A Florida retirement haven is thrown into chaos as a $360 million Medicare overbilling scandal and a Humana–UnitedHealth standoff leave seniors scrambling to keep their doctors.

Behind the gates of The Villages (the pastel Shangri-La of Florida retirement lore) is a place where American seniors zoom around on golf carts like 1977 Thunderbirds and keep wrist stabilizers on the ready for impromptu pickleball matches. It’s a community built on the promise that retirement is a time for sunshine, camaraderie and — most importantly — a health system that doesn’t leave you out in the cold.

HEALTH CARE un-covered has published stories about The Villages in the past – and how the retirement community is rife with Medicare Advantage shenanigans. And today, many Villagers have been blindsided by these shenanigans like they’re part of a Big Insurance hostage crisis straight out of an episode of Days of Our Lives or General Hospital.

A TVH / UnitedHealth dispute leaving seniors “duped”

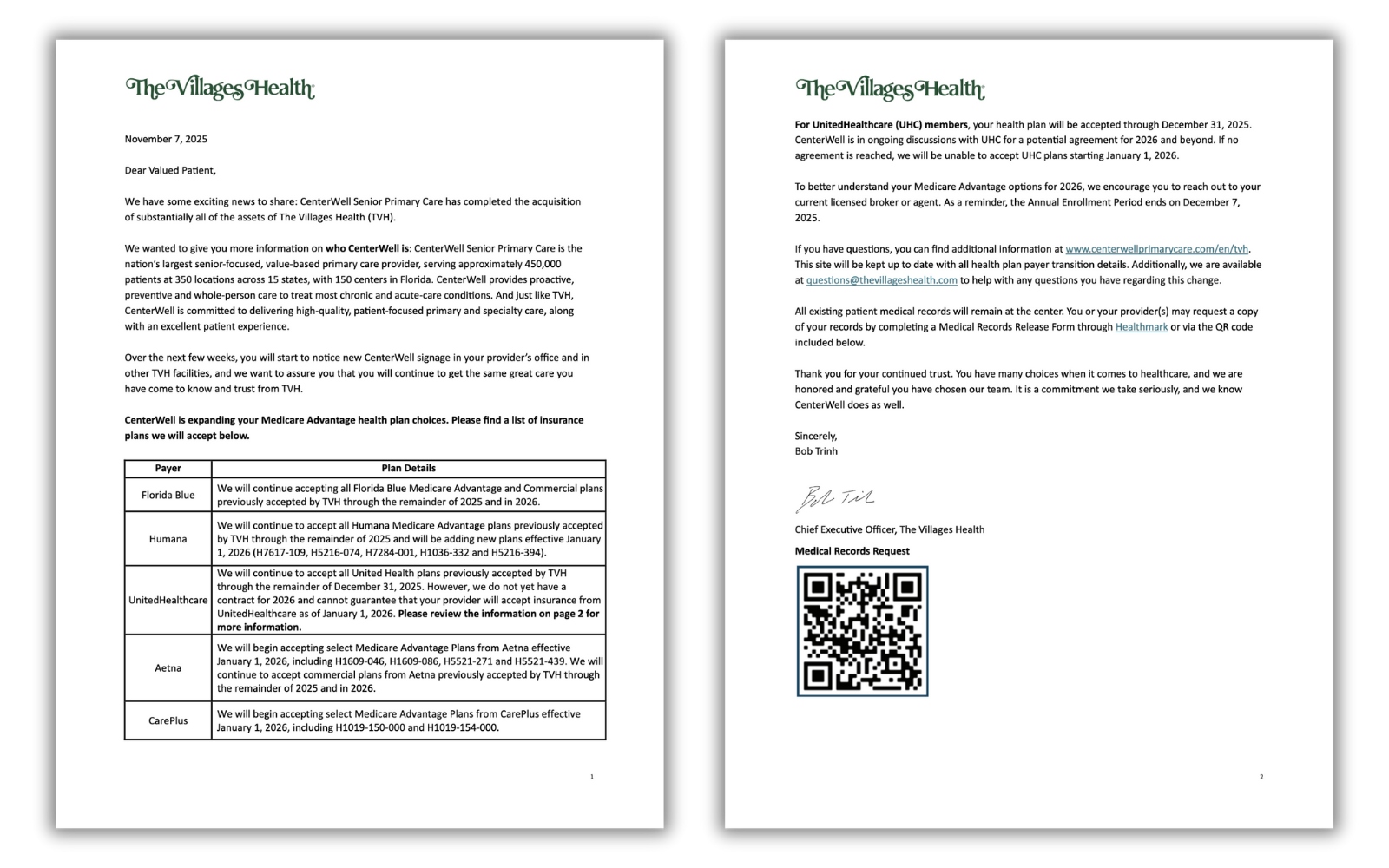

Earlier this year, The Villages Health (TVH) — the health system serving more than 55,000 retirees — promised a smooth handoff as it prepared to sell itself to CenterWell, Humana’s senior-focused primary-care chain. TVH’s CEO assured residents that “no change in care” was coming, according to News 6.

But then came the bankruptcy filing. And then the revelation that TVH owed more than $360 million to the federal government for “Medicare overbilling.” And then the sale. And, according to Village-News, then a bankruptcy judge confirming that, yes, TVH was indeed being swallowed by CenterWell for $68 million.

In other words: the health care version of a soap-opera plot twist. Only with fewer glamorous outfits and more Chapter 11 filings.

On November 7, the very day the sale of TVH closed, patients received a message warning them that their UnitedHealthcare Medicare Advantage plan — the plan they were nudged toward back in 2016 when TVH tried to push all patients into UnitedHealth’s grasp — might not be accepted after Dec. 31, 2025. If negotiations fail, residents must switch doctors or switch insurers.

“Not to be notified until basically the last minute that there isn’t a contract between CenterWell and United at this time is very alarming,” Villager Phyllis McElveen told Spectrum News. “We had already gone out and selected our UnitedHealthcare plan for 2026. We had already done everything. And now to know we might have to make a change is just not a pleasant feeling.”

At The Villages, you can imagine that picking the right Medicare plan is akin to competitive sport — one step removed from a pickleball tournament. The residents do their homework and many reportedly attend “Medicare prep presentations.” So for Villagers, being blindsided is a big deal.

Longtime patient Nancy Devlin told News 6 that she dug through Humana’s and Aetna’s plans to find a plan that might allow her to stay with the physicians she’s seen for six years. But for Devlin, her digging was to no avail. None of the plans matched what she currently had with UnitedHealthcare. Not the same covered medications. Not the same premiums. Not the same out-of-pocket costs. Not the same networks.

“They duped us,” she said. “It’s more expensive and doesn’t have my medications, or I have to pay for them, and I don’t pay for my medications now.”

For retirees on limited incomes, doubling drug costs is a gut punch that can mean one less trip to visit their grandkids or postponing that cruise to the Bahamas. Or for some, putting enough food on the table.

A deal gone sour

To understand how this crisis happened, go back to 2016, when TVH urged residents to switch into UnitedHealthcare Medicare Advantage or lose access to their doctors. Fast-forward to today. TVH is bankrupt, Humana now owns the centers, and UnitedHealth, the world’s largest health conglomerate (and the once-preferred partner for Villagers) is persona non grata unless a deal is reached.

The timing could not be worse. Open enrollment ends December 7, which means that tens of thousands of retirees have just around two weeks to decide whether to switch insurers or switch doctors.

What’s happening here is not simply a contract negotiation gone awry, but a symptom of something deeper. TVH didn’t just owe “some money” to Medicare. It owed about $360 million because of what Humana and The Villages described as a gigantic “Medicare coding error.”

UnitedHealthcare, in turn, accused The Villages’ controlling Morse family of quietly pulling out $183 million between 2022 and 2024 – funds UnitedHealth argued were siphoned off just before the bankruptcy filing.

If that allegation sounds familiar, it’s because we’ve seen versions of this story across the health care industry: private companies treating Medicare Advantage plans like piñatas stuffed with taxpayer dollars. Sometimes, the bat misses the piñata and smacks a whole village of seniors.

Here’s what happens next

The Villages, for all its mid-century charm and retirement-resort quirks, is a microcosm of a national problem that Medicare Advantage is, too often, run for Big Insurance’s advantage with seniors just an afterthought. Corporate acquisitions, bankruptcies, risk-coding schemes, contract disputes and Wall Street demands that lead to fewer and fewer in-network doctors and hospitals and covered drugs. Meanwhile, billions in taxpayer dollars flow through this system with relatively no accountability. Medicare Advantage is corporate welfare on steroids, with the “invisible hand” of the market misleading and then slapping the hell out of vulnerable American seniors to enrich the big guys in control with cushy government handouts.

For Villagers, it’s either/or:

- Either CenterWell and UHC strike a deal: The crisis cools, residents keep their current doctors in 2026.

- Or no deal is reached: Tens of thousands will either change doctors, change plans or risk being turned away at medical appointments starting Jan. 1, 2026.

And remember: If the retirees of The Villages — a community that votes, organizes and documents everything — can be blindsided like this – anyone can – whether it’s CVS / Aetna pulling out of the Affordable Care Act marketplace or Cigna pushing ambulatory surgical centers out of it’s network and “exiting” all of its Medicare Advantage markets. Regardless, until this is figured out, these retirees should take it easy on the pickleball court and drive carefully on those golf carts.