https://mailchi.mp/e1b9f9c249d0/the-weekly-gist-september-15-2023?e=d1e747d2d8

The pandemic worsened the existing mental health crisis in the United States, greatly increasing demand for care. In this week’s graphic, we highlight new data from JAMA Health Forum on mental healthcare trends from 2019 to 2022.

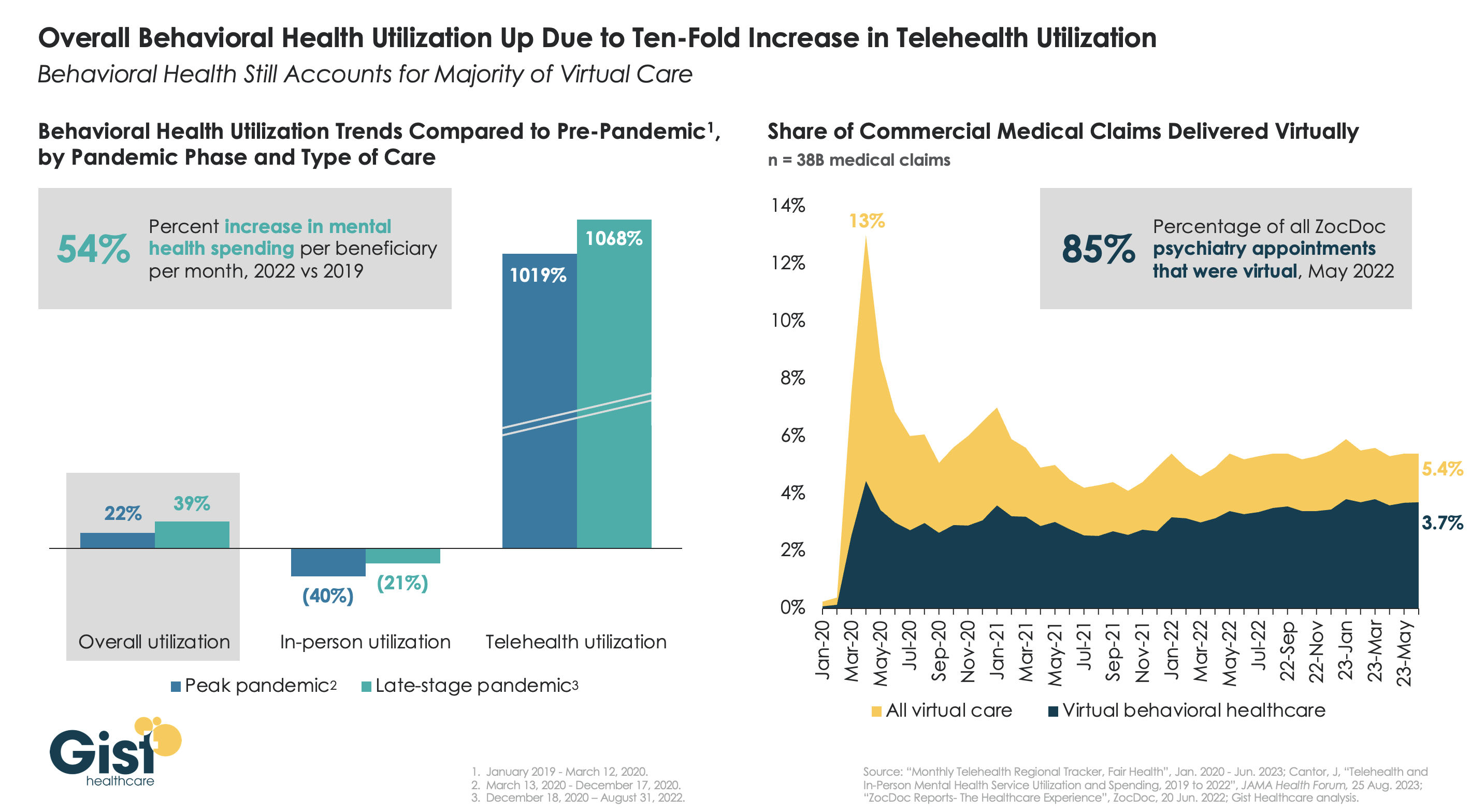

Overall behavioral health utilization increased in 2022 compared to pre-pandemic and peak-pandemic levels, fueled by a ten-fold increase in telehealth usage.

In-person behavioral health utilization decreased early in the pandemic and declines continued in 2022, compared to pre-pandemic levels. Behavioral health still accounts for more than two-thirds of all telehealth visits, a trend that has remained largely unchanged since 2021.

While many consumers and mental health providers continue to embrace telehealth as a means to expand access and increase affordability, a recent Morning Consult survey found that most Americans actually favor in-person visits for quality and efficiency—that is, if they can access it.

Additionally, the future of some types of virtual behavioral healthcare remains murky as the Drug Enforcement Agency (DEA) has yet to establish rules for prescribing controlled substances via telehealth beyond November 2024.