https://mailchi.mp/9b1afd2b4afb/the-weekly-gist-december-1-2023?e=d1e747d2d8

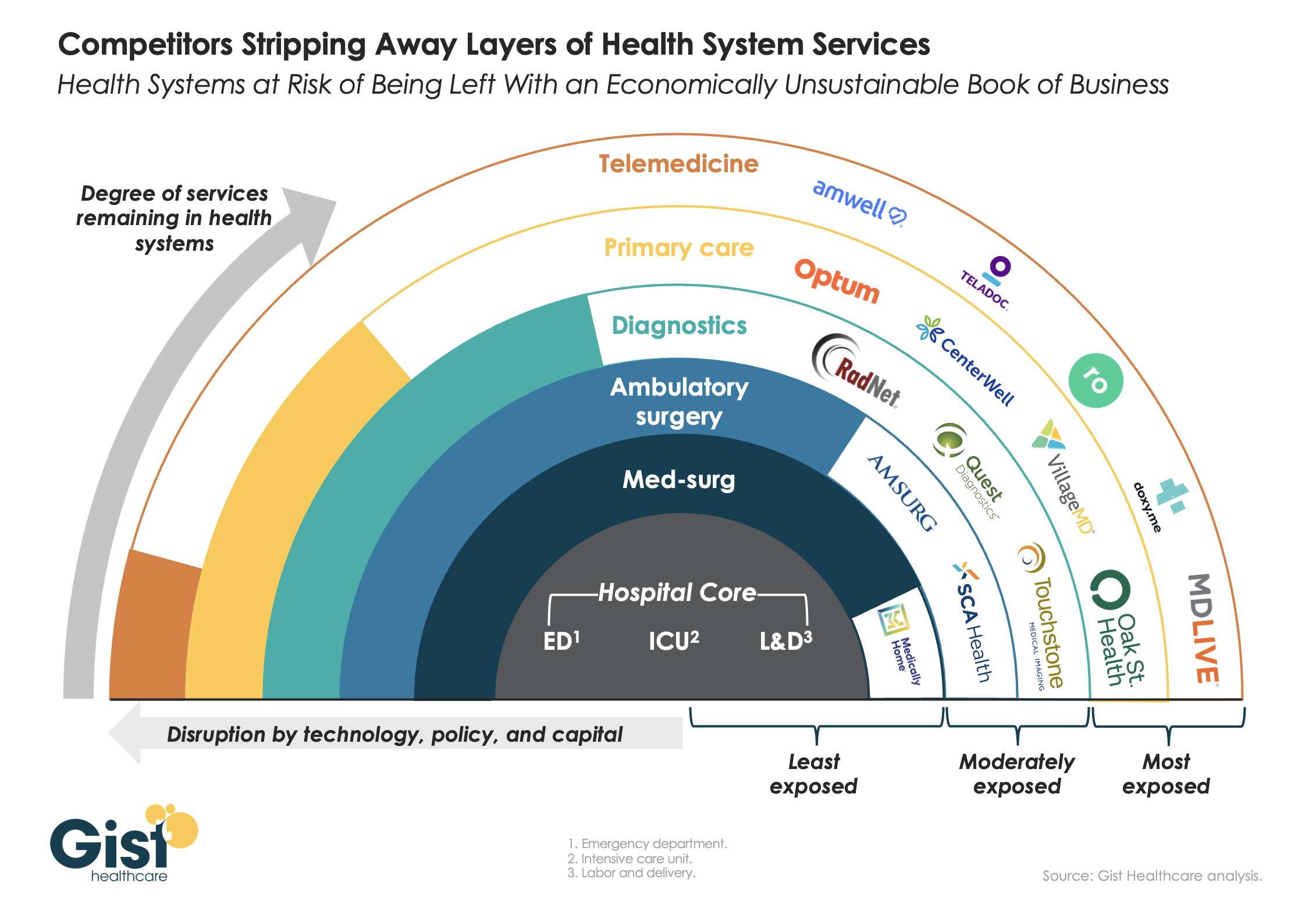

This week’s graphic features our assessment of the many emerging competitive challenges to traditional health systems.

Beyond inflation and high labor costs, health systems are struggling because competitors—ranging from vertically integrated payers to PE-backed physician groups—are effectively stripping away profitable services and moving them to lower-cost care sites. The tandem forces of technological advancement, policy changes, and capital investment have unlocked the ability of disruptors to enter market segments once considered safely within health system control.

While health systems’ most-exposed services, like telemedicine and primary care, were never key revenue sources (although they are key referral drivers), there are now more competitors than ever providing diagnostics and ambulatory surgery, which health systems have relied on to maintain their margins.

Moving forward, traditional systems run the risk of being “crammed down” into a smaller portfolio of (largely unprofitable) services: the emergency department, intensive care unit, and labor and delivery.

Health systems cannot support their operations by solely providing these core services, yet this is the future many will face if they don’t emulate the strategies of disruptors by embracing the site-of-care shift, prioritizing high-margin procedures, rethinking care delivery within the hospital, and implementing lower-cost care models that enable them to compete on price.