As we ring in the new year there is one thing – maybe the biggest thing – lingering from 2025 that can’t be dropped: The alarming state of health care.

Every aspect of the health care system feels like it’s working against its customers by prioritizing profits over care.

There are significant signs we could be at a breaking point.

- More Americans than ever are opting to go without health insurance. A Gallup poll found 1 in 3 are considering running that risk, saying they can’t afford the costs.

- For the first time in history, concern for rising health care costs is stride for stride with housing and food costs as American wages are struggling to keep pace. For many income levels they feel left permanently behind.

- And not only are people paying record-high premiums, what they have to pay for prescription drugs at the pharmacy counter is breaking the bank as insurance companies have gobbled up pharmacy benefit managers to capture more and more of what we spend on health care.

- The number of pharmacies serving the country’s sick has dwindled to the lowest levels in more than 50 years. Rite-Aid, which once operated more than 5,000 stores across the country, closed all of its locations and declared bankruptcy last year. Thousands of independent pharmacies have also closed, largely because of the stranglehold PBMs now have on the prescription drug supply chain. The closures have created hundreds of pharmacy deserts, leaving patients with a dwindling number of low-cost and convenient options.

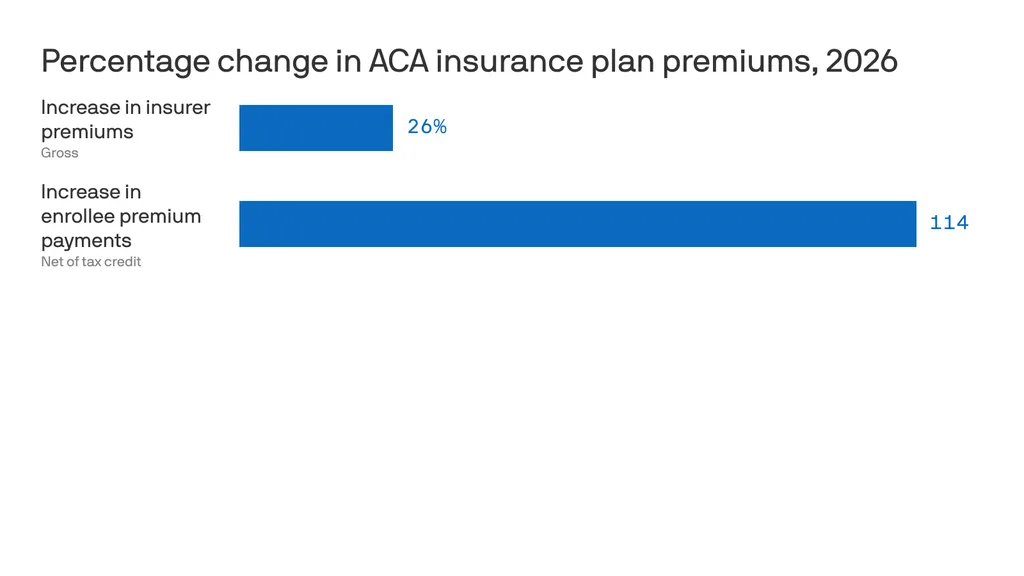

- Medicaid cuts mandated by Congress and the Trump administration last year are expected to cause more rural hospitals to close. More than 100 closed in the last decade and hundreds more are on the brink, according to a Boston University study. Health care is in such a bad spot it’s near the top of the 2026 Congressional agenda. Democrats want to restore the enhanced subsidies that made coverage affordable for the more than 20 million Americans who rely on the Affordable Care Act marketplace for their health insurance but most Congressional Republicans say the subsidies are a waste of money. Despite all that, there’s pessimism that politicians have the appetite for real change.

“We are frogs in a boiling pot,” said Eric Pachman, co-founder of the prescription drug watchdog 46 Brooklyn and data analyst on Wall Street. “Every year health care plans cost more but the coverage we pay for gets crappier.”

Pachman was recently at home when he got a call from a close relative whose son was in the middle of an allergic reaction. The family didn’t have health insurance because the premiums were beyond their means.

“He gave his son an Epi Pen and then drove to the hospital close by,” Pachman said. “He sat there for a while with his son in the parking lot to make sure he didn’t get worse but he didn’t go in.”

Americans are making those alarming decisions while health insurance companies continue to make big profits.

The country’s three largest health insurance companies and their in-house pharmacy benefit managers have rocketed toward the top of the Fortune 500 list of richest companies.

UnitedHealth has become America’s third-richest company behind Walmart and Amazon. In 2024, the company, which has about 30 million Americans enrolled in its health plans, brought in more than $400 billion in revenue, according to its financial filings.

CVS Health is just behind UnitedHealth at No. 5 on the country’s Fortune 500 list, bringing in nearly $373 billion in 2024. Cigna is 13th with $247 billion in revenue.

Health care alarms similar to sirens of 2008 housing collapse

The warning signs of this health care crisis bear a haunting resemblance to the 2008 housing market crash.

- Cost vs. Income: In 2006, the average employer-sponsored family health care plan cost $11,381, representing 23% of the average salary. In 2026, the average plan is expected to exceed $27,000 against an average salary of $84,000 — a staggering 32% of income.

- Shifting Risk: Just as risky mortgages were offloaded onto consumers, employers have shoved a larger portion of health care costs onto their workers.

- Debt: Half of American adults now report they could not pay a $500 medical bill without going into debt.

- Opacity: Much like the complex derivatives in mortgages in 2008, PBMs and insurers refuse to make their pricing public. This lack of transparency leaves patients fearing to open their mail after a hospital visit.

The sad joke in Washington D.C. right now is that everyone keeps talking about the price of health care but no one knows what the actual prices are.

In that Gallup poll, those surveyed gave the U.S. health care system a grade of D+.

“Our government continues to apply band-aids to a bloated pricing system rather than prescribing real, system-wide solutions,” said Antonio Ciaccia, co-founder of the pharmacy drug data site 46Brooklyn.com and former head of government affairs for the Ohio Pharmacist Association.

Lawmakers in more than a dozen states have tried to rein in insurers and their PBMs with lawsuits and regulations. Those lawsuits have led to more than $400 million in payouts by the big three health insurers and their subsidiaries.

Despite that the system keeps on going.

After years of battling insurers and their PBMs, Ohio’s Republican Attorney General, Dave Yost, came to the conclusion that any major reforms would have to come at the federal level.

He formed a coalition with 39 other states and has made repeated trips to Washington D.C. urging Congress to act.

“PBMs were originally intended to reduce the financial burden on Americans for prescription drugs, but the reality today is starkly different,” Yost said. “Instead of prioritizing the interests of patients, PBMs have shifted their focus to maximizing profits and marginalizing local pharmacies from the marketplace.”

Pachman also said if more people do opt out of insurance they will still go to hospitals for medical care.

“Hospitals cannot turn those patients away because they are legally required to treat them,” Pachman. “That means the cost burden will be shifted to those that do pay for insurance.”

While any type of significant reforms seem unlikely, many states are at least starting to ban medical debt from credit reports.

Fifteen states have the ban in place and Ohio, Alaska, North Carolina and Michigan are exploring similar statutes this year.

Chris Deacon, an attorney, author, health care reform advocate and former director for the New Jersey treasury department said the only incentive right now is for insurers to keep growing the $5.3 trillion spent on health care in the United States in 2024.

“There’s no incentive to control prices,” Deacon said. “And there’s no transparency whatsoever in any of this.”