http://healthaffairs.org/blog/2017/07/31/outside-of-washington-there-is-a-new-vital-center-in-health-care-reform/

Republicans in Congress are mired in political quicksand. Following passage of the Affordable Care Act (ACA) in 2010, they locked themselves into a promise to repeal and replace it at the behest of ultra-conservative donors and party activists who control the GOP’s nomination process. Since 2010, however, Americans and rank-and-file Republicans increasingly came to expect help meeting the rising costs of medical care and insurance and to accept the ACA’s tangible programs to address these concrete challenges.

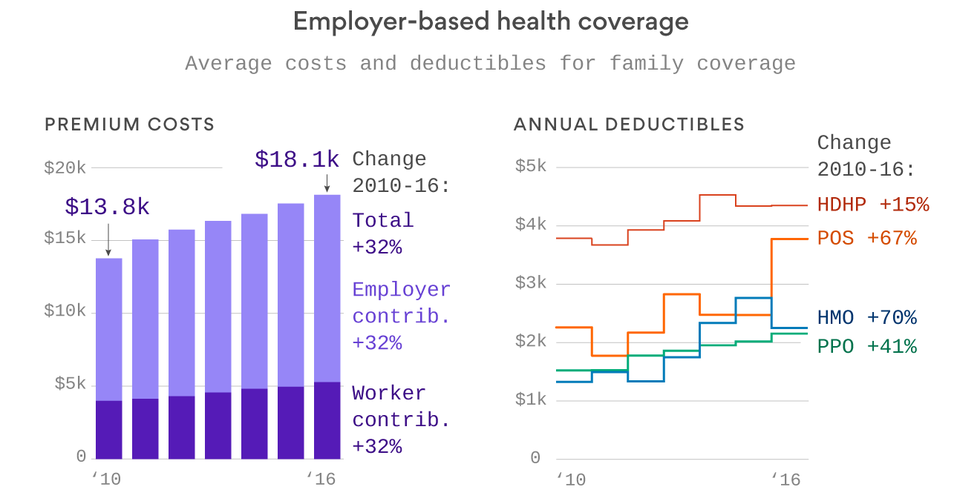

The Democrats created their own political trap. They passed the ACA on the promise of making health care affordable but deductibles and rising premiums continued to present a burden to many Americans.

Both parties are missing, however, the vital center on health reform that has formed since 2010. Americans are frustrated with Democrats for not delivering on their promise of affordability, and they are now alarmed with Republican efforts to repeal—instead of improve—the ACA’s coverage of costs.

Tracking Changes In Public Opinion

Most public opinion polls are unable to track these changes in opinion about health care because they are only snapshots, drawn from a moment in time. To remedy this, we have been gathering panel data, tracking the views of the same group of Americans every two years since the ACA’s passage in 2010. This equips us to study how individuals respond to the ACA as they experience or learn more about the law’s provisions over time. Specifically, we conducted four waves of interviews in the two-month period leading up to national elections from 2010 to 2016 when health reform received heightened attention; this avoided the risk of choosing an arbitrary month when health reform might have arbitrarily lost or gained salience.

The first wave was conducted by the Survey Research Institute (SRI) at Cornell University and consisted of a national sample of 1,200 adults. Abt SRBI (now part of Abt Associates) conducted the last three waves, returning to the same individuals. All waves asked identical questions and were administered by telephone, using only landlines in 2010 and adding mobile phones in 2012, 2014, and 2016. Forty-nine percent of the original 2010 survey (587 individuals) responded to all four waves. Survey weights were applied to each survey to match representative demographic targets and allow us to generalize from our panel to the adult population in the United States.

Why Americans Dislike Health Reform

Republicans have been eager to highlight the unpopularity of the Affordable Care Act, also known as “Obamacare.” Exhibit 1 shows that unfavorable assessments of the ACA have steadily increased since its passage. Unfavorability rose from 44 percent in 2010 to 58 percent in 2016.

Exhibit 1: Increasingly Unfavorable Views Of The Affordable Care Act (Percent)

Question: “As you may know, a major health care bill was signed into law in 2010. Given what you know about this law, do you have a generally favorable or generally unfavorable opinion of it, or do you have a neutral opinion, neither favorable nor unfavorable?” Exhibit 1 presents the “unfavorable” responses.

Why are Americans increasingly disenchanted with the ACA? The public’s displeasure emanates to a large extent from frustrations with health care costs. Democrats promised to lower the costs of medical care and insurance with the enactment of the ACA. They did succeed to slow the rate of increase in national health care spending and insulate most subsidized enrollees in its insurance Marketplace from premium increases, as the Congressional Budget Office reports (Note 1). Yet, the costs of medical care remain high, and premiums and deductibles are out of the reach of some Americans.

The source of the public’s rising frustration with health care costs is picked up in Exhibit 2. The first grouping of bars on the left shows increasing frustration with costs for medical treatments that are not covered by insurers. By 2016, 14 percent expressed dissatisfaction with the amount and number of treatments that their insurance covered, a 6-point increase from 2014. One-third of Americans also expressed dissatisfaction in 2016 with the out-of-pocket costs that they were forced to pay because of gaps in their insurance coverage, as shown in the middle cluster. This is an 8-point increase from 2014.

Exhibit 2: Rising Concerns About Affordability (Percent)

Question: Several questions asked respondents to indicate their satisfaction or dissatisfaction with individual features of the health care system—“The number and kind of treatments your health insurance will cover” and “The amount you spend out of pocket on health care costs your insurance doesn’t cover.” A separate item asked respondents to indicate their agreement or disagreement with the statement: “Public officials care about making health care more affordable for people like me.” (Exhibit 2 shows “disagreement” with the statement.)

The public’s disappointment with the persistent burden of health care costs leads it to blame lawmakers for a lack of responsiveness. The bars on the right in Exhibit 2 indicate that a growing majority of Americans disagree with the statement that, “Public officials care about making health care more affordable for people like me.” Fifty-eight percent of Americans disagreed with this statement in 2016, a 10-point increase since 2012.

In addition, the sense that the ACA has not delivered the affordability that Democrats promised may help account for the sharply stronger conclusion in recent years that the ACA’s taxes present a heavier burden. Exhibit 3 shows that the proportion of Americans who believe that their taxes have increased a lot or a little has risen from 43 percent in 2012 to 56 percent in 2016. This growing perception that the ACA has increased taxes rests on inaccurate assumptions. The ACA’s financing primarily relies on two taxes on individuals whose yearly income exceeds $200,000 or for married couples earning more than $250,000—an increase in Medicare’s tax on earnings by 0.9 percent and a new 3.8 percent tax on capital gains from investments. These taxes fall on less than 2 percent of tax filers, according to the non-partisan Tax Policy Center (Note 2).

Exhibit 3: Growing Perception That The Affordable Care Act Increased Taxes (Percent)

Question: “Do you think that the new health care law enacted in 2010 has increased the taxes that you pay, decreased the taxes that you pay, or has it had no impact on the taxes that you pay?”

Americans Oppose Repeal Because They Appreciate The Effects Of Health Reform

Considering the strong public disapproval of repeal, President Donald Trump and congressional Republicans are discovering that it is a mistake to equate the public’s frustrations with the ACA with support for repealing its programs. When respondents reported “unfavorable” views of the law, we followed up with a question asking them whether they would prefer either “repeal[ing] [the ACA] as soon as possible,” or “giving the law more time to have a chance to work, with lawmakers making necessary changes along the way.” In Exhibit 4, we combined those who favored giving it “a chance to work” with those who expressed “favorable” overall views of the law. This shows that since 2010 more Americans favored the law or wanted to give it time to be improved than backed repeal. Although support for repeal inched up since 2010, a greater percentage of Americans consistently favored the ACA and improving it over repeal by a 41-to-37 margin in 2010 and by 49-to-43 in 2016.

Exhibit 4: More Americans Prefer To Keep And Improve The Affordable Care Act Than Repeal It (Percent)

Question: This figure is based on two survey questions. The first is the following: “As you may know, a major health care bill was signed into law in 2010. Given what you know about this law, do you have a generally favorable or generally unfavorable opinion of it, or do you have a neutral opinion, neither favorable nor unfavorable?” Respondents who had an unfavorable view were asked a second question about their view about the law’s future: “The law should be given more time to have a chance to work, with lawmakers making necessary changes along the way, OR the law should be repealed as soon as possible?” The repeal bar reports responses from the second question; the other bar adds together favorable responses in the first question with the “law should be given more time” responses.

Support for keeping and improving the ACA stems from a growing appreciation for its concrete effects. Exhibit 5 shows that rising percentages pinpoint the ACA’s tangible programs as having either “a great deal” or “quite a bit” of an impact on themselves and their family (other options included “some,” “a little,” and “none”). There is greater recognition in 2016 compared to 2010 or 2012 of the impact of allowing parents with insurance to continue to cover their children until they are 26 years old. More than one in five Americans now report that the ACA expanded their access to health insurance. In addition, nearly one in four Americans, 24 percent, voiced appreciation for the impact of the ACA’s assistance to seniors to pay for prescription medications. Moreover, recognition of a personal impact resulting from the ACA’s tax credits and other subsidies to help people purchase health insurance has remained stable since 2014 and is higher than in earlier years.

Exhibit 5: Rising Appreciation Of The Impact Of The Affordable Care Act (Percent)

Question: “I’m going to read to you a list of some of the features of the health care law that was enacted in 2010. For each one, please answer this question: “How much of an impact has this feature had on you and your family: a great deal, quite a bit, some, a little, none?” Respondents are asked about the following features of health reform: coverage of adult children on their parents’ insurance plans until they are 26 years old; access to health insurance or medical care supported or provided by government; help for seniors to pay for prescription drugs; and tax credits and other subsidies to help people pay for health insurance. Exhibit 5 combines “a great deal” and “quite a bit.”

The New Vital Center On Health Reform

Overall evaluations of the ACA follow the partisan pattern that is familiar today: 68 percent of Democrats have favorable views versus 9 percent of Republicans. What stands out, however, is that the ACA’s tangible effects are starting to loosen rigid partisan dividing lines. Exhibit 6 shows the percentage of Americans reporting a personal impact from at least one of the four provisions presented in Exhibit 5. Democratic elected officials enacted the ACA, and, not surprisingly, majorities of rank-and-file Democrats have generally singled out the law’s effects from early on: 51 percent of Democrats reported an impact from at least one of the law’s features in 2010; by 2016, this recognition remained largely stable, inching up to 54 percent. Strikingly, however, the percentage of Republicans perceiving an impact on themselves or their families has increased by 8 percentage points, from 26 percent in 2010 to 34 percent in 2016 despite vociferous GOP attacks on the ACA. Among independents, the proportion soared by 23 points, from 28 percent to 51 percent. These findings indicate that appreciation for the ACA has expanded beyond the ranks of Democratic partisans who were predisposed to favor it; growing numbers of Americans across the political spectrum increasingly value the impacts of health reform in their own lives.

Exhibit 6. Widening Appreciation Of The Affordable Care Act’s Impact (Percent Reporting Impact Of A New Benefit)

Exhibit 6 presents the percentage of respondents who reported that at least one of the four provisions presented in Exhibit 5 had a “great deal” or “quite a bit” of impact on themselves or their family.

The crux of the public discontent with the ACA—and the repeal proposals by Republicans—is the amount paid for insurance coverage. Respondents to the survey appear to share the complaint of ACA critics that insurance costs are too high. After high expectations following the ACA’s enactment, satisfaction with the cost of health coverage has dropped by 10 points—from 73 percent satisfied in 2010 to 63 percent in 2016. This general assessment misses, however, a crucial condition—whether or not individuals are covered by government programs such as Medicare, Medicaid, or a subsidy financed by the ACA. We found a striking pattern among Republicans, Democrats, and independents: By a margin of 20 points or more, individuals with government coverage were consistently more satisfied with the cost of insurance than those who rely on private health plans. For instance, 79 percent of Republicans with government coverage were content with insurance costs as compared to 56 percent without this coverage. Independents outside the sway of either major party expressed the highest satisfaction when experiencing government coverage (100 percent) and exhibit the largest gap between those covered and those without coverage (41 points).

In short, Republican public officials continue to spotlight what they perceive as the disappointment of Americans with ACA coverage, but the reality is that the most dissatisfied are those who lack government insurance. In fact, most Americans (including Republicans) who benefit from government insurance are content with their coverage.

Health Reform’s New Vital Center

Public opinion toward the ACA has been poorly understood because of an apparent contradiction. On the one hand, a growing share of the public harbor unfavorable views of the ACA as a whole, and proponents of repeal have seized on this dissatisfaction to claim a popular mandate. On the other hand, the discontent of Americans stemmed from disappointment with the ACA for not satisfying their expectations of genuine protection from the burden of costs. Far from wanting to be rid of the ACA, Americans are looking to it to deliver more effective protection.

In the immediate aftermath of World War II, the historian Arthur Schlesinger, Jr., wrote of the “vital center” about the direction of America that was supported by both major political parties and most Americans. Despite today’s fractiousness in Washington over health reform, everyday Americans are converging toward a new vital center of support for health care reform.

Awareness of the ACA’s tangible impacts fits into a robust notion of collective responsibility instead of the individualist approach advocated by conservatives. Since the ACA’s passage, nearly nine out of 10 Americans have consistently embraced access to health care as a “basic right.” Not surprisingly, nearly all Democrats embrace the principle of health care as a right. What stands out is that rank-and-file Republicans overwhelming and increasingly hold the same view—rising from 64 percent in 2010 to 72 percent in 2016. Contrary to the position of Washington Republicans, establishing health care as a birthright owed to Americans is now widely shared. Republican proposals, such as those that would allow states to opt out of some of the ACA’s core consumer protections (including those guaranteeing coverage for individuals with preexisting medical conditions), may well tap into this strain of public opinion and provoke broad opposition.

Elected officials in Washington and, particularly, steadfast opponents of health reform are sliding to the margins of public opinion. The daily problems that Americans face in paying for medical care and insurance mean that pragmatism is trumping ideology. In the past, federal lawmakers responded to broad public agreement and worked across the aisle to improve the flaws in the original legislation that produced Social Security in 1935 and Medicare in 1965. The question today is whether Washington can return to that pragmatic tradition and catch up to the emerging vital center in Americans’ attitudes toward health reform.

Note 1

Congressional Budget Office. American Health Care Act: cost estimate. Washington (DC): CBO; 2017 Mar 13.

Note 2

Tax Policy Center. Tax units above and below the $250,000/$200,000 threshold, 2013–2022. Washington (DC): TPC; 2012 Nov 26