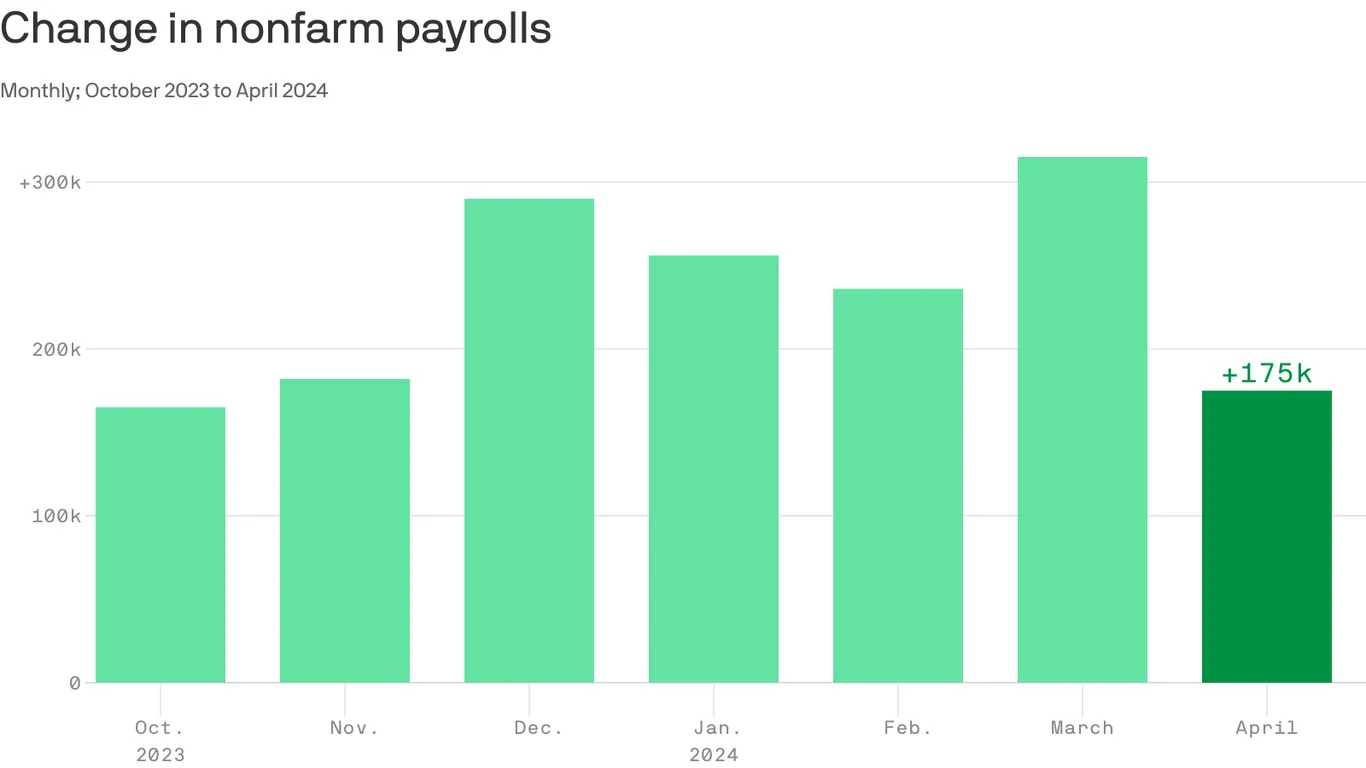

The U.S. economy added 175,000 jobs in April, while the unemployment rate ticked up to 3.9% from 3.8%, the Labor Department said on Friday.

Why it matters:

Jobs growth slowed from the prior month’s hot pace, but the data suggests that the labor market is still chugging along with healthy demand for workers.

The pace of hiring was notably slower than economists’ estimate of 240,000 jobs in April.

Job gains in March were slightly better than previously thought, upwardly revised to 315,000 from 303,000—though payrolls in February were revised lower by 34,000 to 236,000.

Driving the news:

The lower-than-expected job gains were concentrated in health care, social assistance, transportation and warehousing

Average hourly earnings, a measure of wage growth, rose 0.2%.

Over the past 12 months, average hourly earnings increased 3.9%.

State of play:

Friday’s data is the latest evidence that the labor market is holding steady — an important development for the broader economy.

The Federal Reserve this week kept interest rates at the highest level in more than two decades.

Its policymakers suggested that any rate cuts would happen later than previously thought due to stalled progress on curbing inflation.

Fed chair Jerome Powell this week said that the central bank would be “prepared to respond to an unexpected weakening in the labor market.”

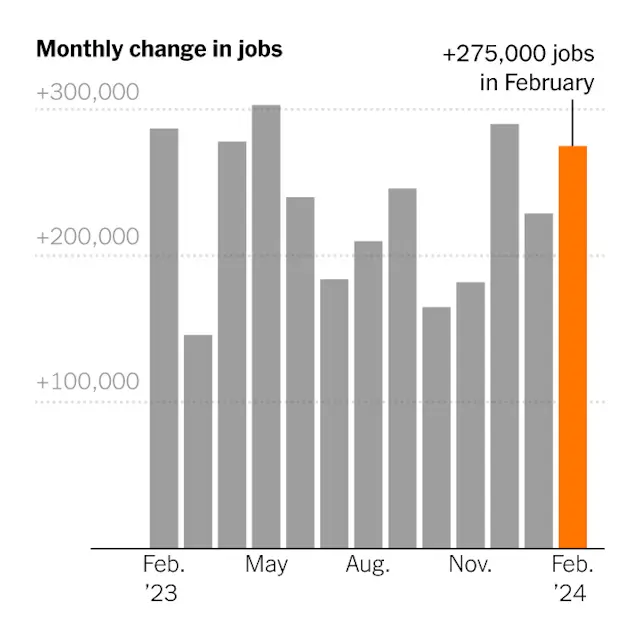

The labor market showed resiliency in February, adding 275,000 jobs, a sign that economic growth is still solid.

If the economy is slowing down, nobody told the labor market.

Employers added 275,000 jobs in February, the Labor Department reported Friday, in another month that exceeded expectations.

It was the third straight month of gains above 200,000, and the 38th consecutive month of growth — fresh evidence that after surging back from the pandemic shutdowns, America’s jobs engine still has plenty of steam.

“We’ve been expecting a slowdown in the labor market, a more material loosening in conditions, but we’re just not seeing that,” said Rubeela Farooqi, chief economist at High Frequency Economics.

The previous two months, December and January, were revised down by a combined 167,000 jobs, reflecting the higher degree of statistical volatility in the winter months. That does not disrupt a picture of consistent robust increases, which now looks slightly smoother..

At the same time, the unemployment rate, based on a survey of households, increased to a two-year high of 3.9 percent, from 3.7 percent in January. A more expansive measure of slack labor market conditions, which includes people working part time who would rather work full time, has been steadily rising and now stands at 7.3 percent.

The unemployment rate was driven by people losing or leaving jobs as well as those entering the labor force to look for work. The labor force participation rate for people in their prime working years — ages 25 to 54 — jumped back up to 83.5 percent, matching a level from last year that was the highest since the early 2000s.

Average hourly earnings rose by 4.3 percent over the year, although the pace of increases has been fading.

“We’ve recently seen gains in real wages, and that’s encouraged people to re-enter the labor market, and that’s a good development for workers,” said Kory Kantenga, a senior economist at the job search website LinkedIn. As wage growth slows, he said, the likelihood that more people will start looking for work falls.

As late as last fall, economists were predicting much more modest employment increases, with hiring concentrated in a few industries. But while some pandemic-inflated industries have shed jobs, expected downturns in sectors like construction haven’t materialized. Rising wages, attractive benefits and more flexible work schedules have drawn millions of workers off the sidelines.

Elevated levels of immigration have also added to the labor supply. According to an analysis by the Brookings Institution, the influx has approximately doubled the number of jobs that the economy could add per month in 2024 without putting upward pressure on inflation, to between 160,000 and 200,000.

Health care and government again led the payroll gains in February, while construction continued its steady increase. Retail and transportation and warehousing, which have been flat to negative in recent months, picked up.

No major industries lost a substantial number of jobs. Credit intermediation continued its downward slide — that sector, which mostly includes commercial banking, has lost about 123,000 jobs since early 2021.

That doesn’t mean the employment landscape looks rosy to everyone. Employee confidence, as measured by the company rating website Glassdoor, has been falling steadily as layoffs by tech and media companies have grabbed headlines. That’s especially true in white-collar professions like human resources and consulting, while those in professions that require working in person — such as health care, construction and manufacturing — are more upbeat.

“It is a two-track labor market,” said Aaron Terrazas, Glassdoor’s chief economist, noting that job searches are taking longer for people with graduate degrees. “For skilled workers in risk-intensive industries, anyone who’s been laid off is having a hard time finding new jobs, whereas if you’re a blue-collar or frontline service worker, it’s still competitive.”

The last few months have been studded with strong economic data, leading analysts surveyed by the National Association for Business Economics to raise their forecasts for gross domestic product and lower their expectations for the trajectory of unemployment. It’s occurred even as inflation has eased, leading the Federal Reserve to telegraph its plans for interest rate cuts sometime this year, which has raised growth expectations further.

Mervin Jebaraj, director of the Center for Business and Economic Research at the University of Arkansas, helped tabulate the survey responses. He said the mood was buoyed partly by fading trepidation over federal government shutdowns and draconian budget cuts, after several close calls since the fall. And he sees no obvious reason for the recovery to end soon.

“Once it starts going, it keeps going,” Mr. Jebaraj said. “You had this external stimulus with all the trillions of dollars of government spending, Now it’s sort of self-sustaining, even though the money’s gone.”

The U.S. economy added 353,000 jobs in January, while the unemployment rate held at 3.7%, the Labor Department said Friday.

Why it matters:

The first look at the 2024 labor market shows it’s on fire — not slowing down as previously thought.

Details:

The January payroll figures show hiring picked up from the 333,000 added the prior month, which itself was revised higher by 117,000.

Job gains in November were revised slightly higher, too, by 9,000 to 182,000 jobs added.

What’s new:

The hiring boom last month came amid strong job gains in health care, retail and professional and business services, while mining and oil and gas extraction are among the sectors that shed jobs.

Meanwhile, the labor force participation rate — the share of workers with or looking for a job — was 62.5% in January.

Average hourly earnings, a measure of wage growth, soared by 0.6%. Over the past 12 month, average hourly earnings increased by 4.5%.

The big picture:

The data is the latest in recent weeks to show that the economy is revving up, with fading inflation and steady hiring — a welcome development for the Biden administration that is touting its economic agenda ahead of the 2024 election.

The intrigue:

The strong growth in both jobs and earnings will make the Federal Reserve reluctant to cut interest rates soon, out of fear that labor market strength could reverse progress on inflation.

Already this week, Fed chair Jerome Powell threw cold water on the idea of a March rate cut.

The bottom line:

Despite high profile layoffs at media and technology companies, the report shows that broader labor market is heating up.

Forget the much-discussed prospect of a soft landing for the U.S. economy. In 2023, there was no landing at all.

Why it matters:

Big economic rules broke last year. The latest data to confirm that is the new GDP report showing very strong economic growth to conclude 2023, even amid a big cooldown in inflation.

Mainstream economists and policymakers believed a period of below-trend growth would be necessary to make progress on inflation.

Instead, above-trend growth in 2023 coincided with inflation falling sharply, reflecting improvement in the economy’s supply potential.

Driving the news:

The economy expanded at a 3.3% annualized rate in the fourth quarter, well above the 2% forecasters expected. That followed the previous quarter’s blockbuster 4.9% growth.

GDP was 3.1% higher in the fourth quarter than a year earlier.

That represents an acceleration from 0.7% GDP growth in 2022, and trounced the growth rates of most other advanced countries — and the 1.8%-ish rate that economists consider the United States’ long-term trend.

Details:

The fourth quarter’s hot growth resulted from bustling activity across the economy.

Consumers spent more on goods and services, with personal consumption expenditures rising at a 2.8% annualized pace. That was responsible for nearly 2 percentage points of the fourth quarter’s GDP rise.

Businesses spent on equipment, factories and intellectual property at a solid pace, with nonresidential fixed investment increasing at 1.9% — up from the previous quarter.

The intrigue:

For two years now, Fed officials have spoken of the need for a period of below-trend growth to bring inflation into line. Now, they face the decision of whether to cut rates — to essentially declare victory on inflation — even as below-trend growth is nowhere to be seen.

A flourishing labor market, strong productivity gains and supply-side improvements — more workers joining the workforce, for instance — has (at least so far) meant the economy can keep growing at a solid pace without risking a pickup in price pressure.

“[W]e had significant supply-side gains with strong demand,” Fed chair Jerome Powell said in his December press conference, adding that potential growth may have been higher than usual “just because of the healing on the supply side.”

“So that was a surprise to just about everybody,” Powell said.

What they’re saying:

“This report feels like a supersonic Goldilocks: very strong GDP reading with cool inflation,” Beth Ann Bovino, chief economist at U.S. Bank, tells Axios. “Good news is good news.”

“With high productivity levels, we can have strong growth with less inflation. That was the case during the last soft landing in the 90s,” Bovino adds.

The U.S. economy added 216,000 jobs last month while the unemployment rate held at 3.7%, the Labor Department said on Friday.

Why it matters:

The final snapshot of the 2023 labor market shows hot hiring — the latest sign that the American job market continues to defy expectations of a slowdown.

The figure is well-above the roughly 170,000 jobs economists expected.

The big picture:

The Federal Reserve has hinted it likely won’t raise interest rates again with encouraging signs that inflation is easing and the labor market is cooling.

That concludes an aggressive rate hiking cycle that began in 2022 and lasted through much of last year.

For now, however, there is little evidence those rate hikes translated into pain for workers in 2022.

American consumers, however, remain dissatisfied with the economy — a problem that may continue to weigh on the Biden White House as the 2024 election heats up.

Details:

Friday’s jobs report shows the labor market stayed strong. Hiring increased in sectors including government, health care, and construction. Transportation and warehousing shed jobs.

Average hourly earnings, a measure of wages, rose by 0.4% last month. Compared to the prior year, average hourly earnings rose 4.1%.

The share of the population with in the labor force — that is, with a job or looking for one — was 62.5% in December, roughly 0.3 percentage point less than the prior month.

The Labor Department also said the economy added a combined 71,000 fewer jobs than initially estimated in October and November.

The bottom line:

The hotter-than-expected jobs figures are one of several more key economic reports due before Federal Reserve officials meet at the end of the month.

The latest CPI was a crowd-pleaser: Inflation has plunged from its peak, helping provide relief for consumers.

Beyond the headline, an underlying measure closely watched by economists and the Fed finally began to cool.

Why it matters:

The worst of the inflation crisis looks to be firmly behind us. Price gains appear to be on a path to returning to normal, but there is huge uncertainty around how long that will take, with plenty of hurdles still ahead.

What they’re saying:

“After a punishing stretch of high inflation that eroded consumer’s purchasing power, the fever is breaking,” Bill Adams, chief economist at Comerica Bank, wrote in a note.

While the Fed appears to be on track to tighten by a quarter percentage point two weeks from today, the promising news lowers the odds of further hikes this year.

Details:

Headline CPI rose 3% (or 2.97%, unrounded) in the 12 months through June, the smallest increase since March 2021. That reflects milder price gains for a slew of goods, including food — and outright deflation for other items consumers buy, like airline fares, which fell 8% in June.

The intrigue:

At the same time last year, headline prices skyrocketed by 9%. Now we’re lapping that period, which makes the comparison much more favorable.

Then, commodity prices soared on disruptions from Russia’s invasion of Ukraine. Those prices are sharply lower now, helping the headline figure cool rapidly. Gasoline, for instance, is down nearly 27%.

Those favorable effects will fade in the year-on-year numbers, so don’t be surprised if the headline CPI figure rebounds some in the coming months.

The most encouraging aspect was the core figure, which strips out volatile food and energy costs and is closely followed by policymakers. That rose by just 0.2% in June, the slowest monthly pace since February 2021.

In the past three months, core inflation has risen at a 4.1% annualized pace — down almost a full percentage point from May.

Under the hood, there was notable disinflation across a key sector of the economy monitored by the Fed: core services, excluding shelter. Prices in that category were flat last month, compared to a 0.2% rise in May.

That cooling is happening alongside a still-healthy labor market and solid wage gains (more on this below), which officials worried could stoke inflation in this category.

The Biden administration is eager to tout the progress. “The economy is defying predictions that inflation would not fall absent significant job destruction,” top White House economic adviser Lael Brainard is expected to say this afternoon at the Economic Club of New York, according to prepared remarks.

“Annual inflation has now declined every month for 12 months in a row,” she will say, “and inflation in the United States is now the lowest among G-7 nations … even as our economic recovery from the pandemic has been the strongest.”

The bottom line:

We have been head-faked before by what appeared to be remarkable progress on inflation, notably in the summer of 2001.

With expected cooling in other areas (including shelter, which makes up a big chunk of the index), there is reason to be hopeful this progress could be here to stay.

The U.S. economy added 517,000 jobs in January, and the unemployment rate fell to 3.4% — the lowest level in over a half-century, the government said on Friday.

Why it matters:

Employers added jobs at an unexpectedly rapid pace, the latest sign of a hot labor market despite aggressive moves by the Federal Reserve to cool it down.

The numbers are more than double the 190,000 forecasters anticipated.

Details:

The extraordinary reportcomes as the Fed continues to dial back its pace of interest rates and prepares to raise rates further to restrain the economy and chill still-high inflation.

Fed chair Jerome Powell has acknowledged progress on slowing inflation in recent months while noting risks lie ahead. Among them is wage growth, which is rising at a pace still too swift for the Fed’s comfort.

In January, average hourly earnings rose 0.3% — or 4.4% over the previous year, according to Friday’s data.

The big picture:

The data also showed that employment in 2023 was even stronger than initially thought, with roughly 568,000 more jobs than previously reported.

The update was part of the Labor Department’s annual revisions, which incorporate more complete data from insurance records and updated seasonal adjustments.

The U.S. economy grew at an annualized 2.9% rate in the final months of 2022, the Commerce Department said on Thursday.

Why it matters:

Economists are bracing for a significant slowdown in economic activity as the Federal Reserve’s interest rates hikes take hold, but that certainly wasn’t the case in the final months of last year.

Economists expected the Gross Domestic Product figures to show the economy grew at a 2.6% annualized rate last quarter, after expanding at a 3.2% pace in the prior quarter.

Details:

Consumer spending and businesses built up private inventories gave GDP the biggest boost. Among the biggest drags: fixed investment, a category that includes housing.

By the numbers:

Over the calendar year, GDP grew by 2.1% in 2022 — a decent pace, especially considering the historically aggressive rate hikes by the Federal Reserve that sought to restrain economic activity to contain inflation.

Those rate hikes hit the housing sector particularly hard, which dragged down overall growth earlier last year.

Catch up quick:

The first half of 2022 was dogged by fears that the economy had entered a recession, after back-to-back quarters of contractions. But by the second half of the year, the economy had returned to growth mode.

The growth over 2022 was an expected slowdown from the 5.9% achieved in 2021, when the economy bounced back from the pandemic shock.

It may be time to update your inflation narrative.

The ultra-hot readings that defined the first half of 2022 appear to be firmly in the rearview mirror, improving the odds that price pressures can dissipate further without excessive economic pain.

That’s the key takeaway from the December Consumer Price Index released this morning, which confirmed notably cooler inflation as the year came to a close.

Why it matters:

The nation’s inflation problem isn’t over, but so far inflation is slowing while the job market is still healthy, an enviable combination.

As Princeton economist Alan Blinder put it in an op-ed last week, inflation was “vastly lower” in the second half of 2022 than the first; yet, “hardly anyone seems to have noticed.”

By the numbers:

In the final three months of 2022, core inflation (which excludes food and fuel costs) came in at an annualized 3.1% — higher than the Fed aims for, but hardly crisis levels. In the second quarter of the year, that number was 7.9%.

It’s a stunning decline, occurring alongside a labor market that by nearly all measures is still flourishing. Just this morning, the Labor Department announced that jobless claims fell to an ultra-low 205,000 last week.

State of play:

Grocery prices rose 1.1% in the final three months of the year, an uncomfortably high rate, but not as extreme as the rates seen earlier in 2022.

Gasoline prices, pushed up by Russia’s invasion of Ukraine, were once the crucial reason why inflation was rising. In recent months, the opposite has been true: December pump prices slid 9.4%, helping drag the overall index into negative territory.

Disinflation was at work for many other goods, including used cars (-2.5%) and new vehicles (-0.1%) where prices have reversed, helped by easing supply chain bottlenecks.

Shelter costs pushed inflation upward, surging 0.8% in December. But private-sector data points to rents on new leases falling in recent months, which would only filter into the CPI data over time. That makes for a more benign inflation outlook in 2023.

What to watch:

That’s not to say there aren’t risks ahead. The war in Ukraine is ongoing, and another energy price shock could occur.

The Fed has also focused in on the services sector, where price increases have slowed from last summer but remain frothy. The risk is that business costs associated with the still-tight labor market (like higher wages) will pass through to prices for consumers.

The bottom line:

Inflation will still be a worry in 2023, but much less so than it seemed a few months ago.

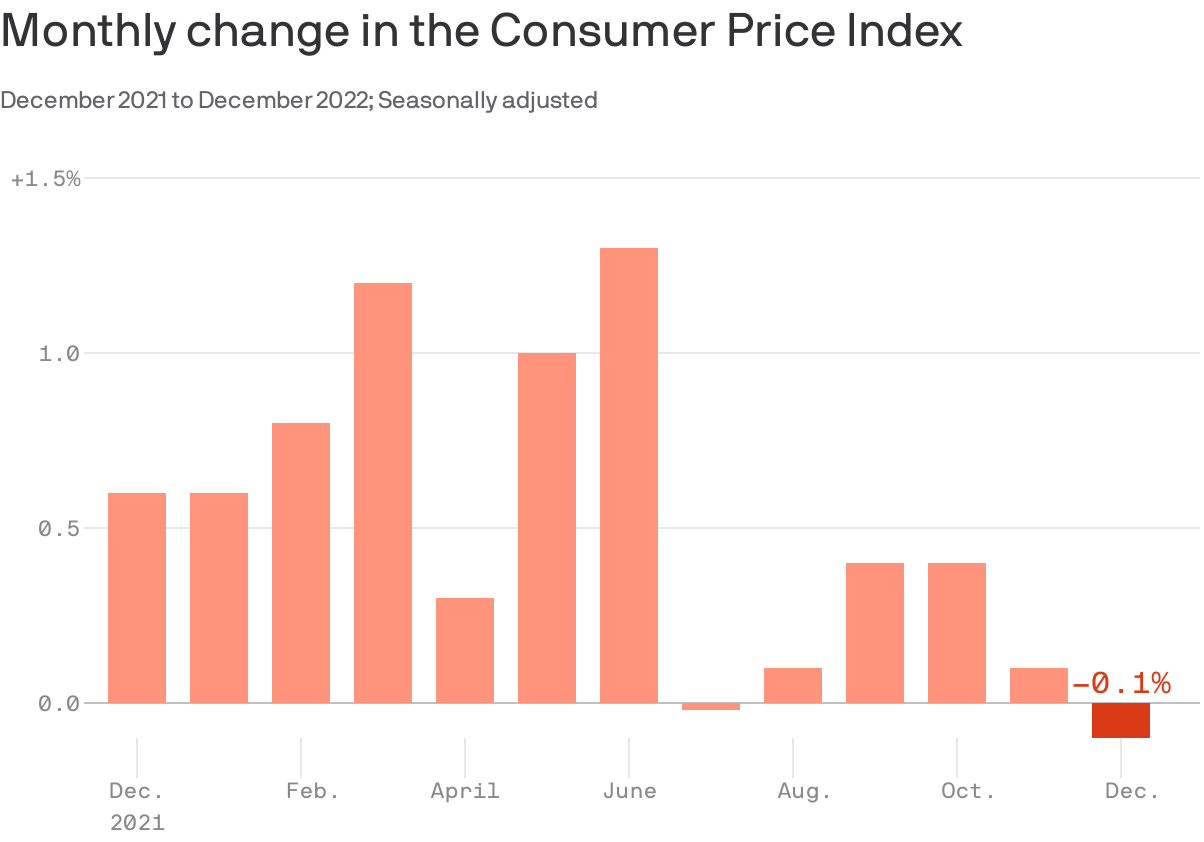

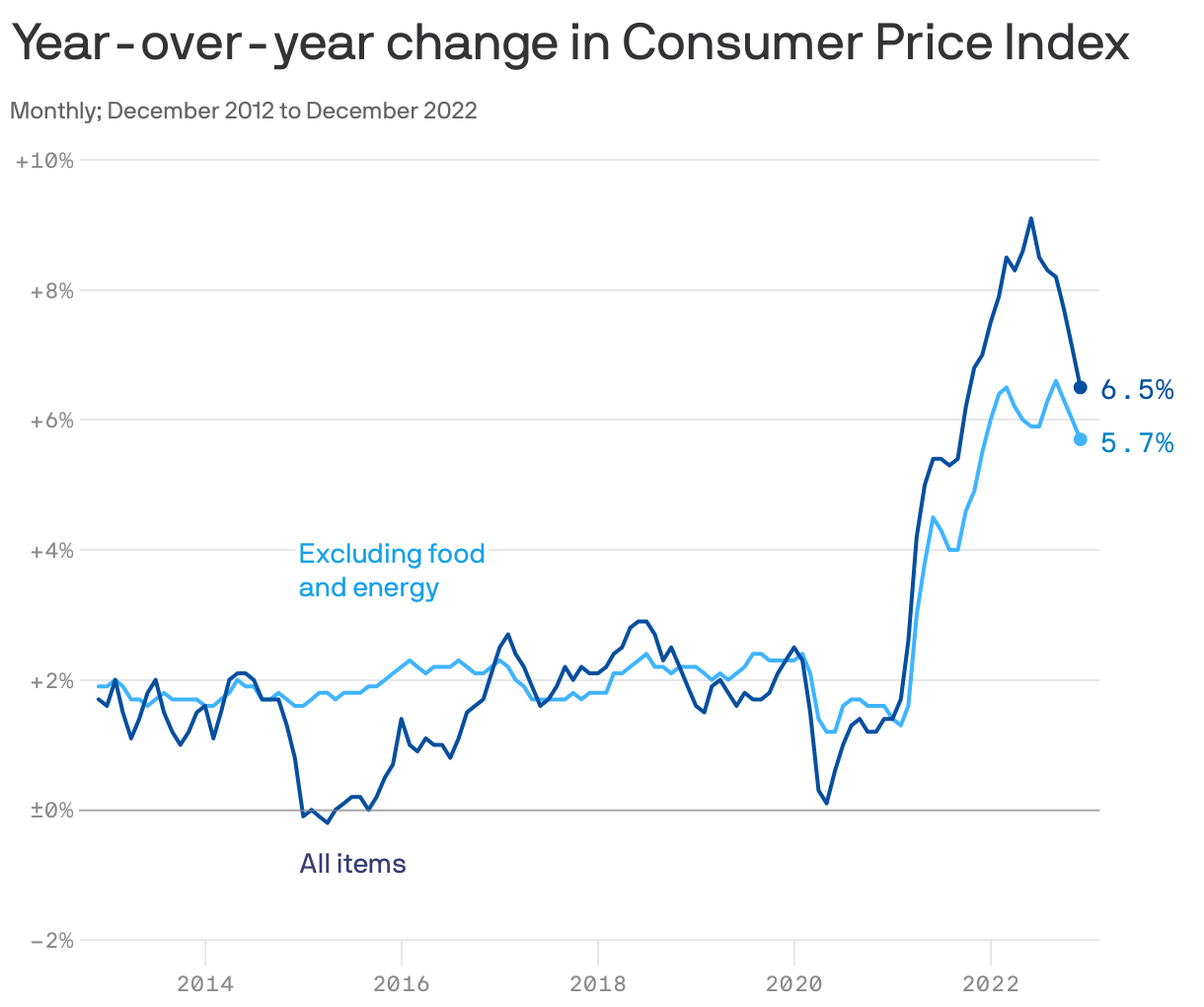

U.S. consumers got a reprieve from soaring costs in December: the Consumer Price Index declined on a monthly basis, the first drop since last summer as falling prices for items including gasoline and used carsdragged the overall index down.

By the numbers:

The index, which captures price changes across a basket of consumer goods and services, fell 0.1%, following an increase by the same amount in November. Over the past 12 months ending in December, the index is up 6.5%, falling from 7.1% through November.

Core CPI, which excludes food and fuel costs, rose by0.3% last month. Over the last 12 months through December, the index rose 5.7%. In November, those figures were 0.2% and 6%, respectively.

Why it matters:

The hot inflation that persisted through much of last year continues to show signs of receding — offering at least some relief for shoppers, the White House and the Federal Reserve, though some underlying inflation pressure remains.

Where it stands:

The data caps a year in which consumer prices rose rapidly, though the pace of cost increases began to slow in the final months of the year.

As consumers shifted spending and supply chains began to heal, price increases for a range of goods have cooled or, in some cases, costs have fallen outright.

Between the lines:

The Federal Reserve, which has been raising interest rates aggressively to tame inflation, is watching the services sector closely, where inflation can be more challenging to stamp out.

A sub-index measuring price moves within the services category (excluding housing) accelerated by 0.4%, after two straight months of cooler readings

Still, in the 12 months through December, this sub-index is up 7.4%(compared to 7.3% in November).