The Federal Reserve cut its target interest rate Wednesday by an extra-large half-percentage point and projected more rate cuts this year and next, as its period of trying to put brakes on the economy to fight inflation comes to a close.

Why it matters:

The move lowers borrowing costs for consumers and businesses, as the central bank aims to keep the economy’s expansion going strong amid warning signs on the outlook.

What they’re saying:

“The labor market is actually in solid condition — and our intention with our policy move today is to keep it there,” Fed chair Jerome Powell told reporters at a press conference on Wednesday.

“The U.S. economy is in good shape. It’s growing at a solid pace,” Powell added. “We want to keep it there.”

Zoom in:

The rate cut reflects the U.S. entering a new phase where the softening job market is the predominant economic risk — rather than elevated inflation.

By going with an aggressive half-point cut instead of its more traditional quarter-point adjustment, the Fed moved to get ahead of some evident faltering in the job market.

However, new projections imply the Fed will shift toward smaller quarter-point rate cuts from here.

The cut also thrusts the Fed into election-year politics, as former President Trump has said the central bank should not ease monetary policy mere weeks before the election. Some Democrats have called for even more aggressive rate cuts.

Driving the news:

The policy-setting Federal Open Market Committee lowered its target range for the federal funds rate to 4.75%–5%, from the 5.25–5.5% range in place since last July.

The central bank also released new projections that anticipated the rate will be cut an additional half-point by December — implying a quarter-point cut at each of its two remaining 2024 meetings.

The median Fed officials anticipated their target rate will be down to 3.4% by the end of 2025, which implies four quarter-point rate cuts next year.

“Job gains have slowed,” the Fed’s policy statement noted, adding that the committee “has gained greater confidence that inflation is moving sustainably toward 2 percent.”

Of note:

The Fed policy meeting marked the first dissent from a board member in more than two years. Michelle Bowman, a Trump-appointed governor who focuses on community banking issues, preferred to cut by only a quarter point.

Bowman’s dissent is also the first by a member of the Fed’s seven-member Board of Governors — as opposed to a regional Fed bank president — since 2005.

Christopher Waller, the other Trump-appointed governor on the board, supported the action.

By the numbers:

The median official saw inflation for the full year coming in at 2.3%, not far from the Fed’s 2% target. By contrast, in June, officials saw 2.6% inflation this year.

They also anticipate slightly higher unemployment. The projections listed a 4.4% unemployment rate in the final quarter of the year. That rate was 4.2% in August, up from 3.7% at the start of the year.

However, the Fed officials’ forecasts also imply the jobless rate leveling out at that point and being flat at 4.4% in the final months of 2025.

The bottom line:

Powell and his colleagues elected to take more aggressive action Wednesday in hopes that it will be enough to forestall any further deterioration in the job market of the sort seen over the last few months — and is betting that the Fed can move to a more gradualist approach from here.

Speaking about the larger-than-anticipated rate cut, Powell said he was pleased the Fed made a strong start in lowering interest rates.

“The logic of this — both from an economic standpoint and also from a risk management standpoint — was clear,” Powell said.

He added: “We’re gonna take it meeting by meeting. … There’s no sense that the committee feels it’s in a rush to do this.”

For more than two years, the economy’s big problem was inflation — it was the key irritant for policymakers, the White House and American consumers.

Today’s Consumer Price Index report confirms that is no longer the case: Prices are no longer rising rapidly, which means the battle to kill inflation appears all but over.

Why it matters:

Inflation looked to be coming down alongside a still-flourishing economy — until recently. The string of upbeat inflation data is all but certain to allow Fed officials to more comfortably shift their attention to the weakening labor market and lower interest rates.

What they’re saying:

“[T]he cumulative improvement in the overall inflation data over the past year now gives the Federal Reserve cover to move into risk management mode with the intent of protecting and preserving the soft landing,” Joe Brusuelas, chief economist at accounting firm RSM, wrote today.

By the numbers:

Overall CPI rose 2.9% in the 12 months ending in July, dropping below 3% for the first time since 2021.

Core CPI, which excludes food and energy prices, rose 3.2% — the smallest increase in three years.

By a different measure, inflation looks more benign. Over the last three months, core CPI rose 1.6% on an annualized basis, down from 2.1% in June.

Zoom in:

Prices for many key items increased more slowly — or, in some cases, got cheaper over the month.

Grocery costs have been rising at a mild pace since February, including a 0.1% increase in July. Prices are up just 1% compared to the same time last year.

Used vehicle costs fell 2.3% in July, a bigger drop than that seen the previous month. New vehicle prices fell 0.2%, the sixth-straight month of price decreases.

The intrigue:

The bad news was in the housing sector, where prices have kept upward pressure on inflation.

The shelter index is a huge component. It accounted for over 70% of core CPI’s 12-month increase through July, the government said.

The sector is “solely responsible for core inflation remaining above the Fed’s 2% target,” Preston Caldwell, senior U.S. economist at Morningstar, wrote today.

In the CPI report, the rent index rose 0.5%, up from 0.3%. Owner’s equivalent rent, which the government uses to account for inflation in homes that people own, rose 0.4% after slowing in June.

What to watch:

The question in recent weeks has been how drastic of a cut the Fed will make at the conclusion of its next policy meeting in September — rather than whether it will do so at all.

The odds that the Fed would cut by a quarter of a percentage point rose to 54% after the inflation report, according to CME’s FedWatch tool.

As of yesterday, odds of a half-percentage point cut looked slightly more likely.

The bottom line:

The incoming data about the health of the labor market will ultimately determine that call.

“This is now a labor data-first Fed, not an inflation data-first Fed, and the incoming labor data will determine how aggressively the Fed pulls forward rate cuts,” economists at Evercore wrote in a note this morning.

The US labor market added more jobs than expected in May defying previous signs of a slowdown in the economy.

Data from the Bureau of Labor Statistics released Friday showed the labor market added 272,000 nonfarm payroll jobs in May, significantly more additions than the 180,000 expected by economists.

Meanwhile, the unemployment rate rose to 4% from 3.9% the month prior. May’s job additions came in significantly higher than the 165,000 jobs added in April.

The print highlights the difficulty the Federal Reserve faces in determining when to lower interest rates and how quickly. The economy and labor market has held up overall, and inflation has remained sticky, building the case for holding rates higher for longer. Yet some cracks have emerged, such as signs of inflation pressuring lower income consumers and rising household debt.

“They’re really walking a tight rope here,” Robert Sockin, Citi senior global economist, told Yahoo Finance of the central bank. He noted the longer the Fed holds rates steady, the more cracks could develop in the economy.

Wages, considered an important metric for inflation pressures, increased 4.1% year over year, reversing a downward trend in year-over-year growth from the month prior. On a monthly basis, wages increased 0.4%, an increase from the previous month’s 0.2% gain.

“To see more confidence that inflation could move lower over time, you’d really like to see the wage numbers look a little lower than we’ve seen them today,” Lauren Goodwin, New York Life Investments economist and chief market strategist, told Yahoo Finance.

Also in Friday’s report, the labor force participation rate slipped to 62.5% from 62.7% the month prior. However, participation among prime-age workers, ages 25-54, rose to 83.6%, its highest level in 22 years.

The largest jobs increases in Friday’s report were seen in healthcare, which added 68,000 jobs in. May. Meanwhile, government employment added 43,000 jobs. Leisure and hospitality added 42,000 jobs.

The report comes as the stock market has hit record highs amid a slew of softer-than-expected economic data, which had increased investor confidence that the Federal Reserve could cut interest rates as of September. After Friday’s labor report, that trend reversed with investors pricing in a 53% chance the Fed cuts rates in September, down from a roughly 69% chance seen just a day prior, per the CME FedWatch Tool.

A number of hospitals and health systems are reducing their workforces or jobs due to financial and operational challenges.

Below are workforce reduction efforts or job eliminations announced this year.

Editor’s Note: This webpage was created Jan. 19 and updated May 10.

May

White Rock Medical Center in Dallaslaid off nearly 35% of its staff. The hospital temporarily stopped taking patients transported by emergency medical services due to the layoffs, The Dallas Morning News reported. It has since resumed accepting those patients.

Oakland-based Kaiser Foundation Hospitals is laying off 76 workers in California. The layoffs primarily affect employees in IT and marketing, according to regulatory documents filed with the state May 1.

April

Pittsburgh-based UPMC will lay off approximately 1,000 employees. The layoffs, which represent more than 1% of the health system’s 100,000 workforce will primarily affect nonclinical, administrative and non-member-facing employees.

Union Springs, Ala.-based Bullock County Hospitallaid off 95 employees beginning April 9, according to regulatory documents filed with the state. The layoffs occurred as Bullock seeks to become a rural emergency hospital and is ending psychiatric services as part of the shift, AL.com reported April 25.

Jackson Health Systemreduced compensation programs for senior leaders; laid off fewer than 25 people, including one hospital CEO; and froze many vacant positions, especially in support and nonclinical areas, a spokesperson for the Miami-based organization confirmed to Becker’s. President and CEO Carlos Migoya shared these efforts in a message to staff, citing financial challenges.

Coos Bay, Ore.-based Bay Area Hospital plans to conduct layoffs as it outsources its revenue cycle management operations, a spokesperson for the hospital confirmed to Becker’s. The transition will affect 27 positions.

Manchester, N.H.-based Catholic Medical Centerplans to cut 142 positions, including 54 layoffs. An April 18 letter to employees from CMC president and CEO Alex Walker, obtained by Becker’s, said cuts would occur through the 54 staff eliminations, open position cuts, reduced hours, planned departures, and resource redeployment in satellite locations for CMC.

Marshfield (Wis.) Clinic Health System will lay off furloughed staff, effective in early May. The health system furloughed about 3% of its workforce in January, affecting positions mostly in non-patient-seeing departments, including leadership roles.

Norwalk, Ohio-based Fisher-Titus Medical Centerlaid off some workers in nonclinical roles and reduced hours for others. Seven employees, about 0.5% of the health system’s workforce, were laid off April 1. Work hours were reduced for another 10 positions, a hospital spokesperson told Becker’s.

March

Robbinsdale, Minn.-based North Memorial Health is laying off 103 employees in clinical and nonclinical roles, citing financial challenges. The layoffs affect several services across the two-hospital system.

AHMC’s San Gabriel (Calif.) Valley Medical Center is laying off 62 workers, according to regulatory documents filed with the state March 13. The layoffs take effect May 13.

Miami-based North Shore Medical Center, part of Steward Health Care, started conducting layoffs as part of cuts to some of its programs amid the Dallas-based health system’s continued financial struggles. Around 152 workers represented by 1199SEIU were laid off, a union spokesperson confirmed. However that number could be higher as their members do not represent every employee at NSMC, the spokesperson said.

Oakland, Calif.-based Kaiser Foundation Hospitals is laying off more than 70 employees. The layoffs primarily affect those in IT roles.

February

Lion Star, the group that operates Nacogdoches (Texas) Memorial Hospital, is closing four of its clinics on March 22, which will result in fewer than 50 layoffs, a Lion Star spokesperson confirmed to Becker’s. No additional layoffs are planned.

Little Rock-based Arkansas Heart Hospital has laid off fewer than 50 employees since the beginning of 2024, citing low reimbursement rates. The layoffs affected lower-paying positions, Bruce Murphy, MD, CEO of the hospital, said, according to Arkansas Business.

Cincinnati-based Mercy Health will lay off some call center positions. The system attributed the move to its partnership with a third party to operate its enterprise contact center for primary care scheduling.

Ridgecrest (Calif.) Regional Hospitalannounced more layoffs to avoid closure. It is laying off 31 more employees, including seven licensed vocational nurses and four registered nurses, two months after it announced plans to lay off nearly 30 others and suspend its labor and delivery unit, Bakersfield.com reported Feb. 15.

Medford, Ore.-based Asante health systemlaid off about 3% of its workforce. The layoffs primarily affected administrative and support roles and were necessary to offset “financial headwinds” over the past several years, according to a report from NBC affiliate KOBI-TV, which is based on an internal memo sent to staff Feb. 9.

Oakdale, Calif.-based Oak Valley Hospital District is scaling back services and laying off workers to improve its finances. The hospital said in a Feb. 2 statement shared with Becker’s that it will close its five-bed intensive care unit, discontinue its family support network department and lay off 28 employees, including those in senior management and supervisor positions.

Chicago-based Rush University System for Healthlaid off an undisclosed number of workers in administrative and leadership positions, citing “financial headwinds affecting healthcare providers nationwide.” No additional information was provided about the layoffs, including the number of affected employees.

University of Chicago Medical Center laid off about 180 employees, or less than 2% of its roughly 13,000-person workforce. The majority of affected positions are not direct patient facing, the organization said in a statement shared with Becker’s.

Fountain Valley, Calif.-based MemorialCarelaid off 72 workers due to restructuring efforts at its Long Beach (Calif.) Medical Center and Long Beach, Calif.-based Miller Children’s and Women’s Hospital. The layoffs include 13 positions at Long Beach Medical Center’s outpatient retail pharmacy, which is closing Feb. 2, a spokesperson for MemorialCare said in a statement shared with Becker’s.

January

George Washington University Hospital in Washington, D.C., part of King of Prussia, Pa.-based Universal Health Services, is laying off “less than 3%” of its employees. The move is attributed to restructuring efforts.

Amarillo-based Northwest Texas Healthcare System, also part of Universal Health Services, announced plans to lay off a “limited number of positions.” The move is attributed to restructuring efforts.

Lehigh Valley Health Network is cutting its chiropractic services and laying off 10 chiropractors. The layoffs are effective April 12 and due to restructuring. The Allentown, Pa.-based health system has 10 chiropractic locations, according to its website.

Central Maine Healthcare is laying off 45 employees as part of management reorganization. The Lewiston-based system, which also ended urgent care services at its Maine Urgent Care on Sabattus Street in Lewiston on Jan. 12, has 3,100 employees total.

University of Vermont Health Network, based in Burlington, is cutting 130 open positions. The move is part of the health system’s efforts to reduce expenses by $20 million.

Med-Trans, a medical transport provider based in Lewisville, Texas, closed its UF Health ShandsCair base serving Gainesville, Fla.-based UF Health Shands Hospital on Jan. 10 due to decreased transportation demands. The move also resulted in layoffs, a spokesperson for UF Health, the hospital’s parent company, told Becker’s in a statement.

RWJBarnabas Health, based in West Orange, N.J., is laying off 79 employees, according to documents filed with the state on Jan. 8. The layoffs are effective March 31 and April 5. A spokesperson for the health system told Becker’s that 74 of the positions were “time-limited information technology training job functions.” The other layoffs were due to closure of an urgent care center.

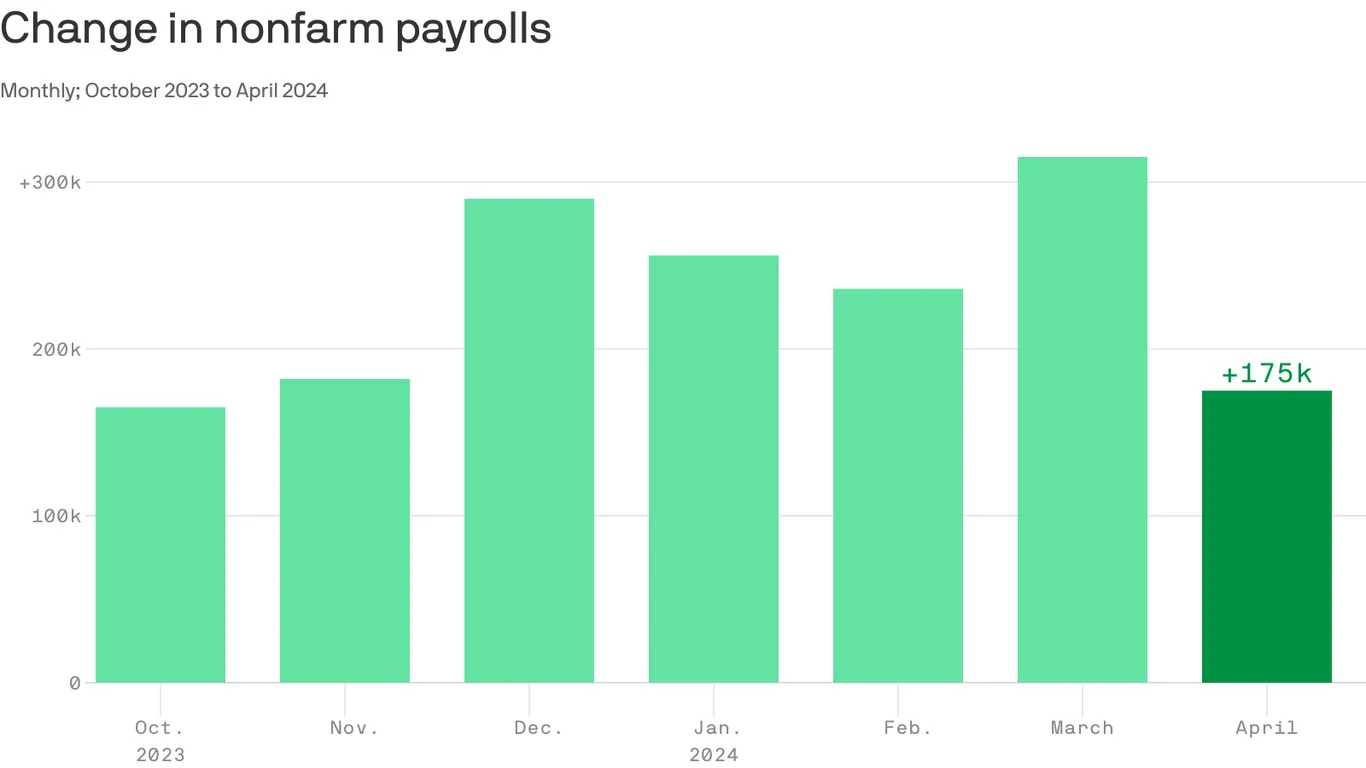

The U.S. economy added 175,000 jobs in April, while the unemployment rate ticked up to 3.9% from 3.8%, the Labor Department said on Friday.

Why it matters:

Jobs growth slowed from the prior month’s hot pace, but the data suggests that the labor market is still chugging along with healthy demand for workers.

The pace of hiring was notably slower than economists’ estimate of 240,000 jobs in April.

Job gains in March were slightly better than previously thought, upwardly revised to 315,000 from 303,000—though payrolls in February were revised lower by 34,000 to 236,000.

Driving the news:

The lower-than-expected job gains were concentrated in health care, social assistance, transportation and warehousing

Average hourly earnings, a measure of wage growth, rose 0.2%.

Over the past 12 months, average hourly earnings increased 3.9%.

State of play:

Friday’s data is the latest evidence that the labor market is holding steady — an important development for the broader economy.

The Federal Reserve this week kept interest rates at the highest level in more than two decades.

Its policymakers suggested that any rate cuts would happen later than previously thought due to stalled progress on curbing inflation.

Fed chair Jerome Powell this week said that the central bank would be “prepared to respond to an unexpected weakening in the labor market.”

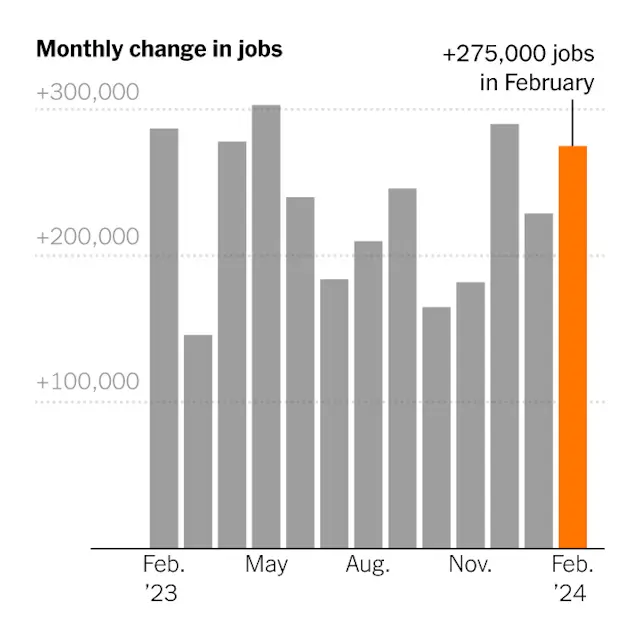

The labor market showed resiliency in February, adding 275,000 jobs, a sign that economic growth is still solid.

If the economy is slowing down, nobody told the labor market.

Employers added 275,000 jobs in February, the Labor Department reported Friday, in another month that exceeded expectations.

It was the third straight month of gains above 200,000, and the 38th consecutive month of growth — fresh evidence that after surging back from the pandemic shutdowns, America’s jobs engine still has plenty of steam.

“We’ve been expecting a slowdown in the labor market, a more material loosening in conditions, but we’re just not seeing that,” said Rubeela Farooqi, chief economist at High Frequency Economics.

The previous two months, December and January, were revised down by a combined 167,000 jobs, reflecting the higher degree of statistical volatility in the winter months. That does not disrupt a picture of consistent robust increases, which now looks slightly smoother..

At the same time, the unemployment rate, based on a survey of households, increased to a two-year high of 3.9 percent, from 3.7 percent in January. A more expansive measure of slack labor market conditions, which includes people working part time who would rather work full time, has been steadily rising and now stands at 7.3 percent.

The unemployment rate was driven by people losing or leaving jobs as well as those entering the labor force to look for work. The labor force participation rate for people in their prime working years — ages 25 to 54 — jumped back up to 83.5 percent, matching a level from last year that was the highest since the early 2000s.

Average hourly earnings rose by 4.3 percent over the year, although the pace of increases has been fading.

“We’ve recently seen gains in real wages, and that’s encouraged people to re-enter the labor market, and that’s a good development for workers,” said Kory Kantenga, a senior economist at the job search website LinkedIn. As wage growth slows, he said, the likelihood that more people will start looking for work falls.

As late as last fall, economists were predicting much more modest employment increases, with hiring concentrated in a few industries. But while some pandemic-inflated industries have shed jobs, expected downturns in sectors like construction haven’t materialized. Rising wages, attractive benefits and more flexible work schedules have drawn millions of workers off the sidelines.

Elevated levels of immigration have also added to the labor supply. According to an analysis by the Brookings Institution, the influx has approximately doubled the number of jobs that the economy could add per month in 2024 without putting upward pressure on inflation, to between 160,000 and 200,000.

Health care and government again led the payroll gains in February, while construction continued its steady increase. Retail and transportation and warehousing, which have been flat to negative in recent months, picked up.

No major industries lost a substantial number of jobs. Credit intermediation continued its downward slide — that sector, which mostly includes commercial banking, has lost about 123,000 jobs since early 2021.

That doesn’t mean the employment landscape looks rosy to everyone. Employee confidence, as measured by the company rating website Glassdoor, has been falling steadily as layoffs by tech and media companies have grabbed headlines. That’s especially true in white-collar professions like human resources and consulting, while those in professions that require working in person — such as health care, construction and manufacturing — are more upbeat.

“It is a two-track labor market,” said Aaron Terrazas, Glassdoor’s chief economist, noting that job searches are taking longer for people with graduate degrees. “For skilled workers in risk-intensive industries, anyone who’s been laid off is having a hard time finding new jobs, whereas if you’re a blue-collar or frontline service worker, it’s still competitive.”

The last few months have been studded with strong economic data, leading analysts surveyed by the National Association for Business Economics to raise their forecasts for gross domestic product and lower their expectations for the trajectory of unemployment. It’s occurred even as inflation has eased, leading the Federal Reserve to telegraph its plans for interest rate cuts sometime this year, which has raised growth expectations further.

Mervin Jebaraj, director of the Center for Business and Economic Research at the University of Arkansas, helped tabulate the survey responses. He said the mood was buoyed partly by fading trepidation over federal government shutdowns and draconian budget cuts, after several close calls since the fall. And he sees no obvious reason for the recovery to end soon.

“Once it starts going, it keeps going,” Mr. Jebaraj said. “You had this external stimulus with all the trillions of dollars of government spending, Now it’s sort of self-sustaining, even though the money’s gone.”

Layoffs are slowing at hospitals and health systems as margins gradually improve, but CFOs continue to focus on controlling costs — particularly on the labor and supply fronts — to secure the long-term sustainability of their organizations.

Last year was characterized by hospital and health systems big and small trimming their workforces due to financial and operational challenges.

From October 2022 through December 2023, Becker’sreported on more than 100 hospitals and health systems across the country that laid off workers, eliminated positions or reduced or closed certain facilities and services to help shore up finances.

While layoffs have been reported at some hospitals this year, workforce cuts have been occuring at a slower rate compared to last year.

Hospital revenues are up year over year as patient volumes continue to rebound. Operating margins have fluctuated in the last 12 months, from a -1.2% low in February 2023 to 5.5% highs in June and December, according to Kaufman Hall. In January, average operating and operating EBITDA margins dropped to 5.1%.

Kaufman analysts noted that too many hospitals are losing money and high-performing hospitals doing better and better, “effectively pulling away from the pack.”

Fitch Ratings has described 2024 as another “make or break” year for a significant portion of the nonprofit hospital sector, which continues to battle an ongoing “labordemic.” However, the U.S. has also avoided a recession so far, partly due to a robust healthcare job market, according to The Wall Street Journal.

The U.S. economy added 353,000 jobs in January, while the unemployment rate held at 3.7%, the Labor Department said Friday.

Why it matters:

The first look at the 2024 labor market shows it’s on fire — not slowing down as previously thought.

Details:

The January payroll figures show hiring picked up from the 333,000 added the prior month, which itself was revised higher by 117,000.

Job gains in November were revised slightly higher, too, by 9,000 to 182,000 jobs added.

What’s new:

The hiring boom last month came amid strong job gains in health care, retail and professional and business services, while mining and oil and gas extraction are among the sectors that shed jobs.

Meanwhile, the labor force participation rate — the share of workers with or looking for a job — was 62.5% in January.

Average hourly earnings, a measure of wage growth, soared by 0.6%. Over the past 12 month, average hourly earnings increased by 4.5%.

The big picture:

The data is the latest in recent weeks to show that the economy is revving up, with fading inflation and steady hiring — a welcome development for the Biden administration that is touting its economic agenda ahead of the 2024 election.

The intrigue:

The strong growth in both jobs and earnings will make the Federal Reserve reluctant to cut interest rates soon, out of fear that labor market strength could reverse progress on inflation.

Already this week, Fed chair Jerome Powell threw cold water on the idea of a March rate cut.

The bottom line:

Despite high profile layoffs at media and technology companies, the report shows that broader labor market is heating up.

The U.S. economy added 216,000 jobs last month while the unemployment rate held at 3.7%, the Labor Department said on Friday.

Why it matters:

The final snapshot of the 2023 labor market shows hot hiring — the latest sign that the American job market continues to defy expectations of a slowdown.

The figure is well-above the roughly 170,000 jobs economists expected.

The big picture:

The Federal Reserve has hinted it likely won’t raise interest rates again with encouraging signs that inflation is easing and the labor market is cooling.

That concludes an aggressive rate hiking cycle that began in 2022 and lasted through much of last year.

For now, however, there is little evidence those rate hikes translated into pain for workers in 2022.

American consumers, however, remain dissatisfied with the economy — a problem that may continue to weigh on the Biden White House as the 2024 election heats up.

Details:

Friday’s jobs report shows the labor market stayed strong. Hiring increased in sectors including government, health care, and construction. Transportation and warehousing shed jobs.

Average hourly earnings, a measure of wages, rose by 0.4% last month. Compared to the prior year, average hourly earnings rose 4.1%.

The share of the population with in the labor force — that is, with a job or looking for one — was 62.5% in December, roughly 0.3 percentage point less than the prior month.

The Labor Department also said the economy added a combined 71,000 fewer jobs than initially estimated in October and November.

The bottom line:

The hotter-than-expected jobs figures are one of several more key economic reports due before Federal Reserve officials meet at the end of the month.

The post-pandemic labor force has 1.5 million fewer individuals with some post-secondary education short of a bachelor’s degree. This shortfall is hitting healthcare hardest, affecting wages and qualification levels among jobholders.

Job vacancies requiring a post-secondary certificate or associate degree, particularly in healthcare, remain high. The mismatch between the supply of workers with this education level and the ongoing demand for them is leading to increased wages and greater reliance on more educated workers, according to a December 2023 bulletin from the Federal Reserve Bank of Kansas City.

Five takeaways from the bank’s report:

1. Before the pandemic, job openings across educational groups moved together and subsequently peaked together in mid-2022. Since then, while vacancies for most groups have fallen, the number of job vacancies requiring some college education remains 60% above its pre-pandemic level.

2. Vacancies for jobs requiring some college education are concentrated in healthcare. As of August 2023, about 50% of all open jobs posted in 2023 that required an associate degree or non-degree certificate were in healthcare.

3. As a result of the high demand, healthcare employers are turning to more educated workers to fill positions with requirements for some college education. Healthcare employment among workers with some college education has dropped by about 400,000 since 2019; healthcare employment among workers with a bachelor’s degree or more has increased by 600,000.

4. Combined, these factors can place upward pressure on healthcare wages. The supply-demand mismatch can lead employers to offer higher wages to competitively attract qualified workers. Employers turning to workers with more education, who are generally more expensive, will increase the average wage in these occupations.

5. From 2019 to 2023, overall wages for healthcare workers rose by nearly 25%, an increase the bank partially attributes to both increased wages within educational groups and composition effects. The shift in employment toward higher-educated workers accounts for an additional 2.7 percentage points of the total wage increase, for instance.