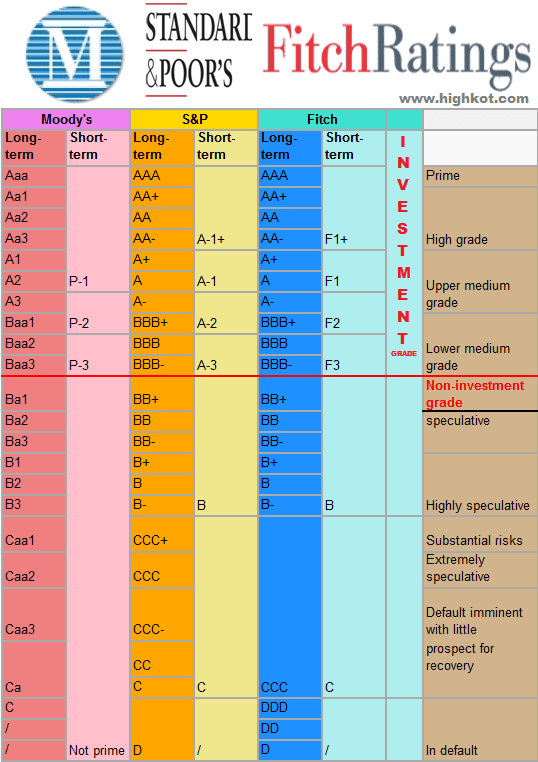

The following hospital and health system credit rating and outlook changes or affirmations occurred in the last week, beginning with the most recent:

1. Fitch affirms ‘AA-‘ rating for SSM Health

Fitch Ratings affirmed St. Louis-based SSM Health’s “AA-” issuer default rating and “AA-“/”F1+” rating where applicable on outstanding rated bonds.

2. Moody’s affirms Cook Children’s Medical Center’s ‘Aa2’ rating

Moody’s Investors Service affirmed its “Aa2” and “Aa2/VMIG 1” ratings for Fort Worth, Texas-based Cook Children’s Medical Center, affecting $356 million of outstanding revenue bonds.

3. Moody’s affirms ‘Baa2’ rating for Children’s Hospital Los Angeles

Moody’s Investors Service affirmed its “Baa2” rating for Children’s Hospital of Los Angeles, affecting $438 million of rated debt.

4. Moody’s affirms ‘A1’ rating for Lucile Packard Children’s Hospital

Moody’s Investors Service affirmed its “A1” revenue bond rating for Palo Alto, Calif.-based Lucile Packard Children’s Hospital.

5. Moody’s affirms ‘A2’ rating for Mary Greeley Medical Center

Moody’s Investors Service affirmed its “A2” rating for Ames, Ia.-based Mary Greeley Medical Center, affecting $64 million of outstanding revenue bonds.

6. Moody’s downgrades Marion County Health and Hospital to ‘Aa2’

Moody’s Investors Service downgraded Marion County (Ind.) Health and Hospital Corp.’s rating from “Aa1” to “Aa2.”

7. Moody’s assigns ‘A2’ rating to HonorHealth

Moody’s Investors Service assigned an “A2” rating to Scottsdale, Ariz.-based HonorHealth’s revenue bonds and affirmed its “A2” rating for the system’s outstanding parity debt.

8. Moody’s upgrades Gainesville Hospital District rating to ‘Ba1’

Moody’s Investors Service upgraded Gainesville (Texas) Hospital District issuer and general obligation limited tax debt ratings from “Ba2” to “Ba1.”

9. Moody’s downgrades Monroe County Health Care Authority rating to ‘Ba1’

Moody’s Investors Service downgraded Monroe County (Ala.) Health Care Authority’s rating from “A3” to “Ba1,” affecting $3.6 million in general obligation limited tax bonds.

10. Moody’s affirms ‘A2’ rating for MedStar Health

Moody’s Investors Service affirmed its “A2” rating on Columbia, Md.-based MedStar Health, affecting $1.4 billion of debt.

11. Moody’s assigns ‘A2’ rating to Mercy Health

Moody’s Investors Service assigned an “A2” rating to Cincinnati-based Mercy Health’s proposed taxable bond and also affirmed its “A2” and “A2/VMIG 1” ratings on the system’s outstanding bonds.

12. S&P revises Spartanburg Regional Health’s outlook to negative

S&P Global Ratings revised its outlook for Spartanburg (S.C.) Regional Healthcare System from stable to negative.

13. S&P affirms ‘A+’ rating for Rush University Medical Center

S&P Global Ratings affirmed its “A+” long-term rating for Chicago-based Rush University Medical Center’s outstanding revenue bonds.

14. S&P raises rating for Columbus Regional Healthcare to ‘A+’

S&P Global Ratings raised its rating for Whiteville, N.C.-based Columbus Regional Healthcare System from “BBB-” to “A+.”