Cartoon – Going the Extra Mile

https://gisthealthcare.com/weekly-gist/

When Presbyterian Health System struck a deal with Intel to manage care for the firm’s Albuquerque employees, followed by Providence Health & Service’s ACO-like contract to provide care to Boeing employees in Seattle, we became optimistic about the potential of direct contracting between health systems and large employers.

But five years after those landmark deals, we were still just talking about Boeing and Intel. Few other employers followed suit, instead preferring to control spend by shifting more of the cost of coverage onto their employees in the form of higher deductibles, larger co-pays, and greater co-insurance.

In 2018 the average family deductible in employer-sponsored insurance hit $3,000, and in most markets deductibles of $5,000 or higher are not uncommon. Our recent conversations with employers suggest that they are now questioning the utility of shifting more costs onto employees. As deductibles rise, employers see diminishing returns. In contrast to instituting the first $1,000 deductible, moving an already high deductible from $3,000 to $4,000 does little to change employee behavior. And employers are genuinely worried about the impact of rising cost sharing on their employee’s financial and physical health.

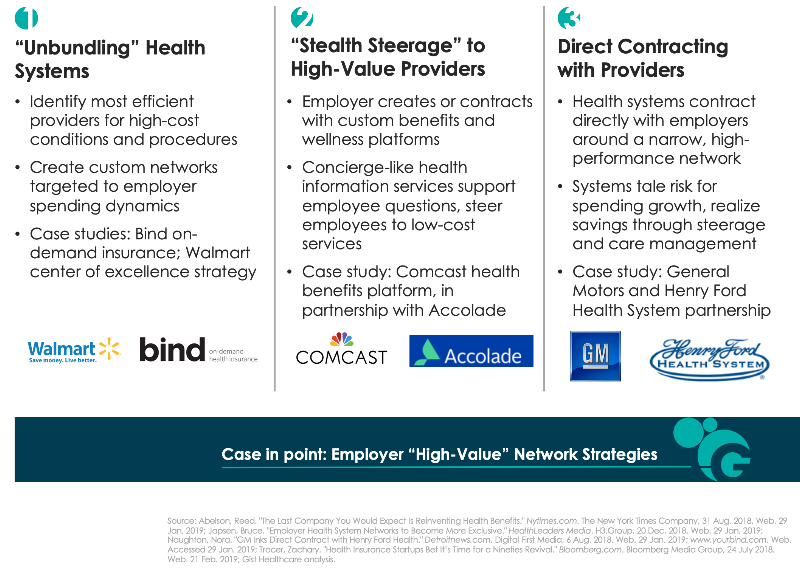

Given the historically strong labor market, employers have been reticent to change benefit design in any way that could be perceived as narrowing choice. But the reluctance to push cost sharing further creates an opening for providers and innovators that offer alternative solutions to encourage employees to choose a “high-performance network”—the new term of art for a narrow network.

Across the past year we’ve seen a range of strategies to create high-performance networks, described in the graphic below. The pace of direct contracting between health systems and employers has quickened. But other solutions challenge the premise that a single health system provides the best solution for every high-cost condition or procedure. Start-up insurer Bind aims to create bespoke networks for high-cost procedures by identifying the best doctors and hospitals regardless of affiliation, essentially “unbundling” the health system. Others, like health benefits solution provider Accolade, create a concierge-like service to support employee decision-making—while preferentially steering them to lower-cost providers.

It remains to be seen which of these solutions will produce the greatest returns, and whether the gains can be sustained over time. However, we wonder whether companies will really have the fortitude to engage employees in conversations about narrower networks. Many will likely prefer to shift the task of narrowing networks onto employees themselves; we still believe that defined contribution health benefits will be the ultimate solution for employers to manage spend. It’s likely employers will require the cover of a recession to make this dramatic switch in benefit design. In the interim, there seems to be a window of opportunity for high-performance network assemblers to demonstrate that they can be an attractive and effective solution to rising costs.

https://gisthealthcare.com/weekly-gist/

Here’s a question we get all the time, and one that I heard again this week from one of our partner health systems: “We’re working on [initiative X]. What have other health systems like us done about that?” We hear it in any number of situations, from hospitals developing clinical protocols to strategic planners putting together business plans for service line growth. Sometimes the question comes in different forms: “Do you have a white paper on [topic X]?”; or “What research do you have on [issue X]?”; or our favorite, “What’s the best practice for [activity X]?”

It’s not surprising, given our past history, that we’d frequently be asked to provide research or best practice information. But as we’ve grown our own business at Gist Healthcare and developed our own independent perspective on where our industry needs to go, we’ve become less and less impressed by “best practice” as a concept. In fact, I’d go so far as to say that “best practice” has become at best a crutch, and in many cases a hindrance, to real progress in healthcare. As we sometimes tell our clients now, healthcare has outgrown “best practice”, at least as we used to understand it.

Don’t get me wrong. Medicine should absolutely be evidence-driven, and clinical care should always be firmly grounded in proven practice. If anything, the actual clinical practice of medicine is one area where our industry must become more, not less, best-practice based.

But as to system strategy, payment innovation, service improvement, and a host of other business and operational issues, simply imitating what other “successful” organizations are doing leads inevitably to reversion to the mean, groupthink, and (most troubling) fad-driven “bubbles” of activity. It’s no surprise, given the pervasive culture of “best practice”, when suddenly every health system’s top priority turns to creating a patient portal, or hiring a chief experience officer, or starting a proton beam center, or opening freestanding EDs.

Healthcare delivery is a highly fragmented, insular business, with little visibility across markets and across institutions. That makes it very susceptible to white paper-driven trend chasing, which tends to outsource innovation to the “wisdom of the crowd”.

It’s pretty rare to find mavericks, following their own innovation instincts without getting caught up in trying to mimic what other “leaders” are doing. That’s why when a delivery organization takes a risk on a truly new strategic innovation—Geisinger’s money-back guarantee, Cleveland Clinic’s promise of same-day access, Presbyterian’s direct contract to manage Intel employees’ health—it immediately sends shock waves across the industry.

Those ideas didn’t come from a white paper. We’re often asked whether we’re building a “best-practice research” capability in our new company. While we’re not quite ready to talk about our upcoming service offerings, the answer to that question is a definitive “no”.

https://gisthealthcare.com/weekly-gist/

Earlier this month I was at a health system board meeting in which we were discussing the transition from volume to value, and the shift to a population health model. One board member had the courage to ask a tough question: “What if we never get there?” Covering just a small slice of a large metropolitan area, this system has consistently ranked third in market share behind two larger competitors—and now they feel they are lagging those systems in moving toward risk. The most recent challenge: a large—and until recently, loyal—independent primary care group had just been acquired by one of their competitors. Yet the system prides itself, justifiably, on delivering low-cost hospital care and outstanding quality.

I raised a heretical notion: suppose the system pursued a strategy focused solely on being the highest-performing inpatient and specialty care provider in the market, and abandoned the goal of bearing population risk? Could the system shift their focus to simply being the best “subcontractor” to other risk-bearing networks in the market?

The ensuing conversation was uncomfortable, to say the least. The notion challenged the system’s assumptions of the role they wanted to play in the market, and whether they could be a leader in population health. I encouraged them to think of being a “subcontractor” to other risk-bearing organizations not as a defeat, but as fulfillment of a vital role—healthcare in their community would be better if more hospital care were delivered at their level of cost and quality.

Our view: for many smaller systems who are driven by a desire to remain independent, becoming a high-performing care subcontractor may be the best path forward, and the most realistic. (It will be interesting to watch the successful investor-owned chains on this front—organizations whose strategic advantage lies in running highly-efficient, low-cost hospitals.) It’s not as sexy as “population health”, but as any builder will tell you, there’s no substitute for a great subcontractor.

Oakland, Calif.-based Kaiser Permanente announced its intent Feb. 19 to waive all four years of tuition for the first five classes of students admitted to its new medical school.

Kaiser officials said in a news release obtained by Becker’s Hospital Review that its medical school has received preliminary accreditation from the Liaison Committee on Medical Education and will begin accepting applications from prospective students in June 2019 for its inaugural class in summer 2020. Each class will contain roughly 48 students, according to The New York Times.

Mark Schuster, MD, PhD, founding dean and CEO of the Pasadena, Calif.-based Kaiser Permanente School of Medicine, told The New York Times that while the institution only plans to cover the entire $55,000-per-year tuition for all of its first five classes of students, Kaiser will offer “very generous financial aid” based on need for future students.

Kaiser is the second institution to announce that it will waive tuition for students. Last August, the New York City-based NYU School of Medicine declared plans to cover its entire tuition costs for all students, which equates to more than 400 students across classes.

While NYU raised $600 million from donors to pay for its tuition plan, Kaiser is using a portion of its revenue set aside for “community benefits,” which all nonprofit hospitals have to provide to maintain their tax-exempt status, according to The New York Times. The health system, which has an operating revenue of nearly $73 billion, spent $2.3 billion on community benefits in 2017, including charity care for the uninsured and community health spending.

The medical school will be one of the only medical schools in the U.S. to be affiliated with a hospital or health system, not a university, The New York Times reports. Its curriculum will include a focus on small-group, case-based learning, and students will travel to the health system’s hospitals and clinics in the greater Los Angeles area for their clinical education.

“We’ve had the opportunity to build a medical school from the ground up and have drawn from evidence-based educational approaches to develop a state-of-the-art school on the forefront of medical education, committed to preparing students to provide outstanding patient care in our nation’s complex and evolving healthcare system,” said Dr. Schuster said in a news release.

In December, Kaiser added 11 executives to the medical school’s leadership team.

To access the full report, click here.

Walmart is offering employees a 90 percent discount on telemedicine, dropping the price of a virtual visit from $40 to $4, The Denver Post reports.

The retailer reduced the cost of telemedicine services Jan. 1 to increase options for employees seeking care, a spokesperson confirmed to Becker’s Hospital Review. Walmart’s health benefits currently cover more than 1 million people enrolled it its Associates’ Medical Plan. Through this plan, virtual visits through the Doctor On Demand app are covered like a normal physician’s office visit.

Walmart is one of many employers to offer telemedicine benefits to workers. Eighty percent of large and midsize companies offered the benefit in 2018, according to the report. However, factors like emotion, forgetfulness and preference have kept utilization down. Just 8 percent of employees at large and midsize companies used telemedicine benefits in 2017, according to the report.

Read more here.