Health insurance is complicated. In many states, it’s about to get worse.

Where states allow short-term plans without restriction, the plans will be a lot cheaper than those sold on the exchanges because they don’t have to comply with the ACA. But that low price comes with big tradeoffs.

Short-term plans don’t have to sell to all comers, nor do they have to cover pre-existing conditions. Sick people will have no real choice but to buy insurance on the exchanges. To cover the medical costs of a relatively sicker group of people, exchange insurers will have to increase their premiums.

People who earn less than four times the poverty level will be shielded from the price increases because the ACA caps premiums at no more than about 10% of income. The federal government, however, has to pick up the rest of the tab-so as prices go up, federal outlays will, too, squandering an estimated $38.7 billion over 10 years.

Hurt worst will be people who earn more than four times the poverty level. Federal actuaries estimate that they’ll pay 6% more on account of the short-term rule by 2022. That will come on top of price increases associated with Congress’s repeal of the individual mandate. In 2019 alone, the Urban Institute predicts that insurance prices will grow, on average, by about 18%.

Beyond that, people who buy short-term plans may be surprised to discover just how stingy they are. Insurance is complicated: people rarely read, much less understand, all the fine print. And there’s a lot of fine print.

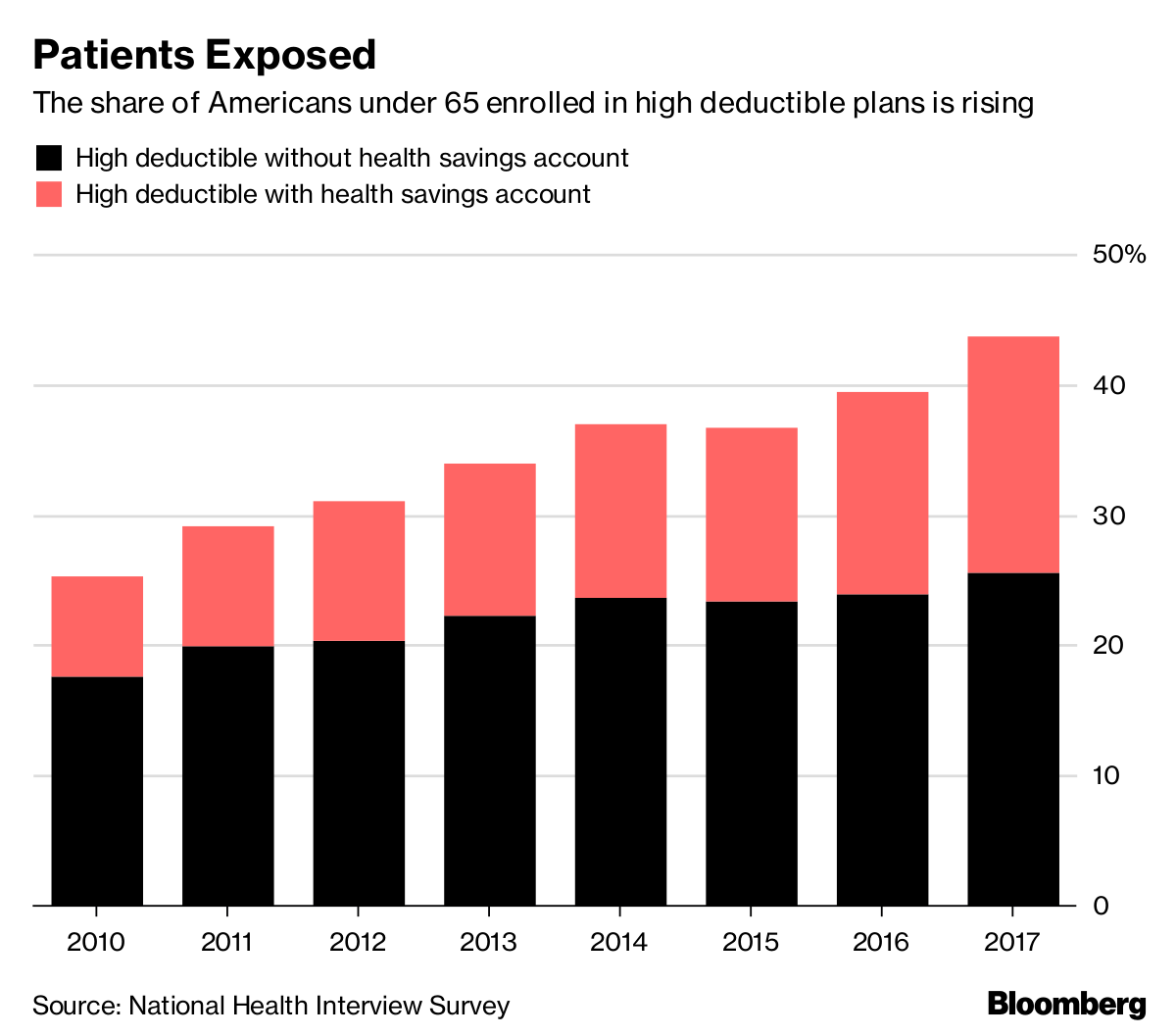

In a series of recent decisions, the Trump Administration is taking steps that will sharply raise insurance premiums for people aged 50 to 64, just before they become eligible for Medicare. While these steps are likely to make coverage less expensive for young, healthy consumers, they will inevitably raise costs for middle-aged people with chronic conditions. For many, insurance will become unaffordable. And that lack of coverage will eventually result in higher costs for Medicare.

Trump is taking three major steps that will affect the availability of Affordable Care Act health insurance for middle-aged consumers.

Repealing but not replacing

First, at the urging of the Trump Administration, Congress last year repealed the tax penalty that has to be paid by those without health insurance, effective for tax year 2019. The penalty is the ACA’s mechanism to push people to buy insurance. The logic: By broadening the pool of those with ACA insurance to include those less likely to incur significant medical costs, the individual mandate would keep premiums relatively low for everyone.

Then, early this month, the Trump Administration refused to defend the remaining provisions of the ACA in federal court. In the case Texas v. the federal Department of Health and Human Services, 20 red states argued that, absent the now-repealed individual mandate, the rest of the ACA will be unconstitutional. Thus, all its other provisions, including several important to those older consumers, also would be thrown out. They include premium limits for those 50-64, minimum benefit requirements, and the ban on insurance companies rejecting potential purchasers due to pre-existing conditions.

Pre-existing conditions

Prior to the ACA, in a practice known as age-rating, 60-year-olds could pay premiums that were 11 times higher than younger buyers. The ACA capped that ratio at 3:1. AARP estimates that bumping it up to 5:1 would raise annual premiums for a 60-year-old by more than $3,000, or 22%.

Similarly, allowing carriers to underwrite for pre-existing conditions would make insurance widely unavailable for people aged 50 to 64. AARP estimates that 25 million people, or 40% of those 50 to 64, have a condition that could disqualify them from non-group insurance.

The Urban Institute’s Health Policy Center estimates that tossing out the remaining provisions of the ACA would result in 17 million people losing commercial insurance and another 15 million losing Medicaid and children’s health care under the CHIP program.

By Urban colleagues project that even those remaining in the private individual insurance market “would likely have policies that cover fewer benefits and require more out-of-pocket spending for services.”

Rare agreement

The Texas lawsuit, and the Administration’s refusal to defend the law in court, has generated an outpouring of opposition. It created a rare moment when consumer groups, hospitals, and doctors agreed on a health policy issue.

But the story doesn’t end there. This week, the Trump Administration took one more step towards dismantling the ACA in a way that will likely harm pre-Medicare consumers: The Department of Labor adopted new rules opening the door to low cost, low-benefit health plans. These will now be widely available to small businesses and, importantly, self-employed individuals.

The Congressional Budget Office estimates that 4 million people will buy these policies, sold by association health plans (AHPs). The consulting firm Avalere Health estimates that individual AHP premiums will be an average of $9,700 cheaper than ACA coverage, and that 1 million people will shift from marketplace plans to AHP policies. But it predicts premiums will rise by 3.5 percent for more comprehensive ACA insurance, largely because the remaining consumers will be older and sicker than AHP buyers.

President Trump promotes these plans as a less costly alternative to ACA coverage. This week he told the National Federation of Independent Business, “You’re going to save massive amounts of money and have much better health care. You’re going to save a fortune and you’re going to be able to give yourselves and your employees tremendous health care.”

Low cost, few benefits

But the plans do not include any minimum benefit requirements. Thus, they can exclude coverage for pregnancies, mental health issues, or drugs or hospital care. Carriers won’t be able to exclude buyers on the basis of pre-existing conditions but can adjust premiums based on age or sex. And, because they often exclude benefits important to those with chronic conditions, such as medications, they don’t need to underwrite: Those consumers simply won’t buy these policies.

Priced out of ACA coverage and uninterested in limited insurance that won’t cover their needs, it is easy to imagine many of those in their early 60s simply going without coverage (and care) until they become eligible for Medicare at age 65. That will not only put their health at risk, it will raise Medicare costs. Medicare spends about one-third more on medical care for those who join the program without having had insurance in the year before enrolling.

The result of all this: Trump is creating two separate individual health insurance markets, one for young and healthy people, and one for older and sick people. Some young people may buy low-cost policies that will serve them well—until they get sick. Many older people won’t buy insurance at all, risking their health and, very likely, raising costs to government.

http://money.cnn.com/2018/06/21/news/economy/health-care-worker-shortage-ohio/index.html

In the three years since, she’s worked as a janitor at a local college, then as a quality manager at an auto supplier. But she wanted a position that offered a lot more job security – and better pay than those jobs.

When she heard about the growing demand for health care workers, she started looking around and found Mercy College of Ohio about 10 minutes away.

The school, which is based in Toledo, specializes in health sciences and offers 16 programs that train students for a variety of medical professions, including certificate programs that can be completed in as little as one semester to master’s degrees.

In January, Ellis enrolled to get a certificate in polysomnographic technology, which will qualify her to conduct sleep studies for patients suffering from disorders such as sleep apnea. To her, it was a perfect fit: not only could she complete the program in just 12 months, she was already accustomed to working late shifts.

“I worked nights a lot at CSX. And most sleep studies are also done at night,” she said, noting that her classmates include a former mechanic, a musician and someone who worked for a delivery company.

At job fairs and community events, Mercy College’s recruiters are seeking out students from a variety of fields, but especially the manufacturing and retail sectors — which have been hit by layoffs after big companies like General Motors, DHL and Toys R Us left scores of people looking for work.

That could prove to be a real boon for the area’s health care system, said Jason Theadore, vice president of ambulatory services and business development with Mercy Health, which partners with the college and operates 23 hospitals and 500 health care centers throughout the state.

Manufacturing workers, he said, come with the experience of working long shifts and odd hours And former retail workers can help put a different spin on customer care in a health care setting.

“People from diverse career backgrounds are helping us think differently about how we deliver care,” said Theadore.

The health care industry also desperately needs the workers. Consulting firm Mercer estimates the United States will need to hire 2.3 million new health care workers by 2025 to adequately take care of the country’s aging population.

“Right now, the labor supply just isn’t there,” said Matt Stevenson, a partner at Mercer.

With unemployment near record lows, the workers that are available often aren’t armed with the right skills.

That’s where programs like Mercy College’s comes in.

Each year, the school graduates roughly 400 students. Among its most popular short-term programs are the ophthalmic technology (training to assist ophthalmologists), community health worker, EMT/paramedic and the sleep technology certificates.

Many of the grads end up working for the Mercy Health System, which operates 23 hospitals and 500 health care centers throughout Ohio.

Kathy Damshroder has been teaching polysomnographic technology at Mercy College since last year.

“Everyone with this skill who wants a job has gotten one,” said Damshroder, 55, who also works as a sleep technologist at Mercy Health hospital in Toledo.

According to Mercy College, nearly all the school’s certificate graduates have been employed in their specialty.

Damshroder graduated from Mercy in 2010. Before that, she ran her own hair salon for 25 years in the nearby town of Elmore, Ohio.

“I still own it,” she said.

Like Ellis, the long-term job security of working in the health care industry appeals to her.

“And there’s bang for the buck,” she said. “Entry level pay is about $22 an hour and goes up. The other huge draws are benefits and retirement plans, which I didn’t have as an entrepreneur.”