Regular readers of HEALTH CARE un-covered know that I write frequently about the huge amounts of money the health insurance industry’s pharmacy benefit managers (PBMs) extract from the prescription drug supply chain. I also submitted a comment letter to the Federal Trade Commission two and a half years ago urging it to launch an investigation into PBM business practices that have contributed to the closure of hundreds of independent pharmacies across the country and to millions of Americans walking away from the pharmacy counter without their medications.

On a bipartisan basis, the FTC did launch an inquiry into the PBM business, and today the Commission issued a damning interim report that confirmed what industry critics, including me, have been saying:

Just six companies now control 95% of the pharmacy benefit market, and these Big Insurance-owned middlemen “profit at the expense of patients by inflating drug costs and squeezing Main Street pharmacies.” Below you’ll find the commission’s statement on its preliminary findings.

Last year, we also published a profile of one of the industry’s most vocal critics in Congress, Rep. Earl L. “Buddy” Carter (R-Ga.), a pharmacist by trade who has seen PBM’s profiteering firsthand. In a press release this morning, Carter said:

Since day one in Congress, I’ve been calling on the FTC to investigate PBMs, which use deceptive and anti-competitive practices to line their own pockets while reducing patients’ access to affordable, quality health care. I’m proud that the FTC launched a bipartisan investigation into these shadowy middlemen, and its preliminary findings prove yet again that it’s time to bust up the PBM monopoly. We are losing more than one pharmacy per day in this country, causing pharmacy deserts and taking the most accessible health care professionals in America out of people’s communities. I am calling on the FTC to promptly complete its investigation and begin enforcement actions if – and when – it uncovers illegal and anti-competitive PBM practices.

Carter and several other members of Congress have introduced bipartisan bills to rein in PBMs. The House has passed PBM reform legislation but the Senate has not yet done so, but there is growing support in both chambers to enact one or more bills by the end of the year. The FTC’s interim report should make that more likely to happen.

Read the FTC’s full press release below:

FTC Releases Interim Staff Report on Prescription Drug Middlemen

Report details how prescription drug middleman profit at the expense of patients by inflating drug costs and squeezing Main Street pharmacies

The Federal Trade Commission today published an interim report on the prescription drug middleman industry that underscores the impact pharmacy benefit managers (PBMs) have on the accessibility and affordability of prescription drugs.

The interim staff report, which is part of an ongoing inquiry launched in 2022 by the FTC, details how increasing vertical integration and concentration has enabled the six largest PBMs to manage nearly 95 percent of all prescriptions filled in the United States.

This vertically integrated and concentrated market structure has allowed PBMs to profit at the expense of patients and independent pharmacists, the report details.

“The FTC’s interim report lays out how dominant pharmacy benefit managers can hike the cost of drugs—including overcharging patients for cancer drugs,” said FTC Chair Lina M. Khan. “The report also details how PBMs can squeeze independent pharmacies that many Americans—especially those in rural communities—depend on for essential care. The FTC will continue to use all our tools and authorities to scrutinize dominant players across healthcare markets and ensure that Americans can access affordable healthcare.”

The report finds that PBMs wield enormous power over patients’ ability to access and afford their prescription drugs, allowing PBMs to significantly influence what drugs are available and at what price. This can have dire consequences, with nearly 30 percent of Americans surveyed reporting rationing or even skipping doses of their prescribed medicines due to high costs, the report states.

The interim report also finds that PBMs hold substantial influence over independent pharmacies by imposing unfair, arbitrary, and harmful contractual terms that can impact independent pharmacies’ ability to stay in business and serve their communities.

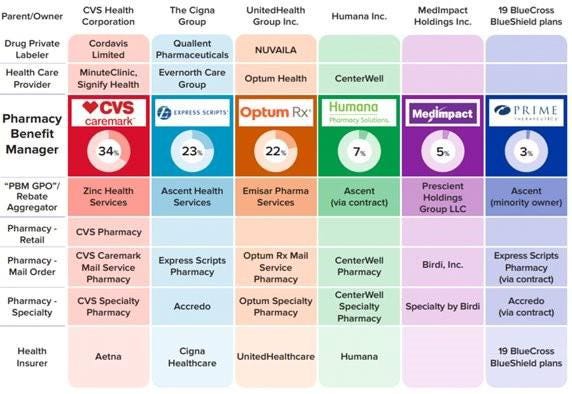

The Commission’s interim report stems from special orders the FTC issued in 2022, under Section 6(b) of the FTC Act, to the six largest PBMs—Caremark Rx, LLC; Express Scripts, Inc.; OptumRx, Inc.; Humana Pharmacy Solutions, Inc.; Prime Therapeutics LLC; and MedImpact Healthcare Systems, Inc. In 2023, the FTC issued additional orders to Zinc Health Services, LLC, Ascent Health Services, LLC, and Emisar Pharma Services LLC, which are each rebate aggregating entities, also known as “group purchasing organizations,” that negotiate drug rebates on behalf of PBMs.

PBMs are part of complex vertically integrated health care conglomerates, and the PBM industry is highly concentrated. As shown in the below image, this concentration and integration gives them significant power over the pharmaceutical supply chain. The percentages reflect the amount of prescriptions filled in the United States.

The interim report highlights several key insights gathered from documents and data obtained from the FTC’s orders, as well as from publicly available information:

Concentration and vertical integration: The market for pharmacy benefit management services has become highly concentrated, and the largest PBMs are now also vertically integrated with the nation’s largest health insurers and specialty and retail pharmacies.

The top three PBMs processed nearly 80 percent of the approximately 6.6 billion prescriptions dispensed by U.S. pharmacies in 2023, while the top six PBMs processed more than 90 percent.

Pharmacies affiliated with the three largest PBMs now account for nearly 70 percent of all specialty drug revenue.

Significant power and influence: As a result of this high degree of consolidation and vertical integration, the leading PBMs now exercise significant power over Americans’ ability to access and afford their prescription drugs.

The largest PBMs often exercise significant control over what drugs are available and at what price, and which pharmacies patients can use to access their prescribed medications.

PBMs oversee these critical decisions about access to and affordability of life-saving medications, without transparency or accountability to the public.

Self-preferencing: Vertically integrated PBMs appear to have the ability and incentive to prefer their own affiliated businesses, creating conflicts of interest that can disadvantage unaffiliated pharmacies and increase prescription drug costs.

PBMs may be steering patients to their affiliated pharmacies and away from smaller, independent pharmacies.

These practices have allowed pharmacies affiliated with the three largest PBMs to retain high levels of dispensing revenue in excess of their estimated drug acquisition costs, including nearly $1.6 billion in excess revenue on just two cancer drugs in under three years.

Unfair contract terms: Evidence suggests that increased concentration gives the leading PBMs leverage to enter contractual relationships that disadvantage smaller, unaffiliated pharmacies.

The rates in PBM contracts with independent pharmacies often do not clearly reflect the ultimate total payment amounts, making it difficult or impossible for pharmacists to ascertain how much they will be compensated.

Efforts to limit access to low-cost competitors: PBMs and brand drug manufacturers negotiate prescription drug rebates some of which are expressly conditioned on limiting access to potentially lower-cost generic and biosimilar competitors.

Evidence suggests that PBMs and brand pharmaceutical manufacturers sometimes enter agreements to exclude lower-cost competitor drugs from the PBM’s formulary in exchange for increased rebates from manufacturers.

The report notes that several of the PBMs that were issued orders have not been forthcoming and timely in their responses, and they still have not completed their required submissions, which has hindered the Commission’s ability to perform its statutory mission. FTC staff have demanded that the companies finalize their productions required by the 6(b) orders promptly. If, however, any of the companies fail to fully comply with the 6(b) orders or engage in further delay tactics, the FTC can take them to district court to compel compliance.

The FTC remains committed to providing timely updates as the Commission receives and reviews additional information.

The Commission voted 4-1 to allow staff to issue the interim report, with Commissioner Melissa Holyoak voting no. Chair Lina M. Khan issued a statement joined by Commissioners Rebecca Kelly Slaughter and Alvaro Bedoya. Commissioners Andrew N. Ferguson and Melissa Holyoak each issued separate statements. The Federal Trade Commission develops policy initiatives on issues that affect competition, consumers, and the U.S. economy. The FTC will never demand money, make threats, tell you to transfer money, or promise you a prize. Follow the FTC on social media, read consumer alerts and the business blog, and sign up to get the latest FTC news and alerts.

Medicare Advantage plans received $50 billion in payments between 2018 and 2021 for diagnoses insurers added to medical records, a Wall Street Journal investigation published July 8 has found.

The Journal investigated billions of Medicare Advantage records and found that some conditions were diagnosed at a much higher rate among Medicare Advantage beneficiaries than among traditional Medicare beneficiaries. For example, diabetic cataracts were diagnosed much more often among Medicare Advantage beneficiaries than among traditional Medicare beneficiaries, the Journal found.

The federal government pays Medicare Advantage plans a rate per beneficiary based on their diagnoses.

CMS does not reimburse MA plans for beneficiaries with non-diabetic cataracts, a common condition among older adults, according to the Journal. The government does reimburse for diabetic cataracts. CMS paid Medicare Advantage plans more than $700 million for diabetic cataracts diagnoses between 2018 and 2021, the investigation found.

A spokesperson for UnitedHealth, the largest Medicare Advantage insurer, told the Journal its analysis was “inaccurate and biased.” Medicare Advantage plans code diagnoses more completely and ensure diseases are caught earlier, the spokesperson told the outlet.

The Journal’s investigation also found some Medicare Advantage beneficiaries were diagnosed with serious diseases in their medical records, but no evidence of treatment for the disease appeared in these patients’ records. Among beneficiaries who had a diagnosis of HIV added to their record by their insurer, just 17% received treatment for the disease, according to the investigation. Among beneficiaries who were diagnosed with HIV by their physician, 92% received treatment.

The Journal’s investigation is the latest examining upcoding by MA plans. A 2022 report in The New York Times alleged some insurers incentivized employees or physicians to add diagnoses to patients’ reports. Nearly every major payer has been accused of overbilling by a whistleblower, the federal government or an investigation by HHS’ Office of Inspector General.

MedPAC, which advises the government on Medicare issues, estimates the federal government will spend $83 billion more on Medicare Advantage beneficiaries than if they were enrolled in fee-for-service Medicare. Coding intensity in MA will be 20% higher than in fee-for-service in 2024, according to the commission.

UnitedHealth Group’s Optum, the largest employer of physicians in the U.S., is expanding its reach in behavioral health.

The company added 45,000 therapists, psychiatrists and behavioral health providers to its network in 2023, and it has more than 430,000 behavioral health clinicians in its network overall.

Here are five things to know about Optum’s behavioral health offerings:

The company is acquiring behavioral health clinics. Optum recently picked up Care Counseling, which employs more than 200 clinicians at 10 clinics in the Minneapolis area. In 2022, Optum acquired Refresh Mental Health, which operates more than 300 outpatient sites in 37 states.

Optum’s acquisitions of behavioral health providers have helped cut wait times for patients, Optum CEO Heather Cianfrocco said in May.

“On average it takes over 50 to 60 days to get an appointment for high-quality behavioral care,” she said. “We started acquiring our own behavioral providers to be able to reduce that access issue.”

The company is also targeting in-home behavioral care. In December 2023, Amar Desai, MD, CEO of Optum Health, said the company had integrated behavioral care into its home health offerings.

“As a practicing physician, I am particularly excited that we are becoming the practice and partner of choice in the marketplace,” Dr. Desai said of the business.

Optum also administers behavioral health benefits systems for states, though it recently lost contracts to manage programs in Maryland and Idaho.

OptumRx, a pharmaceutical benefit manager, provides medication management for behavioral health, substance use disorder and other complex drugs for more than 1 million people each year.

The entities agreed to maintain services, provide capital investments and protect competition in the healthcare market.

California Attorney General Rob Bonta announced a settlement agreement this week reached by The Regents of the University of California and UCSF Health regarding their $100 million purchase of Dignity Health’s two San Francisco hospitals, St. Mary’s Medical Center (SMMC) and Saint Francis Memorial Hospital (SFMH).

Dignity Health is a nonprofit public benefit corporation that owns and operates SFMH, a 259-licensed-bed general acute care hospital, and SMMC, a 240-licensed-bed general acute care hospital. Both hospitals serve a diverse community, including a large number of elderly, unhoused and publicly insured patients who may rely on Medi-Cal, Medicare or charity care to access essential health services.

Under the settlement agreement approved by the San Francisco Superior Court, The Regents and UCSF Health commit to maintain services for the unhoused and Medi-Cal and Medicare beneficiaries, provide $430 million in capital investments, protect competition in the healthcare market and safeguard the affordability of and access to services for residents of San Francisco.

WHAT’S THE IMPACT

The Regents and UCSF Health agreed to a number of conditions over the next 10 years, including operating and maintaining SFMH and SMMC as licensed general acute care hospitals with the same types and levels of services, and associated staffing. They also agreed to continue participating in Medi-Cal and Medicare.

Also agreed upon was providing an annual amount of charity care at SFMH equal to or greater than $6.5 million and at SMMC equal to or greater than $3.5 million, with an annual increase of 2.4% at both hospitals.

The two entities agreed to provide an annual amount of community benefit spending for community healthcare needs at SFMH equal to or greater than $1.6 million and at SMMC equal to or greater than $10.7 million, to increase yearly by 2.4% at both hospitals.

UCSF Health and The Regents also pledged to invest at least $430 million, including at least $80 million for electronic medical record systems and related technologies, and at least $350 million in deferred maintenance and physical infrastructure improvements at both hospitals.

In addition to those agreements, they also agreed to a number of conditions over a seven-year period meant to maintain competition in the healthcare market, in part by maintaining contracts with the City and County of San Francisco for services at SFMH and SMMC unless terminated for cause.

The Regents and UCSF Health agreed to not condition medical staff privileges or contracts on the employment, contracting, affiliation, or appointment status of a physician with UCSF Health or any affiliate; not impose any requirement on any member of the hospitals’ medical staff, as a condition of either their medical staff membership or privileges that restricts them from contracting with providers other than UC Health; and negotiate all payer contracts for the hospitals separately and independently from payer contracts for UCSF Health, and maintain an information firewall between the two negotiating teams.

Finally, the two entities agreed to require, for five years, a price growth cap that limits the maximum that the hospitals may charge a payer from year to year upon renegotiation of contracts.

THE LARGER TREND

Mergers and acquisitions are expected to rebound this year after M&A activity fell to its lowest level in 10 years globally in 2023, according to Reuters.

Deal making last year was weighed down by high interest rates, economic uncertainty and a regulatory scrutiny, with all but the last factor slowly abating for renewed confidence.

Health systems put an emphasis on strategy over scale in hospital transactions announced in the second quarter of 2024, according to a July 9 report from Kaufman Hall.

“As pressure intensifies to transform the current healthcare system to bring greater value to patients and communities, the impetus for M&A activity will rely less on seeking capital in traditional ways and instead move toward new, strategic partnership models,” Anu Singh, managing director and mergers & acquisitions practice leader with Kaufman Hall, said in a July 9 news release. “Many of these M&A transactions enable hospitals to sustain and enhance access to care, launch new services, or strengthen and stabilize systems, which allows for future growth.”

Five things to know:

1. There were 11 hospital transactions announced in the second quarter of 2024, below historic Q2 averages. There were 20 hospital transactions announced in the second quarter of 2023.

2. Despite fewer overall deals, total transacted revenue in the quarter remained near historic highs at $10.8 billion.

3. Three of the 11 announced transactions involved religiously affiliated acquirers. Two involved academic or university-affiliated acquirers. The other six involved not-for-profit health system acquirers.

4. For the first time since Kaufman Hall tracked this data, there were no for-profit health system acquirers in the quarter. Kaufman Hall said in the report that this continues a trend of low for-profit buy-side activity. In the first quarter of 2024, just one of the 20 announced transactions involved a for-profit acquirer.

5. The emphasis on strategy over scale “characterized the most significant transactions of Q2 2024 and built upon trends we have been commenting on in recent past reports,” Kaufman Hall said.

Those trends are:

Pursuit of intellectual capital and new or complementary capabilities through a strategic partnership, often involving an innovative partnership model.

Focus of large regional or national systems on market reorganization and strategic realignment of their system portfolios.

The development of networks involving academic health systems and community hospital partners to sustain and enhance access to care.

Congress returns from its July 4 break today and its focus will be on the President: will he resign or tough it out through the election in 120 days. But not everyone is paying attention to this DC drama.

In fact, most are disgusted with the performance of the political system and looking for something better. Per Gallup, trust and confidence in the U.S. Congress is at an all-time low.

The same is true of the healthcare system:

69% think it’s fundamentally flawed and in need of systemic change vs. 7% who think otherwise (Keckley Poll). And 60% think it puts its profits above all else, laying the blame at all its major players—hospitals, insurers, physician, drug companies and their army of advisors and suppliers.

These feelings are strongly shared by its workforce, especially the caregivers and support personnel who service patient in hospital, clinic and long-term care facilities. Their ranks are growing, but their morale is sinking.

Career satisfaction among clinical professionals (nurses, physicians, dentists, counselors) is at all time low and burnout is at an all-time high.

Last Friday, the Bureau of Labor issued its June 2024 Jobs report. To no one’s surprise, job growth was steady (+206,000 for the month) –slightly ahead of its 3-month average (177,000) despite a stubborn inflation rate that’s hovered around 3.3% for 15 months. Healthcare providers accounted for 49,000 of those jobs–the biggest non-government industry employer.

But buried in the detail is a troubling finding: for hospital employment (NAICS 6221.3): productivity was up 5.9%, unit labor costs for the month were down 1.1% and hourly wages grew 4.8%–higher than other healthcare sectors.

For the 4.7 million rank and file directly employed in U.S. hospitals, these productivity gains are interpreted as harder work for less pay. Their wages have not kept pace with their performance improvements while executive pay seems unbridled.

Next weekend, the American Hospital Association will host its annual Leadership Summit in San Diego: 8 themes are its focus:

Building a More Flexible and Sustainable Workforce is among them. That’s appropriate and it’s urgent.

An optimistic view is that emergent technologies and AI will de-lever hospitals from their unmanageable labor cost spiral. Chief Human Resource Officers doubt it. Energizing and incentivizing technology-enabled self-care, expanding scope of practice opportunities for mid-level professionals and moving services out of hospitals are acknowledged keys, but guilds that protect licensing and professional training push back.

By contrast, the application of artificial intelligence to routine administrative tasks is more promising: reducing indirect costs (overhead) that accounts for a third of total spending is the biggest near-term opportunity and a welcome focus to payers and consumers.

Thus, most organizations advance workforce changes cautiously. That’s the first problem.

The second problem is this:

lack of a national healthcare workforce modernization strategy to secure, prepare and equip the health system to effectively perform. Section V of the Affordable Care Act (March 2010) authorized a national workforce commission to modernize the caregiver workforce. Due to funding, it was never implemented. It’s needed today more than ever. The roles of incentives, technologies, AI, data and clinical performance measurement were not considered in the workforce’ ACA charter: Today, they’re vital.

Transformational changes in how the healthcare workforce is composed, evaluated and funded needs fresh thinking and boldness. It must include input from new players and disavow sacred cows. It includes each organization’s stewardship and a national spotlight on modernization.

It’s easier to talk about healthcare’s workforce issues but It’s harder to fix them. That’s why incrementalism is the rule and transformational change just noise.

PS: In doing research for this report, I found wide variance in definitions and counts for the workforce. It may be as high as 24 million, and that does not include millions of unpaid caregivers. All the more reason to urgently address its modernization.

In 126 days, U.S. voters will settle Campaign 2024 choosing the winners for 435 House seats, 34 Senate seats, 13 Governors and the White House. When final votes are counted, the last week of June, 2024 will be seen as the tipping point when much about politics and policy was re-set as the result of two events:

1-The ‘Great Debate’:

Thursday’s standoff between President Biden and former President Trump drew 51.3 million viewers across 17 networks that carried it. That’s well below previous head-to-head debate match-ups i.e. 84 million for Clinton-Trump in 2016, 73 million for Trump and Biden in 2020. Perhaps more telling, only 3.9 million of these were adults 18-34– 7.6% of debate viewers but 22.9% of U.S. population.

While pundits debated the fitness of the President to continue and speculated about alternative candidates over the weekend, the majority of Americans paid no attention—especially young adults. They think both candidates are old.

In 2020, 57% of 18–34-year-olds voted for a Presidential candidate vs. 69% of 35–64-year-olds and 74% of voters 65+.

Polls show young adults think the political system is fundamentally flawed and partisanship harmful to policies that advance the well-being of the population. They also show their declining trust and confidence in America’s institutions—the press, big business, Congress, organized religion and the medical system.

Young adults get their information from social media and friends and they’re tuning out spin in politics.

2-Supreme Court decisions impacting healthcare:

As is customary for the high court, many of its rulings are handed down in the last week of June before it adjourns for the summer. Only one case remains in limbo: Presidential immunity with a decision expected today. Of the 61 cases SCOTUS has heard in its 2023-2024 term, these four decisions are the most significant to the health industry:

Power of federal agencies (Loper Bright Enterprises v. Raimondo and Relentless, Inc. v. Dept. of Commerce): By a vote of 6-3, SCOTUS ruled that judges no longer have to defer to agency officials when interpreting ambiguous federal statutes about the environment, the workplace, public health and other aspects of American life overturning a 40-year-old legal precedent known as “Chevron deference.” The court’s decision will significantly curtail the power federal agencies have to regulatethousands of private companies, products, industries and the environment.

Emergency room abortions (Idaho v. U.S): SCOTUS ruled 6-3 that hospitals in Idaho that receive federal fundsmust allow emergency abortion care to stabilize patients — even though the state strictly bans the procedure.

Opioid lawsuit settlement (Harrington v. Purdue Pharma): By a vote of 5-4, the justices blocked a controversialPurdue Pharma bankruptcy plan that would have provided billions of dollars to address the nation’s opioid crisis in exchange for protecting the family that owns the company from future lawsuits. The majority found that the plan was invalid because all the affected parties had not been consulted on the deal

Abortion medication restrictions (FDA v. Alliance for Hippocratic Medicine): By a vote of 9-0, the justices maintained broad access to mifepristone, unanimously reversing a lower court decision that would have made the widely used abortion medication more difficult to obtain. The decision was not on the substance of the case, but a procedural ruling that the challengers did not have legal grounds to bring their lawsuit.

Based on these events last week, healthcare organizations and their trade groups making plans for 2025 and beyond should consider:

Young adults. Out of Sight, Out of Mind: Polling data shows young adults think the health system is broken and alternatives worth considering. Affordability, equitable access and price transparency matter to them. Their finances are stretched as inflation (housing, energy, food et al), their medical debt prevalent and mounting and their employers are cutting their health benefits and forcing them to assume more out-of-pocket responsibility. Hospitals, insurers, physicians and drug companies pay close attention to older working age consumers and seniors. They pay little attention to younger adults, and the reverse is true. But history teaches that social movements originate from disenchanted youth and young adults who feel taken for granted, abused by corporate greed and unheard. Might the healthcare status quo be a target?

The federal administrative state in flux: The ripple effect of the court’s Chevron decision is equivalent to its decision ending Roe v. Wade (June 2022). The latitude afforded key federal agencies i.e. CDC, CMS, OSHA, CMMI, FDA, HRSA et al will be revisited. States will be forced to step in where federal guidance is in jeopardy. Governors and the White House will face more frequent court challenges on their Executive Orders and agencies for their Administrative Actions as government oversight of healthcare evolves. For investors, safe bets will be targets. For hospitals, insurers and physicians, federal advocacy will require recalibration.

The administrative state flux means state legislatures and ballot referenda will play a bigger role in healthcare. States already have enormous responsibilities for healthcare:

Medicaid coverage determination

Retail Health i.e. services (efficacy), truth in advertising, consumer safety et al

Public health services i.e. STDs, disease surveillance, immunization policies et al.

Prescription Drug Affordability (in 11 states)

Health Insurance Marketplaces

Healthcare workforce scope of practice

Medical Malpractice and consumer protections

Abortion Rights: as a result of the 2022 Supreme Court ruling that Roe v. Wade

Behavioral health, substance abuse workforce adequacy, licensure, scope of practice et al.

Certificate of Need Programs

Use Medical Marijuana (Cannabis) for Therapeutics and/or Recreational Use.

Health Insurer Licensing, Network adequacy and Liquidity

Quality and patient safety inspection in post-acute & home-based settings.

Workers’ compensation eligibility, administration use and funding.

Formulary design and expense control.

School clinics

Prison health

And others

The court decisions last week open the door to additional actions by state agencies and elected officials in areas where federal policies are in limbo:

Tax exemptions for not-for-profit health systems

Hospital consolidation and price transparency,

Accessibility of hospital emergency services for abortion,

Insurer prior authorization and network adequacy

Minimum staffing requirements,

Telehealth use and payment

Restrictive drug formulary

And more.

For every healthcare organization and trade group, vigilance about pending legislation/action at the state level will take on added importance.

The U.S. health system’s future is not a repeat of its past: The week’s events lend to the health industry’s uncertain future. Today, strategic planning in most U.S. healthcare organizations i.e. insurers, hospitals, physician organization, device and drug manufacturers, et al is based on incremental changes forecast 3-5 years out. While consideration is given “transformational” changes 10-15 years out, it is under-studied by planners and rarely included on board agenda dockets. Yet, signal detection of disruptive shifts in financial services, higher education and other industries predict winners and losers. The U.S. system is change-averse because it benefits its self-interests. Outsiders do not share this view. No trade group or organization in healthcare can afford to bet its future on incrementalism in healthcare. These court decisions and the pending election results suggest that healthcare’s future is not a repeat of its past: new rules, new players and new critical success factors are inevitable.

It was a big week for U.S. politics and perhaps a bigger week for healthcare. Stay tuned.

A health system CEO recently reached out to me with a specific complaint that’s become a hot-button issue for an increasing number of systems:

“Medicare Advantage (MA) is no longer a good payer for us. When you factor in all the pre-auths and denials, we’re now getting four points less yield from our MA patients than from our traditional Medicare patients.

But our market is swinging hard toward MA, and I know the program’s not going anywhere…so how can we rethink our MA business model to make it more profitable?

After more than a decade of rapid growth, MA plans are now running into headwinds that are reducing their margins and creating an even more contentious negotiating environment with providers. However, these heightened competitive pressures could also be seen as an opportunity for provider organizations.

Rather than treating all of their MA payers as a monolith, a health system or other larger provider organization should be reassessing its MA book of business with the goal of identifying priority MA payers with which to pursue deeper, mutually beneficial partnerships.

The first step here is usually for a system to undergo a holistic tiering or ranking exercise for all of their MA payers according to factors like market share, contribution margin, value-based incentives, overall relationship dynamic, and projected market growth.

This exercise will identify not only which MA payers may not be high-priority, long-term partners, but also which MA payers are suitable for developing deeper relationships with (e.g., simplifying administrative burden, better rewards for value-based care, creating a joint insurance product).

If your system is facing challenges with MA and is interested in rethinking its MA portfolio strategy, please don’t hesitate to reach out.

Last Friday, Greensboro, NC-based Cone Health announced that it signed a definitive agreement to join Risant Health, Kaiser Permanente’s not-for-profit subsidiary.

Launched in April 2023, Risant aims to acquire and support not-for-profit health systems focused on value-based care.

If the deal is approved by regulators, Cone Health, a $2.8B not-for-profit system with five hospitals and an insurance arm, would join Danville, PA-based Geisinger as Risant’s second member.

As part of the deal, Risant will invest an undisclosed sum into Cone, but Cone will continue to operate independently, retaining its branding, leadership, and ability to work with multiple insurers. The two parties expect to close the deal in the next six months.

The Gist: Like Geisinger, Cone has a strong track record of value-based care, including a 15K-member health plan and a high-performing accountable care organization.

Neither Risant nor Kaiser has operations in North Carolina, a state currently seeing strong population growth.

Risant has previously said that is looking to acquire four or five more systems in addition to Geisinger, in order to reach a combined revenue target of $30-35B over the next five years.

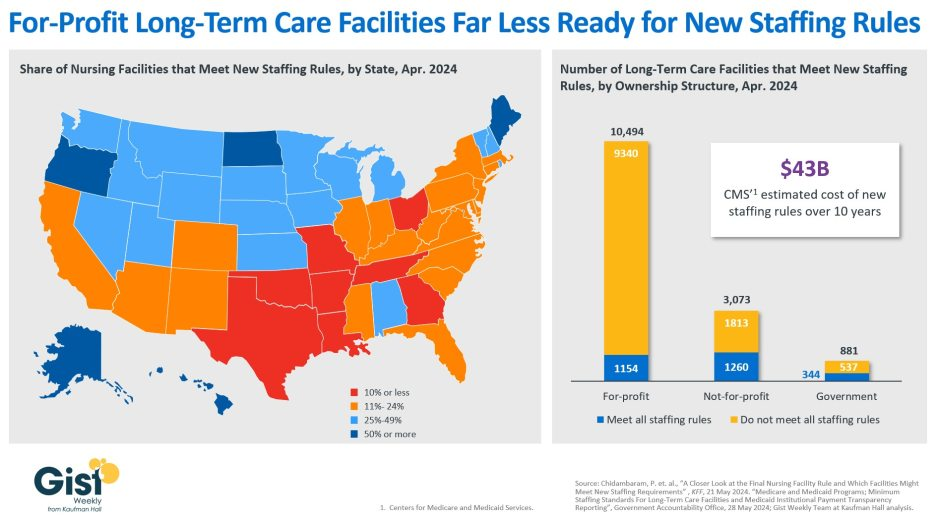

In late April, the Centers for Medicare & Medicaid Services (CMS) establishednew staffing standards for long-term care (LTC) facilities, mandating a minimum of 3.48 hours of nursing care per patient per day, with 33 minutes of that care from a registered nurse, at least one of whom must be always on site. The rule is slated to go into effect in two years for urban nursing homes and three years for rural nursing homes, with some facilities able to apply for hardship exemptions.

Although about one in five LTC facilities nationwide currently meet these staffing standards, staffing levels vary greatly by both state and facility ownership profile. In 28 states, fewer than a quarter of LTC facilities meet the new standards, and in eight states fewer than 10% of facilities are already in compliance.

Facilities in Texas are the least ready, with only 4% meeting the new staffing minimums. In terms of ownership structure, only 11% of for-profit facilities—which constitute nearly three quarters of all LTC facilities nationwide—have staffing levels that meet the new staffing minimums.

The Government Accountability Office projects this new rule will cost LTC facilities $43B over the first ten years, a significant expense at a time when recruiting and retaining nursing talent is already challenging.

Citing the risk of mass closures from facilities unable to comply, nursing home trade groups are suing to stop the mandate from going into effect, and there is also a bill advancing in the House that would repeal the staffing ratios.

That bill is backed by the American Hospital Association, which fears the mandate “would have serious negative, unintended consequences, not only for nursing home patients and facilities, but the entire health continuum.”