Wall Street reacts to the failed ACA subsidy extension — and to the president’s swipe at “money sucking insurance companies.”

Wall Street got the jitters yesterday after Donald Trump’s pointed remarks about “money sucking insurance companies” and a Congressional deal that failed to extend the enhanced subsidies under the Affordable Care Act (ACA) marketplace plans. According to one market analysis, shares of Centene (CNC) plunged about 8.15% in pre-opening trade, while competitors such as Molina (MOH) fell 4.6%, Elevance (ELV) dropped 3.7%, UnitedHealth Group (UNH) slipped 1.9% and Humana (HUM) declined 1.45%.

Why the sell-off? Because the enhanced ACA subsidies — which reduce premiums for some marketplace enrollees — expire at the end of the year and without renewal, an estimated 3.8 million people could lose coverage, and premiums would rise significantly for others. Insurers that rely on the stability and growing enrollee base of the ACA marketplace face heightened risk when that funding is in question – especially when the dollars are guaranteed – like when they are shoveled out from the federal government.

Still, it’s worth noting that the ACA marketplace business is not the primary profit engine for most large payers. Their bigger gains typically come from taxpayer-funded programs like Medicare Advantage, Medicaid managed-care contracts and veterans’ / VA contracts.

Here’s how five of the major players fared in 2024 profits:

Centene: $3.2 billion (+590% since 2014)

UnitedHealth Group: $32.2 billion (+214% since 2014)

Elevance: $9.1 billion (+78% since 2014)

Humana: $2.6 billion (+8.3% since 2014)

Molina: $1.18 billion (+780% since 2014)

Because most of their gains have not come from ACA exchange plans (and especially not the thin margin employer market) but through their other government-subsidized businesses, investors can have some certainty their investments in those companies are still largely safe and Big Insurance will be able to weather this storm.

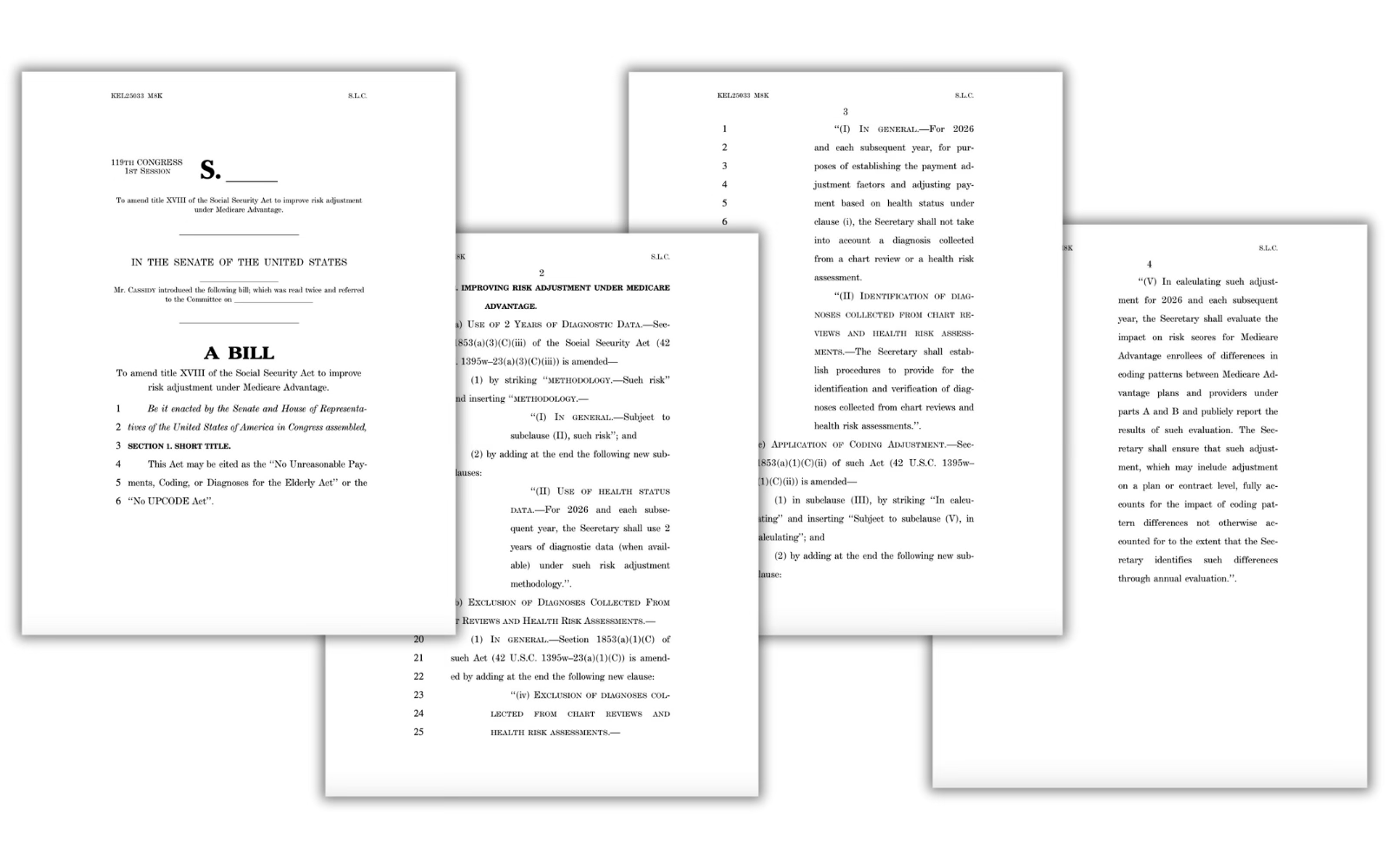

For instance, the industry has always been able to strongarm rough patches in the consumer market – as long as they can stave off any meaningful changes to their bread and butter taxpayer-funded programs. As we reported last month, the industry’s outside PR and lobbying friends – Better Medicare Alliance and Medicare Advantage Majority – have hit the airwaves and the halls of Congress to halt the advancement of the No UPCODE Act. The bipartisan bill, sponsored by Senators Bill Cassidy (R-LA) and Jeff Merkley (D-OR) would end wasteful, fraudulent practices in Big Insurance’s Medicare Advantage businesses that funnel taxpayer money into the pockets of industry executives and Wall Street shareholders and could save taxpayers as much as $124 billion over the next decade and keep the Medicare Trust Fund solvent for years longer.

As of this morning, insurers seem to be fairing better. Centene, UnitedHealth Group, Elevance, Humana and Molina are all back in the green.

As open enrollment begins and Congress remains deadlocked on whether to extend the ACA’s enhanced premium subsidies, one question looms large: Where does all the money we pay for health coverage actually go?

It’s a fair question. Premiums and out-of-pocket costs have risen relentlessly over the past decade. Since the Affordable Care Act was fully implemented, the average premium for an ACA marketplace plan has doubled, and the average deductible for a Silver plan has increased by 92%. Every year, families pay more, yet the coverage often feels thinner.

What the Insurers Say

Health insurance companies routinely claim these increases simply reflect rising medical costs and higher utilization. For example, when justifying rate hikes in 2024, Cigna of Texas wrote:

“The increasing cost of medical and pharmacy services and supplies accounts for a sizable portion of the premium rate increases.”

But the financial filings of these same companies tell a different story.

What the Numbers Show

As Wendell Potter recently wrote, from 2014 to 2024 the seven largest publicly traded health insurance companies, UnitedHealth Group, CVS/Aetna, Cigna, Elevance (formerly Anthem), Humana, Centene, and Molina, reported that they collectively made more than half a trillion dollars in profits.

That’s money collected from individuals, employers and taxpayers for health coverage — dollars that didn’t go to medical care but instead flowed to corporate shareholders and executive bonuses. To put this in perspective, those profits alone could fund the enhanced ACA premium subsidies for another ten years, at an estimated cost of $350 billion.

Over the same period, these seven companies spent $146 billion buying back their own stock or, in other words, using premium dollars from patients and employers to boost share prices and executive compensation (the CEOs and many other top executives of big insurers are compensated primarily through stock grants and options).

Stock buybacks don’t lower premiums, expand networks, or improve care. They simply make investors and executives richer. If that same money had been reinvested in enrollees, it could have provided premium-free health coverage to more than 5 million families for an entire year, based on the average employer-sponsored plan cost of $27,000 in 2026.

Lobbying With Our Premium Dollars

Insurers aren’t just rewarding shareholders, they’re also shaping the political system that protects their profits. Since 2014, the seven largest insurers and their trade association, AHIP, have spent $618 million on lobbying.

That’s money that could have been used to lower out-of-pocket costs or improve patient care, but instead it’s spent to influence Congress and federal agencies to maintain the status quo.

The Real Problem — and the Real Solution

As the cost of health insurance continues to climb, politicians debate how to control those costs and expand coverage. But the truth is, there’s already enough money in the system to cover everyone. It’s just being siphoned off by insurance corporations for profits, lobbying, and stock buybacks.

Though some have been calling for less regulation of Big Insurance, that is not the answer and is partly how we ended up in this situation. Right now, Big Insurance is allowed to use premium dollars and tax dollars on things that do nothing to improve anyone’s health – such as stock buybacks and lobbying – instead of on medical care.

Rather than asking families and taxpayers to pay more, it’s time to demand accountability from insurers. At a minimum, they should not be allowed to use premium dollars, or taxpayer dollars, to enrich shareholders through stock buybacks (which wasn’t even legal until the 1980s) or lobby for policies that drive up costs.

If we want to contain health care costs, the first step is simple: Stop the profiteering by Big Insurance.

For four years, people buying health care on the Affordable Care Act (ACA) marketplace have benefited from government subsidies that made their plans more inexpensive, and thus more accessible.

Now, those subsidies have become a key point of contention between Democrats and Republicans in a government shutdown that went into effect on Oct. 1 after both sides failed to reach a deal.

Democrats want Congress to extend the enhanced premium tax credits first added in 2021; without an extension, the tax credits expire at the end of 2025 and experts say premium prices could double in 2026.

“They know they’re screwed if this debate turns into one about healthcare. And guess what? That’s just what we’re doing. We are making this debate a debate on healthcare,” said U.S. Senator Chuck Schumer, a Democrat from New York, hours before the government shut down.

Republicans say that Democrats want to extend free health care for unauthorized immigrants, a talking point that is not true but that has nevertheless been repeated many times by GOP politicians. (Democrats want to reverse health policy changes that the GOP’s tax law enacted, including limits to federal funding for health care for “lawfully present” immigrants.)

Neither side appears ready to budge, which means that as of right now, people who buy health care on the Affordable Care Act (ACA) marketplace are about to be in for some sticker shock. Monthly out-of-pocketcosts are set to jump as much as 75% for 2026 because of the disappearance of federal subsidies and higher rates from insurers.

“Most enrollees are going to be facing a double whammy of both higher insurance bills and losing the subsidies that lower much of the cost,” says Matt McGough, a policy analyst at KFF for the Program on the ACA and the Peterson-KFF Health System Tracker.

KFF recently calculated that the median rate increase proposed by insurers is 18%, more than double last year’s 7% median proposed increase. But the actual blow to patients is going to be much higher. That’s because enhancements to premium tax credits are set to expire at the end of 2025.

Around 93% of marketplace enrollees—19.3 million people—received the enhanced premium tax credits, according to the Center on Budget and Policy Priorities, saving them $700 yearly on average. For some people, the tax credits meant that they wouldn’t have to pay an insurance premium if they chose certain plans. For others, it meant getting hundreds of dollars off a health plan they otherwise wouldn’t have been able to afford.

Premium tax credits helped people afford plans on the Affordable Care Act marketplaces between 2014 and 2021. Then, in 2021, enhancements to those premium tax credits went into effect with the American Rescue Plan. Before 2021, premium tax credits were only available to people making between 100-400% of the federal poverty limit—so between $25,8200 and $103,280 for a family of three in 2025. The enhanced tax credits were expanded to households with incomes over 400% of the federal poverty limit, and were also made more generous for everyone. That wide range meant they subsidized coverage for people who otherwise would not have gotten any break on their premiums.

The enhancements to the premium tax credits, which are set to expire at the end of 2025, significantly boosted enrollment in Affordable Care Act marketplace plans. More than 20 million people enrolled in marketplace coverage in 2024, according to the Center on Budget and Policy Priorities, up from 11.2 million in February 2021, before the enhancements to the tax credits.

With costs being lowered by half, individuals and families decided, ‘OK, maybe this is financially worthwhile,’” says McGough. “Whereas previously, they thought that they didn’t utilize that much health care, so it wasn’t worth it to purchase health care on the marketplaces.”

Why insurers want to increase rates

Every year, health insurers submit filings to state regulators that detail how much they need to change rates for their ACA-regulated health plans. KFF analyzed 312 insurers across 50 states and the District of Columbia; they found that insurers are requesting the largest rate changes since 2018.

They are requesting the median 18% increase for a few reasons, including rising health care costs, tariffs, and the expiration of the premium tax credit enhancements, KFF found. Health care costs have been rising for years, but insurers say that the cost of medical care is up about 8% from last year. They say that tariffs may put upward pressure on the costs of pharmaceuticals and that growing demand for GLP-1 drugs such as Ozempic and Wegovy is driving up their expenses.

Worker shortages are also driving health care costs up, according to the KFF analysis. It also found that consolidation among health care providers was leading to higher prices because those providers had more market power.

Everyone’s bottom line could be affected

When they went into effect, the enhanced premium tax credits pushed some people into the marketplace who might otherwise have been uncertain about whether to get health insurance. The tax credits were graduated so that people with the lowest incomes got the most help, but they also reached people with slightly higher incomes.

Many people don’t know that those enhancements to the premium tax credits are going away, says Jennifer Sullivan, director of health coverage access for the Center on Budget and Policy Priorities (CBPP). Her organization has been talking to people across the country about how they may be affected if Congress does not extend the enhancements, and has found that even increases of $100 or $200 a month may be enough to force some people out of the marketplace.

“It’s a huge increase in anyone’s budget, particularly at a time when groceries are up and the cost of housing is up and so is everything else,” Sullivan says.

There are other reasons the ACA marketplace may see fewer enrollees, she says. A handful of policies passed by Congress require more verification to enroll in ACA plans and cut immigrant eligibility, for example.

Fewer enrollees are bad news for everyone else. The people who are likely to drop coverage are those who don’t need it for lifesaving treatment or medicine. That means the pool of people who are still covered by ACA plans will be sicker and more expensive to care for.

“The people who are left are statistically more likely to be people with higher health care needs,” says Sullivan, with CBPP. “Those are the folks that are going to jump through extra hoops, whether it’s more paperwork or higher premiums or higher out-of-pocket costs, because they absolutely know they need the coverage.”

There are other society-wide effects to people dropping their health insurance coverage. Many uninsured people end up in emergency rooms for care because that’s their only option, and sometimes, they can’t pay. That increases the cost of health care for everyone else, says Sullivan.

Amy Bielawski, 60, is one of the people who is going to look at her options when rates for marketplace plans are listed in October and decide whether or not to enroll. Bielawski, an entrepreneur and entertainer who performs belly dancing at parties, has spent much of her life without health care.

She finally signed up for an ACA plan in 2019, and was able to go to a doctor and diagnose her hypothyroidism and uterine fibroids. Last year, because of the enhanced premium tax credits, she paid $0 a month in premiums—which will almost certainly go up.

“I’m afraid, I’m very afraid,” says Bielawski, who lives in Georgia. “I can’t wrap my head around it because there are so many things that can go wrong with my health.”

Where politicians stand now

Addressing this uncertainty is one key reason the Affordable Care Act passed in the first place in 2010. It has dramatically improved health coverage for Americans; nearly 50 million people, or one in seven U.S. residents, have been covered by health insurance plans through ACA marketplaces since they first launched in late 2013.

But it has also faced numerous challenges, and Republicans have long said that weakening or revamping the law is a high priority.

It’s unclear if the hassle of a government shutdown will make them change their tune. In September, Senate Majority Leader John Thune, a Republican from South Dakota, said he was open to addressing the expiration of the subsidies, but that he did not want to tie any of those policy changes to government funding measures. Sen. Mike Rounds, also a Republican of South Dakota, has suggested a one-year extension to the subsidies, after which the tax credits return to pre-pandemic levels.

Many Republicans appear determined to end the subsidies eventually, and their insistence on scaling back spending on health care policy seems to be having an impact.

Sullivan, with the CBPP, says that the changes to the Affordable Care Act and looming cuts to Medicaid have the potential to dramatically reduce the number of people able to afford regular medical care in the country. These cuts come at a time when key indicators like infant mortality rates and life expectancy rates are worsening.

“We are seeing a real weakening of that safety net that we spent the last 10-15 years fortifying,” she says.

The government shutdown has left many federal workers furloughed, caused nationwide flight delays, left small businesses unable to access loans and put nonprofit services in jeopardy. It’s only expected to get worse.

As Congress remains deadlocked over passing a stopgap measure to reopen the government, thousands of Americans are at risk of losing benefits from the Supplemental Nutrition Assistance Program (SNAP); the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC); and other programs at the beginning of November.

An additional burden on Americans is the start of open enrollment for the Affordable Care Act (ACA), also known as ObamaCare, on Nov. 1, where they will see more costly health insurance premium plans unless lawmakers act.

Democrats and Republicans have spent weeks pointing fingers at each other, with no deal in sight. The Senate on Tuesday failed to advance a Republican stopgap measure to end the shutdown for the 13th time, while the House was out of session and President Trump was traveling abroad.

With uncertainty around the shutdown’s timeline growing day by day, here are six ways Americans will start to feel more of the shutdown’s impact.

Federal employees

At least 670,000 federal workers have been furloughed while about 730,000 are working without pay as of Oct. 24, according to data from the Bipartisan Policy Center, a think tank based in Washington, D.C. The center estimates that if the shutdown continues through the beginning of December, federal civilian employees will miss roughly 4.5 million paychecks.

The American Federation of Government Employees (AFGE), the nation’s largest federal workers union, urged Congress to pass a “clean” funding measure known as a continuing resolution to reopen the government. AFGE President Everett Kelley said in an Oct. 27 statement, “No half measures, and no gamesmanship. Put every single federal worker back on the job with full back pay — today.”

“I get where they’re coming from. We want the shutdown to end too. But fundamentally, if Trump and Republicans continue to refuse to negotiate with us to figure out how to lower health care costs, we’re in the same place that we’ve always been,” Sen. Tina Smith (D-Minn.) told The Hill on Tuesday.

SNAP and WIC

The U.S. Department of Agriculture (USDA) said benefits won’t be issued on Nov. 1 for SNAP, a program that helps low-income families afford food. Nearly 42 million Americans rely on SNAP benefits every month, according to data from the USDA.

Though the USDA formed a plan earlier this year that said the department is obligated to use contingency funds to pay out benefits during a shutdown, it has since been deleted. The USDA wrote in a memo this month that the contingency fund is only designed for emergencies such as “natural disasters like hurricanes, tornadoes, and floods, that can come on quickly and without notice.”

Democratic officials in more than two dozen states sued the Trump administration this week, arguing the USDA is legally required to tap into those funds. But House Speaker Mike Johnson (R-La.) has claimed those funds are not “legally available.”

Families who rely on WIC, a program that provides food aid and other services to low-income pregnant and postpartum women, infants, and children younger than 5 years old, could also face trouble. The White House had provided $300 million to WIC to keep the program afloat in early October. But 44 organizations signed on to an Oct. 24 letter from the National WIC Association to the White House requesting an additional $300 million in emergency funds, warning that “numerous states are projected to exhaust their resources for WIC benefits” on Nov. 1.

Military pay

Payday is coming up at the end of this week for members of the military.

Earlier this month, Trump directed Defense Secretary Pete Hegseth to “use all available funds” to pay troops. Officials ended up reallocating $8 billion in unspent funds meant for Pentagon research and development efforts toward service members’ paychecks. The administration also received a $130 million donation from a private donor to help cover military members’ paychecks.

Vice President Vance said he believes active-duty service members will get paid this Friday. But Treasury Secretary Scott Bessent told CBS News’s Margaret Brennan on Sunday that troops could go without pay on Nov. 15 if the shutdown continues.

Senate Democrats blocked a bill sponsored by Sen. Ron Johnson (R-Wis.) earlier this month to pay active-duty members and other essential federal workers.

ACA subsidies

At the center of the shutdown fight is the ACA subsidies, which are set to expire at the end of this year. Democrats have been urging Republicans to extend the subsidies, arguing that ACA health insurance premium costs will increase if no action is taken.

Americans can choose their insurance plans for next year on the federal Affordable Care Act exchange website starting Saturday. An analysis from KFF found that without the subsidies extended, Americans will see their marketplace premium payments increase by 114 percent.

Republicans have been firm in their position of reopening the government first before discussing the ACA subsidies.

“The expiring ObamaCare subsidy at the end of the year is a serious problem. If you look at it objectively, you know that it is subsidizing bad policy. We’re throwing good money at a bad, broken system, and so it needs real reforms,” Speaker Johnson said at a Monday press conference.

Head Start

About 140 Head Start programs across 41 states and Puerto Rico serving more than 65,000 children could go dark if the shutdown goes past Nov 1., according to a joint statement from more than 100 national, state and local organizations focused on childhood education and development.

“Without funding, many of these programs will be forced to close their doors, leaving children without care, teachers without pay, and parents without the ability to work,” the statement says.

Head Start programs are designed to help low-income families and their children from birth to age 5 with a focus on health and wellness services, family well-being and engagement and early learning, according to its website.

Nonprofits

Diane Yentel, president and CEO of the National Council of Nonprofits, told The Hill in a statement that the shutdown has forced many nonprofits to halt their operations because of frozen federal reimbursements and grants.

The nonprofits include those handling wildfire recovery in Colorado, housing vulnerable youth in Utah and helping with conservation work in Montana, Yentel said. Many federal workers without pay have also turned to their local food banks, further putting a financial strain on nonprofits.

“With the November 1 cutoff of SNAP and WIC looming, the situation will get even worse. Nonprofit food banks are already facing rising grocery costs and increased demand, including from federal workers and military families,” Yentel said. “If millions of Americans suddenly lose access to these life-saving nutrition programs, local nonprofits will be overwhelmed, and far too many seniors, children, and families will go without help.”

We learned yesterday that the average cost of a family health insurance policy through an employer reached nearly $27,000 this year, 6% higher than what it cost in 2024. As if that weren’t alarming enough, researchers are predicting that the total likely will soar toward $30,000 next year because of rising medical costs and the unrelenting pressure insurers are under from Wall Street to increase their profits. Small businesses will be hit the hardest.

Despite repeated assurances from insurers that we can count on them to hold down the cost of health care – and consequently the premiums they charge – there are now many years of evidence – from researchers like KFF, which tracks annual changes in employer-sponsored coverage – that they have not and cannot deliver on their promises.

Nevertheless, Big Insurance is doing just fine financially as they force America’s employers and workers to shell out increasingly absurd amounts of money for policies that actually cover less than they did ten years ago. A health insurance policy today is generally less valuable than it was a decade ago because families have to spend more and more money out of their own pockets every year before their coverage kicks in. In addition, they are far more likely to be notified that their insurers will not cover the care their doctors say they need.

When you look at KFF’s reports over time, you’ll see that the cost of a family policy has increased 60% since 2014 when it cost an average of $16,834. That is a rate of increase much higher than general inflation and also higher than medical inflation.

Not only has the total cost of an employer-sponsored plan skyrocketed, so has the share of premiums workers must pay. This year, employers deducted an average of $6,850 from their workers’ paychecks for family coverage, up from $4,823 in 2014, a 42% increase.

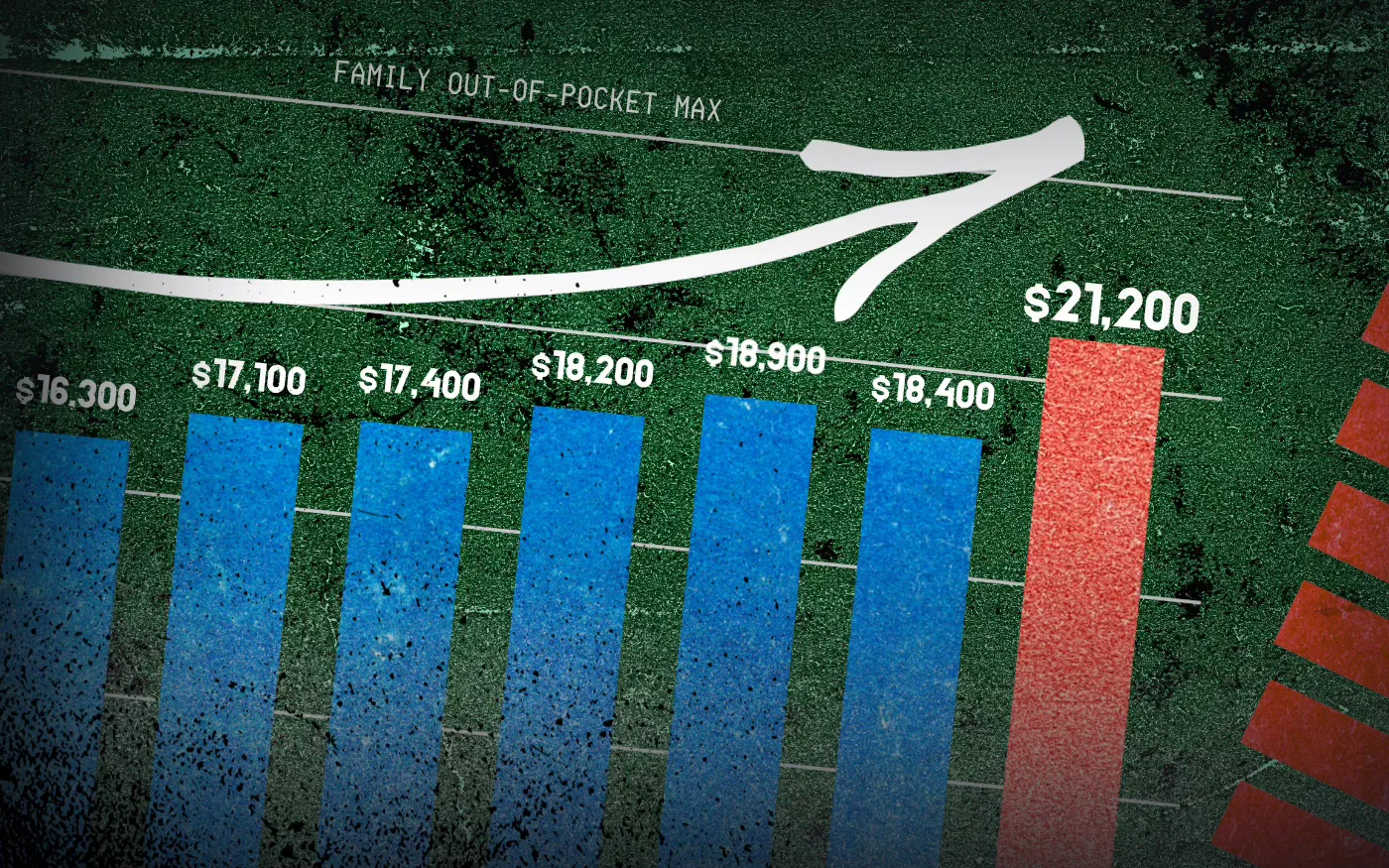

And as premiums have risen, so has the amount of money workers and their dependents are required to spend out of their pockets in deductibles, copayments and coinsurance. The Affordable Care Act, to its credit, instituted a cap on out-of-pocket expenses in 2014, but that cap has been increasing annually along with premiums. (The U.S. Department of Health & Human Services sets the out-of-pocket max every year, pegging it to the average increase in premiums.)

In 2014 the out-of-pocket cap for a family policy was $12,700. Next year, it will rise to $21,200 – a 67% increase. And keep in mind that the cap only applies to in-network care. If you go out of your insurer’s network or take a medication not covered under your policy, you can be on the hook for hundreds or thousands more. While most employer-sponsored plans have caps that are considerably lower, many individuals and families reach the legal max every year.

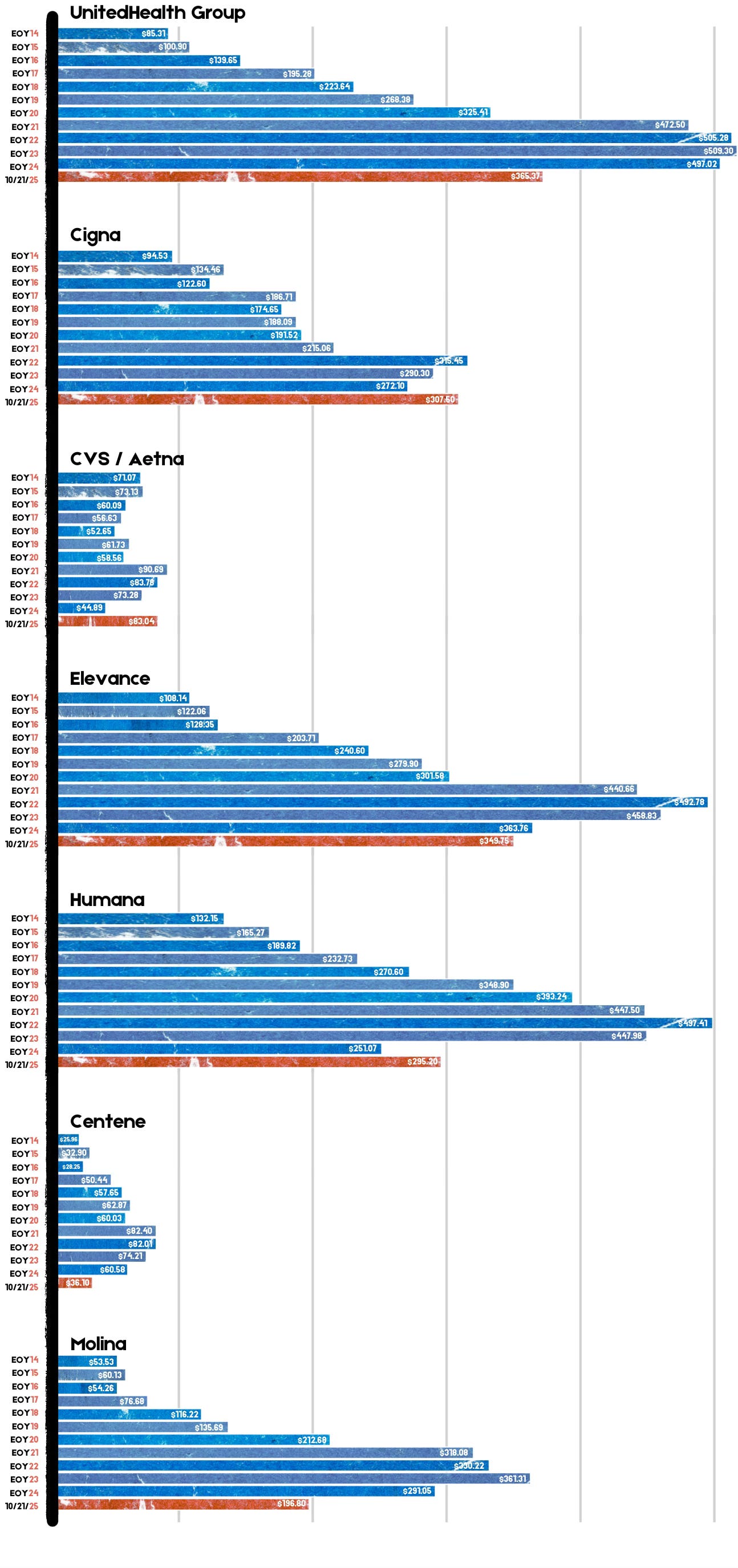

Meanwhile, the seven biggest for-profit health insurers have made hundreds of billions in profits since 2014 as they have jacked up premiums and out-of-pocket requirements and erected numerous barriers, including the aggressive use of prior authorization, that make it more difficult for Americans to get the care and medications they need. Collectively, those seven companies made $71.3 billion in profits last year alone. That was up slightly from $70.7 billion in 2023. Insurers said their 2024 profits were somewhat depressed because more of their health plan enrollees went to the doctor and picked up their prescriptions last year. Investors were furious that insurers couldn’t keep that from happening, as you’ll see in the charts below. Many of them sold some or all of their shares, sending insurers’ stock prices down. But overall, the stock prices of the big insurance conglomerates have increased steadily over the years as we and our employers have had to spend more for policies that cover less.

For example, UnitedHealth Group, the biggest of the seven, saw its stock price increase 483% between 2014 and 2024 – from $85.31 a share on Dec. 31, 2014, to $497.02 on Dec. 31, 2024. Most of the other companies saw similar growth in their shares over that time period.

By contrast, the Dow Jones Industrial Average increased 139% (from $17,823.07 to $42,544.22), and the S&P 500 increased 186% (from $2,058.90 to $5,881.63) during the same period.

Back to those premiums and out-of-pocket requirements. While the KFF numbers pertain to employer-sponsored coverage, people who have to buy health insurance on their own – mostly through the ACA (Obamacare) marketplace – have experienced similar increases. Most Americans who buy their insurance there could not possibly afford it if not for subsidies provided by the federal government on a sliding scale, which is based on income. The most generous subsidies have been available since 2014 to people with income up to 150% of the federal poverty level (FPL). During the pandemic, Congress expanded – or “enhanced” – the subsidies to make them available to people with incomes up to 400% of FPL. Those enhanced subsidies are scheduled to expire at the end of this year. Whether to let them expire or extend them is at the center of the ongoing government shutdown. Most Democrats are insisting they be extended while most Republicans want them to end. It’s important to note that the federal money goes to insurance companies, not to people enrolled in their health plans.

If the enhanced subsidies do end, millions of Americans who get their health insurance through the ACA marketplace will drop their coverage because the premiums will be unaffordable for them and their families. In Pennsylvania where I live, premiums for policies bought on the state’s insurance exchange are expected to increase 102% next year because of the anticipated end of the subsidies and premium inflation.

More than 24 million Americans now get their coverage through the ACA marketplace, primarily because their employers cannot offer health insurance as an employee benefit anymore. Over the past several years, a growing number of small businesses have stopped offering subsidized coverage to their workers because of the expense. Just slightly more than half of U.S. businesses are still in the game. The rest simply can’t afford the premiums. Small businesses can expect an average increase of 11% next year with some of them facing increases of 32%.

It is becoming more clear every passing year that the U.S. has one of the most insidious ways of rationing care. It is rationed based on a person’s ability to pay far more than on a person’s need for care. And among those most disadvantaged by the current system are hard-working low- and middle-income Americans with chronic conditions and those who suddenly get sick or injured.

While the Affordable Care Act prohibited insurers from charging people with pre-existing conditions more than healthier people, insurers have figured out a back door way to discriminate against them: by making them pay hundreds or thousands of dollars out of their own pockets every year – in addition to their premiums – and also by refusing to cover treatments and medications their doctors say they need.

Now you know why Big Insurance is doing so well while the rest of us are getting

Average annual premiums for single health coverage

A grouped column chart comparing average annual premiums for single coverage from 2018 to 2025 for ACA benchmark plans and employer-sponsored plans. Both plan types have increased in cost since 2018. In 2024, ACA benchmark plans were $5.7k annually while employer-sponsored plans were almost $9k on average. No data is available for employer-sponsored plans in 2025.

Something big isbeing missed in the congressional showdown over enhanced Affordable Care Act subsidies: Health insurance premiums are eye-wateringly expensive for the average person without some kind of subsidy.

Why it matters:

Health care in the U.S. is expensive, we know, we’ve all heard it a million times. But most of us don’t really feel its full expense, which removes a lot of the urgency to truly address health care costs.

Whether it’s through government tax credits or employer premium assistance, most Americans with private health insurance don’t pay the entirety of their premium.

But we’re all paying the freight one way or another, either through taxes or paycheck deductions.

State of play:

The past few weeks have been full of dire warnings from Democrats and their allies about what will happen if the enhanced ACA subsidies from the pandemic era are allowed to expire at year’s end.

The gist is that millions of Americans will have sticker shock when they’re exposed to more or all of the premium cost, and many will ultimately opt out of buying coverage. That’s all probably true.

Of course, allowing the enhanced subsidies to expire would just make the law’s structure revert to its original state.

And that’s why some savvy Republican-aligned commenters are asking if that means the ACA is broken, or if the original version was unworkable.

Reality check:

Premiums have gone up — a lot, in some cases. But that’s not unique to the ACA marketplace, and premiums are even pricier in the employer market.

By the numbers:

This year, the average premium for a benchmark ACA plan is $497 a month, or nearly $6,000 a year, according to KFF.

The average employer-employee premium for single coverage was $8,951 last year, also according to KFF.

The average premium for family coverage was a whopping $25,572.

Let’s do some math.

Without any form of subsidization, a single person making $60,000 would spend 10% of pretax income on an ACA plan, and 15% on an employer plan.

Now let’s say that $60,000 income is supporting a family of four. The average premium without subsidies would cost that family 43% of its pretax income.

The median U.S. family income, according to the Census Bureau, was $83,730 in 2024. Health insurance premiums would be 31% of pretax income.

Between the lines:

The definition of “affordable” is obviously very subjective, but it seems safe to say that some of these numbers — especially for families — aren’t meeting it.

What we’re watching:

Open enrollment is coming, and people with ACA coverage aren’t the only ones facing premium increases.

Health benefit costs are expected to increase 6.5% per employee in 2026, according to Mercer. Many employers are planning to limit premium increases by raising out-of-pocket costs for employees.

On average, ACA marketplace plans are raising premiums about 20% in 2026, according to KFF.

How much of that increase gets passed on to enrollees will depend on whether the enhanced subsidies are extended, but the premium increases are partially due to insurers having accounted for the subsidy expiration.

The bottom line:

Policymakers have two broad options: They can keep fighting over who pays for what, or they can do bigger, systemwide reform.

If you’re waiting for the latter, don’t hold your breath!

Medicare Advantage Majority and Better Medicare Alliance are flooding the zone with attacks against bipartisan legislation aimed at curbing health insurers’ “upcoding” maneuver.

HEALTH CARE un-covered readers were the first to tip me off to television attack ads against the bipartisan No UPCODE Act, sponsored by Senators Bill Cassidy (R-LA) and Jeff Merkley (D-OR). The ads in question, airing in the Washington D.C. media market, were paid for byMedicare Advantage Majority (MAM), which bills itself as a patient and provider coalition but has all the markings of a front group funded by the nation’s largest health insurers.

After a quick search through MAM’s YouTube channel, I think I found the ad I was tipped about. Titled “Voices,” the video features six seniors fawning over their Medicare Advantage plans – and it ends with a desperate plea to “oppose the No UPCODE Act” and “protect Medicare Advantage.”

MAM appears to have been propped up fairly recently – with their earliest ad (that I can find) from October 2024. All of their ads support Medicare Advantage. Some appear nonpartisan, while others are more overtly political, like the ad “Biden’s Playbook.” Here is a transcription of that ad:

“President Trump kept his promise to protect Medicare benefits for millions of American seniors. But now some in Congress want to take a page out of Joe Biden’s playbook and cut Medicare. These cuts threaten primary and preventative care that help keep millions of seniors healthy while also raising costs.

It’s a betrayal. It’s why people don’t trust Washington. Don’t let the politicians cut Medicare. Tell Congress to stand with President Trump and protect America’s seniors.”

None of MAM’s ads mention the expensive hidden fees, narrow networks of doctors and life-threatening prior-authorization hurdles often associated with private Medicare Advantage plans. Nor does it even hint at why Sen. Cassidy, a doctor and senior Republican leader and committee chair, introduced the No UPCODE Act in the first place: to reduce the tens of billions of dollars in overpayments to Medicare Advantage insurers and keep the Medicare Trust Fund solvent for years longer. Those overpayments – at least $84 billion this yearalone – is a leading reason why the Medicare Trust Fund is being depleted.

But Medicare Advantage Majority is not the only insurance industry front group flooding the zone.

I kid you not, while I was writing this very article I got a text from a different Big Insurance-funded group fear-mongering the same “cuts” to Medicare Advantage. As I’m typing away on my laptop, my phone dings… The first words in the text read: “ATTENTION NEEDED:”. The message had all the hallmarks of a cookie-cutter political blast that was cooked up by some DNC-alum or K Street PR strategist.

When I followed the prompt and clicked on the link, it took me to one of the industry’s most trusted hands in the Medicare Advantage fight, the Better Medicare Alliance (BMA) – one of my former colleagues’ most essential propaganda shops these days.

BMA is a slickly branded PR and lobbying shop that presents itself as a coalition of “advocates” working to protect seniors’ care, but it’s heavily funded by private insurers in the MA business who reap billions in those overpayments from taxpayers each year. BMA’s board has been stacked with Humana and UnitedHealth representatives and allies tied to medical schools like Emory and Meharry Medical College. For years, they’ve spent millions lobbying and propagating to protect MA insurers’ profits. This includes rallying against the No UPCODE Act since July; opposing CMS’ risk adjustment model in 2024 (which should help reduce some of the overpayments); and objecting vigorously to any Medicare Advantage plan payment reductions, year in and year out.

In short, BMA and MAM are both 501(c)(4) “social welfare” nonprofits used by Big Insurance as part policy shop, part lobbying arm, and part attack dog. Together, they make up a strategy for insurers that want to keep their MA cash cows gorging on your money.

None of this is new, though. It’s the same PR crap I used to fling back in the old days when I was an industry executive and had to peddle Medicare Advantage plans. (Its deliciously ironic that MAM had the audacity to use the term “playbook” in one of its ads. In my old job I used to help write the industry’s playbook.) Each fall we’d work with AHIP (formerly America’s Health Insurance Plans) to host “Granny Fly-Ins” in Washington, D.C. Industry money (actually, taxpayer money) would cover the fly-in expenses, and the seniors would trot around Capitol Hill to extol the supposed benefits of Medicare Advantage plans and dare lawmakers to tamper with it. And that tactic worked for years. Of course, this was all before texting existed.

The squeal tells the story

For years, MA insurers have exaggerated how sick their patients are on paper (making them seem sicker so they can get a bigger taxpayer-funded handout). Hence the term “upcoding.” And the sick joke is – unfortunately – the same insurers who profit most from this upcoding scheme are using their taxpayer loot to stop this bill from gaining traction.

I think the industry’s squeal tells the story.

Let’s be real: Big Insurance wouldn’t be running this PR and lobbying blitz unless this legislation really would do some major good for Americans. The No UPCODE Act is a strong, bipartisan step toward ending wasteful, fraudulent practices that funnel taxpayer money into the pockets of industry executives and Wall Street shareholders. This one bill could save taxpayers as much as $124 billion over the next decade and keep the Medicare Trust Fund solvent for years longer.

You can be sure, though, that people on Capitol Hill and the administration already know ads like these are industry-funded. They see them for what they really are — part of a well-financed intimidation campaign. A game. Running ads like these is the industry’s way of flaunting its power and a reminder that big money can and will be spent in Congressional campaigns — and possibly (again) even during the Super Bowl — to mislead voters.

So remember, when you see an ad or get a text from an organization like MAM or BMA – know that these organizations have a lot to lose if legislation like the No UPCODE Act becomes law. And spending your premium and tax dollars on text blasts and TV spots are well worth the investment – to them, anyway.

Recent analysis of spending data from five states with health care cost growth targets—Connecticut, Delaware, Massachusetts, Oregon, and Rhode Island—revealed an unexpected trend in 2023: Spending grew sharply in service categories that have historically increased more slowly. The most notable increase was in non-claims payments—payments made through financial arrangements between providers and health insurers that are not tied to individual claims. These payments rose by an average of 40.4 percent across the five states, driven largely by increases in Medicare Advantage non-claims spending.

Increases in non-claims payments are often seen as a positive sign. They suggest a shift away from fee-for-service payments toward alternative payment methods (APMs)—value-based payment models that incentivize care coordination, efficiency, and a focus on outcomes. However, it’s unclear what is included in these non-claims payments. A closer examination of this issue revealed a less visible but important concern: the role of insurer-provider vertical integration in potentially weakening the effectiveness of Medical Loss Ratio (MLR) requirements for insurers.

MLR Requirements

Medical Loss Ratio is a measure of the percentage of premium dollars that a health insurer spends on medical care and quality improvement activities—as opposed to administration, marketing, or profit. Since 2011, the Affordable Care Act has required insurers to maintain an MLR of at least 80 percent in the individual and small group markets, and 85 percent in the large group market. That is, for every dollar spent by an insurer, 80 cents or 85 cents—depending on the market—must go toward actual care and improvement. Insurers that don’t meet these required thresholds must pay a rebate to consumers for the premium dollars that were not spent on health care, less taxes, fees, and adjustments. In 2014, the Centers for Medicare and Medicaid Services instituted a requirement for Medicare Advantage and Part D plans; they must maintain an MLR of at least 85 percent or rebate any excess revenues to the federal government.

These MLR requirements aim to ensure that the majority of premium revenue is used to deliver or improve care. However, a significant loophole allows insurers that have “vertically integrated” with providers to inflate reported medical spending. This reduces their rebate liability while increasing held profits. Since the MLR provisions took effect in 2012, an estimated $13 billion in rebates have been issued—highlighting the strong incentive insurers have to minimize these payouts.

The MLR Loophole

A company is vertically integrated when it owns or controls more than one entity in the supply chain. For insurers, this means acquiring physician practices, outpatient clinics, and even entire health systems. As a result of this vertical integration, payments to these affiliated providers count as medical spending when calculating an MLR for the insurer. However, there is no MLR requirement for providers. This creates an incentive for the insurer to direct spending to these affiliated provider entities, which may charge inflated prices, allowing the insurer to increase its reported MLR without delivering more care or improving quality.

Consider a hypothetical scenario: Company X owns Health Insurer A and Clinic Y. There’s another health insurer, B, in the market, but it is not owned by Company X. It costs Clinic Y $300 to deliver a particular service.

When a patient covered by Health Insurer B receives this service at Clinic Y, Insurer B pays the clinic $300 for delivering the service. But when another patient covered instead by Health Insurer A receives the same particular service at Clinic Y, Health insurer A pays the clinic a lot more: $500. The full $500 is counted as medical spending in Health Insurer A’s MLR calculation, even though the additional $200 didn’t buy any more services or any better care. It just represents internal profit for the vertically integrated entity, Company X, that is captured on the provider side of the business, and not true care delivery (see exhibit 1 below).

Exhibit 1: Incentives for vertically integrated insurers to direct spending to these affiliated provider entities

Source: Authors’ analysis.

The structure of APMs exacerbates this problem by making it easier to mask price increases. In fee-for-service systems, a price increase shows up directly. However, in APM payments that are per capitation or per episode, providers receive lump-sum payments for a group of services or a population. There is no service breakdown for these APMs. These lump-sum payments can facilitate investment in population health improvement, but if vertically integrated entities are exploiting the MLR loophole by increasing internal payment rates, the use of APMs make such profit maximization easier to conceal.

This dynamic reveals a limitation of the MLR rules. When the insurer is also the provider, there is less transparency into how health care dollars are actually allocated. The vertically integrated insurer and provider entity can also artificially inflate prices for medical services, worsening the nation’s health care affordability problem.

Potential Impact

Currently, there is no standardized way to assess the extent to which insurers that own or are otherwise affiliated with clinics and health systems are taking advantage of this loophole, or how much the practice contributes to high health care prices. However, with the growing trend toward insurer-provider vertical integration, the potential cost implications are significant.

Insurers That Own Providers Capture A Significant Share Of Commercial And Medicare Advantage Enrollment

In the large-group commercial market, the three largest insurers—Kaiser Permanente, UnitedHealthcare, and Elevance—held a combined 39 percent of the national market share in 2023. In the Medicare Advantage market, the top five plans—UnitedHealthcare, Humana, CVS Health/Aetna, Elevance, and Centene—accounted for 68 percent of total enrollment in 2023.All of these insurers operate within larger parent companies that own or control a range of health care provider entities.

For example, UnitedHealth Group, UnitedHealthcare’s parent company, also owns OptumHealth, which employs or manages more than 90,000 physicians across the country. The recently released Sunlight Report on UnitedHealth Group shows that it grew more than 10 times its size over the past decade, and the company now consists of nearly 3,000 distinct legal entities.

UnitedHealth Group is not the only insurer pursuing this strategy of vertical integration. Elevance Health (formerly Anthem, Inc.) owns Carelon, a health services provider that claims to serve one in three people in the US. CVS Health encompasses retail pharmacy storefronts (CVS Pharmacy), a pharmacy benefits manager (CVS Caremark), a health insurer (Aetna), in-store clinics (MinuteClinic), and provider groups such as Oak Street Health and Signify Health. This high level of consolidation gives these companies significant control over how care is delivered, priced, and reported.

Transactions Between Insurers And Their Affiliated Provider Entities Are Substantial And Growing

A 2022 analysis by the Brookings Institution suggests that in Medicare Advantage plans, internal transactions between affiliated insurers and providers can account for spending that ranges from about 20 percent to as much as 71 percent of the total. Cost growth target states’ reports on 2023 spending growth appear to confirm these trends within the Medicare Advantage market. Upon examination of the drivers behind the sharp increases in non-claims payments, a clear pattern emerged. In Connecticut, UnitedHealthcare launched a program that paid its affiliated provider group, which was then called OptumCare Network, a fixed percentage of Medicare Advantage premiums to cover care and care coordination. Oregon reported that the rise in Medicare Advantage non-claims payments was largely due to UnitedHealthcare shifting a significant share of its claims payments into non-claims spending through Optum.

These trends are not limited to Medicare Advantage, however. UnitedHealth and other major insurers such as Elevance and Aetna operate across multiple markets, raising concerns about similar dynamics in the commercial market. A recent analysis by Seth Glickman, a physician and former insurance executive, shows that in the past five years, UnitedHealth Group’s reported corporate “eliminations”—intercompany revenues reported in its consolidated financial statements that represent all books of business—more than doubled, increasing from $58.5 billion to $136.4 billion. At the same time, the share of Optum’s revenue derived from UnitedHealthcare, as opposed to unaffiliated entities, increased by nearly 50 percent.

Prices Of Health Care Services From Vertically Integrated Insurers And Providers Are Higher Than Prevailing Market Prices

Growing evidence also suggests that insurers are paying more for services provided through their affiliated entities than for those delivered by non-affiliated entities. A STAT News investigation revealed that UnitedHealth Group reimburses its own physician groups considerably more than other providers in the same markets for the same set of services. Similarly, a Wall Street Journal investigation showed how certain insurers and pharmacy benefit managers are generating substantial profits by overcharging for generic drugs within their own networks. The analysis found that for a selection of specialty generic drugs, Cigna and CVS’s prices were at least 24 times higher, on average, than the drug manufacturers’ prices.

Stronger Oversight Is Needed

The potential impact of these trends is so significant that policy makers are beginning to take notice. In 2023, Senators Elizabeth Warren (D-MA) and Mike Braun (R-IN) requested that the Department of Health and Human Services Office of Inspector General evaluate the extent to which vertical integration is increasing costs and allowing insurers to bypass federal MLR requirements. Earlier this year, Representatives Lloyd Doggett (D-TX) and Greg Murphy (R-NC) submitted a bipartisan request to the Government Accountability Office—Congress’s independent, nonpartisan oversight agency—urging an investigation into the same issue in Medicare Advantage. It is unclear whether these investigations have been initiated.

Some states—understanding the role that market consolidation plays in driving up health care prices—have made efforts to strengthen oversight. In 2024, 22 states passed laws related to health system consolidation and competition. However, historically, these efforts have largely focused on promoting competition, preventing monopolies, and limiting dominant providers’ ability to charge prices well above competitive levels. Little attention has been given to the MLR loophole and the ability of vertically integrated insurers to report profits as medical care.

As states pursue policies to slow cost growth, they must apply greater scrutiny of vertical integration arrangements—especially around internal financial transactions between affiliated entities. States should require insurers to report detailed information on transactions between related parties, including non-claims-based APMs to affiliated providers and the pricing methodology used to develop these APMs. This reporting could be integrated into states’ premium rate review processes, allowing regulators to assess whether such transactions reflect actual medical costs. States could then modify or deny rate increases where evidence points to gaming of MLR rules.

Policy makers should also reassess whether, given these market dynamics, current regulatory tools such as the MLR are adequate. Addressing these issues will be essential for maintaining the integrity of cost containment efforts and ensuring that health care dollars are spent on delivering meaningful care.

Lawmakers weigh extending enhanced subsidies that keep plans affordable while grappling with calls to curb hidden costs and insurer abuses.

There’s some real political drama brewing in Washington, and the outcome will determine whether millions of Americans will be able to keep their health insurance. I’m not talking about Medicaid or Medicare but the 24 million Americans who are not eligible for either of those programs or even for coverage through an employer.

As the federal government barrels toward its Sept. 30 shutdown deadline, Democrats say they won’t vote to keep the government open unless Republicans agree to extend the subsidies that make coverage available through the Affordable Care Act (ACA) marketplace more affordable for individuals and families who get their health insurance there. At the heart of the debate are the so-called “enhanced” subsidies that were put in place during the Covid pandemic. Those subsidies are set to expire at the end of this year. If they do, more than 90% of people who buy coverage in the ACA marketplace will have to pay a whole lot more for it next year.

Republicans, who control Congress, are split. Hardliners want the subsidies to disappear, but a growing faction of GOP lawmakers see the political peril staring them in the face: Millions of their constituents will receive marketplace renewal notices with eye-popping premium hikes as open enrollment begins Nov. 1, and they likely will blame Republicans for those hikes.

Virginia Republican Rep. Jen Kiggans has even taken the lead on a one-year extension bill, warning that “people will get a notice that their health care premiums are going to go up by thousands of dollars” if Congress doesn’t act. A July GOP poll found that letting the subsidies lapse could tank Republicans’ midterm prospects.

“The Republicans have to come to meet with us in a true bipartisan negotiation to satisfy the American people’s needs on health care or they won’t get our votes, plain and simple”.

Why extending the subsidies matters — but why it shouldn’t be a blank check

When I was an insurance executive, I used to champion high deductible health plans and steep out-of-pocket costs, arguing Americans needed to have “more skin in the game.” The industry sold Congress on that logic during the ACA debates – and it worked. Lawmakers not only set the law’s out-of-pocket (OOP) maximum high from the start, they also – at the insurance industry’s insistence – let it rise to new heights every year.

The result? That cap ballooned 67% between 2014 and 2025. And in 2026, the max will reach $10,600 for an individual and $21,200 for a family. That means most ACA plans leave people exposed to thousands of dollars in medical bills even after they’ve paid their premiums. And the people who get burned the most are those with chronic illnesses or sudden serious diagnoses – or even an accident.

If the subsidies vanish, the nonpartisan Congressional Budget Office projects about 4 million people will drop out of ACA plans in the first year. People will get sicker. Some will die sooner.

But let’s not kid ourselves: Simply shoveling more taxpayer money into insurers’ coffers is not a solution. These same companies are already awash in tax dollars through their private Medicare Advantage plans, Medicaid contracts, and even the VA.

The concessions for subsidy extension

Here’s the tradeoff Congress should demand: Insurers can get the subsidies (which go straight to them), but only if they agree to put some of their own skin in the game. And they have plenty of it. Just the seven largest for-profit health insurers reported more than $71 billion in profits last year.

Specifically, lawmakers should:

Cap out-of-pocket costs on ACA plans. Apply the same protections Congress just gave to Medicare beneficiaries: a $2,000 cap on prescription drugs AND a $5,000 overall cap on annual out-of-pocket costs. That would be a seismic shift, bringing ACA plans closer to what Americans think they’re buying when they pay for “coverage.”

Crack down on prior authorization abuse. Prior authorization delays and denials are rampant in ACA plans, just as they are in Medicare Advantage. If taxpayers are footing the bill, patients should get timely care — not insurer red tape.

Fix ghost networks. Insurers routinely list doctors who aren’t actually accepting new patients or aren’t even in-network. Regulators should require accurate, verified networks so people can actually see the providers they’re paying to have access to.

My former Big Insurance colleagues will howl and launch a massive propaganda campaign when these ideas gain traction, claiming they’ll have to jack up premiums even more than they usually do if they have to be even slightly more patient-friendly. I know because I used to plan and execute the industry’s fear-mongering campaigns. Don’t fall for it this time or ever again. Those seven giant insurers took in more than 1.5 trillion dollars and shared more than $71 billion of their windfall with their already rich shareholders last year alone. Yes, the industry’s lobbying will be intense. But if members of Congress do the right thing, they won’t just preserve coverage for millions, they will finally start forcing insurers to compete on value, not just premium retention.

What comes next

If Democrats are going to play hardball by threatening a government shutdown if Republicans don’t extend these ACA subsidies, they should make it count. Americans need relief not just on premiums, but on the crushing costs hidden behind their insurance cards.

If Trump and RFK Jr. want to crack down on deceptive health care ads, they should start with the avalanche of misleading Medicare Advantage commercials blanketing seniors every fall.

The Trump administration announced last week it plans to crack down on prescription drug advertising. In reporting on the news, the New York Times quoted former Food and Drug Administrator David Kessler as saying that what the administration is proposing “would in essence remove direct-to-consumer advertising from television.”

In a press release, Health and Human Services Secretary Robert F. Kennedy Jr. said the intent is to “shut down that pipeline of deception and require drug companies to disclose all critical safety facts in their advertising.”

You’ll get no argument from me that companies of any kind, especially those that make money in health care, should not be allowed to deceive the public by withholding critical facts.

What I do argue – and hope this administration and Democrats in Congress will agree on – is that this crackdown should also include so-called Medicare Advantage ads.

As we get close to “open enrollment” season, the period of time every fall when seniors and people with qualifying disabilities can choose between Traditional Medicare and one of many private health insurance plans, we already are beginning to see deceptive ads by Big Insurance to once again lure Medicare beneficiaries into their often deadly money machine.

You’ve seen the ads: happy, smiling seniors playing tennis or pickleball and gabbing about “free” groceries and dental benefits they presumably get because of the generosity of their MA plans. Nowhere – ever – have you seen or heard anything in any of those ads about the potentially lethal side effect of signing up for those plans. But the terrifying truth is that an untold number of MA enrollees have gone to early graves because their insurers delayed or outright denied a test, treatment or medication their doctors said they needed. Or because they couldn’t even find a high-quality doctor, hospital or skilled nursing facility close to their home – or even far away for that matter. Many centers of excellence – hospitals and clinics that are renowned for things like cancer and cardiac care – are not in many MA plans’ “networks.”

Seniors need to be told how limited MA networks can be – and that Traditional Medicare, by contrast, doesn’t even have networks. Traditional Medicare doesn’t restrict you to certain providers. That’s because almost all doctors, labs, clinics and hospitals participate in Traditional Medicare.

And seniors need to be told explicitly in ads what prior-authorization is and how it can affect them. And they need to be told about how much money they’ll have to pay out of their own pockets if they knowingly or unknowingly get care from an out-of-network provider. They also need to be told that their MA plans can and do drop doctors and hospitals from their networks during the course of a given year and that more and more physician practices and hospitals – including world-class facilities like Johns Hopkins and M.D. Anderson and the Cleveland Clinic – have dropped out of many MA networks. And they need to be told that their MA plan could very well dump them next year by “exiting” the community they live in, as Humana, Aetna, UnitedHealth and other plans did this year and plan to do next year.

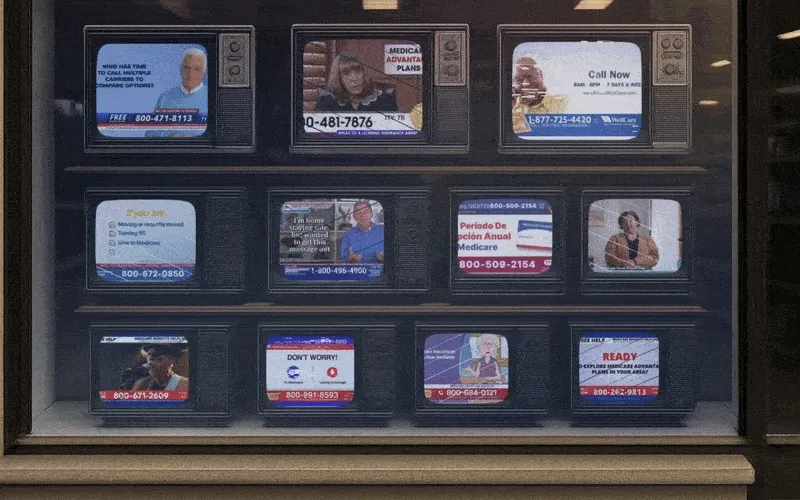

Why, Mr. Trump and Mr. Kennedy, are MA insurers not held to the same standards as pharmaceutical companies? And how fast can you put standards in place to assure us that MA ads don’t omit “critical facts?” You know as well as anyone that between October 15 and December 7 (the open enrollment period) you won’t be able to turn on your TV or scroll through your social media feeds without seeing multiple MA ads that blatantly lie by omission.

Researchers at the nonpartisan KFF found TV ads hawking MA plans ran 650,000 times during the 2022 open enrollment period. You can expect that number will be surpassed this year because Medicare Advantage has become such a cash cow for Big Insurance. As just one example, UnitedHealthcare, a division of the biggest health care conglomerate in the world, got more than 75% of its revenue last year from Medicare and other taxpayer-supported programs. Now you know why those deceptive ads are so ubiquitous, and why private insurers lie with impunity.

Speaking of UnitedHealthcare, it co-brands its MA plans with AARP, which gives that corporation a kind of good seal of approval. AARP has received billions of dollars from UnitedHealthcare over the years as part of the relationship. To its credit, AARP called attention to that KFF study on its website just before the 2023 open enrollment season started. That’s notable, but AARP needs to do much more. So I am hereby calling on AARP to join us in demanding that both the Trump administration and Congress take immediate action to make sure MA ads cannot leave out essential information. Truthful MA ads are just as important as drug company ads. Maybe even more so when you consider all the potential harms MA plans inflict on seniors and people with disabilities every single year.