The fate of ObamaCare repeal-and-replace could hinge on an amendment from Sen. Ted Cruz.

The Texas senator is pushing for a provision that would allow insurers to sell plans that do not comply with ObamaCare insurance regulations, so long as they also sell plans that comply with those rules. Cruz says giving insurers a path around the regulations should allow them to offer some plans at a lower cost.

It’s unclear whether the amendment will be added to the Senate bill, or even whether it will pass muster under budgetary rules.

But the amendment could be the key to ensuring that the legislation passes both the House and the Senate.

House Freedom Caucus Chairman Mark Meadows (R-N.C.) indicated he could support the Senate bill if the Cruz amendment is included. That’s different than a little over a week ago, when Meadows said the Senate’s legislation lacked enough conservative support to pass the House.

“If the Cruz Consumer Choice amendment gets there, yes I can support it without the MacArthur amendment in there because I think it gives everybody some options,” Meadows told reporters late last week.

Leaders have sent two version of a revised Senate healthcare bill to the Congressional Budget Office — one with the Cruz amendment and one without it, a GOP aide confirmed to The Hill.

The text of Cruz’s amendment hasn’t been publicly released, but the goal is for the plans that don’t adhere to ObamaCare’s insurance regulations to be cheaper than those that do.

For many conservatives, lowering insurance premiums is key.

It wasn’t easy to net conservatives’ support in the House for the healthcare bill, as it took weeks for the ultra-conservative Freedom Caucus to come on board.

Leadership couldn’t pass the bill without Freedom Caucus votes, and eventually won their support after the addition of a controversial amendment from Rep. Tom MacArthur (R-N.J.). That amendment would let states apply for waivers to opt out of certain core ObamaCare insurance requirements, such as a ban from charging sick people more and the requirement that they cover a list of “essential” services, such as maternity and mental health care.

Meadows suggested the Cruz amendment would be an acceptable substitute for the House’s MacArthur amendment.

“Right now I’m looking at the Cruz consumer Choice amendment as the primary vehicle that makes the most sense to me,” Meadows said, “and I applaud him for stepping out.”

The Cruz amendment could also help get the vote of Sen. Mike Lee (R-Utah), who quickly came out in opposition to the Senate bill in its current form, in part because it doesn’t lower the cost of consumers’ healthcare enough.

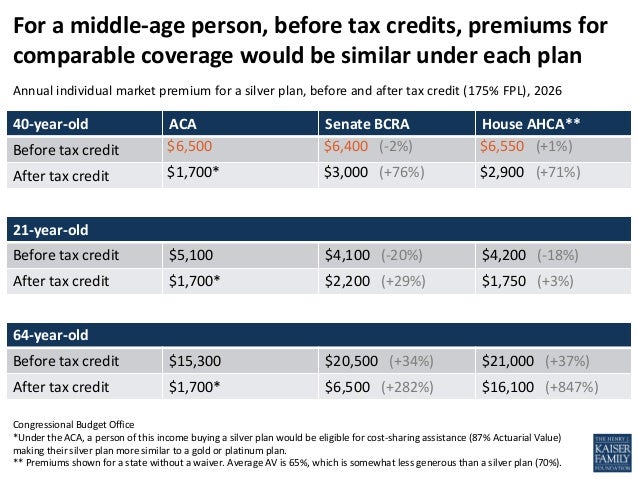

In an analysis of the Senate bill, the nonpartisan Congressional Budget Office estimated premiums would be 20 percent higher in 2018 and 10 percent higher in 2019. Then, in 2020, premiums would drop 30 percent lower than under ObamaCare.

In a June 23 Medium post, Lee wrote that “for all my frustrations about the process and my disagreements with the substance of [the Better Care Reconciliation Act], I would still be willing to vote for it if it allowed states and/or individuals to opt-out of the Obamacare system free-and-clear to experiment with different forms of insurance, benefits packages, and care provision options.”

But the Cruz amendment risks alienating Senate moderates, who want to keep the protections for pre-existing conditions in place.

Previous efforts at health care reform show us that rural areas are uniquely vulnerable. Efforts need to take account not only of coverage and access – as has been the focus of the current debate – but also how reform affects rural health care institutions and the larger social factors shaping overall health.

The particular economic factors affecting rural health care institutions make rural areas particularly vulnerable to political shifts that disrupt services for existing patients and for those newly insured, creating immense challenges for rural providers. Steps that fail to account for the impact of financial hardship on these institutions not only hurt their bottom line but contribute to poor morale and workforce turnover and larger-scale decisions to reduce services, which decrease their ability to address patient needs.

If our leaders are serious about reform that will lessen the rural-urban mortality gap, they should recognize the unique needs of rural America and ensure health care policy reflects how vital access to quality care is to their financial success – not to mention their well-being.

After much secrecy and no public deliberation, Senate Republicans finalized release their “draft” repeal and replace bill for the Affordable Care Act on June 22. Unquestionably, the released “draft” will not be the final version.

Amendments and a potential, albeit not necessary, conference committee are likely to make some adjustments. However, both the House version – American Health Care Act (AHCA) – and the Senate’s Better Care Reconciliation Act (BCRA) will significantly reduce coverage for millions of Americans and reshape insurance for virtually everyone. The Congressional Budget Office (CBO) is expected to provide final numbers early the week of June 26.

If successful, the repeal and replacement of the Affordable Care Act would be in rare company. Even though the U.S. has been slower than any other Western country to develop a safety net, the U.S. has rarely taken back benefits once they have been bestowed on its citizenry. Indeed, only a small number of significant cases come to mind.

My academic work has analyzed the evolution of the American health care system including those rare instances. I believe historical precedents can provide insights for the current debate.

Providing help to mothers and infants

The first major federal grant program for health purposes was also the first one to quickly be eliminated. The program was authorized under the Sheppard-Towner Maternity and Infancy Protection Act of 1921. It provided the equivalent of US$20 million a year in today’s dollars to states in order to pay for the needs of women and young children.

Sheppard-Towner, which provided funding to improve health care services for mothers and infants, was enacted after a long debate in Congress amid accusations of socialism and promiscuity. Interestingly enough, the act may have passed only due to pressure from newly voting-eligible women.

Jeanette Rankin, the original sponsor of the Shepard-Towner Act and the first woman elected to Congress, pictured in 1970.John Duricka/AP

Overall, the program was responsible for more than 3 million home visits, close to 200,000 child health conferences and more than 22 million pieces of health education literature distributed. It also helped to establish 3,000 permanent health clinics serving 700,000 expectant mothers and more than 4 million babies.

The program continued until 1929, when Congress, under pressure from the American Medical Association, the Catholic Church and the Daughters of the American Revolution, terminated the program. Without federal support, a majority of states either eliminated the programs or only provided nominal funding. Fortunately for America’s children and mothers, the Social Security Amendment of 1935 reestablished much of the original funding and expanded it over time.

Helping America’s farmers during the New Deal

America’s next major program confronted a similar fate. To address the challenges of rural America during the Great Depression, the federal government developed a variety of insurance and health care programs that offered extensive and comprehensive services to millions of farm workers, migrants and farmers.

Grandmother and sick baby of a migratory family in Arizona. These types of families were targeted for help by the Farm Security Administration.NARA/ Dorothea Lange

Some of these programs provided subsidies to farmers to form more than 1,200 insurance cooperatives nationwide. At times, the federal government’s Farm Security Administaton (FSA) provided extensive services directly to migrant farm workers through medical assistance on agricultural trains, mobile and roving clinics, migratory labor camps that included health centers staffed with qualified providers, full-service hospitals and Agricultural Workers Health Associations (AWHA).

In all cases, services were generally comprehensive and included ordinary medical care, emergency surgery and hospitalization, maternal and infant care, prescription drugs and dental care.

Although these services were accepted during wartime, the American Medical Association and the Farm Bureau opposed them, which ultimately led to their demise shortly after World War II. Millions of farmers lost their insurance.

Medicaid in the 1980s

Perhaps the most indicative expectations on what will happen in case congressional Republicans are able to pass their proposal hails from the Medicaid program itself.

In the early 1980s, Medicaid underwent a series of cuts and reductions leading to the first contracting in the program’s history. These involved both a reduction in federal funding and in eligibility, and an increase in state flexibility to run the program, as do the Republican proposals in Congress.

The 1980s also saw the creation and quick demise of another health care program. The Medicare Catastrophic Coverage Act of 1988 sought to fill in the gaps of the original Medicare program for America’s seniors. Specifically, it sought to provide them with protection from major medical costs and offer them a prescription drug benefit for the first time.

Similarly to the Affordable Care Act, the law had a redistributive foundation by requiring richer seniors to contribute more than poorer individuals. Also, similarly to the Affordable Care Act, it phased in benefits over a period of time.

Congress, confronted by affluent seniors who would have shouldered much of the financial burden of the program, quickly repealed much of the law before its provisions came into effect.

A Republican President, George W. Bush, was responsible for extending prescription drug benefits to seniors under Medicare Part D.Jason Reed/Reuters

It took more than a decade to provide America’s seniors with a prescription drug benefit through Medicare Part D, while only limited steps have been taken to protect seniors from major medical losses.

The consequences of those rare cases are nonetheless instructive. States were unable to continue the program without federal support or offer a valid replacement. Indeed, the programs quickly faded away. With them, millions of Americans lost access to health care.

In all three previous cases, the federal government eventually renewed its financial support. However, at times it took time for a replacement program to emerge.

The current changes proposed by congressional Republicans, particularly to the Medicaid program, are tremendously more consequential than anything we have previously experienced.

Indeed, in scale and extent, the proposed changes are unprecedented and would significantly roll back, likely for the foreseeable future, America’s safety net.

Republicans may be too timid or lack the votes to advance structural reform. And they may feel it necessary to prop up insurance companies struggling with the costs of insuring high-risk patients. That’s a fair calculation.

But are they ready to create a health care system that aids every group except the working poor? The wealthy will have their health care and their tax cuts. The middle classes will continue to enjoy expensive, generous insurance that’s indirectly funded through the tax code. And insurance companies will accept whatever assistance the government provides – from tax cuts to coverage penalty periods – to continue increasing their authority over the medical system.

That’s an arrangement that leaves out the very groups that are most desperate for health care reform: lower-income families and the working poor.

As Majority Leader Mitch McConnell (R-Ky.) tries to negotiate his way to a health bill that can win at least 50 Republican votes, there is one woman in the Senate who could stop the bill cold.

She isn’t even a senator.

Elizabeth MacDonough is the Senate’s parliamentarian, the first woman to hold that post, which involves advising senators on the chamber’s byzantine rules and procedures. She alone can decide what pieces of the emerging Senate overhaul of the Affordable Care Act can be included under the budget reconciliation process senators are using. That process allows them to pass the measure with a simple majority vote rather than needing the usual 60.

In theory at least, she could reject the very deals McConnell is trying to cut.

By all accounts, MacDonough, who has spent almost her entire career working for the Senate and was appointed to her position in 2012, is scrupulously fair and trusted by both major parties.

“Elizabeth is great,” said Rodney Whitlock, a former Republican staffer on the Senate Finance Committee who has argued tricky legislative points before her numerous times. Democrats agree. “She’s a straight shooter and an honest broker,” said Bill Dauster, a longtime Democratic staff director for the Budget Committee.

It’s good that both sides like her, because if the Senate bill comes to the floor, MacDonough may have to make some tough decisions that will make one side or the other very unhappy.

MacDonough, along with her assistant parliamentarians, are charged with deciding which pieces of the bill violate the rules of budget reconciliation, in particular the “Byrd Rule,” named for its author, the late Sen. Robert Byrd (D-W.Va.). That rule requires that everything in the bill pertain directly to the federal budget. The idea is to prevent senators from loading up the budget bill, which gets fast-track consideration, with unrelated items that belong in the regular, slower Senate process.

The judgments mostly involve parts of the bill that opponents argue don’t add to or subtract from federal spending, or whose budget impact is “merely incidental” to the purpose of the policy. Outside observers say the parts of the Senate measure that are vulnerable under this rule include provisions that would defund Planned Parenthood and those affecting the rules for private insurance plans.

Generally, the “Byrd bath,” as it’s called on Capitol Hill, involves a string of meetings between Senate committee staff and the parliamentarian.

(Photo courtesy of the U.S. Senate)

“The Democrats go in, the Republicans go in, then both of them go in together,” said Dauster. Each side argues whether certain language should or should not be allowed in the bill.

The parliamentarian’s office in the Capitol “is actually a small room,” said Whitlock. “And when they are ready to have you in, you’re standing around and all the assembled in the room have at it.”

MacDonough does not make her rulings immediately after the arguments. “She has, of late, gotten back to people by email” with her decisions, said Dauster.

That has not always been the case. In the past, said Bill Hoagland, a longtime GOP staff director for the Senate Budget Committee, after making their arguments “we would wait until we went to the floor and [a senator] would raise a point of order” against some specific language, and senators and staff would learn the parliamentarian’s decision only then.

MacDonough’s ruling may prompt the bill’s authors to delete language before the bill comes to the Senate floor. Or they may opt to let the drama may play out in front of the C-SPAN cameras. Any senator can raise a point of order against a specific provision claiming it violates the Byrd Rule. It takes 60 votes to overcome such a point of order.

But what if Senate leaders opt not to accept MacDonough’s decision?

“That’s what scares the heck out of me,” said Hoagland. Under the Senate’s rules, the senator who is acting as the presiding officer during the debate does not have to take the parliamentarian’s advice. But if he or she rules against what the parliamentarian has advised, “I would argue that you have basically destroyed the Byrd Rule and you’ve destroyed the purpose of reconciliation at that point,” he said.

That’s because it would allow the majority party, which controls the Senate, to effectively include any provisions it wants in the fast-track budget bill with only a simple majority.

“It’s another way to go nuclear,” said Dauster, referring to efforts to end the Senate filibuster, which requires 60 votes to break.

Will that happen? It depends how MacDonough rules. And how badly the Republicans want their health bill to pass.

The path to 50 votes for an Obamacare replacement bill seemed to narrow dramatically Thursday as efforts to craft a quick compromise foundered — but Senate Majority Leader Mitch McConnell has $200 billion to build a bridge to victory. His dealmaking may be just beginning.

While many policy experts, lobbyists and senators Kaiser Health News spoke to this week seemed skeptical that the Better Care Reconciliation Act could be saved, they said they could envision a way for McConnell (R-Ky.) to succeed in crafting a bill that would partially replace the Affordable Care Act.

McConnell has significant wiggle room in his repeal bill. Under the budget rules he is using to move the legislation, he needs to reach $133 billion in deficit reduction over 10 years. The Congressional Budget Office estimated that the BCRA would save $321 billion.

That leaves about $200 billion in deficit savings that McConnell can afford to give back and use to make deals with as many as a dozen senators who oppose his draft bill.

“There’s clearly a path to do this,” said Matt Salo, the executive director of the National Association of Medicaid Directors. “McConnell has enough candy to do it, and enough time. It’s still a very real possibility.”

Figuring out exactly how to spread the confectionery around, though, is no simple matter.

Air Force veteran Billy Ramos, from Simi Valley, Calif., is 53 and gets health insurance for himself and for his family from Medicaid — the government insurance program for low-income people. He says he counts on the coverage, especially because of his physically demanding work as a self-employed contractor in the heating and air conditioning business.

“If I were to get hurt on the job or something, I’d have to run to the doctor’s , and if I don’t have any coverage they’re going to charge me an arm and a leg,” he said. “I’d have to work five times as hard just to make the payment on one bill.”

There are about 22 million veterans in the U.S. But fewer than half get theirhealth care through the Veterans Affairs system; some don’t qualify for various reasons or may live too far from a VA facility to easily get primary health care there.

Many vets instead rely on Medicaid for their health insurance. Thirty-one states and the District of Columbia chose to expand Medicaid to cover more people — and many of those who gained coverage are veterans.

The GOP health care bill working its way through the Senate would dramatically reduce federal funding for Medicaid, including rolling back the expansion funding entirely between 2021 and 2024.

Air Force veteran Billy Ramos, now 53, in a 1982 photo from his basic training days as an airman in Texas, at Lackland Air Force Base. Now self-employed, Ramos relies on Medicaid for his family’s health insurance needs. (Courtesy of Billy Ramos)

Medicaid coverage recently has become especially important to Ramos — a routine checkup and blood test this year showed he’s infected with hepatitis C. California was one of the states that chose to expand Medicaid, and the program covers Ramos’ costly treatment to eliminate the virus.

“Right now, I’m just grateful that I do have [coverage],” he said. “If they take it away, I don’t know what I’m going to end up doing.”

The Senate health plan — which proposes deep cuts to federal spending on Medicaid — has veterans and advocates worried. Will Fischer, a Marine who served in Iraq, is with VoteVets.org, a political action group that opposes the Republican health plan.

“If it were to be passed into law, Medicaid would be gutted. And as a result, hundreds of thousands of veterans would lose health insurance,” Fischer said.

It’s too early to know just how many veterans might lose coverage as a result of the Medicaid reductions. First, states would have to make some tough decisions: whether to make up the lost federal funding, to limit benefits or to restrict who would get coverage.

“The people who are saying that this is going to harm millions of veterans are not being entirely truthful,” Caldwell said. “They’re leaving out the fact that many of these veterans qualify for VA health care or in some cases already are using VA health care.”

About a half-million veterans today are enrolled in the VA’s health care program as well as in some other source of coverage, such as Medicaid or Medicare. Andrea Callow, with the non-profit group Families USA, wrote a recent report showing that nearly 1 in 10 veterans are enrolled in Medicaid.

“Oftentimes veterans will use their Medicaid coverage to get primary care,” Callow said. “If, for example, they live in an area that doesn’t have a VA facility, they can use their Medicaid coverage to see a doctor in their area.”

Whether a particular veteran qualifies for coverage through the VA depends on a host of variables that she said leaves many with Medicaid as their only option.

But, Caldwell said, rather than fighting to preserve Medicaid access, veterans would be better served by efforts to reform the care the VA provides to those who qualify.

“We believe that giving veterans more health care choice and restructuring the VA so that it can act more like a private health care system will ultimately lead to veterans who use the VA receiving better health care,” he said.

The Urban Institute found that the first two years after the enactment of the Affordable Care Act saw a nearly 44 percent drop in the number of uninsured veterans under age 65 — the total went from 980,000 to 552,000. In large part, that was the result of the law’s expansion of Medicaid.

Behavioral health conditions affect a substantial number of people in the U.S. and are especially common among people with low incomes.1,2,3 Behavioral health conditions include mental illnesses, such as anxiety disorders, major depression, bipolar disorder, schizophrenia, and post-traumatic stress disorder, as well as substance use disorders (SUD), such as opioid addiction. These conditions range in severity, with some being more disabling than others. People with behavioral health needs may require a range of services, from outpatient counseling or prescription drugs to inpatient treatment.

As a major source of insurance coverage for low-income Americans, and as the only source of funding for some specialized behavioral health services, Medicaid plays a key role in covering and financing behavioral health care. In 2015, Medicaid covered 21% of adults with mental illness, 26% of adults with serious mental illness (SMI), and 17% of adults with SUD.4 In comparison, Medicaid covered 14% of the general adult population.5 In total, approximately 9.1 million adults with Medicaid had a mental illness and over 3 million had an SUD in 2015. Nearly 1.8 million of these adults had both a mental illness and an SUD.6,7

Current Medicaid program financing guarantees federal financial support to states with no pre-set limit. The Better Care Reconciliation Act (BCRA), as proposed by the Senate, restructures federal Medicaid financing by changing it to a per capita cap or block grant, which would likely impact states’ ability to provide coverage for and access to behavioral health services for people who need them. This issue brief provides an overview of Medicaid’s role for people with behavioral health needs, including eligibility, benefits, service delivery, access to care, spending, and the potential implications of the BCRA.

The state could be forced to rebuild its public insurance program because the impact of the bill would affect one-third of its residents.

California risks losing $114.6 billion in federal funds within a decade for its Medicaid program under the Senate health care bill, a decline that would require the state to completely dismantle and rebuild the public insurance program that now serves one-third of the state, health leaders said Wednesday.

The reductions in the nation’s largest Medicaid program would start at $3 billion in 2020 and would escalate to $30.3 billion annually by 2027, according to an analysis released by the state departments of finance and health care services.

“It is not Medicaid reform,” Jennifer Kent, director of the state Department of Health Care Services, said in an interview. “It is not entitlement reform. It is simply a huge funding reduction in the Medicaid program. We are deeply concerned what that means for the long-term viability of the program as it stands today.”

Medicaid covers a staggering 13.5 million low-income Californians — children, people with disabilities, nursing home residents and others. About 3.8 million of them, many of whom are chronically ill, became eligible for coverage under the Affordable Care Act, informally known as Obamacare.

California would face the biggest losses of any state, according to a report issued Wednesday by the consulting firm Avalere Health. Federal funding would drop by 26 percent over 10 years, the report said. Many states, including Alabama, Georgia, Texas and Florida, would face a drop of less than 10 percent.

The Senate bill to repeal and replace the ACA would be a “massive and significant fiscal shift” of responsibility from the federal government to states, according to the analysis. It would force difficult decisions about who and what to cover and how much to pay doctors, hospitals and clinics, the report said.

In addition to expanding its Medicaid population early and vigorously under Obamacare, the state began covering undocumented immigrant children last year. California’s program, known as Medi-Cal, also provides dental care and other services that are optional under federal Medicaid rules.

The state’s Medicaid director, Mari Cantwell, said Republican proposals present a fundamental problem that can’t be solved by making cuts around the edges.

“Nothing is safe — no population, no services,” Cantwell said. “It is really disheartening and honestly horrifying to think about the world under this Senate bill and what it would mean.”

{kind=link}