As early as today, the House of Representatives is expected to vote on a government funding package (approved by the U.S. Senate last Friday) that includes long-sought reforms to pharmacy benefit managers (PBM) – pharmaceutical middlemen, the biggest of which are owned by just three health insurance conglomerates – that sit between patients and their prescriptions.

None of this happened over night. PBM reform – even in the health care advocacy world – has only recently become a bi-partisan, winning issue. PBMs were largely only known to pharmacists, other middlemen, health-policy wonks and the small but mighty circle of advocates who understood how they squeeze patients and independent pharmacies and funnel profits back to Big Insurance. PBMs began life as intermediaries meant to negotiate lower drug prices on behalf of consumers, but over time their role changed as they huge profit centers for insurers like UnitedHealth, Cigna and Aetna merged with or created their own PBMs – which now control more than 80% of the PBM business in the country.

This monopolistic-evolution captured the attention of policymakers and watchdogs after HEALTH CARE un-covered and reform advocates began to raise the alarm about PBM abuses and profiteering.

The need for PBM reform was one of the reasons I started the Lower Out-of-Pockets (LOOP NOW) Coalition, in 2021. Over the years, the LOOP NOW Coalition, along with its 100 partner organizations, have worked to educate lawmakers about how PBMs restrict access to life-saving medications and contribute to the U.S. medical debt crisis. The coalition has endorsed legislation to ban several PBM business practices, like spread pricing, and to force PBMs to be far more transparent, especially in their dealings with employers that offer health benefits to their workers. Our work also led to an invitation for me to testify at a meeting of the Department of Labor’s Advisory Council on Employee Welfare and Pension Benefit Plans (the ERISA Advisory Council) and to meet with the Federal Trade Commission regarding the vertical integration of big insurers and the need for PBM (and Medicare Advantage) reform.

Through the work of advocates on the ground, things began to shift. What was once a side quest among health-policy activists became something real in Washington because the issue is easy to understand: PBMs have become unneeded profit centers insurers erected between patients and the medicines their doctors say they need.

We came close to reining in the PBM industry in late 2024 when reforms were included in House Speaker Mike Johnson’s first spending package, but they were scrapped after Elon Musk complained about the size and scope of the legislation.. His Tweets prompted GOP leadership to strip out the PBM provisions, even though they had broad bipartisan support in Congress and were backed by many consumer advocates and independent pharmacists. But now, it seems like the PBM language in the current spending package is more locked in. Here’s what the bill will do:

Change how PBMs get paid in Medicare Part D by moving them away from percentage-based payments tied to high drug list prices and toward flat, transparent service fees — so PBMs no longer profit more when drug prices are higher.

Require CMS to define and enforce contract terms between PBMs and Medicare Part D plans, giving the agency real authority to police abusive or one-sided arrangements.

Increase transparency by allowing CMS to track how PBMs pay pharmacies and which pharmacies are included (or excluded) from PBM networks, so regulators can finally see payment patterns and network practices across the system.

Lock into law existing protections requiring plan sponsors and PBMs to contract with any pharmacy that agrees to their standard terms — as long as those terms are reasonable and relevant — instead of quietly steering business to preferred or affiliated pharmacies.

These are important reforms, although more are needed. We’ll keep you posted on PBM-related efforts not only on Capitol Hill but also at the Department of Labor and in the states.

And the questions I’d ask UnitedHealth Group’s CEO about his company’s ACA pledge.

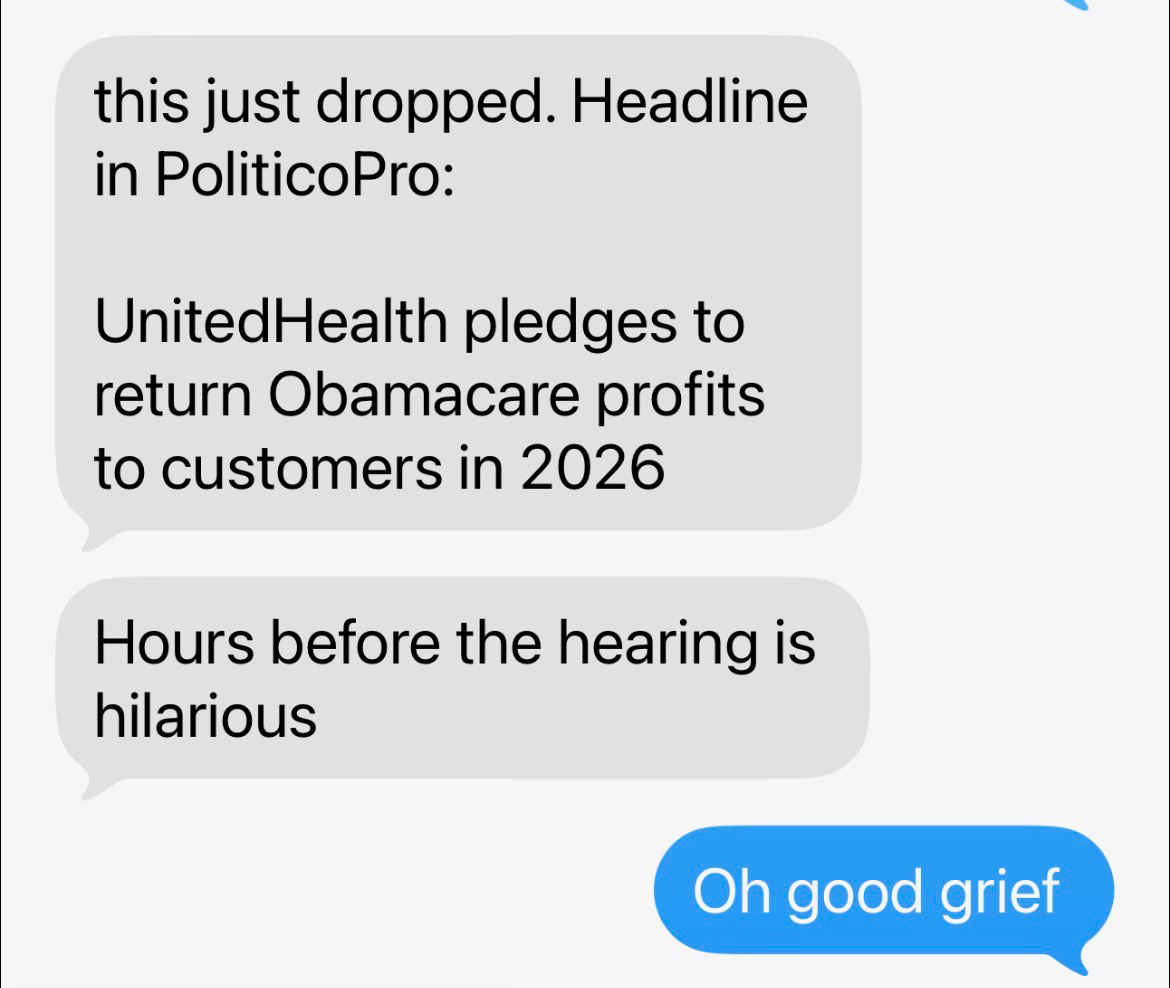

When I first saw the headline that UnitedHealth Group would “return Obamacare profits to customers in 2026,” my immediate reaction was: Oh good grief.

The timing is just too perfect.

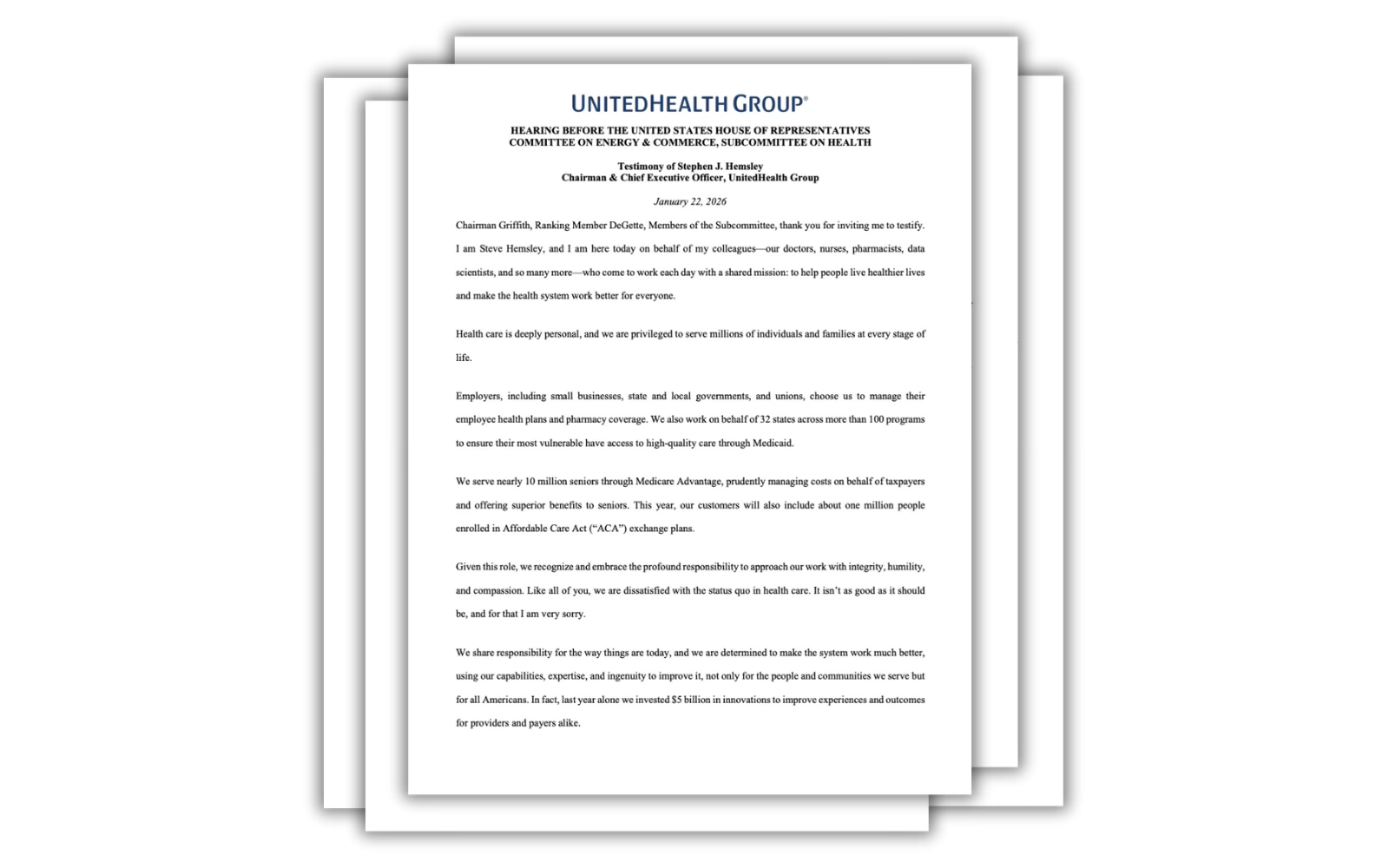

UnitedHealth’s pledge was tucked neatly into prepared testimony from CEO Stephen Hemsley, just hours before he (and four other Big Insurance CEOs) are to be hauled into Congress to testify before two House hearings on health care affordability.

“A text message conversation between my colleague, Joey Rettino, and me.

Today, the CEOs will be asked to explain why Americans are paying through the nose for coverage and still getting denied care, trapped in narrow networks and buried under medical debt. As of late, Republican lawmakers — and President Trump himself — have discovered religion on the issue, publicly fuming about high premiums and insurer abuses.

If you’re feeling a little misty-eyed about this sudden burst of corporate altruism, let me save you the trouble. This isn’t a moral awakening. It’s a PR maneuver and narrative control being implemented in real time.

Hail Mary

It’s the corporate version of a quarterback, down by four points, seconds left on the clock, closing his eyes and launching the ball fifty yards downfield, hoping something — anything — miraculous happens before the time runs out. UnitedHealth’s pledge is just a long, desperate PR pass into the end zone, praying lawmakers and reporters will focus on the gesture instead of the business model that allows them to gobble up those dollars in the first place.

It’s worth noting that UnitedHealthcare, while the largest insurer in the country with 50 million health plan enrollees, is actually a relatively small player in the ACA marketplace — about 1 million customers in 2026, compared with roughly 6 million for Centene, according to Politico. This is not UnitedHealth sacrificing a part of its core profit engine. (It doesn’t even disclose how much it makes on its ACA business, but I can assure you it’s a very small part of the more than $30 billion in annual profits it’s been making in recent years.) This is a carefully calibrated concession of a slice of this conglomerate’s business that won’t jeopardize its Wall Street standing, which is what Hemsley cares about most.

As I wrote yesterday, I spent years inside the insurance industry, helping executives shape their public image and get ahead of bad headlines. I know this playbook by heart. When scrutiny spikes, you roll out a “good guy” story. You announce a consumer-friendly initiative and you flood the zone with talking points. You give lawmakers anything they can point to as evidence of “progress,” so the temperature in the room drops just a few degrees. It’s all an optics game, and if I was in my old job I’d probably get a bonus for thinking of a stunt like this.

Reputational damage control

When Hemsley and his Big Insurance buddies sit before Congress, don’t be surprised if he pivots quickly from this show of supposed humility to pointing fingers at everyone else for driving up costs – including hospitals, doctors, drug companies and whoever else. How do I know this? Hemsley said as much in his prepared testimony. His fellow CEOs sang from the exact same hymnbook, written by the best flacks money can buy.

So no, I’m not impressed by UnitedHealth Group’s gesture. And neither should lawmakers.

If UnitedHealth and its peers were serious about affordability, they wouldn’t be waiting until the night before a congressional grilling to dangle a symbolic rebate. They would be opening their books and explaining their pricing algorithms. They’d come clean about how much of our premium dollar goes to care and how much goes to executive compensation, stock buybacks and acquisitions that tighten their grip on the health care system.

This isn’t a gift. It’s a distraction.

And like most Hail Marys, it doesn’t work if you’re already down a whole lot of points. I hope the lawmakers at today’s hearing remember the score.

In light of UnitedHealth Group’s latest move, see below for some questions that I would ask Hemsley if I were in Congress:

ACA plan and pledge specifics

How many people are enrolled in your ACA marketplace plans, and how much total profit are you committing to rebate to them?

What were your profits from ACA marketplace plans in recent years?

Will you commit to disclosing ACA-specific enrollment and profit figures when you announce 2025 earnings next Tuesday? And how many people dropped coverage after the enhanced ACA subsidies were not renewed?

By how much, on average, did you raise ACA premiums because Congress did not renew those subsidies?

Public money vs. private plans

Between 2020–2024, your filings show about $140 billion in operating profits and roughly $894 billion in revenue from Medicare and Medicaid versus $321 billion from commercial plans. Do you agree that about 74% of your revenue now comes from taxpayers and seniors?

Given that you have about twice as many people in commercial plans as in Medicare/Medicaid, do you agree the government is paying you far more per enrollee than private customers are?

Accountability going forward

Will you commit to disclosing ACA-specific enrollment and profit figures when you announce 2025 earnings next Tuesday?

Will you commit not to raise premiums or fees in your other lines of business to offset the ACA rebates?

Will you commit to providing the transparency and granularity needed for the public to verify that this rebate pledge is real and not a PR maneuver?

Rising health care costs are quietly reshaping family life and pushing homeownership, parenthood and financial stability further out of reach for millions of Americans.

The youngest of Millennials will hit 30 years old this year. For them and their older Millennial-counterparts, this is supposed to be the stage of life where people buy homes, have kids and settle into the textbook version of stability. But the reality for far too many Americans is something entirely different. It means delaying marriage, delaying children, delaying homeownership — and adopting pets to save them from college tuitions and pediatric specialists.

It’s not because an entire generation is collectively bucking the way “adulthood” used to be. It’s because the math doesn’t work anymore – and health insurance costs are a huge part of why.

Health care is eating the family budget

According to a new analysis from the Center for Economic and Policy Research (CEPR), the typical working family spent $3,960 on health care in 2024, including premiums and out-of-pocket costs. That’s the median… meaning half of families paid more.

Another striking finding from CEPR is that one in ten working families paid more than $14,800 in a single year on health care expenses. And for many low-income and rural households, health care consumed more than 10% of their entire income.

When the average Millennial earns about $47,034 a year, even the “average” health insurance spending now represents a meaningful slice of take-home pay before rent, student loans or the price of simply existing are even deducted. That threshold forces real tradeoffs: rent or deductible? Daycare or co-pays? Savings or prescriptions?

For young families trying to get started, that tradeoff answers itself.

Families with children spend significantly more on both health insurance and health care than those without. Working families with at least one child spent a median $5,150 per year.

Add that to childcare costs and it becomes clearer why many Millennials are putting off parenthood — or skipping it altogether. Hence the cat that doesn’t need braces or an albuterol prescription.

Health costs and home ownership

Diapers aside, medical bills also directly collide with the ability to own a home.

A recent study published in JAMA Network Open found that adults carrying medical debt were significantly more likely to experience housing instability such as trouble paying rent and mortgage, or evictions and foreclosures. As KFF researchers found, more than 100 million Americans have medical debt, and the vast majority of them have health insurance. It just isn’t adequate coverage because of ever-growing cost-sharing requirements.

That matters enormously for young families and would-be homeowners. Medical debt lowers credit scores, drains savings needed for down payments and makes lenders more hesitant. It’s hard to compete in today’s housing market when your emergency fund got wiped out by an MRI. Or your credit score took a hit because you found a lump.

This is not about lifestyle choices

In part because of these costs, the traditional milestones that once built financial security now often increase financial risk. Health insurance and health care costs are rising faster than inflation and faster than they did for previous generations. That’s why more and more insured families are delaying prescriptions and skipping care because of cost.

These uniquely American costs bleed into career moves, relationships, everything.

Millennials aren’t afraid of commitment. They’re afraid of math that doesn’t add up in large part because of a health care system that continues to be an ever-growing weight that is capable of wiping out savings and reshaping family decisions.

It’s easy to frame these trends as cultural shifts or personal preferences, but the data helps fill in the blanks. It’s not just Millannials facing these issues. Gen Xers and even Baby Boomers (some of whom still have a few years until they cross the Medicare and Social Security finish line) are dealing with budget-eating health care costs and medical debt, too.

When nearly half of adults say they couldn’t afford an unexpected $500 medical bill, it’s not surprising that people hesitate before taking on a 30-year mortgage or the lifelong responsibility of raising a child (or taking that trip to celebrate their retirement for that matter.)

For now, all that can be said is that Millennials’ cats are doing fine. They are benefiting heavily from the status quo. Maybe they have something to do with all of this.

Health insurers are feeling political heat as Republicans try to shape the affordability narrative and counter Democratic messaging on health care costs.

Why it matters:

President Trump and his allies have been increasingly assailing health plans over costs while seeking to deflect blame for blocking enhanced Affordable Care Act subsidies that help people afford premiums.

But the administration and Congress have less leverage than they have with drugmakers, and would have to address underlying drivers of health costs to really do something about premiums.

Driving the news:

House Republicans have called CEOs of five of the largest health insurance companies in back-to-back hearings on Thursday, where they will be pressed on costs of coverage.

Executives from UnitedHealth, CVS, Elevance, Cigna and Ascendiun will appear before the House Energy and Commerce and Ways and Means committees.

Energy and Commerce Chair Brett Guthrie (R-Ky.) said on Wednesday the companies cover over half of the insured lives in the U.S., “so everybody’s being affected by the high cost of health insurance.”

Between the lines:

It’s one thing to bash insurers, but quite another to match the talk with substantive health system changes.

“I think it’s interesting that they’re adopting some of the anti-insurer, populist rhetoric, but it needs to be backed up with actual policies that hold the health industry to account,” said Anthony Wright, executive director of consumer group Families USA.

He added that the hearing also should not be used to “distract” from the need to extend the ACA subsidies.

The other side:

Insurers agree that health care costs are too high, but say they’re the part of health care that’s working to bring costs down. Executives blame high premiums on the prices charged by hospitals and drug companies.

“Congress is doing its job,” Mike Tuffin, CEO of the insurer trade group AHIP, told Axios when asked about the pressure from Republicans.

But he added that “a thorough evaluation of the causes of higher premiums clearly demonstrates that it’s the underlying cost of medical care that is the reason that premiums continue to go up.”

What they’re saying:

Stephen Hemsley, CEO of UnitedHealth Group, will strike a note of contrition in his testimony, saying “like all of you, we are dissatisfied with the status quo in health care,” according to prepared remarks.

“The cost of health insurance is driven by the cost of health care,” he adds. “It is a symptom, not a cause.”

Still, Hemsley will say his company will rebate its profits this year from ACA coverage back to consumers, though he notes the company is a “relatively small participant” in that market. It’s unclear how much money will be rebated.

UnitedHealth became the object of widespread consumer anger just over a year ago, when the killing of CEO Brian Thompson unleashed a wave of social media-fueled rage over coverage denials and other business practices.

The big picture:

Insurers say they support a range of policies aimed at lowering health care costs by targeting hospitals and drug companies.

Those include “site-neutral” payment policies to address hospital outpatient billing, efforts to curb hospital consolidation and a crackdown on tactics drug companies use to delay cheaper generic competition.

But lawmakers have broached other changes that would directly strike health plans, like targeting what many experts say are overpayments in Medicare Advantage, or restricting pretreatment reviews that can lead to denials of care.

What’s next:

Trump earlier this month said he wanted a meeting with health insurance executives to press them on costs, but nothing is on the schedule and it’s unclear if that will happen.

Tuffin said he also expects future House hearings on health care costs with other parts of the health care industry besides insurers.

An Energy and Commerce Committee spokesperson confirmed there’s more to come but declined to provide details.

Yesterday, the Centers for Medicare and Medicaid Services released the latest data on national health expenditures (NHE). The headline number, 7.2 percent growth in 2024, is concerning but hardly a surprise. It follows 7.4 percent growth in 2023. This rate of NHE growth is not sustainable. It exceeds general inflation and growth in the gross domestic product (GDP), pushing the share if GDP devoted to health care spending to 18 percent in 2024; the share of GDP devoted to health care is projected to rise to 20.3 percent by 2033. In fact, these figures may be an underestimate of the fiscal burden of the health care system because spending on some things, such as employer administrative costs, are not captured.

Government policies that shield employers, their workers, those seeking individual coverage and participants in public insurance programs from the financial burden of the health care system can mitigate access and affordability problems from the perspective of those groups. But shifting the financing burden from employers and individuals to taxpayers broadly does not solve the affordability problem and will exacerbate already challenging federal and state fiscal situations. Long term fiscal stability of the system requires addressing the underlying growth in spending, not simply who pays.

What Is Not Driving Spending Growth

Given all the attention to prices and insurer profits, it is important to note that those factors are not the main drivers of spending growth—this time, it’s not the prices, stupid. There was virtually no excess medical inflation (medical inflation above general inflation) for 2023 or 2024. In fact, prices for retail drugs (net of rebates) rose at a rate below inflation. There will certainly be cases of rising prices driving spending, but on average, price growth is not the problem. This does not mean high-priced products and services are not an important component of spending growth, but instead it implies that their contribution to spending growth on average stems from their greater use, not rising prices.

Similarly, non-medical spending by private health insurers, which includes profits, grew at 4.4 percent rate, which is below overall spending growth. As the study notes, the increased medical spending was unanticipated by many insurers, which led to reductions in nonmedical insurance expenditures, the subcategory that includes underwriting gains or losses and thus where profits (or surpluses in the case of non-profit insurers) are recorded.

What Is Driving Spending Growth

The main driver of spending growth is greater volume and intensity of care. Volume refers to the number of encounters (admissions, visits, etc.) and intensity refers to the mix of services (high-cost versus low-cost admissions, shifts from an inpatient to an outpatient setting or from an office to a hospital outpatient department, or the use of expensive vs less-expensive drugs). Most decompositions of health spending growth follow the national health accounts framework, focusing on the sector getting paid (hospital, physicians, retail drugs). This may mask some underlying dynamics related to mix that are important.

Coding Intensity

Payment for health care services is based on service codes and the coding system is dependent on coding patterns. Spending may rise if the care delivered is coded differently, even if the underlying delivery of care is unchanged. There is some evidence from recent years of an uptick in coding for sepsis, greater use of higher acuity evaluation and management codes and use of new Evaluation & Management codes.

The drivers of greater coding intensity are unclear. Coding concerns are not new, but new technologies enabled by artificial intelligence (AI) and ambient scribe technology may be accelerating the trend. Some of the coding may be accurate. But if payment rates are based on earlier coding patterns, the payment rates may not be appropriate. As a result, greater coding intensity increases spending and may add very little clinical value.

AI-Enabled Medical Services

Apart from the role of AI technology in supporting administrative activities such as coding, AI offers great potential to improve the value and efficiency of care. New AI-enabled services, particularly diagnostic services, can better direct care, eliminating unnecessary, potentially harmful, and costly services.

It stands to reason that such tools will lower spending, but realization of that promise depends on how AI services are priced and how providers respond. If the new services are paid for by fee for service, price will likely exceed marginal cost and use may grow beyond what would be optimal. (Because of the potential for quality improvement, the optimal level of use would be above the money-saving level.) Moreover, such tools may require use of other, potentially expensive diagnostic services. For example, AI tools that help diagnose heart disease may require CT-scans that would otherwise not occur. Finally, the productivity gains from AI may free up resources to deliver services that would otherwise not be used.

We are very early in the adoption of AI-based services into the health care system, and it is unlikely that such services contributed significantly to the 2024 spending trend. But going forward, monitoring and evaluating the impact of these services will be a first order concern.

Changes In Health Care Infrastructure, Provider Consolidation And Shifts In Patient Flows

The infrastructure of health care is constantly changing. New outpatient facilities (independent and system-affiliated) are opening and providers are consolidating. Private equity firms have a growing presence in the market. These developments may have important consequences for spending. The shift to lower price settings may lower spending, but integration of physician practices with health systems may raise it because, in general, systems are paid more. Expanding infrastructure may also lead to greater utilization of care. Shifts in patients towards higher-priced providers within sectors (e.g., from low-priced to high-priced hospitals) may also increase spending.

Much of the related policy attention has been focused on antitrust issues and private equity, both of which are important, but the impact of the evolving infrastructure and changing patient flows extends well beyond these issues and remains poorly understood. The key issue is the balance between, on the one hand, efficiency-generating shifts toward lower-priced or better-quality care and, on the other hand, inefficient shifts towards high-priced settings, higher-priced providers within settings, or potentially inappropriate use of services.

Use Of Expensive Products

A non-trivial, though likely not the dominant, driver of spending growth is the increased use of expensive products. Prescription drugs, both in the retail setting and those covered by the medical benefit, garner the most attention. GLP-1s, used to treat diabetes and obesity, are the sentinel example. Despite declines in prices, increased utilization drove up spending on these medications. Yet other products matter as well, including skin substitutes, whose use has skyrocketed. As with all products and services, though more saliently for expensive ones, the core policy questions involve limiting use to situations where the clinical benefit is sufficient to justify the cost (net of any offsets elsewhere) and restraining prices without unduly hampering innovation. Policies such as greater bundling of similar medications, reforming the Average Sales Price+ 6 percent payment policy for drugs under Medicare Part B. and ensuring value is a cap on price should be explored. CMS has been very active in this area, launching several new financing models, including the GLOBE model, the GUARD model and the Generous model, on top of very active implementation of Inflation Reduction Act policies related to drug pricing. Monitoring the impact of these demonstrations on prices, spending, access and innovation will be important.

Looking Forward

Health care spending growth continued at an unsustainable pace in 2024. Early reports suggest spending growth in 2025 will remain elevated. Such growth challenges policy makers and private payers alike.

Reactions often involve efforts to shift the financial burden to other stakeholders. For example, reductions in the federal share of Medicaid spending (the federal Medicare assistance percentage, or FMPAP) shift funding from the federal to state governments; decreases in marketplace subsidies shift some of the burden to individuals, as do employer increases in employee premium contributions. In some cases, shifting who pays may induce reductions in aggregate spending, but such decreases—for example in the case of reductions from higher out-of-pocket cost sharing—may result in lower use of high value services. Our ultimate goal should be to reduce spending in the least deleterious manner possible.

In that spirit, several options include:

Focusing on strategies to reduce low-value care and inappropriate coding in fee-for-service settings. The WISeR model and private utilization management programs seek to accomplish this goal. The devil is always in the details.

Improving designs of alternative payment models (APM) that create incentives for providers to practice efficiently. Benchmark-setting rules and risk adjustment are likely the greatest leverage points, but it is also important to consider APM programs holistically; Maintaining too many constantly evolving APM experiments will likely be counter-productive.

Regulating areas where markets fail. This may include price regulation (including Medicare fee schedule improvement), standardization to support choice, and simplification of administratively burdensome regulations (including broad revision of programs to improve quality). System simplification should be a guiding principle

Improving market mechanisms to induce more efficient care-seeking behavior and pricing, which may involve antitrust enforcement, providing better consumer information, improving choice support tools, and creating benefit packages based on the principles of value-based insurance design. But market mechanisms have limits and past efforts have not proven very successful. Thus, pursuit of more efficient markets should not forestall necessary regulation.

The specifics of these strategies will be central to establishing a fiscally sustainable health care system. But the spending growth we have experienced, and will experience in the future, reflect system design choices. Our ability to support access to high-quality care at a cost that is affordable in aggregate will require redoubled efforts to reform both health care financing and delivery.

This week, 8000 healthcare operators and investors will head west to the 44th Annual JP Morgan Health Conference in San Francisco. Per JPM: “The (invitation-only) conference serves as a vital platform for networking, deal-making, and discussing the latest innovations in healthcare, attracting global industry leaders, emerging companies, and members of the investment community.” Daily media coverage will be provided by Modern Healthcare and STAT and most of the agenda will be at the St. Francis Hotel at Union Square.

General sessions about drug discovery, AI in healthcare obesity and more are scheduled, but that’s not why most make the trip.Representatives of the 500 presenting companies are there to engage with health investors in the tightly orchestrated speed-dating format JPM has fine-tuned through the years.

JPM circa 44 will be no different this year. It’s scheduled as company financials and market indicators for 2025 are coming in. Healthcare deal-flow was robust and bell-weather companies had a good year overall. The S&P, Dow and Nasdaq ended the year at all-time highs and investors appear poised to do more healthcare deals in 2026. Despite growing voter concern about affordability and their costs of living, there’s nothing on the immediate horizon that will dampen healthcare investor appetite for deals. That includes policy changes from the Trump administration that advantage healthcare companies that adapt to the administration’s playbook. It’s built on 3 fundamental assumptions:

The healthcare system is fundamentally flawed. Waste, fraud and abuse are deep-seeded in its SOP. It protects its own and resists accountability. The public wants change.

Fixing the health system requires policy changes that are attractive to the private companies that currently operate in the system. A federally-mandated regulatory framework (aka “the Affordable Care Act”) will cost more and be harmful. Companies, not Congress, are keys to system transformation.

Voters will support changes that make healthcare services more affordable and accessible. The means toward that end are less important.

What’s evolved from the administration’s first year in office is a mode of operating that’s predictable and uncomfortable to industries like healthcare:

It’s transactional, not ideologic. The administration believes its control of Congress, SCOTUS, the FTC and DOJ and legislatures in red states give it license to disrupt norms with impunity. Price transparency, limits on consolidation, mandated participation in ACOs, supply-chain disruption and AI-enabled workforce modernization are ripe for administrative action. A long-term vision for the system is not required to make needed short-term changes supported by its MAHA base.

It’s populism vs. corporatization. Healthcare’s proclivity for self-praise, addiction to “Best of…” recognition, celebrity CEOs and handsome executive compensation have postured it as “Big Business” in the eyes of most. Business practices associated with corporatization are fair game to the administration’s corrective agenda: hearings in the House Ways and Means and Energy and Commerce and Senate Health, Education, Labor and Pensions (HELP) committees will showcase the administration’s populist grievances. The administration will lavish advantages on private organizations that demonstrate support for its policies.

This week, the Senate will probably green-light a two-year extension of Tax Credits to temporarily avoid premium hikes. Barring a major escalation of tension abroad, attention will turn back to affordability where the K-economy is exacting its toll on lower-and-middle income households and widening despair among the young.

The health system’s role in making matters better or worse for consumers will be front and center alongside housing and costs of living. That context will be key to discussions between health investors and companies seeking their funds, though subordinate to term sheets.

In 2026, the Trump effect on dealmaking in healthcare will be significant.

Congressional negotiators are working to revive the health care deal that was dropped from a government spending package in late 2024 — but the odds of resurrecting enhanced Obamacare subsidies as part of the effort appear dire.

Why it matters:

Long-stalled bipartisan priorities that are in play include an overhaul of pharmacy benefit manager practices, as well as a measure that would place more controls on Medicare outpatient spending.

They’d likely be combined with a renewal of health programs due to expire Jan. 30, including certain Medicare telehealth flexibilities and funding for community health centers.

Driving the news:

Leadership and health committees in both parties have quietly swapped offers on a package over the past week while attention was primarily focused on the fight over expired Affordable Care Act tax credits.

Democrats included a three-year extension of the ACA subsidies in their latest offer knowing that GOP leadership is likely to reject it, sources said.

That would still leave intact most of the health care deal that was destined to ride on a government funding package before it was scuttled at the last minute by Elon Musk and then President-elect Donald Trump.

What we’re hearing:

Asked about the likelihood of a health package without the ACA subsidies, Senate Finance Committee Ranking Member Ron Wyden (D-Ore.) pointed to the overwhelming 26-0 vote in his committee for the PBM overhaul in 2023.

“I’m not going to negotiate with myself but the reality is I think a 26-0 vote in the Senate … it’s like unheard of,” Wyden told Axios, adding he is “feeling upbeat” about getting the PBM bill over the finish line.

Senate Finance Chairman Mike Crapo (R-Idaho) also told Axios he is “feeling optimistic” about the PBM bill, saying there is “broad support here and at the White House.”

That measure includes provisions like “delinking” the price of a drug from PBM compensation in Medicare Part D.

The prospective package would also include a measure that would require off-campus hospital outpatient departments to have a unique identifier number.

It’s a cost-saving measure designed to prevent outpatient departments from billing payers at higher amounts associated with full-service hospitals.

But it would stop short of a full-scale, more sweeping change known as site-neutral payments that would more closely align Medicare payments to hospital outpatient departments with freestanding physician offices.

The intrigue:

The outlook for renewing enhanced ACA subsidies, which help millions of Americans afford their premiums, is much bleaker.

While a separate bipartisan group of senators continues to meet in search of a compromise, a key negotiator, Sen. Bernie Moreno (R-Ohio), told reporters on Tuesday that a release of a proposal would be punted until after next week’s Senate recess.

Even if the group can release a proposal — which would include GOP-backed changes like eliminating $0 premium plans — there is deep skepticism in both parties that it can actually pass.

Many Republicans are opposed to any kind of ACA subsidy extension, saying it is wasteful spending that benefits insurance companies.

Top Democrats are pushing for a clean subsidy extension without GOP-backed changes and blasting Republicans for blocking it, in what could be a preview of midterm campaign messaging.

Between the lines:

There still are significant divisions over whether to include new limits on the ACA funding going to plans that cover abortions.

The bipartisan group has discussed a potential compromise that would increase audits and levy penalties on insurance companies that don’t comply with existing rules requiring them to segregate taxpayer money from paying for abortions.

The idea immediately drew fire from the anti-abortion group Susan B. Anthony Pro-Life America, and many Senate Republicans think it does not go far enough.

The bottom line:

There still could be an election-year health deal — just don’t expect it to address ACA subsidies.

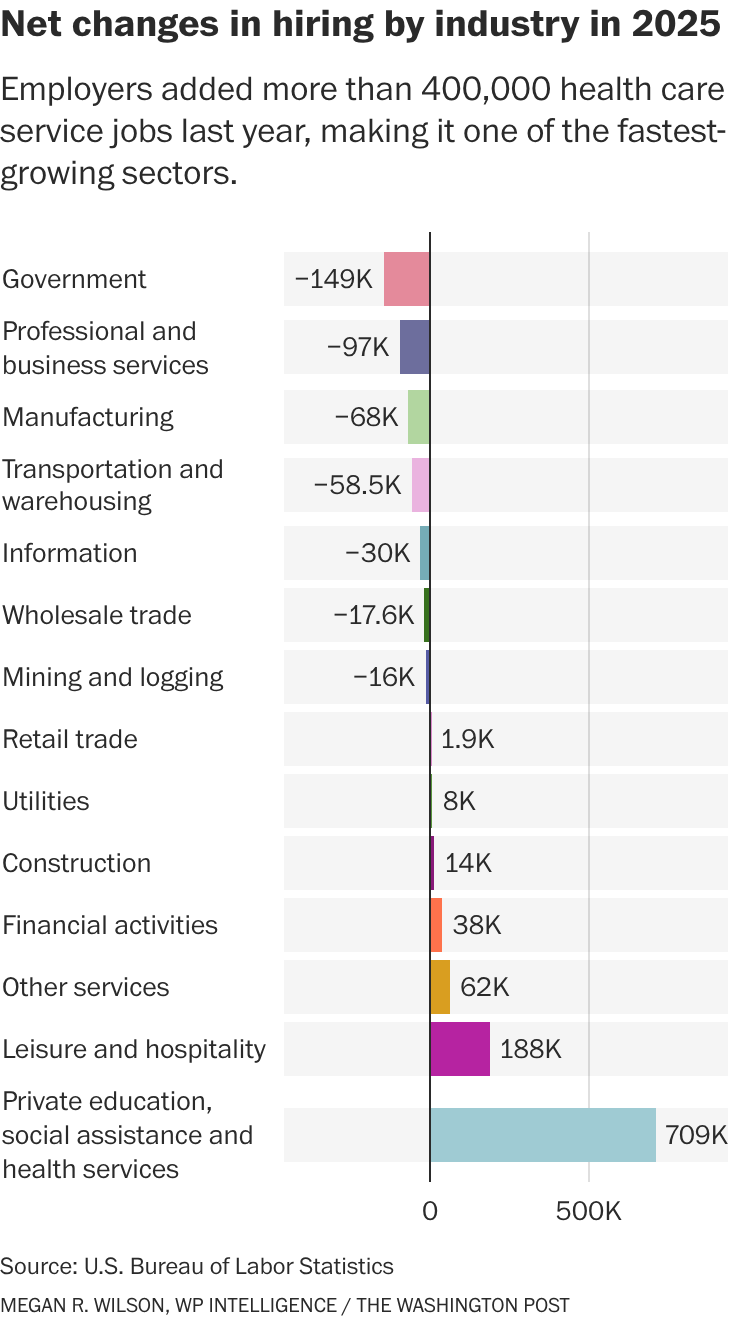

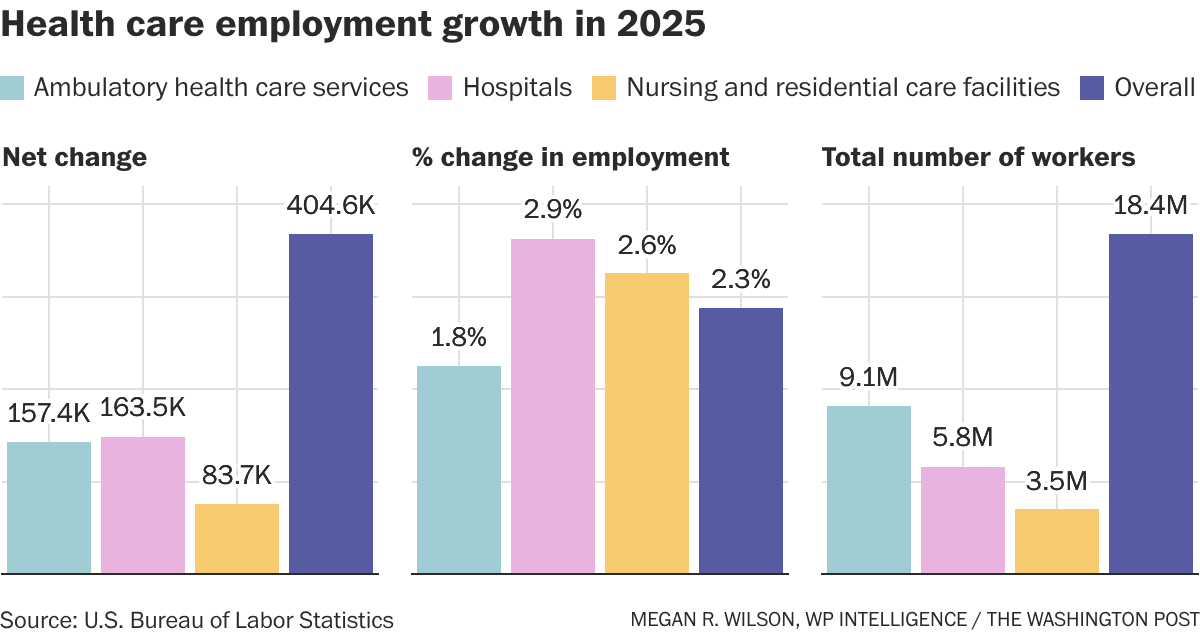

The health services industry was once again a bright spot in the economic data in today’s jobs report, which otherwise landed with a thud and capped off the weakest year for overall hiring since the pandemic.

The growth underscores how much health care employers are propping up the overall labor market — accounting for most of the gains, both in sheer numbers and percentage growth.

“The fundamental reason why health care employment continues to grow so strongly is that the aging population continues to boost demand for health care services,” said Jed Kolko, a senior fellow at the Peterson Institute for International Economics. “The population will continue to age, so that fundamental driver of demand continues.

”Behind the numbers: Although economists expect the health industry to continue expanding, they note that 2025 represented a slowdown from the previous year. Although many factors are at play, multiple analysts said the Trump administration’s restrictive immigration policies may be to blame. More on that later.

It’s not a huge surprise that people working in places such as hospitals, dentists’ offices and nursing homes represent the largest growth in hiring: Health care makes up about 18 percent of the overall U.S. economy — which means that $1 out of every $5 that Americans spend goes to health care. Advertisement

But this also highlights how health services hiring is keeping broader U.S. employment from sliding — even as other industries cool. Patients and providers alike are bracing for cost and workforce pressures in 2026.

Dive in: Although the number of people working in health services increased by more than 404,000 in 2025, it’s still a slowdown from the level of growth the sector saw the year before. In 2025, the health industry added about 34,000 workers per month, according to federal data, compared to an average monthly gain of 56,000 health jobs in 2024. This included people working in hospitals, residential care facilities or nursing homes, diagnostic labs, and for home health providers .

Here’s how it breaks down:

Hospitals represented the highest employment growth rate — 2.9 percent — in the health services industry, followed by jobs at nursing homes and residential care facilities, at 2.5 percent.

“We’re getting older and sicker. And, on top of that, we’re getting older and sicker in a way [where] we don’t have young people around to take care of the older, sicker people, right?” said Richard Frank, economic studies senior fellow at Brookings and director of its Center on Health Policy. Advertisement

“So what used to be long-term care delivered by family members when we had four or five kids per household, that looks very different today,” Frank said. “You’re going to have to pay people to do that work.

”While economists anticipate health care hiring to continue to grow — in part for that very reason — there two major policy shifts loom as a dark cloud over the industry and may impact the health services workforce.—

Immigration: Providers around the country have said that the Trump administration’s approach to immigration has hampered their ability to hire people. The administration has been cracking down on legal immigration as well as on people who have come to the U.S. illegally. Meanwhile, immigrants make up 28 percent of the long-term care workforce and 32 percent of home care workers, according to KFF.—

Medicaid cuts: The Republicans’ tax-and-domestic-policy law enacted last July is expected to slash nearly $1 trillion from the Medicaid program for low-income Americans. Researchers estimate that this will hammer the balance sheets of many hospitals, which are likely to see an influx in patients seeking care but are unable to pay for it. Hospitals and health clinics are already shutting down or laying off workers across the country. Although the Medicaid policy changes — which won’t fully kick in for years — aren’t the only reason for the closures, it shows how vulnerable many providers already are.

Other changes, including the proposed cuts to the National Institutes of Health, could trickle down to communities with research hospitals and ultimately impact the labor market, according to research from the Brookings Institution. New Medicare payment policies that aim to shift care away from expensive hospital services and toward primary care could also have an impact, although it likely won’t be large enough to show up in the data, I’m told.

However: Some states are working to offset some of the administration’s immigration policy changes or health program cuts, which could make it hard to evaluate their impact in the next round of employment data. “There are a lot of … crosswinds blowing in the aggregate that might cover up” the overall impact of these policies,” said Frank.

Other data: Employment in what the government calls “individual and family services” — listed under the “social assistance” category — increased by more than 289,000 people in 2025, representing a nearly 9 percent increase over 2024. These jobs include personal care aides, social workers and substance abuse counselors.

Health care costs hurt Californians every day. Millions can’t afford the care they need. More than half of all Californians skip or delay getting care because it costs too much.

How did we get here?

Health care is too expensive for people in large part because underlying costs in our health care system have grown unchecked for decades. Underlying costs are the “base ingredients” that determine how expensive health care is. Think of things like hospital operating costs, prescription drug prices, and doctor fees — when these costs go up year after year, they get passed on to patients through higher premiums, bigger deductibles, and larger medical bills.

The solution to the affordability crisis isn’t to slash health care spending across the board — that often makes things worse for patients. Instead, we need to be smart about cutting that 25% that doesn’t provide any value for patients.

Some of that rising cost has produced things we actually want, such as breakthrough treatments that save lives, cutting-edge medical equipment, or hospitals retrofitted to withstand earthquakes.

The solution to the affordability crisis isn’t to slash health care spending across the board — that often makes things worse for patients. Instead, we need to be smart about cutting that 25% that doesn’t provide any value for patients. Sometimes that might actually mean spending more money upfront, like making sure everyone can see a primary care doctor, to save money down the road by keeping people healthier.

This work is challenging, but it’s critical. Millions already can’t afford health care. If Californians’ health care costs keep rising the way they have been, even more families will be left behind.

Unchecked growth in the underlying costs of our health care system has driven total health care spending — from families, governments, employers and others combined — to more than triple since 2000, far outpacing inflation, economic growth, and wages.

Here are just a few key examples of the impact on California families:

Health insurance is increasingly becoming unaffordable for California families.

38% of all Californians report carrying medical debt. For Californians with low incomes, that rises to 52%.

Overview of the 3 Reasons

1. Administrative Waste

Health care requires some office work — doctors and hospitals have to schedule appointments, send bills, and keep records. But in the U.S., we spend way too much time and money on administrative tasks, which does nothing to make care better for patients.

Why Does This Happen?

Our health care system is complex. Different hospitals, doctors, and insurance companies often all use different computer systems for clinical data, billing, and administrative tasks. They can’t easily share information with each other. This means:

Staff in different parts of the system spend extra time entering the same information over and over;

Insurance companies and hospitals have to hire more people just to handle paperwork; and

Simple tasks become complicated and expensive.

How Much Money Gets Wasted?

Researchers in 2020 estimated that administrative waste cost the California health care system nearly $21 billion a year, making it the number one source of health care spending that doesn’t do anything to help patients or improve care.

How This Hurts Patients

Administrative waste doesn’t just cost money. It also hurts patient care:

Doctors spend less time with patients because they’re busy with forms.

Patients wait longer to get care.

Doctors have to call insurance companies over and over to find out what’s covered, and this can delay treatment when people need help.

Health care spending depends on two things: 1) how much care people get and 2) the prices that are charged for that care. In California, we have a big problem with pricing.

Same Care, Very Different Prices

The same medical procedure can cost wildly different amounts depending on where you go. For example, a knee replacement might cost $50,000 at one hospital and $70,000 at another. This happens even when both hospitals provide the same quality of care. In other words, the more expensive hospital is not necessarily better.

Lack of Competition Drives Prices Up and Hurts Patients

In many areas, there isn’t enough competition among health care organizations. For example, big hospital systems are buying up smaller hospitals. In some areas, there’s only one major hospital system left. Likewise, a few large insurance companies control most of the market. In some areas, one insurance company dominates.

When hospitals and insurance companies don’t have to compete:

Prices can go up without any improvement in care quality.

Patients have fewer choices about where to get care.

Families pay more for the same treatment.

Some areas become “take it or leave it” markets.

This creates unfair contracts where the biggest companies can demand high prices because patients have nowhere else to go.

When doctors find health problems early, they’re much easier and cheaper to treat. For example:

Regular cancer screenings can find problems before they become serious cancer.

Checking on people with heart problems can prevent expensive hospital stays.

Treating diabetes early prevents costly complications later.

Too often, though, people don’t get these early checks because there might not be a primary care doctor that can see them when they need it. By the time they see a doctor, their problems are much more serious and expensive to fix.

We Don’t Spend Enough on Prevention

Most prevention happens when you visit your primary care doctor for regular check-ups and basic care. But the U.S. has a big problem: We spend only 5 cents of every health care dollar on primary care, while other wealthy countries spend three times that amount.

California research shows that when provider organizations spend more money on primary care:

Patients get better quality care.

People are happier with their treatment.

Fewer people end up in the emergency room.

Fewer people need expensive hospital stays.

Overall health care costs go down.

We could save billions of dollars by helping people stay healthy instead of waiting until they get really sick. It’s like fixing a small leak in your roof instead of waiting until your whole ceiling falls down.

The good news is that we can fix these problems. California is working on several smart solutions right now.

The Office of Health Care Affordability

Created in In 2022, the Office of Health Care Affordability (OHCA) aims to break the cycle of the last decades and make sure that underlying costs in the health care system don’t continue to spiral out of control year over year.

Cost Growth Targets

In 2024, OHCA set an important new target: Total spending by health care’s major players — like hospitals, insurance companies, and large medical groups — can’t increase by more than 3% each year. That’s roughly how much a typical California family’s income grows every year. The target will be implemented in phases over the next several years.

This creates a powerful new incentive for these health care organizations to manage their underlying costs, rather than allowing them to grow unchecked and passing on increases every year to patients. Over time, this should help make health care more affordable for families.

If a health care organization exceeds its spending growth target without a good reason, OHCA will take increasingly serious enforcement actions, starting with guidance to the company on how to meet the target all the way to financial penalties. Penalty money will go into a fund and then back to California families to help them pay for their health care.

Making Sure Quality Stays High

Spending caps are intended to target things like administrative inefficiencies and monopolies, not quality of care.

To ensure health care organizations are focusing in the right places, OHCA is charged with ensuring:

Patients can still get the care they need.

Care quality stays just as good.

Hospitals and clinics have enough doctors and nurses.

OHCA is taking steps to address unfair pricing by reviewing health care mergers and acquisitions.

As we ring in the new year there is one thing – maybe the biggest thing – lingering from 2025 that can’t be dropped: The alarming state of health care.

Every aspect of the health care system feels like it’s working against its customers by prioritizing profits over care.

There are significant signs we could be at a breaking point.

More Americans than ever are opting to go without health insurance. A Gallup poll found 1 in 3 are considering running that risk, saying they can’t afford the costs.

For the first time in history, concern for rising health care costs is stride for stride with housing and food costs as American wages are struggling to keep pace. For many income levels they feel left permanently behind.

And not only are people paying record-high premiums, what they have to pay for prescription drugs at the pharmacy counter is breaking the bank as insurance companies have gobbled up pharmacy benefit managers to capture more and more of what we spend on health care.

The number of pharmacies serving the country’s sick has dwindled to the lowest levels in more than 50 years. Rite-Aid, which once operated more than 5,000 stores across the country, closed all of its locations and declared bankruptcy last year. Thousands of independent pharmacies have also closed, largely because of the stranglehold PBMs now have on the prescription drug supply chain. The closures have created hundreds of pharmacy deserts, leaving patients with a dwindling number of low-cost and convenient options.

Medicaid cuts mandated by Congress and the Trump administration last year are expected to cause more rural hospitals to close. More than 100 closed in the last decade and hundreds more are on the brink, according to a Boston University study. Health care is in such a bad spot it’s near the top of the 2026 Congressional agenda. Democrats want to restore the enhanced subsidies that made coverage affordable for the more than 20 million Americans who rely on the Affordable Care Act marketplace for their health insurance but most Congressional Republicans say the subsidies are a waste of money. Despite all that, there’s pessimism that politicians have the appetite for real change.

“We are frogs in a boiling pot,” said Eric Pachman, co-founder of the prescription drug watchdog 46 Brooklyn and data analyst on Wall Street. “Every year health care plans cost more but the coverage we pay for gets crappier.”

Pachman was recently at home when he got a call from a close relative whose son was in the middle of an allergic reaction. The family didn’t have health insurance because the premiums were beyond their means.

“He gave his son an Epi Pen and then drove to the hospital close by,” Pachman said. “He sat there for a while with his son in the parking lot to make sure he didn’t get worse but he didn’t go in.”

Americans are making those alarming decisions while health insurance companies continue to make big profits.

The country’s three largest health insurance companies and their in-house pharmacy benefit managers have rocketed toward the top of the Fortune 500 list of richest companies.

UnitedHealth has become America’s third-richest company behind Walmart and Amazon. In 2024, the company, which has about 30 million Americans enrolled in its health plans, brought in more than $400 billion in revenue, according to its financial filings.

CVS Health is just behind UnitedHealth at No. 5 on the country’s Fortune 500 list, bringing in nearly $373 billion in 2024. Cigna is 13th with $247 billion in revenue.

Health care alarms similar to sirens of 2008 housing collapse

The warning signs of this health care crisis bear a haunting resemblance to the 2008 housing market crash.

Cost vs. Income: In 2006, the average employer-sponsored family health care plan cost $11,381, representing 23% of the average salary. In 2026, the average plan is expected to exceed $27,000 against an average salary of $84,000 — a staggering 32% of income.

Shifting Risk: Just as risky mortgages were offloaded onto consumers, employers have shoved a larger portion of health care costs onto their workers.

Debt: Half of American adults now report they could not pay a $500 medical bill without going into debt.

Opacity: Much like the complex derivatives in mortgages in 2008, PBMs and insurers refuse to make their pricing public. This lack of transparency leaves patients fearing to open their mail after a hospital visit.

The sad joke in Washington D.C. right now is that everyone keeps talking about the price of health care but no one knows what the actual prices are.

In that Gallup poll, those surveyed gave the U.S. health care system a grade of D+.

“Our government continues to apply band-aids to a bloated pricing system rather than prescribing real, system-wide solutions,” said Antonio Ciaccia, co-founder of the pharmacy drug data site 46Brooklyn.com and former head of government affairs for the Ohio Pharmacist Association.

Lawmakers in more than a dozen states have tried to rein in insurers and their PBMs with lawsuits and regulations. Those lawsuits have led to more than $400 million in payouts by the big three health insurers and their subsidiaries.

Despite that the system keeps on going.

After years of battling insurers and their PBMs, Ohio’s Republican Attorney General, Dave Yost, came to the conclusion that any major reforms would have to come at the federal level.

“PBMs were originally intended to reduce the financial burden on Americans for prescription drugs, but the reality today is starkly different,” Yost said. “Instead of prioritizing the interests of patients, PBMs have shifted their focus to maximizing profits and marginalizing local pharmacies from the marketplace.”

Pachman also said if more people do opt out of insurance they will still go to hospitals for medical care.

“Hospitals cannot turn those patients away because they are legally required to treat them,” Pachman. “That means the cost burden will be shifted to those that do pay for insurance.”

While any type of significant reforms seem unlikely, many states are at least starting to ban medical debt from credit reports.

Fifteen states have the ban in place and Ohio, Alaska, North Carolina and Michigan are exploring similar statutes this year.

Chris Deacon, an attorney, author, health care reform advocate and former director for the New Jersey treasury department said the only incentive right now is for insurers to keep growing the $5.3 trillion spent on health care in the United States in 2024.

“There’s no incentive to control prices,” Deacon said. “And there’s no transparency whatsoever in any of this.”