https://gisthealthcare.com/weekly-gist/

When Presbyterian Health System struck a deal with Intel to manage care for the firm’s Albuquerque employees, followed by Providence Health & Service’s ACO-like contract to provide care to Boeing employees in Seattle, we became optimistic about the potential of direct contracting between health systems and large employers.

But five years after those landmark deals, we were still just talking about Boeing and Intel. Few other employers followed suit, instead preferring to control spend by shifting more of the cost of coverage onto their employees in the form of higher deductibles, larger co-pays, and greater co-insurance.

In 2018 the average family deductible in employer-sponsored insurance hit $3,000, and in most markets deductibles of $5,000 or higher are not uncommon. Our recent conversations with employers suggest that they are now questioning the utility of shifting more costs onto employees. As deductibles rise, employers see diminishing returns. In contrast to instituting the first $1,000 deductible, moving an already high deductible from $3,000 to $4,000 does little to change employee behavior. And employers are genuinely worried about the impact of rising cost sharing on their employee’s financial and physical health.

Given the historically strong labor market, employers have been reticent to change benefit design in any way that could be perceived as narrowing choice. But the reluctance to push cost sharing further creates an opening for providers and innovators that offer alternative solutions to encourage employees to choose a “high-performance network”—the new term of art for a narrow network.

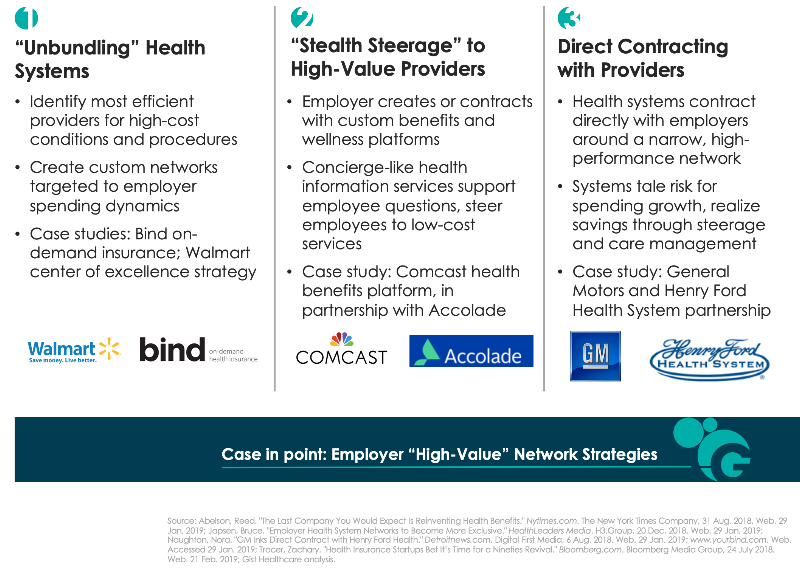

Across the past year we’ve seen a range of strategies to create high-performance networks, described in the graphic below. The pace of direct contracting between health systems and employers has quickened. But other solutions challenge the premise that a single health system provides the best solution for every high-cost condition or procedure. Start-up insurer Bind aims to create bespoke networks for high-cost procedures by identifying the best doctors and hospitals regardless of affiliation, essentially “unbundling” the health system. Others, like health benefits solution provider Accolade, create a concierge-like service to support employee decision-making—while preferentially steering them to lower-cost providers.

It remains to be seen which of these solutions will produce the greatest returns, and whether the gains can be sustained over time. However, we wonder whether companies will really have the fortitude to engage employees in conversations about narrower networks. Many will likely prefer to shift the task of narrowing networks onto employees themselves; we still believe that defined contribution health benefits will be the ultimate solution for employers to manage spend. It’s likely employers will require the cover of a recession to make this dramatic switch in benefit design. In the interim, there seems to be a window of opportunity for high-performance network assemblers to demonstrate that they can be an attractive and effective solution to rising costs.