Sweeping changes to Medicaid and the Affordable Care Act are combining with rising health costs to make 2026 a high-stakes year for hospital operators.

Why it matters:

While major health systems like HCA are likely to weather the worst, some safety net providers and facilities on tight margins could close or scale back services as uncompensated care costs mount and uncertainty around future policies swirls.

“We took a big hit in 2025,” said Beth Feldpush, senior vice president of policy and advocacy at America’s Essential Hospitals.

“I don’t think that the field can absorb any further hits without us really seeing a crisis.”

State of play:

Last year’s GOP tax-and-spending law will decrease federal Medicaid funding by nearly $1 trillion over the next decade, translating into millions more uninsured, lower reimbursements and higher costs for hospitals.

The Trump administration is also considering big changes to the way Medicare pays for outpatient services that could reduce hospital spending by nearly $11 billion over the next decade, including paying less for chemotherapy.

Hospitals have the rest of this year to boost their balance sheets, invest in technology including AI, and even consider merger plans before the biggest changes take effect in 2027, Fitch Ratings wrote in its annual outlook for the nonprofit hospital sector. The financial outlook remains stable for the sector overall next year, the report predicts.

“People are already very proactively looking at those out years and saying, if that’s the worst-case scenario that I’ve got to deal with, what can I do today to make that impact less,” said Kevin Holloran, a senior director at Fitch.

Threat level:

Hospitals in some instances have started closing unprofitable services like maternity care and behavioral health care in the face of financial pressures.

More than 300 rural hospitals are at immediate risk of closing their operations entirely, according to a December report.

Safety net providers also are going to court to fight an administration effort to make them pay full price for medicines they currently get at a steep discount and reimburse them later if they’re found to qualify under the government’s 340B discount drug program.

“Those hospitals that have been underperforming … they are going to continue to struggle,” said Erik Swanson, managing director at consulting firm Kaufman Hall. “Those who are doing really, really well may continue to see growth in their performance.”

Private equity firms will likely continue buying up and building new businesses in outpatient service areas like ambulatory surgery, labs and imaging, he said.

“Hospitals and health systems should continue to expect quite a bit of challenge and disruption in those spaces.”

Congress still could extend the industry some lifelines, though any effort to delay or roll back some of the biggest Medicaid cuts face tough odds this year.

Sen. Josh Hawley (R-Mo.) introduced a bill to repeal parts of the GOP budget law that would slash hospitals’ Medicaid dollars.

Lawmakers are debating whether to renew enhanced ACA subsidies that expired at the end of 2025 and could result in millions more uninsured patients, but that effort would also have to overcome significant GOP opposition.

“Our job is to make sure that we create a predicate that, as these provisions come online, they may very well need to be revisited,” said Stacey Hughes, the American Hospital Association’s executive vice president for government relations and public policy.

What’s ahead:

Beyond policy changes, hospitals also are dealing with inflationary pressures, including rising medical supply costs, and administrative overhead from insurer pre-treatment reviews.

Those trying to pad their margins may ramp up their use of artificial intelligence to code patient visits in a way that increases reimbursements from public and private payers, Raymond James managing director Chris Meekins wrote in an analyst note.

While hospitals have historically been able to navigate big policy challenges, if things don’t go their way, it could turn into a “tornado of trouble,” Meekins wrote.

Congressional negotiators are working to revive the health care deal that was dropped from a government spending package in late 2024 — but the odds of resurrecting enhanced Obamacare subsidies as part of the effort appear dire.

Why it matters:

Long-stalled bipartisan priorities that are in play include an overhaul of pharmacy benefit manager practices, as well as a measure that would place more controls on Medicare outpatient spending.

They’d likely be combined with a renewal of health programs due to expire Jan. 30, including certain Medicare telehealth flexibilities and funding for community health centers.

Driving the news:

Leadership and health committees in both parties have quietly swapped offers on a package over the past week while attention was primarily focused on the fight over expired Affordable Care Act tax credits.

Democrats included a three-year extension of the ACA subsidies in their latest offer knowing that GOP leadership is likely to reject it, sources said.

That would still leave intact most of the health care deal that was destined to ride on a government funding package before it was scuttled at the last minute by Elon Musk and then President-elect Donald Trump.

What we’re hearing:

Asked about the likelihood of a health package without the ACA subsidies, Senate Finance Committee Ranking Member Ron Wyden (D-Ore.) pointed to the overwhelming 26-0 vote in his committee for the PBM overhaul in 2023.

“I’m not going to negotiate with myself but the reality is I think a 26-0 vote in the Senate … it’s like unheard of,” Wyden told Axios, adding he is “feeling upbeat” about getting the PBM bill over the finish line.

Senate Finance Chairman Mike Crapo (R-Idaho) also told Axios he is “feeling optimistic” about the PBM bill, saying there is “broad support here and at the White House.”

That measure includes provisions like “delinking” the price of a drug from PBM compensation in Medicare Part D.

The prospective package would also include a measure that would require off-campus hospital outpatient departments to have a unique identifier number.

It’s a cost-saving measure designed to prevent outpatient departments from billing payers at higher amounts associated with full-service hospitals.

But it would stop short of a full-scale, more sweeping change known as site-neutral payments that would more closely align Medicare payments to hospital outpatient departments with freestanding physician offices.

The intrigue:

The outlook for renewing enhanced ACA subsidies, which help millions of Americans afford their premiums, is much bleaker.

While a separate bipartisan group of senators continues to meet in search of a compromise, a key negotiator, Sen. Bernie Moreno (R-Ohio), told reporters on Tuesday that a release of a proposal would be punted until after next week’s Senate recess.

Even if the group can release a proposal — which would include GOP-backed changes like eliminating $0 premium plans — there is deep skepticism in both parties that it can actually pass.

Many Republicans are opposed to any kind of ACA subsidy extension, saying it is wasteful spending that benefits insurance companies.

Top Democrats are pushing for a clean subsidy extension without GOP-backed changes and blasting Republicans for blocking it, in what could be a preview of midterm campaign messaging.

Between the lines:

There still are significant divisions over whether to include new limits on the ACA funding going to plans that cover abortions.

The bipartisan group has discussed a potential compromise that would increase audits and levy penalties on insurance companies that don’t comply with existing rules requiring them to segregate taxpayer money from paying for abortions.

The idea immediately drew fire from the anti-abortion group Susan B. Anthony Pro-Life America, and many Senate Republicans think it does not go far enough.

The bottom line:

There still could be an election-year health deal — just don’t expect it to address ACA subsidies.

The 119th Congress headed into the holidays no doubt looking forward to quality time with their loved ones and a fat goose on the dinner table—or whatever the privileged stewards of the People eat at Christmas—with what seemed like little concern for the mess and panic they left behind. Messy panic like what the nearly 25 million Americans getting their health insurance through the ACA are facing as their monthly premiums increase at astronomical rates. (Assuming they stick with the devil they know.) Now they’re back, surely refreshed with all engines blazing on their New Year’s resolution to make health care more affordable. It is, after all, what the People want.

But while what to do with the ACA gets fought over like an unloved middle child in a divorce, another form of health care dupery will continue to operate like a mob-run casino.

Many of us navigate our health care thinking that if we can land a full-time job at a company offering benefits, we—and our families—will be covered for most physical and mental health issues without complete disruption to our financial health. And in many cases, sure, that tracks. What we’re not seeing is the financial fleecing that those companies are experiencing at the hands of third-party administrators (TPAs). What’s more is that the companies aren’t seeing it either. And that’s not a bug. It’s a feature.

An employer has options when deciding how to provide health benefits to its employees. One is to contract directly with an insurance company and pay fixed premiums. Another is to self-insure. Self-insured employers pay for all enrolled member benefits and claims directly from their own funds instead of paying those aforementioned fixed premiums. It’s an attractive option for employers because even though the company assumes the financial risk, it offers control over costs, plan design and claims-related data, all of which can help the company run more efficiently and with greater fiduciary understanding. They’re popular, too, with approximately 57% of private sector workers enrolled in these self-funded plans, according to KFF. To facilitate the company’s coverage, employers contract with a TPA to broker plan details, manage claims, pay providers, assist plan members and ensure the benefit program remains compliant with state and federal regulations.

This is theoretical.

TPAs say they’re looking after the company, but they don’t. They’re looking after themselves and their parent companies. And just who are these parents? Blue Cross Blue Shield, UnitedHealthcare, Cigna, and Aetna. Or, as they’re collectively called, the BUCAs. The usual suspects in the web of health care greed and deception.

It’s like taking a pregnancy test then being told the results can’t be shared with you because the results belong to the stick with the pee on it.

Skimming the till the TPA way

The Employee Retirement Income Security Act (ERISA) was passed in 1974 to protect patients by requiring transparency, fiduciary standards and fair claims processes for employer-sponsored health (and retirement) plans. TPAs have found clever ways to avoid ERISA accountability in the way they structure the administrative services agreements (ASAs) they sign with employers. One is by enlisting gag clauses in the ASAs to protect TPAs from showing their work to the employer, which obviously defeats the whole purpose of choosing to self-fund and have more oversight of how their money is being spent. The Consolidated Appropriation Act of 2021 prevented these gag clauses. But TPAs are nimble and clever, and when pressed to offer up information, such as any of the data related to claims managed and paid, TPAs argue they don’t have to because the data is proprietary. It’s an odd argument to make. It’s the employer’s money being spent and their employees being treated. It’s like taking a pregnancy test then being told the results can’t be shared with you because the results belong to the stick with the pee on it.

Not sharing crucial plan information with the employer is one thing, tacking on fees under the guise of good stewardship is another. Like the overpayment recoupment fee. Here’s how this could play out:

The TPA discovers a provider was overpaid due to an error made by duplicating payments, incorrect coding, or any other administrative whoopsie

The TPA recoups the overpaid amount, say, $5,000, then takes a percentage of the recouped money—typically 30% — as a fee for cleaning up the mess they made

They recover the extra $5,000 the employer paid, the employer gets back $3,500 while the TPA banks $1,500

This means that the employer paid a total of $6,500 on a $5,000 claim, making carelessness an incentive for TPAs

Shared savings fees are put in play when someone enrolled in a health plan uses an out-of-network (OON) provider. As we know, OON claims are often hefty bills. Seemingly, in good faith, the TPA will negotiate a discounted rate with the provider. It could look like this:

The OON provider bills the employer $50,000

The TPA negotiates the provider down to $20,000 then takes their shared savings fee out of the $30,000 savings

Again, this fee rate is often around 30%. That puts $9,000 in the TPA’s pocket

The TPA is incentivized here to push members to go OON, and why not? A $30,000 savings sounds real good. But employers aren’t getting the opportunity to weigh in on these negotiations because they are, you know, “proprietary.”

Putting it honestly, TPAs are the neighborhood mafioso.

TPAs also have skip lists, which are providers they do not apply oversight to when looking for billing errors, which they rarely do anyway, but these lists make it more, um, official. In May 2024, W.W. Grainger, Inc., a product distribution company with 20,000-plus employees (and their family members) filed a lawsuit against Aetna claiming Aetna took money paid by Grainger intended to pay for claims, paying providers only a portion of the money, keeping the rest for itself. The suit claims, “Aetna did not use the fraud prevention techniques it regularly employs when administrating claims for its own fully insured plans. Aetna never refunded or credited the difference to the Plans.” The suit further states, “Aetna also engaged in active deception to conceal its breaches of its duties to the Plans. Aetna prevented Grainger from discovering Aetna’s improper conduct, including by limiting audit rights, providing false or inaccurate claims reports, and preventing Grainger from obtaining or accessing data about the actual financial transactions between Aetna and the health care providers.”

Many other similar suits have been filed against TPAs but are either dismissed or held up in the court’s web of confusion and legal ballet.

The uphill battle for Capitol Hill

Putting it kindly, TPAs are middlemen sold as a way to lighten the administrative load for a company. Putting it honestly, TPAs are the neighborhood mafioso. Imagine with me, a neighborhood dry cleaner… One day, a wise guy walks in and tells the owner that he needs to pay 30% of the profits each week in exchange for protection. “Protection from what?” the dry cleaner asks. “From, you know, trouble. And you don’t want any trouble. Not at a nice establishment such as this.” There’s no way the dry cleaner can win. Either pay the guy or risk going to open the door one morning only to discover the door is the only thing left standing after the place mysteriously burned down overnight.

A bill introduced last year by Senators John Hickenlooper (D-Colo.) and Roger Marshall (R-Kan.) called the Patients Deserve Price Tags Act (PDPTA) is designed to make health costs more transparent and provide employers with better tools to hold TPAs accountable as well as to strengthen and expand existing transparency measures like requiring TPAs to disclose compensation practices truthfully, completely and upfront instead of leaving the burden to employers. The bill would make void any provisions in ASAs that support limiting access to employers. Furthermore, it would empower the Department of Labor (DOL) to fine TPAs $10,000 for each day a violation continues. TPAs would also be required to make quarterly reports detailing pricing and compensation practices and report the total they have been paid in rebates, fees, discounts and other forms of payment. Failure to provide this information would be a violation of ERISA, and the DOL could fine the TPA $100,000 per day until the report is provided.

But will it pass? And if so, how much of it will get hacked away thanks to BUCA lobbying efforts? And is another bill even the answer? Legislation has been passed to defend against these practices, and yet, they persist. Apparently, doing the same thing over and over again and expecting a different result is not insanity, but progress for Congress. Another bill may just add to the complexity of things. And the big question remains: Will it save self-insured employers money? Doubtful. TPAs can simply raise the price of doing business. That’s BUCA forecasting 101—everything can always be more expensive.

Perhaps Washington needs to begin thinking of TPAs and BUCAs like the organized criminals they are and bring a RICO case against them.

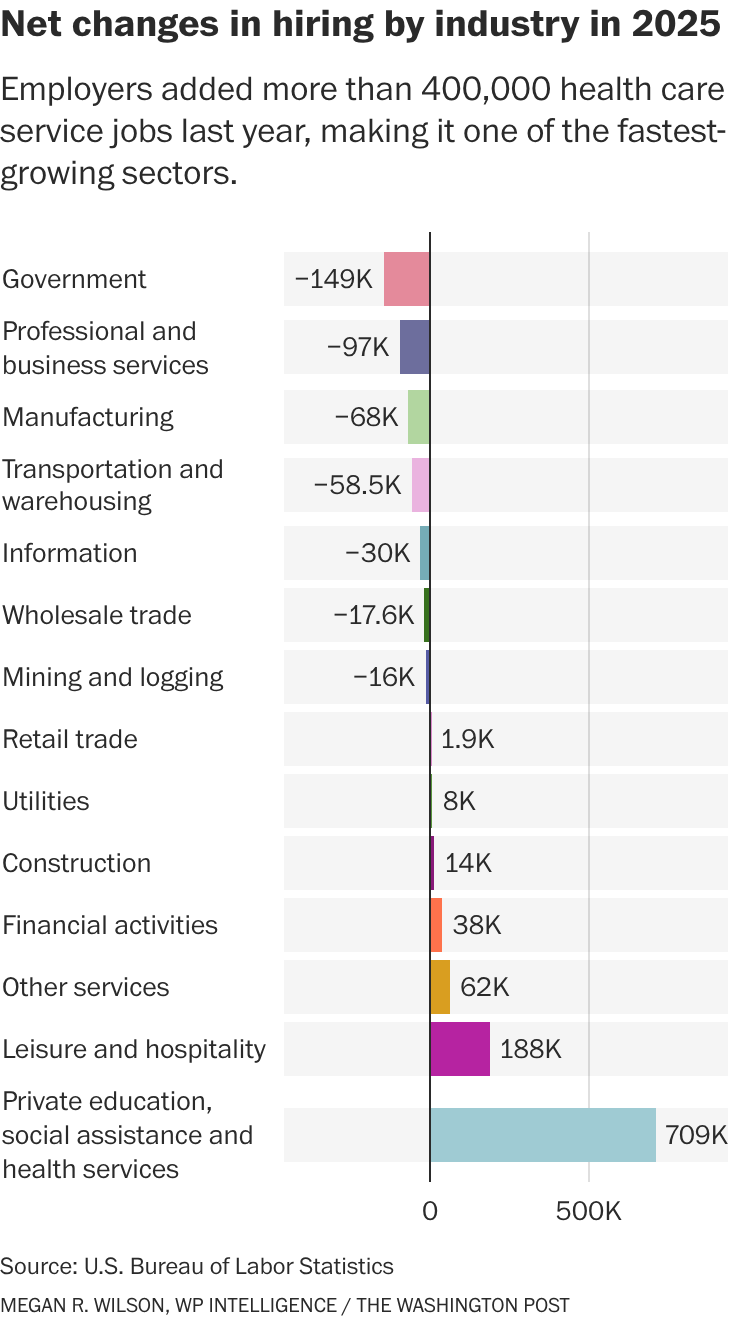

The health services industry was once again a bright spot in the economic data in today’s jobs report, which otherwise landed with a thud and capped off the weakest year for overall hiring since the pandemic.

The growth underscores how much health care employers are propping up the overall labor market — accounting for most of the gains, both in sheer numbers and percentage growth.

“The fundamental reason why health care employment continues to grow so strongly is that the aging population continues to boost demand for health care services,” said Jed Kolko, a senior fellow at the Peterson Institute for International Economics. “The population will continue to age, so that fundamental driver of demand continues.

”Behind the numbers: Although economists expect the health industry to continue expanding, they note that 2025 represented a slowdown from the previous year. Although many factors are at play, multiple analysts said the Trump administration’s restrictive immigration policies may be to blame. More on that later.

It’s not a huge surprise that people working in places such as hospitals, dentists’ offices and nursing homes represent the largest growth in hiring: Health care makes up about 18 percent of the overall U.S. economy — which means that $1 out of every $5 that Americans spend goes to health care. Advertisement

But this also highlights how health services hiring is keeping broader U.S. employment from sliding — even as other industries cool. Patients and providers alike are bracing for cost and workforce pressures in 2026.

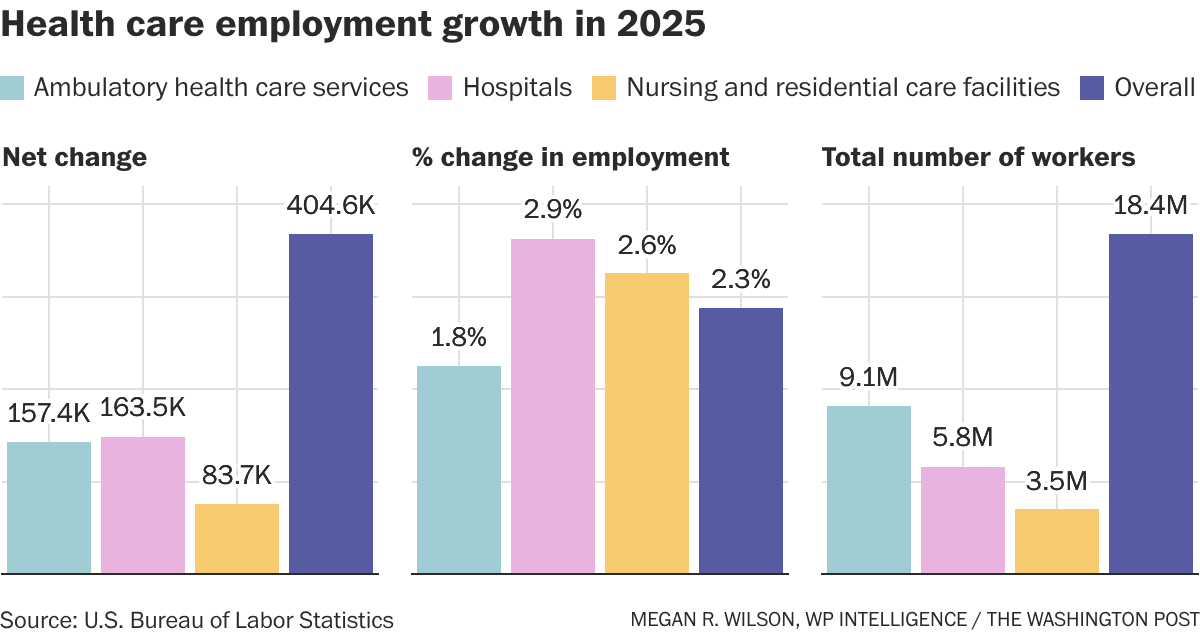

Dive in: Although the number of people working in health services increased by more than 404,000 in 2025, it’s still a slowdown from the level of growth the sector saw the year before. In 2025, the health industry added about 34,000 workers per month, according to federal data, compared to an average monthly gain of 56,000 health jobs in 2024. This included people working in hospitals, residential care facilities or nursing homes, diagnostic labs, and for home health providers .

Here’s how it breaks down:

Hospitals represented the highest employment growth rate — 2.9 percent — in the health services industry, followed by jobs at nursing homes and residential care facilities, at 2.5 percent.

“We’re getting older and sicker. And, on top of that, we’re getting older and sicker in a way [where] we don’t have young people around to take care of the older, sicker people, right?” said Richard Frank, economic studies senior fellow at Brookings and director of its Center on Health Policy. Advertisement

“So what used to be long-term care delivered by family members when we had four or five kids per household, that looks very different today,” Frank said. “You’re going to have to pay people to do that work.

”While economists anticipate health care hiring to continue to grow — in part for that very reason — there two major policy shifts loom as a dark cloud over the industry and may impact the health services workforce.—

Immigration: Providers around the country have said that the Trump administration’s approach to immigration has hampered their ability to hire people. The administration has been cracking down on legal immigration as well as on people who have come to the U.S. illegally. Meanwhile, immigrants make up 28 percent of the long-term care workforce and 32 percent of home care workers, according to KFF.—

Medicaid cuts: The Republicans’ tax-and-domestic-policy law enacted last July is expected to slash nearly $1 trillion from the Medicaid program for low-income Americans. Researchers estimate that this will hammer the balance sheets of many hospitals, which are likely to see an influx in patients seeking care but are unable to pay for it. Hospitals and health clinics are already shutting down or laying off workers across the country. Although the Medicaid policy changes — which won’t fully kick in for years — aren’t the only reason for the closures, it shows how vulnerable many providers already are.

Other changes, including the proposed cuts to the National Institutes of Health, could trickle down to communities with research hospitals and ultimately impact the labor market, according to research from the Brookings Institution. New Medicare payment policies that aim to shift care away from expensive hospital services and toward primary care could also have an impact, although it likely won’t be large enough to show up in the data, I’m told.

However: Some states are working to offset some of the administration’s immigration policy changes or health program cuts, which could make it hard to evaluate their impact in the next round of employment data. “There are a lot of … crosswinds blowing in the aggregate that might cover up” the overall impact of these policies,” said Frank.

Other data: Employment in what the government calls “individual and family services” — listed under the “social assistance” category — increased by more than 289,000 people in 2025, representing a nearly 9 percent increase over 2024. These jobs include personal care aides, social workers and substance abuse counselors.

Health care costs hurt Californians every day. Millions can’t afford the care they need. More than half of all Californians skip or delay getting care because it costs too much.

How did we get here?

Health care is too expensive for people in large part because underlying costs in our health care system have grown unchecked for decades. Underlying costs are the “base ingredients” that determine how expensive health care is. Think of things like hospital operating costs, prescription drug prices, and doctor fees — when these costs go up year after year, they get passed on to patients through higher premiums, bigger deductibles, and larger medical bills.

The solution to the affordability crisis isn’t to slash health care spending across the board — that often makes things worse for patients. Instead, we need to be smart about cutting that 25% that doesn’t provide any value for patients.

Some of that rising cost has produced things we actually want, such as breakthrough treatments that save lives, cutting-edge medical equipment, or hospitals retrofitted to withstand earthquakes.

The solution to the affordability crisis isn’t to slash health care spending across the board — that often makes things worse for patients. Instead, we need to be smart about cutting that 25% that doesn’t provide any value for patients. Sometimes that might actually mean spending more money upfront, like making sure everyone can see a primary care doctor, to save money down the road by keeping people healthier.

This work is challenging, but it’s critical. Millions already can’t afford health care. If Californians’ health care costs keep rising the way they have been, even more families will be left behind.

Unchecked growth in the underlying costs of our health care system has driven total health care spending — from families, governments, employers and others combined — to more than triple since 2000, far outpacing inflation, economic growth, and wages.

Here are just a few key examples of the impact on California families:

Health insurance is increasingly becoming unaffordable for California families.

38% of all Californians report carrying medical debt. For Californians with low incomes, that rises to 52%.

Overview of the 3 Reasons

1. Administrative Waste

Health care requires some office work — doctors and hospitals have to schedule appointments, send bills, and keep records. But in the U.S., we spend way too much time and money on administrative tasks, which does nothing to make care better for patients.

Why Does This Happen?

Our health care system is complex. Different hospitals, doctors, and insurance companies often all use different computer systems for clinical data, billing, and administrative tasks. They can’t easily share information with each other. This means:

Staff in different parts of the system spend extra time entering the same information over and over;

Insurance companies and hospitals have to hire more people just to handle paperwork; and

Simple tasks become complicated and expensive.

How Much Money Gets Wasted?

Researchers in 2020 estimated that administrative waste cost the California health care system nearly $21 billion a year, making it the number one source of health care spending that doesn’t do anything to help patients or improve care.

How This Hurts Patients

Administrative waste doesn’t just cost money. It also hurts patient care:

Doctors spend less time with patients because they’re busy with forms.

Patients wait longer to get care.

Doctors have to call insurance companies over and over to find out what’s covered, and this can delay treatment when people need help.

Health care spending depends on two things: 1) how much care people get and 2) the prices that are charged for that care. In California, we have a big problem with pricing.

Same Care, Very Different Prices

The same medical procedure can cost wildly different amounts depending on where you go. For example, a knee replacement might cost $50,000 at one hospital and $70,000 at another. This happens even when both hospitals provide the same quality of care. In other words, the more expensive hospital is not necessarily better.

Lack of Competition Drives Prices Up and Hurts Patients

In many areas, there isn’t enough competition among health care organizations. For example, big hospital systems are buying up smaller hospitals. In some areas, there’s only one major hospital system left. Likewise, a few large insurance companies control most of the market. In some areas, one insurance company dominates.

When hospitals and insurance companies don’t have to compete:

Prices can go up without any improvement in care quality.

Patients have fewer choices about where to get care.

Families pay more for the same treatment.

Some areas become “take it or leave it” markets.

This creates unfair contracts where the biggest companies can demand high prices because patients have nowhere else to go.

When doctors find health problems early, they’re much easier and cheaper to treat. For example:

Regular cancer screenings can find problems before they become serious cancer.

Checking on people with heart problems can prevent expensive hospital stays.

Treating diabetes early prevents costly complications later.

Too often, though, people don’t get these early checks because there might not be a primary care doctor that can see them when they need it. By the time they see a doctor, their problems are much more serious and expensive to fix.

We Don’t Spend Enough on Prevention

Most prevention happens when you visit your primary care doctor for regular check-ups and basic care. But the U.S. has a big problem: We spend only 5 cents of every health care dollar on primary care, while other wealthy countries spend three times that amount.

California research shows that when provider organizations spend more money on primary care:

Patients get better quality care.

People are happier with their treatment.

Fewer people end up in the emergency room.

Fewer people need expensive hospital stays.

Overall health care costs go down.

We could save billions of dollars by helping people stay healthy instead of waiting until they get really sick. It’s like fixing a small leak in your roof instead of waiting until your whole ceiling falls down.

The good news is that we can fix these problems. California is working on several smart solutions right now.

The Office of Health Care Affordability

Created in In 2022, the Office of Health Care Affordability (OHCA) aims to break the cycle of the last decades and make sure that underlying costs in the health care system don’t continue to spiral out of control year over year.

Cost Growth Targets

In 2024, OHCA set an important new target: Total spending by health care’s major players — like hospitals, insurance companies, and large medical groups — can’t increase by more than 3% each year. That’s roughly how much a typical California family’s income grows every year. The target will be implemented in phases over the next several years.

This creates a powerful new incentive for these health care organizations to manage their underlying costs, rather than allowing them to grow unchecked and passing on increases every year to patients. Over time, this should help make health care more affordable for families.

If a health care organization exceeds its spending growth target without a good reason, OHCA will take increasingly serious enforcement actions, starting with guidance to the company on how to meet the target all the way to financial penalties. Penalty money will go into a fund and then back to California families to help them pay for their health care.

Making Sure Quality Stays High

Spending caps are intended to target things like administrative inefficiencies and monopolies, not quality of care.

To ensure health care organizations are focusing in the right places, OHCA is charged with ensuring:

Patients can still get the care they need.

Care quality stays just as good.

Hospitals and clinics have enough doctors and nurses.

OHCA is taking steps to address unfair pricing by reviewing health care mergers and acquisitions.

Congress returns to DC this week to debate the merits of extending the advanced premium tax credits that enable coverage for 4 million in a climate of high anxiety about U.S. intervention in Venezuela and heightened tension with Russia and China.

For many, these unfolding events are numbing: helplessness, frustration and fear are widespread. As 2026 unfolds for U.S. healthcare, the realities are these:

The healthcare economy will be under pressure to do more with less. The health economy is increasingly controlled by private investors and large publicly traded companies in every sector whose shareholder obligations are primary. Public funding from federal, state and local sources is shrinking as a result of the Big Beautiful Bill and pushback from taxpayers who think the system wasteful and ineffective. The S&P Health Index for 2025 closed the year underperforming the broader market. Private equity investments in healthcare except AI solutions that reduce operating costs at scale are troubled. Thus, in 2026, operating margins in every sector will be stressed, access to private capital will be vital and business as usual obsolete.

Mass populism will magnify attention to the healthcare affordability. Per polls, costs of living are issue one to voters. While prices for gas and groceries have moderated, housing and healthcare prices have escalated unabated. Voters think both essential but the majority think consolidation, corporatization and regulatory protections advantage the biggest players and protect special interests. In housing, it’s simpler for consumers: mortgages, rent and utility costs are straightforward. But healthcare is more complicated: out of pocket costs—premiums, co-pays, deductibles, caregivers, OTC et al—are not easily calculable and price estimator tools, patient support and revenue cycle management policies make it easier for consumers. The net result: a large and growing majority of voters think healthcare is unaffordable and government intervention needed.

The mid-term election November 3, 2026 will be likely be the reset for healthcare’s future in 2028 and beyond. All 435 House Seats, 35 U.S. Senate seats and 39 state/territorial governors will be elected. All will face voters anxious about the future and how they’ll pay their bills. The 2026 results will set the stage for 2028 Presidential campaigns that will feature a wide range of alternatives to the healthcare status quo. Some will be incremental; others labeled radical. But all will promise changes unwelcome to many of its prominent incumbents.

Each sector in healthcare—hospitals, physician services, long-term care, insurers, life science manufacturers, enablers and advisors—is vulnerable. None welcomes unflattering attention and all spend heavily on messaging and advocacy to protect themselves. All recognize the elephant in the room—large employers that have patiently funded the system’s profitability and value protective regulation that limit disruption. And in all, implementation of AI solutions that lower operating costs and streamline performance is THE immediate priority.

The realties of 2026 for healthcare are foreboding: business as usual is not an option.

As we ring in the new year there is one thing – maybe the biggest thing – lingering from 2025 that can’t be dropped: The alarming state of health care.

Every aspect of the health care system feels like it’s working against its customers by prioritizing profits over care.

There are significant signs we could be at a breaking point.

More Americans than ever are opting to go without health insurance. A Gallup poll found 1 in 3 are considering running that risk, saying they can’t afford the costs.

For the first time in history, concern for rising health care costs is stride for stride with housing and food costs as American wages are struggling to keep pace. For many income levels they feel left permanently behind.

And not only are people paying record-high premiums, what they have to pay for prescription drugs at the pharmacy counter is breaking the bank as insurance companies have gobbled up pharmacy benefit managers to capture more and more of what we spend on health care.

The number of pharmacies serving the country’s sick has dwindled to the lowest levels in more than 50 years. Rite-Aid, which once operated more than 5,000 stores across the country, closed all of its locations and declared bankruptcy last year. Thousands of independent pharmacies have also closed, largely because of the stranglehold PBMs now have on the prescription drug supply chain. The closures have created hundreds of pharmacy deserts, leaving patients with a dwindling number of low-cost and convenient options.

Medicaid cuts mandated by Congress and the Trump administration last year are expected to cause more rural hospitals to close. More than 100 closed in the last decade and hundreds more are on the brink, according to a Boston University study. Health care is in such a bad spot it’s near the top of the 2026 Congressional agenda. Democrats want to restore the enhanced subsidies that made coverage affordable for the more than 20 million Americans who rely on the Affordable Care Act marketplace for their health insurance but most Congressional Republicans say the subsidies are a waste of money. Despite all that, there’s pessimism that politicians have the appetite for real change.

“We are frogs in a boiling pot,” said Eric Pachman, co-founder of the prescription drug watchdog 46 Brooklyn and data analyst on Wall Street. “Every year health care plans cost more but the coverage we pay for gets crappier.”

Pachman was recently at home when he got a call from a close relative whose son was in the middle of an allergic reaction. The family didn’t have health insurance because the premiums were beyond their means.

“He gave his son an Epi Pen and then drove to the hospital close by,” Pachman said. “He sat there for a while with his son in the parking lot to make sure he didn’t get worse but he didn’t go in.”

Americans are making those alarming decisions while health insurance companies continue to make big profits.

The country’s three largest health insurance companies and their in-house pharmacy benefit managers have rocketed toward the top of the Fortune 500 list of richest companies.

UnitedHealth has become America’s third-richest company behind Walmart and Amazon. In 2024, the company, which has about 30 million Americans enrolled in its health plans, brought in more than $400 billion in revenue, according to its financial filings.

CVS Health is just behind UnitedHealth at No. 5 on the country’s Fortune 500 list, bringing in nearly $373 billion in 2024. Cigna is 13th with $247 billion in revenue.

Health care alarms similar to sirens of 2008 housing collapse

The warning signs of this health care crisis bear a haunting resemblance to the 2008 housing market crash.

Cost vs. Income: In 2006, the average employer-sponsored family health care plan cost $11,381, representing 23% of the average salary. In 2026, the average plan is expected to exceed $27,000 against an average salary of $84,000 — a staggering 32% of income.

Shifting Risk: Just as risky mortgages were offloaded onto consumers, employers have shoved a larger portion of health care costs onto their workers.

Debt: Half of American adults now report they could not pay a $500 medical bill without going into debt.

Opacity: Much like the complex derivatives in mortgages in 2008, PBMs and insurers refuse to make their pricing public. This lack of transparency leaves patients fearing to open their mail after a hospital visit.

The sad joke in Washington D.C. right now is that everyone keeps talking about the price of health care but no one knows what the actual prices are.

In that Gallup poll, those surveyed gave the U.S. health care system a grade of D+.

“Our government continues to apply band-aids to a bloated pricing system rather than prescribing real, system-wide solutions,” said Antonio Ciaccia, co-founder of the pharmacy drug data site 46Brooklyn.com and former head of government affairs for the Ohio Pharmacist Association.

Lawmakers in more than a dozen states have tried to rein in insurers and their PBMs with lawsuits and regulations. Those lawsuits have led to more than $400 million in payouts by the big three health insurers and their subsidiaries.

Despite that the system keeps on going.

After years of battling insurers and their PBMs, Ohio’s Republican Attorney General, Dave Yost, came to the conclusion that any major reforms would have to come at the federal level.

“PBMs were originally intended to reduce the financial burden on Americans for prescription drugs, but the reality today is starkly different,” Yost said. “Instead of prioritizing the interests of patients, PBMs have shifted their focus to maximizing profits and marginalizing local pharmacies from the marketplace.”

Pachman also said if more people do opt out of insurance they will still go to hospitals for medical care.

“Hospitals cannot turn those patients away because they are legally required to treat them,” Pachman. “That means the cost burden will be shifted to those that do pay for insurance.”

While any type of significant reforms seem unlikely, many states are at least starting to ban medical debt from credit reports.

Fifteen states have the ban in place and Ohio, Alaska, North Carolina and Michigan are exploring similar statutes this year.

Chris Deacon, an attorney, author, health care reform advocate and former director for the New Jersey treasury department said the only incentive right now is for insurers to keep growing the $5.3 trillion spent on health care in the United States in 2024.

“There’s no incentive to control prices,” Deacon said. “And there’s no transparency whatsoever in any of this.”

The drug price hikes that are helping drive the health affordability crisis will continue for the rest of President Trump’s term, key industry stakeholders are now predicting —despite his deals with drugmakers and Medicare negotiating lower prices.

The big picture:

Insurers, drug supply middlemen and hospitals who represent 13% of all pharmaceutical purchases predict single-digit price increases for branded drugs over the next three years, according to a new survey by TD Cowen.

The increase will be largely driven by pricey new medications, such as drugs for cancer, diabetes and obesity, as well as cell and gene therapies, the purchasers said.

Drugmakers are already set to raise prices this year on at least 350 medications, including common vaccines and cancer treatments.

State of play:

Democrat and Republican policymakers have prioritized lowering drug prices in recent years in response to mounting public concern over health costs.

Congress during the Biden administration passed the Inflation Reduction Act, allowing Medicare to negotiate lower prices for select drugs.

Trump has made direct deals with drugmakers for decreased U.S. prices on certain products.

Yes, but:

TD Cowen’s latest annual drug purchaser survey shows these policy interventions aren’t driving prices down, at least in the near term.

Insurers, pharmacy benefit managers and other payers said they expect their cost of acquiring a drug to increase by 8%, on average, over the next three years. They gave the same figure when surveyed in 2024, 2023 and 2022.

Prices for generic drugs are predicted to increase by 2% over the same period.

“As long as biopharma delivers innovation, we see no change in the upward trend in drug prices,” TD Cowen wrote in its analysis.

By the numbers:

44% of purchasers surveyed expect Medicare drug negotiations to have a modest impact on cost, and another 30% said they don’t think they will have any impact.

But 74% said they think drug usage will increase over the next five years due to the policy changes and the IRA’s out-of-pocket cost protections for seniors.

Reality check:

Patients aren’t necessarily going to see an out-of-pocket increase as drug acquisition prices rise, due to rebates and other discounts.

But payers often pass increased costs along to patients, including by raising monthly premiums.

Net drug prices increased one-tenth of a percent in 2024 after accounting for rebates and discounts, per an IQVIA report published in April.

What they’re saying:

Patients “bear an unfair burden as out-of-pocket costs have risen faster than the net prices paid by PBMs and insurers,” PhRMA spokesperson Chanse Jones said. “At the same time, innovation … continues to skyrocket.”

Advocacy group Patients for Affordable Drugs said in response to the survey results that the IRA’s reforms are working for seniors.

“[T]hat’s exactly why expanding and protecting the law matters,” Alyson Bancroft, director of policy, legislation and alliances, told Axios in an email.

Health and Human Services communications director Andrew Nixon told Axios the agency doesn’t weigh in on third-party analyses, but said HHS continues to advance policies to lower drug costs so patients can afford treatments.

What we’re watching:

Purchasers expect coverage of obesity drugs to grow over the next three years.

Almost 30% of respondents said they currently have very limited coverage of GLP-1s for obesity, but nearly 20% said they expect to offer complete coverage for a finite amount of time within three years.

Medications for diabetes, obesity and rheumatological conditions were cited as likely to have the greatest decrease in price over the next three years. That’s due to coming patent expirations and increased competition among advanced products, TD Cowen noted.

In mid-December, members of Congress members left Capitol Hill for the final time in 2025, thus ensuring that the year would end with a failure arguably more significant than anything they accomplished during the prior 12 months: the end, despite a widespread public clamor for action, of subsidies put in place during the pandemic that made premiums of ACA marketplace plans affordable for millions of Americans.

Although important health care stories often fail to get much media attention, the failed efforts – mostly, but not exclusively, by Democrats – to save the Affordable Care Act/Obamacare subsidies were different. As patients from Maine to California opened their yearly renewal letters, many were shocked to see their monthly premiums for 2026 would be doubling or even tripling – right when the rising cost of living was already the No. 1 voter concern.

But there’s another aspect to America’s looming health care crisis that almost no one is talking about.

This is the other side of the coin – the out-of-pocket expenses that everyday consumers pay for doctor visits or prescription drugs – because of higher deductibles, or because of the growing number of patients who will risk not having any insurance at all next year because they can no longer afford it.

Even before the new year began, many Americans were dreading a double whammy of skyrocketing premiums and a sharp spike of what they expect to pay on top of that, out of their own pockets.

For example, Doug Butchart of Elgin, Ill., told ABC News that while his wife Shadene – who is living with the neurological disorder amyotrophic lateral sclerosis (ALS) – paid about $3,000 in out-of-pocket costs last year, that’s expected to rise as high as $10,000 in 2026, on top of monthly premiums that are tripling with government inaction on the ACA subsidies. It’s all more than the senior couple currently earns from Social Security.

Of course, millions of other Americans who switched to insurance plans that trade lower monthly premiums for sharply higher deductibles are taking an economic gamble that won’t play out until they see how healthy they are in 2026. In particular, those joining the surge of patients switching their ACA health coverage from the common Silver plan to the lower-premium Bronze coverage could pay thousands more as a result.

An analysis by KFF, the health care think tank, found that the average deductible in 2026 for patients who sign up for a Silver plan, assuming no reductions for cost sharing, will rise to $5,304, but for those who opt into a Bronze plan, the average deductible will spike to $7,576 – meaning a more than $2,000 higher outlay for sicker patients who max out on their covered expenses.

Katie Keith, director of Georgetown University’s Center for Health Policy and the Law and a former Biden administration aide, said the skyrocketing cost of insurance means “people are so premium sensitive that they might still go with Bronze and kind of leave money on the table – then they’re facing at least a $9,000 deductible, or whatever out-of-pocket max is, and just huge burdens.”

Keith and other health policy experts see a perfect storm of negative factors for higher out-of-pocket expenses in 2026 – from the impact of generally rising health costs to the added burden of government inaction or indifference in Washington. Among the factors behind a looming crisis:

Last summer, the Trump administration finalized new rules for the ACA that changed a key calculation and thus increased the maximum in out-of-pocket expenses that can be set by insurers – a ruling that also affects the millions of Americans who receive health insurance through a private employer.

The new math proposed by the Trump administration’s Centers for Medicare and Medicaid Services (CMS) adds yet another 4% hike on top of an already expected steep increase. The higher limit means individuals in some plans will pay $10,600 before their insurance kicks in, with a bump to $21,200 for families – an overall increase of 83% for individuals and 67% for families since the out-of-pocket maximum established by the ACA went into effect in 2014.

The Center on Budget and Policy Priorities reported that, because of these changes, a family of two or more people on the same plan could face an additional $900 in medical bills if a family member is seriously ill or injured in 2026.

Increasingly, employers are putting more of the economic burden on their workers for health care costs, especially through higher deductibles. For one thing, the KFF Employer Health Benefits Study has found that – for employees whose coverage carries a deductible, on individual plans – that average out-of-pocket cost has outpaced inflation and more than tripled in less than two decades, from $567 in 2006 to $1,887 in 2025.

What’s more, increasing pressure for workers to share the cost burdens of their health insurance has also caused more employer plans to offer a higher deductible option, and more people are signing up for that risk. Federal data shows that while only 38% of private-company employees had the option for a high-deductible plan in 2015, that number has now risen to more than half.

Perhaps the biggest factor is the end, for now, of the tax credits that had been holding down the cost of monthly premiums for ACA marketplace coverage since the COVID-19 epidemic. In states gathering data about early enrollment trends this past fall as higher premium notices went out, the shift away from traditionally popular Silver plans into Bronze coverage, with its higher out of pocket costs, has been dramatic.

For example, in California, where the Covered California program is considered a trailblazer in public health plans, officials told NBC News they’ve seen a “substantial” movement of enrollees choosing the Bronze plans with the highest out-of-pocket deductibles. Typically, officials reported, about one in five new enrollees go with the Bronze option, but for 2026 that number has soared to more than one-third. It’s a similar story in Idaho, where officials told NBC that Bronze enrollments are running 5% higher than normal, with most moving from Silver plans.

“There’s a lot yet to be seen, but there are definitely some early warning signs in terms of the decisions consumers are having to make in reaction to the changing federal policy,” Jessica Altman, executive director of Covered California, told the network.

Even more worrisome, however, is the number of Americans who are cancelling their ACA marketplace coverage altogether, because – all evidence suggests – they can no longer afford the premiums for any level of plan. In Pennsylvania, after families began receiving notices that – in many cases – their premiums had doubled, officials reported that about 40,000 people dropped their coverage, which is double the total from the 2024 enrollment period. What’s more, new enrollments in the Keystone State are also running about 20% lower than this time last year.

This is on top of a growing number of people – especially in the younger age brackets – who are switching to other low-cost alternatives that also are essentially a big gamble. These include so-called short-term plans, which are not compliant with ACA coverage requirements and that often come with annual or lifetime caps on coverage, don’t cover certain critical expenses like prescription drugs or paternity care and can penalize patients with preexisting conditions. There are also so-called catastrophic plans, which usually carry the maximum allowable deductible and which – in recognition of the worsening health insurance climate in the U.S. – have been expanded as an option to consumers over age 30. You may have even heard ads for faith-based sharing plans, whose members pool their expenses. People who sign up for those plans often find out they are not covered for a serious illness.

No wonder growing numbers of us are more anxious about the cost of health care than any time since the ACA was enacted in 2010 – perhaps ever. In November, a West Health-Gallup survey found that 47% of U.S. adults are worried they can’t afford health care next year – the highest number since the survey began in 2021. Those surveyed cited the rising cost of out-of-pocket requirements for prescription drugs in particular. And the number of Americans who say the cost of health care is causing “a lot of stress” in their daily lives has nearly doubled since the survey began, to 15%.

Georgetown’s Keith noted that – with patients and their families getting hit with higher costs on all sides – both the federal government and individual states have shown there are legislative actions that can reduce out-of-pocket costs for these anxious consumers. These include the federal No Surprises Act, which was signed into law by President Donald Trump in 2020 to address surprise medical bills, and a $2,000 annual cap on prescription drug costs for Medicare beneficiaries that went into effect in 2025 (it will rise to $2,100 this year), as well as various state efforts to curb tack-on facility fees or impose limits on insulin charges.

“There are many different flavors – ways that patients are getting charged,” Keith said. Indeed, that’s the bad news, since many of the fixes that lawmakers have been working on feel like bail-out buckets of water against a tsunami of rising medical expenses that in 2026 threaten the broader American economy, not to mention the national psyche.

Rising out-of-pocket expenses might be the looming health crisis that no one is talking about, but the lack of media coverage is likely to change over the course of 2026 as horror stories trickle in from those who gambled on not getting sick over the next 12 months – and lost that wager.

There’s a good chance your health insurance premiums are going up next year, regardless of where you get coverage.

Why it matters:

The spike in what millions of Affordable Care Act plan enrollees pay will be acute, but workplace insurance is getting more expensive, too — and all at a time when affordability is prominently on Americans’ minds.

ACA premiums have dominated the political discourse in Congress for weeks, but there’s no real sign that any relief is coming from Washington.

Even extending the Biden-era enhanced ACA subsidies — which most Republicans don’t want to do — would do nothing to address what’s driving the surging cost of care or employer insurance affordability issues.

And all signs point to Democrats hammering Republicans for high costs in all forms of health insurance leading up to next year’s midterm elections.

The big picture:

Health insurance gets more expensive almost every year, keeping up with increases in the costs of procedures, tests, drugs and more. But some years see bigger jumps than others, and 2026 is looking like one of those years.

That means tough choices for families, employers and workers all faced with shouldering higher premiums or out-of-pocket spending. Some will conclude it’s prohibitively expensive and go uninsured.

Another thing that’s different about this year is that the white-hot political rancor around ACA premiums is putting health insurance back centerstage politically.

By the numbers:

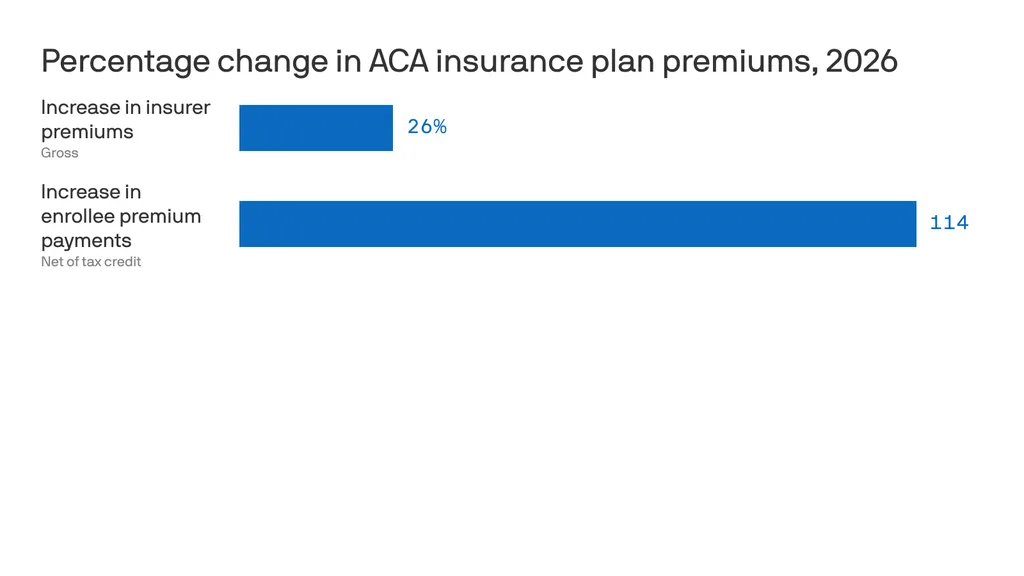

ACA insurers themselves are raising premiums by an estimated 26%, in part due to rising hospital costs, higher demand for pricey GLP-1 drugs like Ozempic, and the threat of tariffs.

But add in the loss of federal subsidies, and the increase is 114% — or more than double what they currently pay, according to KFF. 22 million out of 24 million marketplace enrollees now receive subsidies.

Premiums in the small group employer market will go up by a median of 11%, also per KFF, due to some of the same reasons insurers cite in ACA markets.

For employer health insurance, there’s no comprehensive data yet for 2026, but estimates from earlier this year put the increases in the high single digits.