http://www.tampabay.com/news/business/1-inch-1-inch-of-body-type-1-inch-1-inch-of/2335280

It has not been a market for the faint of heart.

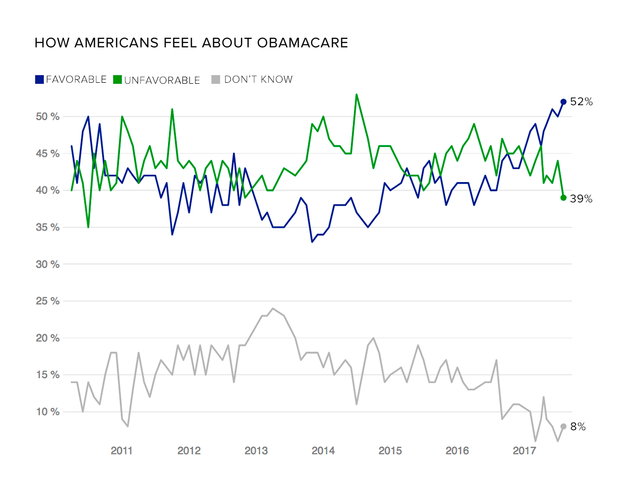

Supporters of the Affordable Care Act achieved a major victory this past week when, thanks to cajoling and arm-twisting by state regulators, the last “bare” county in the United States — in rural Ohio — found an insurer willing to sell health coverage through the law’s marketplace there. So despite earlier indications that insurance companies would stop offering coverage under the law in large parts of the country, insurers have now agreed to sell policies everywhere.

But a moment of truth still looms for the industry in the coming weeks under the law known as Obamacare. Companies must set their final plans and premiums by late September, even as the Trump administration continues to threaten to cut off billions of dollars in government subsidies promised by the legislation. Insurers are also awaiting Senate hearings set to start Sept. 6 for a hint of what steps, if any, lawmakers may take to stabilize the market.

With congressional Republicans’ yearslong quest to dismantle the Affordable Care Act dead for now, the fate of the landmark law depends in large part on the health of the insurance marketplaces and the ability of insurers to make a viable business out of selling coverage to individuals. When the law passed seven years ago, insurers saw a potential bonanza: tens of millions of brand-new paying customers, many backed by generous government subsidies and required by the new law to have health coverage. Now, about four years after the law’s marketplaces opened for business, most of the industry’s biggest players have pulled out.

Yet the continuing churn among insurers and the anxiety pervading the industry have obscured an encouraging fact: Many of the remaining companies have sharply narrowed their losses, analysts say, and some are even beginning to prosper.

“Outside of the noise,” the surviving companies “are seeing a path forward in this marketplace,” said Deep Banerjee, an analyst with Standard & Poor’s who has examined the financial results of more than two dozen Blue Cross insurers.

“It is still a new market,” he added, “and everyone is adjusting to it.”

The healthier business outlook has been achieved at a big cost to consumers. To stanch their losses, many companies raised their prices substantially for this year while narrowing their networks of providers to hold down costs.

In some cases, companies will seek even higher rates for 2018; the lone insurer left in Iowa is asking for a nearly 60 percent increase, on average.

Among the insurers now making money in the individual market and expanding is Centene, a for-profit company. Some of the Blue Cross insurers, including Health Care Service Corp., which operates plans in multiple states, including Texas and Illinois, and Independence Blue Cross, which has 300,000 customers in Pennsylvania and New Jersey, began to turn a profit in the market this year.

Oscar Health, a venture capital-backed insurance startup, lost roughly $200 million last year but, sensing a more promising future, plans to enter three more states and expand in California and Texas.

Centene made use of its experience, including setting up networks of hospitals and doctors that care for Medicaid patients, to sell coverage. The company now insures about 1.1 million people in the individual market.

“For 2018, we intend to grow this profitable segment of our business,” Michael Neidorff, the company’s chief executive, told investors last month.