While headlines fixate on the future of the Affordable Care Act’s health insurance exchanges, a more consequential fight is brewing over the future of Medicaid. Proposed reforms would affect tens of millions of Americans and state governments across the country. Previous attempts have failed, however, and longstanding roadblocks may sink this administration’s efforts as well.

With over 70 million enrollees, Medicaid covers more Americans than any other insurer. Responsibility for funding the program – which accounts for nearly 20 percent of all healthcare spending – is shared between states and the federal government. At a minimum, the federal government covers 50 percent of costs, with that share rising to nearly 75 percent in the poorest states and more than 90 percent for those covered through ACA Medicaid expansions. This amounts to nearly $350 billion in federal funding per year.

Importantly, this money is allocated in an open-ended manner. As states increase the generosity of their Medicaid programs, the federal government is obliged to pay its portion of the higher costs.

During his campaign, Donald Trump joined a long list of Republican lawmakers who argue that this gives states the wrong incentives. Because the federal government covers at least half of each dollar spent, they argue, states may take less care to weed out inappropriate and inefficient spending as they otherwise would.

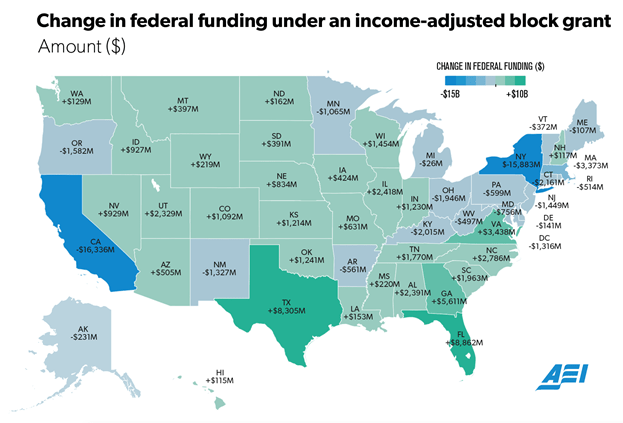

To eliminate this open-ended feature, Trump’s plan calls for federal money to be allocated in fixed lump sum payments known as block grants.

First proposed in 1981 by President Reagan, block granting of Medicaid hardly represents a novel policy option. Why then has the current system endured, and what does this portend for the resistance Trump’s efforts may encounter?

To understand, consider the most basic decision for any block grant policy: How should each state’s grant be initially determined?