Healthcare Triage News: The Trump Administration Has Many Options to Undermine Obamacare

While the Senate and the House haven’t been very effective in passing a repeal of Obamacare, the ACA’s provisions are still at risk. There’s a lot that Donald Trump’s administration can do (or not do) to undermine Obamacare’s provisions and marketplaces.

The financial burden of cancer treatment is a well-established concern.1,2 Owing to cost sharing, even insured patients face financial burden and are at risk for worsened quality of life3 and increased mortality.4 Underinsured patients (those spending more than 10% of their income on health care costs) are a growing population,5 and are at risk given the looming heath policy and coverage changes on the horizon. In this setting, little is known about what expectations patients have regarding those costs and how those cost expectations might impact decision making.

After approval from the institutional review board at Duke University Medical Center, we conducted a cross-sectional survey study of financial distress and cost expectations among patients with cancer presenting for anticancer therapy. We enrolled a convenience sample of adult patients at a comprehensive cancer center and at 3 affiliated rural oncology clinics. Patients provided written informed consent and were compensated with $10 for completing the survey. Trained interviewers surveyed patients in person.

We abstracted the electronic health record for cancer diagnosis, stage, type of treatment, and duration of treatment at the time of enrollment. Demographics including race and income were obtained from the patient. Patient out-of-pocket expenses were based on patient’s best estimation of recent, averaged monthly costs. We surveyed patients about whether their actual costs met their expectations, and about how much they were willing to pay out-of-pocket for cancer treatment, not including insurance premiums. Financial distress was measured using a validated measure. We measured median relative cost of care, defined as monthly out-of-pocket costs divided by income. Expected financial burden, willingness to pay, and subjective financial distress were dichotomized to assess the impact of unexpected costs and high financial distress. We used hypothesis testing to examine variables associated with burden and distress. Multivariable logistic regression included specific variables of interest along with select variables found to be statistically significant in bivariate testing. Statistical analyses were performed using SAS software (version 9.4, SAS institute).

Of 349 consecutive patients approached, 300 were eligible and agreed to participate, and 3 withdrew (86% response rate). Of the 300 patients, 157 (52%) were men. Patient characteristics, income, and costs are described in the Table along with unadjusted analyses. Forty-nine (16%) patients reported high or overwhelming financial distress (score >7).

The median relative cost of care was 11%. The relative cost of care for patients with high or overwhelming distress was 31% vs 10% for those with no, low, or average financial distress. One hundred eighteen (39%) participants endorsed higher than expected financial burden from cancer care. In unadjusted analysis, unexpected burden was associated with being younger, unmarried, nonwhite, unemployed/not retired, having lower household income, higher costs, colorectal/breast cancer diagnosis, lower quality of life and higher financial distress (Table). In adjusted analysis, experiencing higher than expected financial burden was associated with high or overwhelming financial distress (OR, 4.78; 95% CI, 2.02-11.32; P < .01) and with decreased willingness to pay for cancer care (OR, 0.48; 95% CI, 0.25-0.95; P = .03).

More than one-third of insured cancer patients receiving anticancer therapy faced out-of-pocket costs that were greater than expected, and patients with the most distress were underinsured, paying almost one-third of their income in health care-related costs. Patients at risk for unexpected costs had less household income and faced higher out-of-pocket costs.

Facing unexpected treatment costs was associated with lower willingness to pay for care, even when adjusting for financial burden. This suggests that unpreparedness for treatment-related expenses may impact future cost-conscious decision making. Interventions to improve patient health care cost literacy might impact decision making. Indeed, the Institute of Medicine has listed cancer cost-related health literacy as a high priority for future research, and this priority has been included in the Center for Medicare and Medicaid’s Oncology Care Model.6 Future studies should test interventions for cost mitigation through shared decision making.

Kaiser Health Tracking Poll – August 2017: The Politics of ACA Repeal and Replace Efforts

President Donald Trump renewed his call for Senate Republicans to take another crack at dismantling Obamacare, saying Thursday it’s a “disgrace” that they failed to pass a repeal bill.

“They lost by one vote,” Trump said from his Bedminster, New Jersey, golf course. “For a thing like that to happen is a disgrace.”

The president has hectored Senate Republicans for days over their collapsed health care effort, most recently singling out Majority Leader Mitch McConnell for criticism.

“I just want him to get repeal and replace done,” Trump told reporters, when asked about his multi-day string of tweets attacking the Kentucky Republican over health care. “It’s almost two years, and all I hear is repeal and replace. And I get there, and I said where’s the bill? I want to sign it.”

McConnell has suggested that the GOP should move on from health care after falling just short of the 50 votes he needed to pass a “skinny” repeal bill, and instead focus on tax reform. And earlier this week, McConnell said Trump has “excessive expectations” about how quickly Congress can pass legislation.

But Trump demanded that Republicans follow through on their agenda, suggesting further failure could cost McConnell his job atop the Senate GOP.

“If he doesn’t get repeal and replace done, and if he doesn’t get taxes done, meaning cuts and reform, and if he doesn’t get a very easy one to get done, infrastructure, he doesn’t get them done, then you can ask me that question,” Trump said.

https://www.thefiscaltimes.com/2017/08/10/Taxpayers-Will-Pay-Price-Uncertainty-Over-Obamacare-2018

The health insurance industry remains in the throes of a largely unnecessary crisis of confidence, according to an analysis released by the Kaiser Family Foundation on Thursday.

With the open enrollment period approaching for Obamacare insurance plans sold through state exchanges, Kaiser Foundation experts were able to analyze the proposals for 2018 submitted by insurance companies to 20 states and the District of Columbia — the only places where enough information is made public to allow an assessment of what health care costs would look like for an average policyholder under the insurers’ requested rate structures.

“Insurers attempting to price their plans and determine which states and counties they will service next year face a great deal of uncertainty,” the authors wrote. “They must soon sign contracts locking in their premiums for the entire year of 2018, yet Congress or the Administration could make significant changes in the coming months to the law – or its implementation – that could lead to significant losses if companies have not appropriately priced for these changes. Insurers vary in the assumptions they make regarding the individual mandate and cost-sharing subsidies and the degree to which they are factoring this uncertainty into their rate requests.”

What that means for consumers is a bit of a mixed bag. Almost all insurers are seeking rate increases, with some approaching a 50 percent jump. But the actual impact on consumers varies depending on where they buy their insurance and how much money they earn. One thing is for sure, though: The federal government, and therefore taxpayers, will be on the hook for larger subsidy payments.

Because the majority of Americans obtain health insurance through an employer-sponsored plan or from federal programs like Medicare and Medicaid, the impact of the premium increases of exchange-based policies will mean little to a large element of the population.

Of those who buy insurance on the exchanges, the overwhelming majority receive tax credits meant to keep their premium payments to a specific fraction of their annual income. The remaining 16 percent, depending on their income, receive either a smaller subsidy or no subsidy at all. It is these people who, if they live in some of the regions facing large premium increases, who will be hurt the most.

The Kaiser study gathered information from the largest city in each of the 20 states plus the District of Columbia. (Benchmark levels for tax credits are based on the second-cheapest Silver Level plan available in the largest city in a state.) They estimated the change in costs for a 40-year-old non-smoker earning $30,000 a year.

In only one state was the annual premium expected to fall in 2018: Rhode Island, which anticipates a 5 percent drop. Vermont’s premiums will remain static in 2018 if the data holds. The other 19 states can all expect increases, from a modest 3 percent in Michigan to a whopping 49 percent in Delaware.

The average increase in the data collected by Kaiser is 17 percent.

However, none of those costs would be passed on to the consumer making $30,000 a year. In fact, because of adjustments to the tax credit, he could expect to see monthly costs fall by 3 percent, to $201, next year, regardless of what premium levels do where he lives.

But somebody has to pay when premiums go up, and if it isn’t the consumer, it’s the Treasury and by extension, the taxpayer.

The change in premium payments required to keep that 40-year-old’s health insurance premium at $201 per month will increase very sharply in many states, depending greatly on how far from the premium cap a silver plan was in 2017.

In Washington State, according to Kaiser, the premium tax credit would increase 239 percent, from $31 per month to $105. In New Mexico, it would jump 183 percent, from $51 to $144. In Rhode Island it would fall 13 percent, while in Vermont it would rise a modest 2 percent. On average, though, the amount of premium payment picked up by the federal government will increase by about 63 percent in the states reviewed by Kaiser.

Perversely, as Kaiser points out, that fiscal wound is largely self-inflicted. While it is impossible to gauge just how much of this year’s rate increases are attributable to insurers being nervous about whether the federal government would slash support payments in the middle of the 2018 policy year, the answer is surely non-trivial, and the dollars are coming out of the pockets of taxpayers.

http://altarum.org/health-policy-blog/bipartisanship-is-back

In a much-discussed early-morning vote on July 28, the U.S. Senate voted decisively to move in a different direction on health care, sending a clear signal that future reform efforts will likely have to be bipartisan. Affirmation came on August 1, when Sens. Lamar Alexander of Tennessee and Patty Murray of Washington, the Senate Health Committee’s top ranking Republican and Democrat, announced bipartisan hearings will begin this fall on possible policy solutions for American consumers and insurers participating in state exchanges.

Yet, beyond the fights over “repeal and replace,” a larger issue is looming: Our health care system is not prepared to care for the age wave—which will come with a surge in need for ongoing, daily assistance. Congressional representatives from both sides of the aisle must work together to plan for burgeoning numbers of elders and individuals with disabilities, recognizing that there are diminishing numbers of family caregivers, and that the health services and delivery system as currently configured is poorly designed to meet long-term care needs.

Combining Forces for Better Policy

Fortunately there are stirrings of interest and activity: Rep. Ileana Ros-Lehitnen of Florida, the most senior Republican woman in the House of Representatives, joined Rep. Michelle Lujan-Grisham, a Democrat who served as Aging Secretary in New Mexico before her election to Congress, to introduce the Care Corps Demonstration Act. HR 3494 is a thoughtful measure that is designed to galvanize communities by helping them train and deploy volunteers of all ages, whose mission would be to help aging neighbors, friends, colleagues, and family members thrive in their own homes. Rep. Ros-Lehitnen’s predecessor from the 27th District of Florida was one of Congress’ best-known champions of older adults, Rep. Claude Pepper. Rep. Ros-Lehitnen announced on April 30 that she would not be running for re-election, while Rep. Lujan-Grisham has said she will run for Governor of New Mexico in 2018. Before Reps. Ros-Lehitnen and Lujan-Grisham leave Congress, they are trying to recruit supporters from across the aisle and around the country for the Act, so that it can either find its way into a “must pass” bill, or attract widespread acceptance as a standalone measure.

Here’s what the Care Corps Demonstration Act would do:

“It’s clear that seniors want to remain in their homes and they want control over their own health care,” Rep. Lujan-Grisham noted on introduction. “Most of all, they want to remain as independent as they can, for as long as they can. The same is true for individuals with disabilities. Care Corps will allow them to keep that independence. Unfortunately,” she added, “we’re facing high costs, along with a shortage of direct-care workers, which results in the lack of access to these important services, especially for middle class families. A national Care Corps will help build the workforce, while building intergenerational relationships that allow seniors and young people to learn from each other.”

Addressing the looming shortage of direct care workers is exactly what Rep. Bobby Scott of Virginia’s third congressional district is setting out to do. Next month, the Virginia lawmaker will introduce the Direct Creation, Advancement, and Retention of Employment (CARE) Opportunity Act (or Direct CARE Opportunity Act), which will propose to give the Department of Labor funds to establish advanced care training and mentoring programs and establish career ladders and better job opportunities, for direct care workers in up to 15 parts of the country. “Direct care workers are instrumental in supporting and assisting people across the country, particularly seniors and people with disabilities,” said Rep. Scott. “Moreover, if we invest in the direct care workforce, we invest in a rapidly growing and in-demand field. Growing the number of direct care workers is simply a win-win for investing in both the health of our communities and the jobs of tomorrow.”

PHI, a leading national organization representing and supporting direct care workers, is strongly backing Rep. Scott’s efforts: “Direct care workers are a critical part of delivering quality, person-centered long-term care, and we support this national effort to increase training, improve retention, and enhance the overall quality of jobs for this workforce,” noted Daniel R. Wilson, director of federal affairs.

Additionally, on July 27 Rep. Matt Cartwright of Pennsylvania’s 17th congressional district introduced the Improving Care for Vulnerable Older Citizens through Workforce Advancement Act. “This bill would improve both the quality of jobs for direct care workers nationwide, as well as the care they deliver, by helping to create expanded roles with sufficient training and compensation, and by helping them support people with increased complex conditions, such as Alzheimer’s and related dementias, congestive heart failure, diabetes, and other chronic conditions,”said PHI President Jodi M. Sturgeon.

Creating a System that Can Meet the Needs of Aging Americans

Together, these bills represent crucially needed investments in thinking through how to train more men and women who can serve on the frontlines of a multi-generational society in an era of mass longevity. With a majority of women now in the workforce and smaller and more scattered families quickly becoming the norm, the availability of traditional family caregivers—middle-aged women—is shrinking rapidly. This is giving rise to an urgent need to create a more flexible, community-focused workforce that is prepared to provide targeted supports in home settings on an as-needed basis to an increasing proportion of elders and individuals with disabilities.

Beyond the workforce, there is a need for more policy analysis and research to adapt and revamp existing social insurance programs that are still organized around delivering episodic medical services, and with financing protocols that are designed to pay providers and organizations without regard to the population’s need for ongoing services across a given geographic region or community. Making this shift—from provider-centric financing models to population health models—will also require tweaking payment rules to reward comprehensive, longitudinal services that include long-term care; adjusting performance metrics to emphasize population health and incorporate key social determinants of health factors; better information technology to foster communication across multiple providers and with individuals living at home and their family caregivers; and development of ways to accurately measure need, quality, and supply of services at a community level, with the help of local leaders and experts.

There are signs that lawmakers may rise to the challenge of helping to forge solutions to these issues. In the House, an ad hoc “problem solvers caucus” has surfaced with a set of initial ideas for fixing state exchanges, and the group of roughly 40 lawmakers may continue to hold discussions about other topics. There is solid bipartisan, bicameral work being done in the Assisting Caregivers Today (ACT) caucus on long-term care issues. Parallel caucuses focusing on Alzheimer’s and other types of cognitive impairment have already made excellent contributions to development of policy on “cure” and “care.” These and other budding efforts have the capability, if further developed, to begin contributing ideas necessary to address larger-scale systems challenges in ways that can inspire and complement the work of researchers, advocates, families, providers and stakeholders.

Between now and 2030, the U.S. will change profoundly as mass longevity becomes a central dynamic. To prepare, now is the time to invest and build for long-term care, not disinvest; to map existing assets and use current programs as platforms for improving and making more efficient; and to generally acknowledge gaps and focus work on addressing common goals in a long-lived society.

In summary, evidence-based, high-value health care reform is greatly aided by congressional bipartisanship, but more is needed. To create a value-based system requires the combined efforts of many. Now that bipartisanship is breaking out, let’s get to it!

https://www.axios.com/the-aca-stability-crisis-in-perspective-2470990374.html

The big questions about the stability of the Affordable Care Act marketplaces have focused on how fast premiums will rise, and how many plans will participate. But an equally important question, and the heart of the matter politically, is: How many people will be affected by the sharp premium increases?

The bottom line: The answer is about 6.7 million Americans who buy coverage in the non-group market in and out of the exchanges, and do not receive premium subsidies. That is a significant number of people, and an urgent policy problem requiring congressional attention and action by the administration, but it’s not a system-wide health insurance crisis. The non-group market has always been the most troubled part of the insurance system, and it was far worse before the ACA.

The breakdown:

Yes, 17.5 million is a sizeable number, and what happens to their health insurance coverage and costs is important. But, to put it in perspective:

According to our new analysis of proposed 2018 premium changes in the exchanges, double-digit increases for benchmark silver plans are quite common, though the range across major cities is large, from a 5% decrease in Providence, R.I. to a 49% increase in Wilmington, Del.

A big reason for these increases is the uncertainty in the market surrounding Trump administration policies, especially whether they will let the $7 billion in cost-sharing reduction (CSR) subsidies flow and whether the individual mandate will be enforced.

Who’s getting hit: 84% of the enrollees in the marketplaces – about 8.7 million people – receive premium subsidies under the ACA and are insulated from these premium hikes.

However, roughly 6.7 million people — the ones who buy ACA-compliant plans inside or outside the marketplace and aren’t subsidized — will feel the full brunt of premium increases. They’ll be hit if the uncertainty is not resolved and the rates do not come down before they are finalized.

In many cases, there is as much as a 20 percentage point swing or more in rates depending on whether the CSRs are paid.

The big picture: Dealing with this uncertainty is an urgent situation, particularly since it may result in some counties having no insurers at all, as well as coverage that is unaffordable for millions of Americans. But it is far from a crisis affecting most Americans and their health insurance.

The media needs to take great care to put this problem in perspective — otherwise they could unduly alarm the public and drive people to support the wrong policy solutions. Already, most Americans wrongly believe that premium increases in the relatively small non-group market affect them. So the headline should be: “Premiums Spike for SOME Americans.”

The danger in Congress is that discussion will spread too far beyond the immediate need to stabilize the non-group market, opening up all the old wounds surrounding the ACA and producing stalemate.

When Sen. Tom Carper was shopping for votes to block GOP health care bills, he didn’t just turn to his fellow senators. He turned to their governors.

A self-described “recovering governor,” himself, the Delaware Democrat carried out a communications blitz – calling, texting, emailing – and made contact with up to half of them. He skipped out on a Democratic campaign retreat to make a case at the National Governors Association summer meeting in Rhode Island.

His message: The legislation will hurt your states. Put your opposition in writing so the Senate can pause, work together to stabilize the insurance exchanges, and return to “regular order,” with hearings, bipartisan amendments — and input from governors, he said.

Delaware’s senators are bullish that debate over health care will turn to fixing the Affordable Care Act after the Senate early Friday morning defeated a proposal to repeal parts of the landmark law. 7/28/17 Damian Giletto/The News Journal

“He came up and spent a morning discussing the ins and outs, the details of health care changes,” Colorado Gov. John Hickenlooper, a Democrat, said on CBS’s “Face the Nation” Sunday.

Ohio Gov. John Kasich, a Republican, speaking on the same show, said, “Tom Carper from Delaware has been unbelievable in terms of his looking at trying to solve this problem.”

Carper believed that governors’ objections would be key to blocking the GOP effort to repeal and replace Obamacare, and it turned out they were. Even Sen. John McCain of Arizona, one of three Republicans who helped sink the GOP’s last-ditch effort, repeatedly highlighted his governor’s concerns.

Senate Minority Leader Charles Schumer of New York tapped Carper to lead outreach efforts to governors in early July when Carper complained that their voices weren’t being heard. In the health care drama, where there were many players, Democrats’ casting of Carper as the lead governors’ lobbyist made sense. He’s a former NGA chairman who loves the organization (and is prone to gushing about it).

“Tom Carper was really our point person with the governors, he kind of managed it,” said Sen. Tim Kaine, a former Democratic governor of Virginia. “He played a very important role in all of this. And the governors themselves, their voices were very important.”

Several days before the NGA summer meeting, Carper learned administration officials would discuss GOP health care proposals with the governors and was alarmed to discover that no one was scheduled to present the opposing view. He wangled an invitation to speak on a closed-door panel on July 15 alongside Seema Verma, administrator of the Centers for Medicare and Medicaid Services, and Secretary of Health and Human Services Tom Price.

“(Carper) was spreading this word that we should do this together, that people shouldn’t be hurt who are not in a position of being able to help themselves,” Kasich, an opponent of the GOP health care bills, said in an interview with USA TODAY. “And it was a message of slow down and let’s get this right. At no time did he ever say we should do nothing.After that, Carper kept contact information for every governor by his side, calling them during free moments between hearings and meetings. They discussed how the legislation would impact states’ Medicaid expansions, for example, or how a straight repeal of Obamacare would impact the states.

When he couldn’t reach Arizona Gov. Doug Ducey, a Republican, he said he talked several times to his Medicaid director and to his chief of staff. He said he spoke with Kasich “a dozen times or more.”

“One night he called me and it was like 10:30 at night,” Kasich said. “He was relentless in terms of what he did. And do I think he made a difference? I have no doubt that he did. Did he switch anybody? You don’t know. Did he have some people that would have not voted for this had McCain not voted ‘no,’ I just can’t tell you. But he deserves a lot of credit for being a really good public servant, keeping in mind the people that he serves.”

Carper said his outreach efforts helped him develop trust with governors “and just to let them know if they are interested in finding a path forward, they have a number of Democratic senators… who want to find common ground.”

Three days after Carper’s pitch at the NGA meeting, Kasich, Hickenlooper and nine other bipartisan governors who had been vocal about their concerns issued a statement opposing efforts to repeal the current system and replace it later. The statement, which Kasich said had been in the works for a while, called for governors to be included in the next steps.

“The best next step is for both parties to come together and do what we can all agree on: fix our unstable insurance markets,” they wrote.

They may be getting their wish, and so may Carper.

After the GOP’s three legislative failures, the Senate Health, Education, Labor and Pensions Committee announced it would begin hearings in September on ways to stabilize the individual health insurance market. The committee will hear from a wide range of stakeholders, including governors.

Moving forward, Carper said “the stage has been set” for better, more affordable health care coverage. Though he isn’t on the HELP Committee, he believes he can play a role in bipartisan discussions on health care.

“The key now is for the Senate to do its job,” Carper said.

https://www.axios.com/the-different-ways-your-health-care-costs-are-going-up-2471186113.html

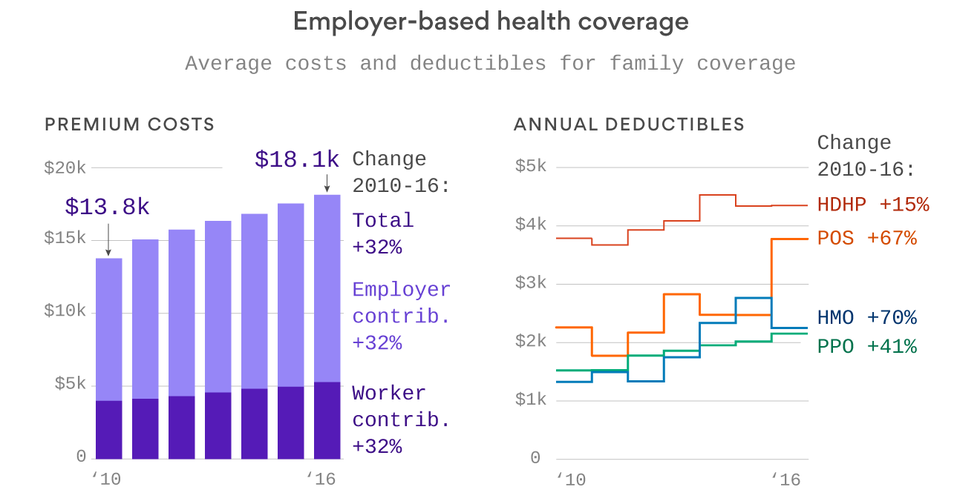

We’ve spent so much time talking about Affordable Care Act costs this year that it’s easy to forget what most people are actually paying for health care — the 156 million Americans who get their health coverage through the workplace. Turns out, most of us aren’t seeing sky-high premium increases. But it’s also worth remembering that deductibles matter too — because that’s what we pay out of pocket before insurance kicks in.

Take a look at these two graphics from Axios datavisuals genius Chris Canipe. The premium increases between 2010 and 2016 weren’t that bad — they’re single digits each year, and just add up over time. But you can see some big increases in deductibles, especially in point-of-service plans and HMOs.

Why it matters: That’s a big reason why people feel their health care costs going up, because it means they’re paying more out of pocket. And when prescription drug prices rise, they’re more likely to feel it directly.