospital. They’re essentially mergers with a membership substitution, so a tax exempt entity merges with another tax-exempt entity and substitutes the tax-exempt member of the company with the new business.

“They don’t pay any cash, typically,” said Fraiman. “And the acquirer essentially picks up all the liabilities as well as all of the assets of the system. As far as risks, they’re merging with an enterprise that may have financial stress, which may be what’s leading the board to choose to do a transaction. Those financials don’t go away just because a transaction happens. It happens if the acquiring entity can go in and make some significant changes.”

There are also elements related to what kind of payer contracts the entity has. When two systems join together, replacing the contracts the acquirer has with the payer is not a quick, snap-of-the-finger type of move. It happens over time. Initially, the buyer is stepping into the shoes of whatever the seller has in place. Those contracts are a part of the reason there’s stress on the part of the target entity, so the acquirer is assuming that risk, though it tends to be short-term risk.

Capital is what drives a lot of those transactions, said Fraiman. Ultimately, the hospital industry is very capital intensive. In many of these instances, the target hospital or health system looks at the three-to-five-year time horizon and concludes they don’t have enough capital to invest in their business, and they need some deeper pockets. It’s not about price. It’s about terms, and how much capital they’re prepared to commit.

“There’s a huge risk the buyer is taking to assess whether the amount of capital they’re willing to commit over five or eight years is in fact going to be a good investment,” said Fraiman. “And if it’s not, that’s a huge risk, obviously, for the acquirer. At that point they’re really committed to it.”

There’s a view in the healthcare industry that scale is critically important, said Fraiman. Large corporate players are transforming how they’re operating in the healthcare economy.

“You’ve got some very, very large transactions that are happening in other parts of the healthcare economy, typically in the payer world, and that has a huge impact on hospitals,” he said. “In a given market or state, there’s a handful of insurance companies, and if a couple of them combine, that can have a real impact on the hospital system. Similarly, physician groups are going through a massive consolidation. All of that has a direct or indirect impact on health systems.”

Strode said that risk is slowly shifting away from insurance companies, and that this has had a catalytic effect on the ways mergers and acquisitions have played out in healthcare over the past several years.

“Insurance companies used to handle all the risk,” said Strode. “Now when they’re pushing that risk on hospitals and health systems, they have to spread that risk over larger and larger populations of people. They need more people to spread that risk. They need more doctors to spread that risk. The system needs to be bigger. You’re looking to be bigger because bigger geography gets the attention of payers. Smaller hospitals and community health systems can’t keep up. They can’t negotiate the same deals. They’d rather join them than fight them.”

Strode said that, despite the decreased number of independent facilities due to consolidation, the trend is still good in terms of market competition — at least for now — because it tends to drive down prices. He sees continued consolidation in the coming years, partly because there are still a lot of fragmented markets throughout the country. There are also a lot of academic medical centers that are expanding their sphere of influence by swallowing up some of the smaller hospitals around them.

Fraiman said the key to these deals is to be as prepared as possible.

“Like any business, it’s all about management,” said Fraiman. “Do they have the management capability to actually implement what they say they’re going to implement? That’s really hard. The implementation is harder than the deal. The deal might takes six months or a year, but you’ve got to live with it forever.”