Tag Archives: HMO

How Medicare Advantage steers the Silver Tsunami into coordinated, value-based care

CMS and other health insurers are using the program to deliver innovative and unique value to customers, both in terms of cost and quality.

Today’s Medicare Advantage plans are flourishing and the Silver Tsunami is among the reasons.

“Over the last four years, Medicare Advantage enrollment increased by more than 30 percent, while the number of people eligible for Medicare grew by about 18 percent,” said Steve Warner, vice president of Medicare Advantage Product for UnitedHealthcare Medicare and Retirement.

Other reasons for the growth: Innovative models from big insurers and upstarts alike that improve care for health plan members and drive revenue for payers as they look beyond fee-for-service.

IT STARTS WITH THE CONSUMER

Consumers are finding unique value in MA, both in terms of the quality of care and in the financial value.

Medicare Advantage, in fact, makes it easier for consumers to navigate the healthcare system and choose providers, in a way that traditional Medicare does not, said those interviewed.

“Actually it’s pretty hard to navigate the healthcare system on your own,” said Tip Kim, chief market development officer at Stanford Health Care. “Most Medicare Advantage plans have some sort of care navigation.”

Warner of UnitedHealth’s Warner added that Medicare Advantage also offers value and simplicity.

“It provides the convenience of combining all your coverage into one plan so you have just one card to carry in your wallet and one company to work with,” Warner said. “Most plans also offer prescription drug coverage and additional benefits and services not available through original Medicare, including dental, vision and fitness.”

REBRANDING FOR THE NEW ERA

MA plans did not emerge out of thin air. By another name, Medicare Advantage is managed care, a term that was the bane of healthcare during the height of HMOs in the 1980s.

“Medicare Advantage has rebranded ‘managed care’ to ‘care coordination,'” said consultant Paul Keckley of The Keckley Report. “Humana and a lot of these folks have done a pretty good job. Coordinating care is a core competence. Managed care seems to be working in this population.”

MA came along at the right time for CMS’s push to value-based care.

“I would suggest on the providers’ side, embracing Medicare Advantage is an opportunity to get off the fee-for-service mill,” said Jeff Carroll, senior vice president of Health Plans for Lumeris, which recently paired with Stanford Health Care on the Medicare Advantage plan, Stanford Health Care Advantage.

“Provider-sponsored Medicare Advantage plans are a way to put teeth into an accountable care organization,” Keckley added. “Medicare Advantage success is a silver tsunami among major tsunamis. Obviously it’s a profitable plan for seniors and profitable for underwriters. The winners in the process will get this to scale.”

MA is an innovative model that is not a government-run system, but a privately-run system essentially funded by the government.

PAYERS IN THE MA GAME

UnitedHealthcare has the largest MA market share of any one insurer. Twenty-five percent of Medicare Advantage enrollees are in a UnitedHealthcare MA plan, followed by 17 percent in Humana, 13 percent in a Blue Cross Blue Shield and 8 percent in Aetna, according to the Kaiser Family Foundation.

Numerous insurers, in fact, have gotten into the MA market, including Clover Health in San Francisco, a five-year-old startup which has Medicare Advantage as its only business.

Clover is a tech-oriented company that boasts machine learning models that can accurately predict and identify members at risk of hospitalization.

Because Clover focuses only on MA, it can do a better job at problem solving the needs of an older population, said Andrew Toy, president and CTO of Clover Health.

“The problems we face in Medicare Advantage are very different from a younger generation,” Toy said.

Forty percent of the older population is diabetic. Most seniors will be dealing with a chronic disease as they get older.

In other insurance, whether its individual or commercial, the lower cost of the healthier population offsets the cost of the sicker population. MA has no way to offset these costs. Plans can’t cherry-pick consumers or raise premiums for a percentage of the population.

What MA plans can do is design plans that fit the varying needs of the population. A plan can be designed for diabetics. For younger seniors or those not dealing with a chronic disease, a plan can be designed that includes a gym membership.

“All these plans are regulated,” Toy said. “We have the flexibility to move dollars around. We can offer a higher deductible plan, or a nutrition plan. The incentives for us in Medicare Advantage are different than the incentives in Medicare. CMS has explored giving us more leeway for benefits. Consumers have a choice while still having the guarantees of Medicare.”

Toy believes regular Medicare is more expensive because MA offers a more affordable plan based on what an individual needs.

“When you need it, we get more involved in that care,” Toy said, such as “weight control issues for diabetics.”

The drawbacks are narrower networks, though Toy said Clover offers an out-of-network cost sharing that is pretty much in line with being in-network.

UnitedHealthcare’s Medicare Advantage LPPO plans offer out-of-network access to any provider who accepts Medicare, Warner said.

UnitedHealthcare also offers a wide variety of low and even zero-dollar premium Medicare Advantage plans and annual out-of-pocket maximums, Warner said. By contrast, original Medicare generally covers about 80 percent of beneficiaries’ healthcare costs, leaving them to cover the remaining 20 percent out-of-pocket with no annual limit.

“From a consumer value proposition, it makes Medicare Advantage a better deal,” Kim said. “One is Part B, 20 percent of an unknown number. Knowing what the cost will be in a predictable manner is a preferable manner.”

Stanford Health Care launched a Medicare Advantage plan in 2013. Lumeris owned and operated its own plan, Essence Healthcare, for more than eight years. Stanford and Lumeris partnered on Stanford Health Care Advantage in northern California, using Lumeris technology to help manage value-based reimbursementand new approaches to care delivery through artificial intelligence-enabled diagnostic tools and other methods.

“We are not a traditional insurance company,” Kim said. “We’re thinking about benefits from a provider perspective. It’s a different outlook than an insurance company. By definition we’re local.”

MA MARKET STILL HAS ROOM TO GROW

While the Medicare Advantage market is competitive, it is also under-penetrated, Brian Thompson, CEO for UnitedHealthcare Medicare & Retirement, said during a 2018 earnings report.

Currently, about 33 percent of all Medicare beneficiaries are in an MA plan, he added, but UnitedHealth sees a path to over 50 percent market concentration in the next 5-10 years.

It’s a path not so subtly promoted by the Centers for Medicare and Medicaid Services.

As a way to encourage insurers to take risk and get in the market, around 2009, CMS gave MA insurers 114 percent of what it paid for fee-for-service Medicare. The agency began decreasing those payments so that by 2017, traditional Medicare and MA became about even.

MA insurers instead thrive on their ability to tailor benefits toward wellness, coordinate care and contain costs within the confines of capitated payments, the essence of value-based care.

They have received CMS support in recent rate notices that gives them the ability to offer supplemental benefits, such as being able to target care that addresses the social determinants of health. Starting in 2020, telehealth is being added to new flexibility for these plans.

WHAT THE FUTURE MAY HOLD FOR MA

Medicare Advantage plans have expanded and, in so doing, opened innovative new options for plans and their customers alike at the same time that the ranks of people eligible for Medicare continues to swell.

So where is it all going?

Medicare Advantage is changing the way healthcare is paid and delivered to the point that Keckley and Toy agreed the future may not lie in Medicare for All, but in Medicare Advantage for all.

“I think a reasonable place to end, is in some combination where the government is involved in price control, combined with the flexibility of Medicare Advantage,” Toy said. “That’s really powerful.”

Health Insurance Startups Bet It’s Time for a Nineties Revival

As high health costs squeeze employers, managed care is making a comeback.

Nineties throwbacks have swept through music, television and fashion. Some startups want to bring a bit of that vintage feel to your workplace health insurance plan.

Health maintenance organizations drove down costs but were painted as villains in that decade for limiting patient choice, rationing care and leaving consumers to grapple with high bills for out-of-network services. But some features of the plans are regaining currency. Companies reviving the model say that new technology and better customer service will help avoid the mistakes of the past.

Rising health-care costs and dissatisfaction with high-deductible plans that ask workers to shoulder more of the burden are pushing employers to consider new ways of controlling spending—and to rethink the trade-offs they’re willing to make to save money.

Medical costs have increased roughly 6 percent a year for the past half-decade, according to PwC’s Health Research Institute, outpacing U.S. economic growth and eroding workers’ wage gains. Some employers, such as Amazon.com Inc., Berkshire Hathaway Inc. and JPMorgan Chase & Co.—wary of asking workers to pay even more—are trying to rebuild their health programs.

Barry Rose, superintendent of the Cumberland School District in northern Wisconsin, went shopping recently for a new health plan for the district’s 290 employees and family members after its annual coverage costs threatened to top $2 million.

“How do we provide quality, affordable and usable health care for employees,” said Rose. “I can’t keep taking money out of their paychecks to spend on health insurance.”

The company he picked, called Bind, is part of a new generation of health plans putting a tech-savvy spin on cost controls pioneered by HMOs.

Bind, started in 2016, ditches deductibles in favor of fixed copays that consumers can look up on a mobile app or online before heading to the doctor. Another upstart, Centivo, founded in 2017, uses rewards and penalties to nudge workers to get most of their care and referrals for specialists from primary-care doctors.

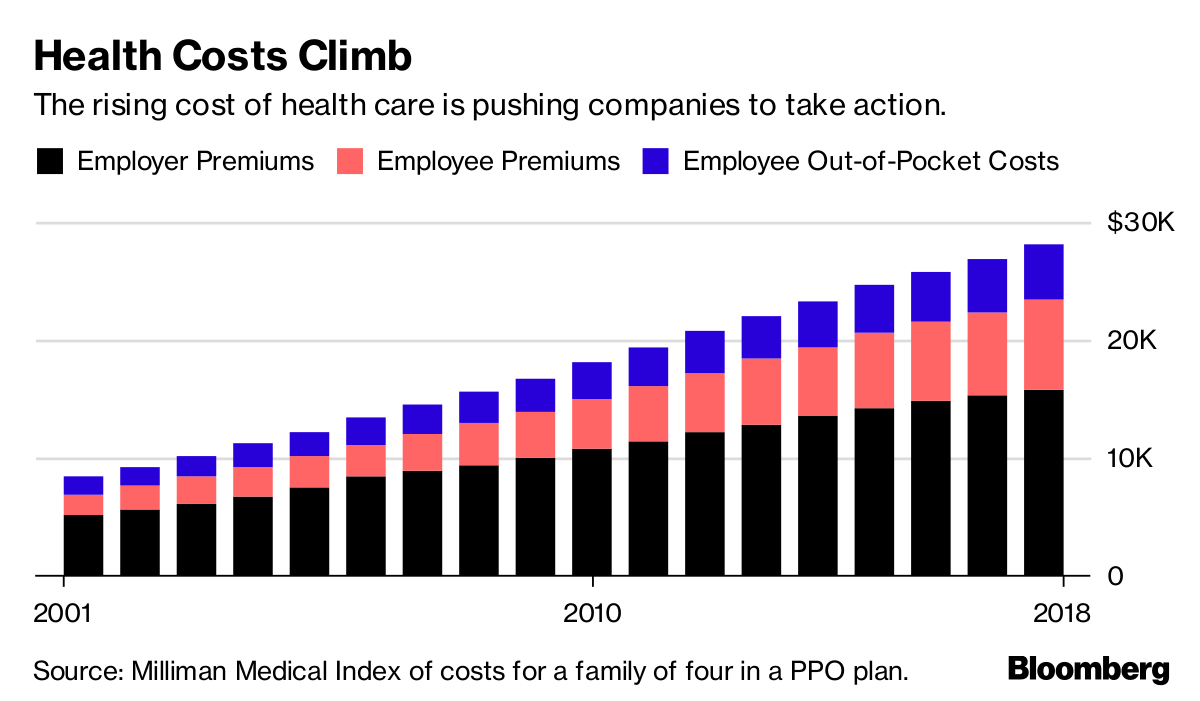

Health Costs Climb

The rising cost of health care is pushing companies to take action.

For many years, employers offered health plans that paid the bills when workers went to see just about any doctor, imposing few limits on care. The companies themselves usually paid much or all of the premiums.

Confronted with rising costs in the 1990s, many employers switched to HMOs or other forms of what became known as managed care. The switch worked, helping hold health costs down for much of the decade.

Soon, however, consumer and physician opposition grew amid horror stories of mothers pushed out of the hospital soon after childbirth, or patients denied cancer treatments. States and the federal government passed laws to protect consumers, and, in 1997, then-President Bill Clinton appointed a panel to create a health consumers’ Bill of Rights.

“The causes of the backlash are much deeper than the specific irritations or grievances we hear about,” Alain Enthoven, the Stanford health economist who helped pioneer the idea of managed care, said in a 1999 lecture. “They are first, that the large insured employed American middle class rejects the very idea of limits on health care because they don’t see themselves as paying for the cost.”

Workers would soon bear the cost, though. By the end of the decade, employers had moved away from these limited health plans. In their wake, costs skyrocketed, giving rise to a new cost-containment tool: high deductibles.

Centivo co-founder Ashok Subramanian spent the past decade trying to figure out how to offer better health insurance at work. His first startup, Liazon, helped workers pick from a big menu of coverage options. He sold it for some $215 million to Towers Watson in 2013, but he said it didn’t fix the bigger problem: Workers had lots of options, but none of them were very good.

“Yes, we were increasing choice, yes we were enabling personalization, but the choices themselves were not that good,” Subramanian said in an interview. “The choices themselves were predicated on a system in which the fundamental incentives in health care are broken.”

Tony Miller, Bind’s founder, helped give rise to health plans with high out-of-pocket costs. He sold a company called Definity Health that combined health plans with savings accounts to UnitedHealth Group Inc. for $300 million in 2004. He now says high-deductible plans failed to deliver on their promises.

“There’s a fever pitch of frustration at employers,” he said. “They’re tired of using the same levers that they’ve been using for the past 20 years.”

UnitedHealth, the biggest U.S. health insurer, helped create Bind with Miller’s venture capital firm and is an investor in the company, which has raised a total of $82 million. Bind is also using UnitedHealth’s network of doctors and hospitals as well as some of its technology.

Centivo has raised $34 million from investors including Bain Capital Ventures.

Centivo and Bind both promise to reduce costs for patients and employers while making it easier to find doctors and check coverage. They say they’ll reduce costs by making sure patients get the care they need, keeping them healthy and avoiding emergencies or unnecessary treatment.

Covered?

The proportion of Americans under 65 in health plans with high deductibles continues to increase.

In most cases, workers who follow the rules of Centivo’s plans won’t face a deductible. When signing up, employees pick a primary-care doctor, who’s responsible for managing their care and making decisions on whether they need to see a specialist. Care provided or directed by that primary physician is free, as is some treatment for chronic diseases such as diabetes, depending on how employers choose to set up the coverage.

The goal is to ensure workers get the care they need, while avoiding low-value treatments. Those who go to an emergency department in cases that aren’t true emergencies, for example, could face high costs.

“The big question is: Is the market ready for it?” said Mike Turpin, who advises employers on their health benefits as an executive vice president at USI Insurance Services. “The American consumer just has it built into their head that access equals quality.”

Bind bundles its coverage so consumers don’t get billed for lots of charges for services that are part of the same treatment. In Rose’s district, the copay for an emergency room visit is $250, while the cost of a hospital stay is capped at $1,000. Office visits are $35; preventive care is free.

Bind also offers what it calls on-demand insurance. Coverage for planned procedures such as knee surgery, tonsil removal or bariatric surgery must be purchased before the operation. That gives Bind a chance to push customers toward a menu of lower-cost alternatives or cheaper providers.

A patient who looks up knee arthroscopy, for instance, would also be offered physical therapy. The patient’s cost for the surgery ranges from $800 at an outpatient center to more than $6,000, in an example used by Miller. Surgeries in hospitals are typically more costly. Bind also charges more for providers who tend to be less efficient or have worse outcomes.

The ability to view costs upfront is part of what appealed to Rose, the Wisconsin superintendent. “Each of my employees knows exactly what they’re paying for, and they have choice in it,” he said.

Rose said the switch to Bind will save his district several hundred thousand dollars, depending on how much health care his workers need over the next year.

Lawton R. Burns, director of the Wharton Center for Health Management and Economics at the University of Pennsylvania, recently authored a paper with his colleague Mark Pauly arguing that it’s probably impossible to simultaneously improve quality, lower costs and achieve better health outcomes. The ideas now being pushed forward, he writes, are similar to ideas tested in the 1990s.

“It’s deja vu all over again,” he said. “It’s not clear to me, this is just me talking, that people have learned the lessons of the 1990s.”

Cartoon – Modern Drug Coverage

Cartoon – Good Luck Cards

Paying Hospitals To Keep People Out Of Hospitals? It Works In Maryland.

https://khn.org/news/paying-hospitals-to-keep-people-out-of-hospitals-it-works-in-maryland/

Saturdays at Mercy Medical Center used to be perversely lucrative. The dialysis clinic across the street was closed on weekends.

That meant the downtown Baltimore hospital would see patients with failing kidneys who should have gone to the dialysis center. So Mercy admitted them, collecting as much as $30,000 for treatment that typically costs hundreds of dollars.

“That’s how the system worked,” said Mercy CEO Thomas Mullen. Instead of finding less expensive alternatives, he said, “our financial people were saying, ‘We need to admit them.’”

Maryland’s ambitious hospital-payment overhaul, put in place in 2014, has changed such crass calculations, which are still business as usual for most of American health care. A modification of a long-standing state regulation that would be hard to replicate elsewhere, the system is nevertheless attracting national attention, analysts say.

As soon as Mercy started being penalized rather than rewarded for such avoidable admissions, it persuaded the dialysis facility to open on weekends, saving government insurance programs and other payers close to $1 million annually.

In the four years since Maryland implemented a statewide system of pushing hospitals to lower admissions, such savings are adding up to hundreds of millions of dollars for the taxpayers, employers and others who ultimately pay the bills, a new report shows.

Maryland essentially pays hospitals to keep people out of the hospital. Analysts often describe the change as the most far-reaching attempt in the nation to control the medical costs driving up insurance premiums and government spending.

Like a giant health maintenance organization, the state caps hospitals’ revenue each year, letting them keep the difference if they reduce inpatient and outpatient treatment while maintaining care quality. Such “global budgets,” which have attracted rare, bipartisan support during a time of rancor over health care, are supposed to make hospitals work harder to keep patients healthy outside their walls.

Maryland’s system, which evolved from a decades-old effort to oversee hospitals as if they were public utilities, regulates all hospital payments by every private and government insurer. That makes it radically different from piecemeal attempts to lasso health spending, such as creating accountable care organizations, which seek savings among smaller groups of patients.

From the program’s launch in 2014 through 2016, per capita hospital spending by all insurers grew by less than 2 percent a year in Maryland. That’s below the economic growth rate, according to new results from the state’s hospital regulator and the federal Department of Health and Human Services.

Keeping hospital spending below economic growth — defined four years ago as 3.58 percent annually — is a key goal for the program and something that rarely happened.

Counting The Savings

The state plan saved the Medicare program for seniors and the disabled about half a billion dollars over three years and achieved “substantial reductions in hospitalization and especially improvements in quality of care,” said a Medicare spokesman.

In the three years measured so far, he added, “the state has already exceeded the required performance for the full five years of the model.”

As high costs for hospital care have been growing more slowly nationwide, Maryland hospital costs over that period rose even less.

“It looks like it has very strong results,” said John McDonough, a Harvard health policy professor who helped craft the federal Affordable Care Act.

What Maryland is doing, he said, “is pretty bold and it’s pretty thoughtfully done and has generated a huge amount of interest around the country.”

Comprehensive results through 2016 are the most recent available from Maryland and HHS, although savings continued last year, Maryland officials said. Independent researchers found mixed results for savings in the earlier years of Maryland’s system.

Maryland’s global budgets saved Medicare $293 million — 1.8 percent of total Medicare spending — in 2014 and 2015, research firm RTI International reported in August.

A separate paper from a team led by Eric Roberts at the University of Pittsburgh found that Maryland’s program in those years couldn’t be clearly credited for reducing hospital use.

The system’s advocates say several years of results are needed to show it’s working.

“These are not fake savings,” said Joseph Antos, an economist at the conservative-leaning American Enterprise Institute who sits on Maryland’s hospital-payment commission. “It didn’t happen instantaneously. It’s taken this number of years to achieve the kinds of savings that you see” for 2016 and beyond.

Even boosters such as Joshua Sharfstein, the former Maryland health secretary who got approval for global budgets from the Obama administration, say the system is far from perfect or finalized.

“There is a range of responses. Some hospitals have been able to do more than others,” said Sharfstein, now an associate dean at the Johns Hopkins Bloomberg School of Public Health in Baltimore. “Change in health care is notoriously slow.”

Hospitals have lagged in delivering primary, preventive care to people with chronic conditions such as asthma, diabetes and heart failure, especially in low-income neighborhoods.

Maryland’s system does little to control soaring costs of drugs or nursing home care, doctors’ office treatments and other care not connected to hospitals, although policymakers are working on proposals to do both.

Even so, “what Maryland has done is just so far ahead of many of these other models” to try to control costs, said Dan D’Orazio, a management consultant who has worked with hospitals across the country. One Maryland hospital CEO told him: “This has fundamentally changed how we wake up and do business every day,” D’Orazio said.

Seeing A Difference

At Mercy, described by policymakers as more aggressive than many hospitals in watching costs, about a third of the patients now leave the hospital with medications in hand, said Dr. Wilma Rowe, the hospital’s chief medical officer. That bypasses the tendency for patients to skip a follow-up pharmacy visit and risk landing back in the emergency room.

A statewide data network notifies Mercy and other hospitals when one of their patients ends up in an emergency room somewhere else. That helps coordinate care.

Greater Baltimore Medical Center, north of the city, has hired dozens of primary care doctors to track around 1,000 people with diabetes — staying in touch, advising on diets and keeping them on insulin so they avoid the hospital.

Often clinicians visit elderly patients’ homes to prevent what might turn into an ambulance call and admission, said the hospital’s CEO, Dr. John Chessare.

Before global budgets, “I’d look at the waiting room in the [emergency department], and if it wasn’t full I’d get scared,” he said.

Now he worries it might be full of people who could be better treated elsewhere — including Gilchrist, a GBMC affiliate delivering hospice care for those at the end of life.

These days, he said, “we consider it a defect if someone with chronic disease dies in the hospital.”

Cartoon – HMO Cost Cutting Measure

The different ways your health care costs are going up

https://www.axios.com/the-different-ways-your-health-care-costs-are-going-up-2471186113.html

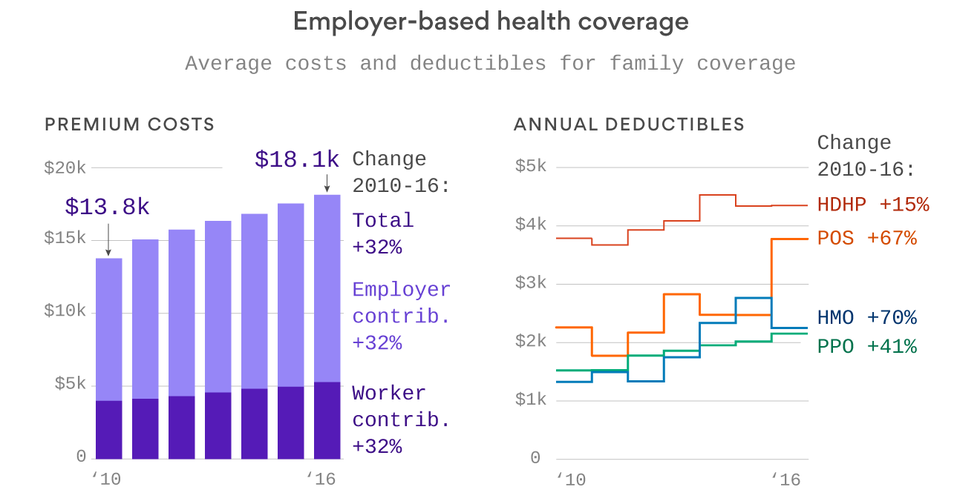

We’ve spent so much time talking about Affordable Care Act costs this year that it’s easy to forget what most people are actually paying for health care — the 156 million Americans who get their health coverage through the workplace. Turns out, most of us aren’t seeing sky-high premium increases. But it’s also worth remembering that deductibles matter too — because that’s what we pay out of pocket before insurance kicks in.

Take a look at these two graphics from Axios datavisuals genius Chris Canipe. The premium increases between 2010 and 2016 weren’t that bad — they’re single digits each year, and just add up over time. But you can see some big increases in deductibles, especially in point-of-service plans and HMOs.

Why it matters: That’s a big reason why people feel their health care costs going up, because it means they’re paying more out of pocket. And when prescription drug prices rise, they’re more likely to feel it directly.

Dynamics of Decline: The Truth About HMOs

http://www.chcf.org/articles/2016/11/dynamics-decline-truth-hmos

California’s commercial health maintenance organization population shrank from 11.9 million to 9.8 million enrollees between 2004 and 2015 (see figure below), a 17.5% decline. But the decline has not been consistent across all HMOs — Kaiser’s commercial enrollment has actually grown during this period.

Two new publications from CHCF take a closer look at how commercial managed care enrollment (including individual enrollment) and the public sector’s embrace of managed care are shifting the way physician organizations are paid — important trends that could affect California’s delivery system.

The first report, As Commercial Capitation Sinks, Can California’s Physician Organizations Stay Afloat?, by Laura Tollen uses quantitative data and findings from stakeholder interviews to shed light on the extent to which commercial capitation is losing ground in California.

A companion set of charts and graphics compiled by Katherine Wilson provides additional detail on health plan enrollment and changes in HMO participation over the past decade.

It is important to look separately at Kaiser and non-Kaiser enrollment. Kaiser is characterized by a mutually exclusive relationship between the health plan (Kaiser Foundation Health Plan) and its two associated Permanente Medical Groups in Northern and Southern California. While Kaiser is by far the largest HMO in California, the health plan offers capitated contracts only to these two medical groups.

Kaiser HMO enrollment increased from 5.6 million to 6.1 million in the last decade, while commercial HMO enrollment for all non-Kaiser plans plummeted, from 6.3 million in 2004 to the current 3.6 million — a loss of more than 40%.

Uncertain Future

The impact of these trends on the state’s non-Permanente physician organizations is uncertain. While declining commercial capitation has not yet had a big effect on their operations, medical group leaders suspect it will soon, according to interviews. The change in commercial payment methods has been slow enough that their organizations have been able to adapt, repurposing some of their HMO-based infrastructure (utilization management tools, for example) for value-oriented payment programs that are FFS-based, such as private accountable care organizations (ACOs).

Among the other findings from the interviews were:

- Declining capitation and rising fee-for-service will not influence individual physicians’ clinical decisions. All interviewees noted that their organizations’ strong culture of providing high-value care would prevent them from fundamentally changing the way they practice, regardless of payment type.

- Despite commercial trends, capitation from Medicare Advantage and Medi-Cal managed care plans is on the rise. However, neither of these types of capitation is seen as a substitute for commercial capitation in terms of supporting infrastructure. While the perception is that Medicare Advantage capitation rates are generous, there is also recognition that these patients are costly. Interviewees said Medi-Cal capitation rates are inadequate.

- Along with the decline in commercial capitation, interviewees expressed alarm at the large increases they observed in patient cost-sharing requirements. All said they fear that patients will not obtain the care recommended by their providers because of high out-of-pocket costs, and some said they already see this happen frequently.

Why This Matters

As more employers shift coverage from HMOs to preferred provider organizations (PPOs) and other non-capitated plans to achieve lower premium rates, they are sacrificing quality and financial protection for employees in exchange for short-term premium savings.

A recent CHCF blog post by Jeff Rideout of the Integrated Healthcare Association highlights the patterns of higher quality / lower cost that distinguish HMO plans in the state (compared to PPOs and other plan types). Large multispecialty physician organizations, which have flourished in California, have a long history and significant expertise in managing risk and coordinating care. These are the very skills that health care purchasers demand from value-based payment programs. Without sufficient infrastructure — which is supported by capitation/prepayment — the foundation of high-value care could crumble.

Given these trends, are employers being penny-wise but pound-foolish in pursuing short-term savings at the expense of longer-term value?

In California, What’s Driving the Variation in Total Cost of Care — Volume or Price?

http://www.chcf.org/articles/2017/02/variation-total-cost-care

As the “repeal and replace” debate continues in Washington over the future of the Affordable Care Act, policymakers considering new legislation should not lose sight of the key concept of the ACA — affordability. High and rising costs are among the most intractable health care issues facing consumers across California and the nation, and any discussion must keep underlying cost drivers at the forefront.

But where should the focus be? At the most elementary level, total health care spending boils down to two main factors: how much care we use (volume, or utilization) and what we pay for that care (price). Teasing out how each factor — utilization or price — contributes to costs is important because cost-control solutions vary depending on the answer.

Across 19 regions in California, the annual risk-adjusted, per capita total cost of care for commercially insured people varies dramatically — from an average high of $5,400 in San Francisco to a low of $3,600 in Kern County, according to 2013 data in the California Regional Health Care Cost & Quality Atlas, a web-based interactive tool produced by the Integrated Healthcare Association (IHA) to monitor cost and quality trends across the state.

Adjusted to reflect differences in population health status, the atlas shows a clear geographic cost pattern. All Northern California regions have higher costs than the statewide average of $4,300, all Southern California regions have lower costs than the state average, and Central California regions have mixed costs.

Three Key Measures

What is driving these differences? Is it variation in per capita utilization, or is it price? While the atlas does not have unit price information, it does include three important hospital utilization measures: emergency department (ED) visits, all-cause readmissions, and inpatient bed days. This allows for basic comparisons of total cost per enrollee vs. three critical measures of utilization. If hospital utilization were driving the overall cost of care, there would be a positive correlation between the cost and utilization measures. However, an analysis of atlas information actually shows the opposite. When considering all commercial health maintenance organization (HMO) and preferred provider organization (PPO) products and regions, cost and volume tend to move moderately in opposite directions.

The quadrant chart below illustrates the relationship between total cost of care and hospital utilization, based on a composite score representing the three utilization metrics. Each orange circle represents a region’s PPO products, and each blue triangle represents a region’s HMO products. With the exception of one outlier region, the data show a moderate negative correlation between hospital utilization and cost. In other words, lower hospital utilization is associated with higher total costs of care.

In the atlas data, total cost of care includes both what the enrollee pays — for example, deductibles and coinsurance — as well as the insurance payments that go to providers. That means cost variation can’t be explained by differences in benefit design among commercial products. Because higher total costs are not driven by greater hospital utilization, and not accounted for by benefit design differences, price seems to be playing a strong role.

There is also an alternative but less likely explanation. Because the atlas only looks at hospital utilization, it’s possible that the total cost of care could be driven by nonhospital utilization as much as the price of care. But because hospital utilization accounts for almost one-third of overall spending on average, it is unlikely that utilization of other services, such as physician and other ambulatory care, has as great an impact on cost variation.

Much of the focus to date on making health care more affordable has involved transferring more financial responsibility to individual patients, the idea being that if consumers have “skin in the game” they will be more discriminating in their care purchases. But if the cost problem is primarily driven by price, which is related to market forces prevalent in a geographic region, is shopping really the solution?

The next version of the atlas, scheduled for release in 2017, will include additional utilization measures and cost information. These will offer a clearer picture of the roles of utilization and price in determining health care costs for commercially insured Californians. Until then the atlas findings stress the need for a better understanding of how pricing differences contribute to total cost variation and encourage us to search for more effective strategies to influence prices as well as utilization.