Millions of ACA enrollees will face steep premium hikes in 2026 as insurer rate increases collide with the expiration of enhanced federal subsidies.

As health insurance premium costs have taken center stage this fall, you may have seen seemingly conflicting reports about how much premiums are increasing, especially for ACA marketplace plans. This isn’t a reporting error. Instead, it reflects a double whammy of increases that more than 20 million ACA enrollees are poised to face in 2026.

To understand what’s happening, it helps to think of ACA premium increases as a one-two punch.

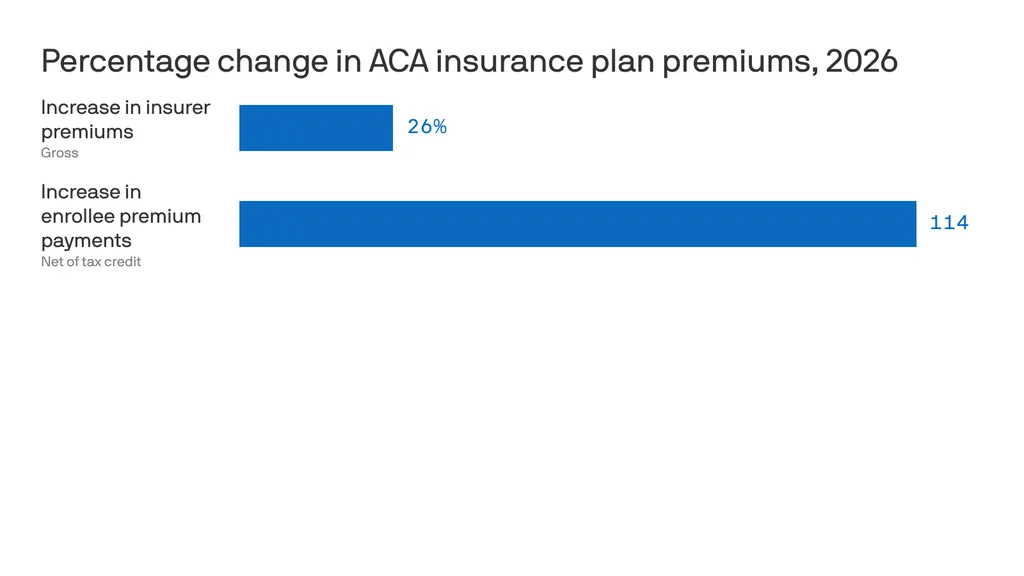

The first hit comes from the overall increase in health insurance premiums for 2026. On average, insurers raised premiums for ACA marketplace plans by roughly 26 percent from 2025 to 2026. This increase reflects a rise in the total cost of coverage, the full premium paid jointly by enrollees and the federal government through subsidies, not just what individuals pay out of pocket.

Premium increases are not new. Insurers raise rates every year. But the 2026 hike is striking: more than three times the 7 percent increase in 2025 and the 6 percent increase in 2024. Insurers have attributed roughly four percentage points of this increase to the anticipated expiration of the enhanced premium tax credits, arguing that enrollment will decline and that sicker, higher-cost enrollees will make up a larger share of the risk pool. Insurers also cite provider consolidation and high pharmaceutical prices as drivers of higher premiums.

These explanations deserve scrutiny. As Wendell Potter recently documented, the seven largest private insurance corporations have collectively taken in more than $10 trillion in revenue since 2014 with revenues steadily increasing each year. Against that backdrop, claims that today’s premium spikes are unavoidable or purely defensive ring hollow.

The second hit falls directly on consumers who currently rely on enhanced premium subsidies (in the form of tax credits) to make coverage affordable. Those enhanced subsidies, first made available during the pandemic, are set to expire at the end of 2025, and Congress appears poised to let them lapse without an extension. If that happens, many enrollees will see the tax credits that lower their monthly premiums shrink dramatically or disappear altogether. Taking this into account, the amount people pay out of pocket for ACA premiums is expected to increase by an estimated 114 percent in 2026. And that is just for the premiums. People enrolled in ACA plans will also have to spend hundreds if not thousands of dollars out of their own pockets in deductibles and copays before their coverage kicks in.

This double whammy will have drastic, and potentially deadly, consequences for millions of Americans. I am already seeing panic from people in my own community and across the country, echoed daily on social media. Yet Congress has taken no action to cushion the blow. The Republicans leading both the House and the Senate are leaving Washington without extending the enhanced tax credits, even as the clock runs out.

This is an abdication of Congress’s responsibility to represent the people it serves, people who have been clear about what they want and need: health insurance they can actually afford. Rather than getting bogged down in partisan gridlock or abstract market ideology, Congress must act now to extend the enhanced premium tax credits. That extension should be treated as an urgent bridge to a real fix to our health care system; one that reduces dependence on Big Insurance, lowers costs for patients, and ensures that no one is forced to go without care.

2025 was one of the most turbulent years in modern U.S. healthcare. The headlines were explosive, the rhetoric dramatic and the controversies nonstop. Yet for all the hoopla and upheaval, the medical care Americans received this month looked almost identical to what they experienced on January 1 — except more expensive.

That yearlong pattern (of intense disruption followed by little improvement) played out across nearly every major healthcare storyline.

Luigi Mangioli is preparing to stand trial almost exactly twelve months after the fatal shooting of UnitedHealth CEO Brian Thompson. The killing sparked fears for major health insurers and raised questions about the fragility of the nation’s largest payer. In a February article, I called it a defining moment for UnitedHealth: an opportunity for the company to start competing on health, not denials. But despite the initial shock and ongoing scrutiny, nothing has shifted in how UnitedHealth pays for (or denies) medical care.

Then, in late fall, the nation endured the longest government closure in U.S. history, driven largely by conflicts over healthcare spending and the Affordable Care Act’s health exchanges. However, the eventual resolution to reopen the government came with no respite for the 24 million Americans currently enrolled in an exchange.

For a broader view of the year, here are five major areas of healthcare that generated chaos, confusion and conflict in 2025 – but little meaningful improvement.

1. Political chaos: Turning science into a battleground

No aspect of healthcare saw more volatility in 2025 than in the political arena. The tone was set in January when President Trump returned to office and began reshaping federal health agencies with unprecedented speed.

Within days, he issued a record flurry of executive orders targeting the Affordable Care Act, Medicaid waivers, Medicare Advantage oversight, prior-authorization rules and federal nutrition standards.

He replaced long-entrenched leaders at HHS, NIH, CDC and FDA with political outsiders, many of whose views on vaccines, chronic disease and scientific evidence diverged sharply from the career experts they superseded. The nomination of RFK Jr. to lead HHS became a flashpoint. His reluctance to confront the measles outbreak in Texas, combined with mixed messaging on vaccine policy, have deepened concern for public health.

2. Economic crisis: Costs soar as coverage grew more fragile

Beneath the political theatrics of 2025 was a sobering reality: Americans will once again pay far more for healthcare next year than the year before. And for many, the financial protections that once softened those increases are disappearing.

Insurers on the Affordable Care Act (ACA) marketplace requested median premium hikes of 18% for 2026, the steepest jump since 2018 and well above this year’s 7% hike. If Congress fails to extend the enhanced ACA subsidies, families who once paid affordable monthly premiums will see their costs double or even triple.

The broader economic picture makes these pressures unavoidable. The United States is now spending $5.6 trillion annually on healthcare. National health expenditures are projected to climb another 7.1% this year, far outpacing economic growth. At the same time, federal debt service continues to soar, consuming more of the national budget than Medicaid itself.

The result is an economic crisis hiding in plain sight, one that will increasingly strain the financial, physical and mental health of Americans in the year to come.

3. Regulatory confusion: Agencies rebooted but didn’t improve health

This year shook the foundations of America’s public-health architecture and left yawning gaps where trust, clarity and expert oversight once stood. Politics has replaced science as the primary driver of healthcare policy.

The Centers for Disease Control and Prevention lost its director just weeks after her confirmation. Within days, top-level scientists and center heads resigned en masse, citing political interference and a collapse of scientific independence. Months later, there still is no permanent CDC head.

At the Food and Drug Administration, career reviewers say they’ve been forced to reconsider or abandon scientific best practices. Across both the CDC and FDA, advisory committees that once evaluated evidence through rigorous, peer-driven processes now rely on anecdote and ideology. One striking example is the FDA’s decision to stop requiring hepatitis B vaccination at birth, a move that public-health experts warn could lead to tens of thousands of additional infections for a disease that had been reduced to fewer than 20 annual cases.

Meanwhile, the administration’s sweeping “health-freedom agenda” (under the banner Make America Healthy Again) has identified food packaging, additives, school-lunch standards and “ultra-processed” diets as public-health priorities. But the proposals to improve nutrition remain largely unformed, as the likelihood of meaningful improvements fade.

What remains at year’s end is a set of agencies still functioning, but with public trust weakened and no clear path to rebuilding it.

4. Technological contradiction: AI leapt ahead while medicine stood still

No field generated more excitement, or exposed more contradictions, in 2025 than generative artificial intelligence.

In the broader economy, GenAI models transformed finance, logistics, law, retail and customer service. New large language models, including GPT-5, DeepSeek and Gemini 3, demonstrated near-expert performance on clinical reasoning, interpretation of complex symptoms and risk prediction. Ambient listening matured into a reliable documentation tool, and with the emergence of Artificial General Intelligence (AGI), Americans are relying on large language models when they have medical questions.

Yet inside traditional medicine, progress remains stalled. Clinicians continue to be encouraged to use AI for administrative shortcuts (coding, charting, prior authorization claims) but national specialty organizations haven’t pushed them to use GenAI for diagnosing disease, reducing medical errors or improving clinical outcomes.

Fear of liability has discouraged technology companies from offering GenAI tools that would allow patients to evaluate symptoms or manage their chronic diseases. Yet usage continues to grow. In polling I conducted this fall, 77% of patients and 63% of healthcare professionals reported using a generative-AI tool in the past three months for health-related information or decision support. Meanwhile, medical schools still teach pre-AI workflows, even as medical students and residents turn to GenAI for clinical knowledge and case analysis. The divide between institutional practice and the behaviors of patients and the next generation of physicians is expanding at an accelerating pace.

5. Cultural conflict: A growing divide between the public & the profession

If 2025 revealed anything about American healthcare, it was a widening cultural rift: between younger patients and medical professionals, and between science and public belief.

This rift is felt particularly among Gen Z and Millennials, generations that grew up online, accustomed to second-screen verification and skeptical of traditional authority. As I wrote in 3 Ways Doctors Can Win Back Gen Z And Millennial Patients, younger Americans expect shared decision-making, transparency and digital-first convenience — expectations medicine failed to fulfill in 2025.

At the same time, disinformation and political rhetoric seeped deeper into public life. Social media spread half-truths faster than public-health leaders could correct them. Vaccine skepticism rose thanks to political disinformation. Basic nutritional science became partisan, too. And the public’s confusion only intensified.

What 2025 reveals about the road ahead

By year’s end, one truth became impossible to ignore: despite unprecedented political turmoil, economic instability, scientific breakthroughs and cultural upheaval, the basic structure of American healthcare remained unchanged.

The incentives driving the system, the chronic diseases afflicting the population and the unaffordability confronting families all persist as we enter 2026. At the same time, as generative AI transforms nearly every other sector of the economy, the fax machine remains the most common method physicians use to exchange vital medical information.

The question now is whether mounting economic, political and cultural pressures will finally force American medicine to transform care delivery next year. For more on that, follow me on Forbes and look for my next article on January 5, featuring my healthcare predictions for 2026.

There’s a good chance your health insurance premiums are going up next year, regardless of where you get coverage.

Why it matters:

The spike in what millions of Affordable Care Act plan enrollees pay will be acute, but workplace insurance is getting more expensive, too — and all at a time when affordability is prominently on Americans’ minds.

ACA premiums have dominated the political discourse in Congress for weeks, but there’s no real sign that any relief is coming from Washington.

Even extending the Biden-era enhanced ACA subsidies — which most Republicans don’t want to do — would do nothing to address what’s driving the surging cost of care or employer insurance affordability issues.

And all signs point to Democrats hammering Republicans for high costs in all forms of health insurance leading up to next year’s midterm elections.

The big picture:

Health insurance gets more expensive almost every year, keeping up with increases in the costs of procedures, tests, drugs and more. But some years see bigger jumps than others, and 2026 is looking like one of those years.

That means tough choices for families, employers and workers all faced with shouldering higher premiums or out-of-pocket spending. Some will conclude it’s prohibitively expensive and go uninsured.

Another thing that’s different about this year is that the white-hot political rancor around ACA premiums is putting health insurance back centerstage politically.

By the numbers:

ACA insurers themselves are raising premiums by an estimated 26%, in part due to rising hospital costs, higher demand for pricey GLP-1 drugs like Ozempic, and the threat of tariffs.

But add in the loss of federal subsidies, and the increase is 114% — or more than double what they currently pay, according to KFF. 22 million out of 24 million marketplace enrollees now receive subsidies.

Premiums in the small group employer market will go up by a median of 11%, also per KFF, due to some of the same reasons insurers cite in ACA markets.

For employer health insurance, there’s no comprehensive data yet for 2026, but estimates from earlier this year put the increases in the high single digits.

For example, according to Mercer, health benefit costs are expected to increase 6.5% per employee in 2026, and many employers are planning to limit premium increases by raising out-of-pocket costs for employees.

One factor driving these increases is advances in medicines, like new cancer treatments, that are more expensive, according to Mercer.

But people are also using health care more, per Mercer. That’s possibly because they missed or delayed care during the pandemic — but also because the use of AI in doctors’ offices gives them more capacity and allows them to work faster.

Between the lines:

Just this month, Gallup polling found that approval of the ACA has hit an all-time high of 57%, including more than 6 in 10 independents but only 15% of Republicans.

Another recent Gallup poll found that 29% of Americans say that cost is the “most urgent health problem” facing the country, up from 23% a year ago.

The bottom line:

Get ready to hear a lot more about health care costs over the next year — while potentially also experiencing your own premium increase.

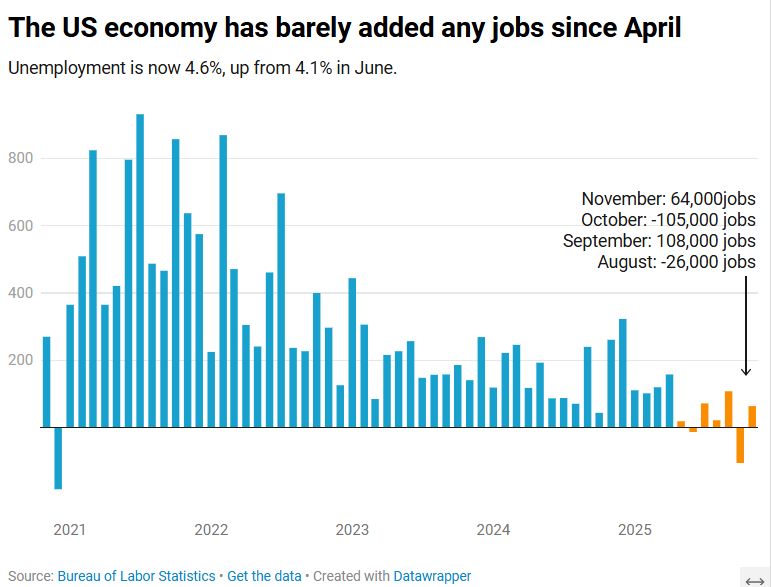

The US economy added 64,000 jobs in November, according to the Bureau of Labor Statistics.

The US economy added 64,000 jobs in November as the unemployment rate crept up to 4.6%, according to Labor Department data published Tuesday.

The unemployment rate is now at its highest level since September 2021.

The November jobs report, originally scheduled to be published Dec. 5 before the 43-day government shutdown delayed multiple economic data releases, comes as Americans stress over rising layoffs and a frozen job market that can feel impossible to break into. Tuesday’s report suggested those conditions persisted toward the end of the year.

Economists surveyed by Bloomberg had expected a gain of 50,000 jobs. The healthcare sector, which has fueled job growth this year, added 46,000 positions for the month.

November’s data additionally showed that the number of people employed part-time for economic reasons rose to 5.5 million in November, an increase of 909,000 over September. Meanwhile, the long-term unemployment rate, or the share of unemployed people who have been without jobs for 27 weeks or more, was 24.3% in November, down from August’s high of 25.7% but higher than the rate of 23.1% seen a year ago.

“The US economy is in a hiring recession,” Heather Long, chief economist at the Navy Federal Credit Union, wrote in a post on X.

“Almost no jobs have been added since April,” Long added. “Wage gains are slowing. 710,000 more people are unemployed now versus November 2024.”

Nancy Vanden Houten, lead US Economist at Oxford Economics, said in a statement that the government shutdown appears to have contributed to the increase in the unemployment rate.

“The number of permanent job losers, which had been ticking higher, declined. Labor force growth also contributed to the increase,” she said.

Partial data for October, also published Tuesday, showed a loss of 105,000 positions. The unemployment rate for the month will not be released. Bank of America economist Shruti Mishra had noted that October’s payroll numbers would be affected by the delayed impact of DOGE-led government job cuts, since many federal employees who opted for the “deferred resignation program” officially left their positions Sept. 30.

The federal government lost 162,000 jobs in October and 6,000 in November, according to the Labor Department.

Next year, seniors and families will have more stringent and more unaffordable health coverage thanks to new AI-driven prior authorizations in Medicare and loss of subsidies in the ACA.

The New Year is just two weeks away, and when Americans wake after clinking champagne and kissing at midnight, the health care landscape in the United States will be in worse shape than it was in 2025. There is a growing list of why that’s true, but here are a couple of developments that will make it harder for many of us to get the care we need:

The December 31 expiration of the Affordable Care Act enhanced subsidies, which will lead to millions of Americans losing coverage and make premiums barely affordable for millions of others; and

CMS’s January 1 implementation of a new pilot project that will put private, for-profit contractors using AI-powered prior authorization in traditional Medicare.

Unless policymakers change course, many Americans will be ringing in 2026 with higher costs, less access and a nasty health care hangover.

WISeR strikes at 12

As we’ve reported, the implementation of the Wasteful and Inappropriate Service Reduction (WISeR) model’s will mark the first time in traditional Medicare’s 60-year history that for-profit companies will decide whether seniors receive certain medical services their doctors recommend. Six companies — many with deep ties to Big Insurance and insurer-backed venture capital — will suddenly have the power to say yes or no to 17 procedures that never required prior authorization before. And for these companies, the more the denials, the bigger the profits.

As Dr. Seth Glickman documented after sitting through CMS’s own WISeR webinar, the rollout has been vague on details and confusing to providers and patients. CMS even admitted during the webinar that the vendors chosen to administer the model were selected in part based on their “success” of using prior authorization in the private Medicare Advantage program, which is notorious for denials, delays and life altering decisions.

Some lawmakers in Washington have taken notice. A coalition of Democrats introduced the Seniors Deserve SMARTER Care Act, warning that WISeR creates “a dangerous incentive to put profits ahead of patients’ health.” Imposing prior authorization in traditional Medicare “will kill seniors,” said Rep. Mark Pocan, one of the bill’s sponsors.

Kiss subsidies goodbye

While WISeR threatens seniors’ access to care, millions of working families are facing a different New Year’s surprise: the expiration of enhanced ACA marketplace subsidies, which Congress has (so far) failed to extend or replace. As Rachel Madley, PhD wrote in October, families will have to gamble when they pick a health insurance plan. She added:

The enhanced premium subsidies being debated in Congress right now are a lifeline for so many of us and must continue in the short term, but they don’t fix the underlying problem: Private insurers extract value rather than control costs or provide access to necessary and affordable care. Decades of experience show that when profits rule health insurance, families face financial ruin no matter which plan they pick during open enrollment.

But as we’ve noted before, this isn’t an existential crisis for Big Insurance. ACA marketplace plans are not where insurers make their real money. Their profits flow increasingly from taxpayer-funded programs like Medicare Advantage and Medicaid managed care — the same universe WISeR is quietly expanding.

One proposal to “solve” the subsidy issue, endorsed by President Donald Trump and HELP Chairman Bill Cassidy, would not extend the tax credits but put $1000 to $1500 into government-sponsored health savings accounts (HSAs). HSAs can be helpful if you you have crappy insurance – or are rich and need an additional place to put your money to avoid taxes – but not a meaningful solution to the millions of Americans facing a 75% hike in premiums or finding themselves priced out of coverage altogether in 2026. The supporters of this approach claim it would somehow take money away from health insurers, but it would just reroute federal dollars to those same companies. For instance, UnitedHealth Group, which owns the nation’s biggest HSA custodian, could grab even more of our tax dollars than they already do. Meanwhile, families would still be exposed to unaffordable premiums and massive out-of-pocket costs. Champagne dreams.

Thanks to these changes in health care: The hangover on January 1, 2026, won’t only be from the previous night’s festivities – and it won’t be cured with some water and Advil. Cheers.

The OIG found that Anthem paid its own corporate sibling as if it were an outside vendor. The maneuver transformed a cost-based function into a source of “unlimited profit.”

When the Office of Inspector General (OIG) audited Anthem Blue Cross and Blue Shield insurance plans for federal employees recently, auditors appeared to be conducting a typical contract compliance review.

While they may not have been looking for a smoking gun, they stumbled upon one.

At first glance, the report on Elevance Health’s Anthem Blue Cross and Blue Shield insurance under the Federal Employees Health Benefits Program (FEHBP) looks like just another technical review, questioning charges and payments across familiar audit categories such as uncollected claim overpayments, administrative expense overcharges, medical drug rebates, provider offsets and lost investment income. The auditors’ stated goal was to “obtain reasonable assurance” that Anthem was complying with contract terms. The review took a turn from the routine when the OIG looked at how Elevance is using a common insurance practice known as subrogation.

The issue of subrogation emerged after the OIG observed irregularities in recoveries and fees being passed through the plan. Subrogation – recovering costs from insurers, auto carriers or liable third parties – is a familiar function. But the structure Anthem created is not.

Anthem Inc. became Elevance Health Inc. in 2022 and also launched Carelon health services. Elevance became the name of the parent company, but the name Anthem was retained for the health plans the company operates across the country. Carelon, a wholly owned Elevance subsidiary, is a corporate sibling of the Anthem health plan division, and it’s the fastest-growing of the two. In fact, Elevance views Carelon as the company’s profit engine.

The OIG discovered that Anthem treated Carelon as a commercial provider of services in an arm’s length transaction and paid Carelon a percentage of recoveries, even though, as OIG wrote, this was a “related party transaction.” Auditors discovered that Anthem had contracted its subrogation work to Carelon, and then billed the FEHBP a percentage-based “fee,” deducted directly from the recoveries, and recorded it as a health benefit expense rather than an administrative cost. The subrogation fees then passed through FEHBP as medical claims, thereby avoiding oversight limits on administrative costs and creating “unlimited” profit on a function that should have been cost-based.

Self-enrichment

The OIG was especially troubled because the transaction was a “related party transaction,” which in government contracting is the polite way of saying you’re paying yourself. Worse, the OIG found that:

“The method Anthem uses to charge these subrogation recovery fees results in unlimited profits for essentially an ‘in-house’ service…

And that:

“Elevance Health, Anthem, and/or Carelon should not benefit or self-enrich at the expense of the FEHBP.”

The auditors also concluded that:

“… the only profit that can be charged to the FEHBP is the negotiated annual service charge…”

But Anthem had charged $39,235,156 in subrogation fees plus $5,638,360 in lost investment income – exactly the kind of profit the contract prohibits.

What’s most shocking about this audit isn’t what Anthem did – it’s how openly they did it, and how little anyone plans to do about it.

To appreciate the magnitude of the audit discovery, it helps to understand how the Federal Employees Health Benefits Program actually operates – and who really runs it. The FEHBP is a roughly $70billion annual program covering more than eight million federal workers, retirees and dependents. Yet the federal government does not administer these benefits directly. Instead, it contracts with the Blue Cross Blue Shield Association (BCBSA), which then delegates day-to-day administration to individual Blue plans across the country.

Among those plans, Anthem administers services in 14 states – more than any other Blue plan – and during the audit period was responsible for $40.6 billion in FEHBP benefit payments and $2.1 billion in administrative expenses. Anthem isn’t simply one contractor in a crowded field; it is the dominant operational arm of the BCBSA for a vast portion of the federal population. When Anthem selects a vendor, sets payment terms or withholds documentation, it is not a peripheral actor – it is effectively shaping how the federal health plan functions.

What’s worse than getting caught red-handed breaching the contract? The company’s response. Its posture throughout the report is equal parts dismissive, pedantic and openly defiant. It insisted the fees represented “allowable, commercially reasonable charges,” argued that subrogation was a “commercial service,” and maintained that the costs were “not subject to cost analysis.”

The company repeatedly pushed back with formulations that would seem to suggest that Elevance itself, and not the OIG, was the final authoritative voice on contract compliance and legality:

“We disagree with the OIG’s characterization.”

“We do not concur.”

“The services are allowable and reasonable in view of the commercial marketplace.”

When the OIG pressed for documentation to substantiate these so-called “commercially reasonable” fees, they were met with outright refusal. They were told that no such documentation existed. Unfortunately for Anthem, they proved themselves wrong in a meeting with OIG when they inadvertently displayed a detailed spreadsheet showing a cost analysis for corporate subrogation services – the very spreadsheet the company had insisted did not exist. As the OIG noted:

“Anthem inadvertently shared an Excel spreadsheet which included the total corporate Carelon subrogation costs by year – precisely the cost data we have been requesting.”

Rather than simply hand it over, the company declared the spreadsheet “not accurate,” “not relevant,” and “not responsive.”

It gets worse. When the auditors asked for a valuation prepared by the company’s accounting firm, Deloitte – the same valuation Anthem itself relied upon as proof that they had studied the reasonableness of their charges – the company responded by producing six heavily-redacted pages out of a 900-page report. That’sless than 1% of the analysis they claimed fully justified their pricing, which costs the FEHBP over $40 million.

The OIG, in its dry bureaucratic tone, noted that the company’s justification for withholding “over 99 percent of the Deloitte study” was “insufficient” – which is government-speak for, “Are you kidding me?” The OIG all but throws up its hands:

“We cannot determine the actual profit charges and/or the reasonableness of these fees due to the scope limitation created by Anthem’s refusal to provide documentation access.”

Anthem behaves as though the worst that can happen is that someone at OIG writes a sternly worded paragraph in a report that will sit unread on a government website. Unfortunately, they are probably right.

As the OIG delicately put it:

“Throughout the audit process, we encountered numerous instances where Anthem responded untimely and/or initially provided incomplete responses.”

And why would Anthem cooperate? The OIG report is unlikely to trigger meaningful enforcement, the federal Office of Personnel Management has historically acted more like a deferential plan sponsor than a regulator, and Congress appears largely uninterested in disrupting a status quo that serves the BCBSA and its licensees quite well.

62% profit margin

Ultimately, due to the lack of information from Anthem, OIG acknowledged that it was forced to estimate the degree of unallowable profit. Based on the limited corporate subrogation cost data they could see, auditors concluded that Anthem was likely earning a profit margin of approximately 62%.

Think about that: a federal contractor potentially earning a 62% profit margin on a supposedly in-house function, inside a federal health plan that legally prohibits this form of profit.

Discovery of a profit extraction model

All of this is visible only because the OIG happened to expand a limited audit sample into subrogation recoveries. The OIG did not enter the process intending to uncover a profit-extraction model. But it found one.

Which raises the question: what would the numbers look like if OIG examined all subrogation? Or payments for all Carelon services? Or fees related to recovery services, out-of-network negotiation and payment integrity? Or medical management? Or pharmacy recoveries?

The answers are not in the report.

What this audit shows is not just that Anthem crossed a line. It shows that those running the FEHBP lack the power, or the will, to draw one. If a contractor can profit in violation of the contract, get caught, and then simply withhold the evidence and declare they disagree, then the rules are performative and enforcement is imaginary. Anthem’s response – dismissing the OIG’s findings, withholding a 900-page Deloitte report, refusing cost documentation, and asserting a legal right to decide what data the government may review – reflects not caution, but confidence.

Confidence that there will be no consequence. Confidence that the FEHBP cannot or will not act. And, perhaps most troubling, confidence that the American taxpayer will never know the difference.

The contractor knowingly violated profit limits, hid the margin inside claims, refused to provide cost data, and continues billing unchanged. If this is what turns up accidentally, just imagine what would be exposed if anyone actually went looking.

Chris Deacon, JD, is a health care executive and consultant recognized for her advocacy for transparency and accountability. She previously ran New Jersey’s public sector health plan, covering 820k lives.

There’s likely to be one more round of health care votes in the House next week after the Senate votes down two rival Affordable Care Act subsidy proposals Thursday — but they won’t get any closer to extending the enhanced subsidies.

Why it matters:

Those subsidies now appear certain to expire at the end of the year, short of a last-minute breakthrough — and out-of-pocket premium costs will more than double on average for roughly 20 million ACA enrollees.

Driving the news:

The Democratic proposal that will get a Senate vote Thursday would extend the enhanced subsidies for three years, while the Senate GOP proposal would not extend the subsidies but instead provide money for health savings accounts.

Both will fail to get the needed 60 votes.

Senate Majority Leader John Thune (R-S.D.) has left the door open for further bipartisan talks after both votes fail, but there is deep skepticism in both parties that any such deal is possible.

Sen. Tim Kaine (D-Va.) said it’s possible there is “additional discussion” after the failed votes, but said the issue also might end up in a “political solution in November when people pick the side that’s for them.”

The latest:

House GOP leaders outlined a range of possible health care options on Wednesday morning, but they have little to do with the subsidies, which weren’t included in their plans.

GOP leaders will bring “consensus” bills to the floor next weekthat aim to lower health care costs, a source who attended House Republicans’ Wednesday morning conference meeting told Axios.

Those could include expanding health savings accounts and association health plans, which allow employers to band together to purchase coverage.

Overhauling pharmacy benefit managers with the goal of lowering drug costs was also discussed, along with funding ACA payments known as cost-sharing reductions (CSRs).

The intrigue:

On the House side, a bipartisan group of moderates including Reps. Brian Fitzpatrick (R-Pa.) and Jared Golden (D-Maine) filed a discharge petition, a procedural move to force a vote on a compromise extension plan.

But that effort to go around House GOP leadership faces long odds against getting the required majority of the chamber to sign on.

Modifications to the subsidies in that plan designed to win over GOP votes, like a crackdown on zero premium plans that backers say fuel fraud, could lose Democratic support due to concerns about coverage loss.

Democratic leaders havebeen focused on a clean three-year extension, saying that is the clearest way to address the issue with little time remaining to implement changes before the new coverage year starts Jan. 1.

House Democratic Leader Hakeem Jeffries (N.Y.) told reporters Wednesday he has no position on the discharge petition.

The bottom line:

There is also deep resistance to a subsidy extension among many Republicans.

Thune has said he thinks Democratic leadership is more interested in a “political messaging” vote this week than in entertaining reforms to the subsidies that Republicans point to.

Even if members in either chamber are able to make progress on a consensus compromise subsidy plan, which in theory could be attached to a government funding bill needed before Jan. 30, the divisive issue of abortion hangs over all of the discussions.

Many Republicans insist on new limits preventing the subsidies from going to insurance plans that cover abortion. Democrats say that is a dangerous expansion of safeguards that already require taxpayer funds to be segregated and not pay for abortion coverage.

Yesterday aboard Air Force One, President Trump was asked by a reporter if he supported Senators Bill Cassidy (R-LA) and Mike Crapo’s (R-IN) new health care proposal, which would authorize $1,500 deposits in Health Saving Accounts (HSAs) for lower-income individuals to replace the expiring Affordable Care Act (ACA) subsidies. The president’s response to the question was telling. And it shows just how much Big Insurance has fallen from grace in recent months.

For decades, merely expressing disenchantment with private health insurers could get you labeled as a socialist. Now we are seeing daily criticism of health insurance companies from people across the political spectrum, leading one to not know if a quote like “Americans are getting crushed by health insurance with monthly payments” is coming from a progressive, like AOC, or a conservative like MTG. (Hint: that quote was from MTG). Trump’s response was in the same vein and could lead one to believe there is a chance of the left and right finding common ground in holding insurance companies accountable for their greed.

Where Trump is right. Where Trump is wrong.

Below we will dissect the president’s response and explain where he’s right and wrong.

“I like the concept [of the Cassidy-Crapo legislation]. I don’t want to give the insurance companies any money. They’ve been ripping off the public for years.“

This is true. Big Insurance has been ripping us off for years. And almost all of insurers’ growth in recent years has come from us as taxpayers. Most big insurers now make far more money on the lucrative Medicare Advantage business and managing state Medicaid programs than from their commercial health insurance plans. And they’ve even figured out how to bilk the VA.UnitedHealthcare, the biggest insurer, now gets more than 75% of its revenues from taxpayer-funded programs. And yes, insurers are getting hundreds of billions of dollars every year from the ACA subsidies that are at the center of debate in Washington.

Here are a couple of examples. Private health insurers took in over $500 billion in tax dollars to administer Medicaid in 2023. And this year alone, they will be overpaid – yes overpaid – $85 billion as a consequence of how they’ve rigged the Medicare Advantage program.

Insurers also take in massive amounts of money in the form of premiums that people pay thinking that money goes to care. Much of that money ends up going toward things (and people) that do nothing to get us well or keep us well. Since 2014, the seven largest insurers have made over $500 billion in profits, and they used $146 billion to buy back their own stock. So yes, Trump is correct, health insurance companies have been ripping people off for years.

“Obamacare is a scam to make the insurance companies rich.”

No, Mr. President, the ACA is not a scam and most Americans now know that it has done a lot of good for a lot of people. Among other things, it made it possible for millions of people who previously had been blackballed by insurers because of a preexisting condition to finally get coverage. It brought us many long-overdue consumer protections, outlawed junk insurance, enabled young people to stay on their parents policies until they turned 26, alleviated job-lock through the creation of the ACA (Obamacare) marketplaces, and it made millions more low-income families eligible for Medicaid.

But, the president is right to say that Big Insurance has gotten rich since the passage of the ACA. Between 2014 (the year the entirety of the ACA was implemented) and 2024, just seven for-profit health insurers amassed $543.4 billion in profits and took in a staggering $10.192 trillion in revenues.

“And they have made, I mean, you look, $1,400 to $1,700 increase, 100 percent increase over the last number of years. There’s really few things that have gone up like insurance companies.”

The president is kind of right. As KFF reports, the cost of a family policy has increased 60% since 2014 – a rate of increase much higher than general inflation and also higher than medical inflation. And as we’ve published previously, not only has the total cost of an employer-sponsored plan skyrocketed, so has the share of premiums workers must pay. This year, employers deducted an average of $6,850 from their workers’ paychecks for family coverage, up from $4,823 in 2014. And keep in mind, all that money our employers are having to send to insurance companies is not money that’s available to give raises to workers or hire more people.

“They’re getting numbers and money like nobody’s ever seen before. Billions and billions of dollars is paid directly to insurance companies. We’re not going to do that anymore.”

The president is right. Several Big Insurance companies have ballooned in size over the past decade to become some of the world’s biggest corporate conglomerates. UnitedHealth Group, CVS/Aetna and Cigna are now numbers 3, 5 and 13 on the Fortune 500 list. The only American companies that take in more revenue than UnitedHealth are Walmart and Amazon.

“I believe Obamacare was set up to take care of insurance companies, not to take care of the American public.”

The president has his history wrong here. While there are plenty of Monday-morning-quarterbacking you can do for the ACA – the law was not passed to “take care of insurance companies.” While the ACA didn’t fix everything – not by a long shot – it did stop some of the insurance industry’s worst abuses, like refusing to sell policies to people with preexisting conditions – even acne – and “rescinding” policies to avoid paying for life-saving care. Some insurers were found to be paying employees bonuses to find policies to rescind, including the policies of women almost immediately after being diagnosed with breast cancer.

It prohibited health insurers from charging people more because of a preexisting condition and from dumping the sick so they could reward their shareholders more generously. Keep in mind that insurers consider every claim they pay as a loss, hence the term “medical loss ratio” (MLR), which the ACA addressed by requiring insurers to spend at least 80%-85% of our premiums on our health care.

And it’s not like Big Insurance wanted the ACA to pass. Back in 2010, America’s Health Insurance Plans (AHIP), the PR and lobbying group for health insurers, quietly funneled $100 million to the U.S. Chamber of Commerce to orchestrate a PR, advertising and lobbying blitz to keep the ACA from being passed.

While big health insurance companies have only grown since the passage of the ACA, it has been Big Insurance’s corporate maneuvers and work on Capitol Hill (not the law itself) that has allowed these companies to flout some of the ACA’s regulations and bend the law to do their will.

“I love the idea of money going directly to the people, not to the insurance companies. Going directly to the people. It could be in the health savings account. It could be a number of different ways.”

While that is a compelling sound bite, it’s disingenuous. The money proposed by Cassidy and Crapo to go to HSAs would then be used by enrollees to buy insurance, thus still giving money to the insurance companies. Even worse, the proposed amount of money to go to people’s HSAs to help them pay for health insurance and care is $1,000-$1,500. This is money that would be used to purchase a bronze or copper plan with a high deductible (with many of those plans having deductibles north of $5,000). That means under this plan people would still need to come up with thousands to meet their deductible on top of paying their premiums every month. $1,000 wouldn’t come close to even covering the premiums for a decent policy, much less the out-of-pocket costs.

Replacing ACA subsidies with HSAs would still keep Americans tied to the same private health insurers that Trump calls “big, bad” and “money-sucking.”Most families would still be exposed to crippling medical bills, and even more tax dollars would flow to insurance conglomerates that own HSA custodian businesses (like UnitedHealth’s Optum Bank).

“And the people go out and buy their own insurance, which can be really much better health insurance, health care.”

That’s wishful thinking far removed from reality. The health insurance plans available to people who get money for their HSAs under the Cassidy-Crapo proposal – rather than getting subsidies – are the same as those currently available. Worse, without the subsidies, people will not be able to afford the gold or silver plans that have lower out-of-pocket costs. In reality the plans that people buy under the proposed Cassidy-Crapo plan would have less value than the plans they previously bought with subsidies.

Trump’s comments are coming ahead of tomorrow’s scheduled vote in the Senate on dueling Democratic and Republican proposals to deal with the enhanced subsidies for ACA plans that will expire in three weeks. Without those subsidies, premiums will spike for many of the 24 million American enrolled in “Obamacare” plans. Democrats want to extend the subsidies for three years. Republicans, led by Senate Majority Leader John Thune, will push a plan replacing those subsidies with direct payments into individuals’ Health Savings Accounts (HSAs), as the president is suggesting. Neither plan is expected to get the 60 votes required for passage. What happens next is anybody’s guess.

The Senate will vote tomorrow on dueling health care plans: Democrats’ proposal to extend enhanced Affordable Care Act subsidies for three years, and a plan from two Republican chairmen that would instead give enrollees funds in health savings accounts.

Why it matters:

The move gives the GOP an alternative to point to if the ACA subsidies expire at the end of the year and health care costs spike for millions of people.

But neither plan is expected to get the 60 votes to advance.

Driving the news:

The plan from Finance Committee chair Mike Crapo (R-Idaho) and health committee Chair Bill Cassidy (R-La.) wouldn’t extend the tax credits past their year-end expiration, instead providing $1,000 to $1,500 in health savings accounts to help certain marketplace enrollees with out-of-pocket costs.

It’s drawn sharp criticism from some Democrats for leaving working-class Americans saddled with high health costs.

Senate Majority Leader John Thune (S.D.) left open the possibility of talks after both votes fail on Thursday, though there is deep skepticism about the chances of reaching a bipartisan agreement.

“If neither proposal gets 60 then we’ll see where it goes from there,” Thune said.

President Trump, asked later about the Crapo-Cassidy bill and whether Republicans should vote for it, told reporters, “I like the concept. … I love the idea of money going directly to the people.”

Between the lines:

On the House side, GOP leadership, committee chairs and leaders of House GOP factions met yesterday to discuss health proposals, with an eye toward a possible House vote this year.

Members left the meeting tight-lipped, saying discussions are ongoing.

The full House Republican conference is expected to discuss health proposals in its meeting this morning ahead of potential votes next week.

Over 17 million nonelderly Californians (55%) received health benefits through an employer in 2023. The California Health Benefits Survey (CHBS) tracks trends in these workers’ coverage, including premiums, employee premium contributions, cost sharing, offer rates, and employer benefit strategies. In 2025, the survey also included questions about provider networks, coverage for GLP-1 agonists, premium cost drivers, and employee concerns about utilization management. The CHBS is jointly sponsored by the California Health Care Foundation and KFF.

KEY FINDINGS INCLUDE:

Premiums for covered workers in California are higher than premiums nationally. The average annual single coverage premium in California is $10,033, higher than the national average of $9,325. The average annual family premium in California is $28,397, higher than the national average of $26,993.

Overall, the average family premium has increased annually by 7% in California and 6% nationally. The average single premium has increased 8% annually in California and 6% nationally. Since 2022, the average premium for family coverage has risen 24% in California, higher than national measures of inflation (12.2%) and wage growth (14.4%).

Workers are typically required to contribute directly to the cost of coverage, usually through a payroll deduction. On average, covered workers in California directly contribute 14% of the premium for single coverage and 27% for family coverage in 2025. These shares vary considerably, and some workers face much higher premium contributions, especially for family coverage.

A lower share of covered workers in California face a general annual deductible for single coverage than covered workers nationally (75% vs. 88%), and the average deductible is lower ($1,620 vs. $1,886). The share of California covered workers with a deductible has increased since 2022 (68% to 75%).

Employers in California are significantly less likely than employers across the nation to say there were sufficient mental health providers in their plans’ networks to provide timely access to services.

Many employers report concerns about out-of-pocket costs: 47% of firms offering health benefits indicate that their employees have a “high” or “moderate” level of concern about the affordability of cost sharing in their plans. About one in 10 covered workers in California faces a general annual deductible of $3,000 or more for single coverage.

Large California employers view drug prices as a major driver of rising premiums. Thirty-six percent of large firms report that prescription drug prices contributed “a great deal” to premium increases.

Over one-quarter of large firms (28%) offering health benefits in California say they cover GLP-1 agonists when prescribed primarily for weight loss. Nearly one-third of these firms report higher-than-expected utilization of this benefit.

Read the full report on the KFF website or download it below.