Sweeping changes to Medicaid and the Affordable Care Act are combining with rising health costs to make 2026 a high-stakes year for hospital operators.

Why it matters:

While major health systems like HCA are likely to weather the worst, some safety net providers and facilities on tight margins could close or scale back services as uncompensated care costs mount and uncertainty around future policies swirls.

“We took a big hit in 2025,” said Beth Feldpush, senior vice president of policy and advocacy at America’s Essential Hospitals.

“I don’t think that the field can absorb any further hits without us really seeing a crisis.”

State of play:

Last year’s GOP tax-and-spending law will decrease federal Medicaid funding by nearly $1 trillion over the next decade, translating into millions more uninsured, lower reimbursements and higher costs for hospitals.

The Trump administration is also considering big changes to the way Medicare pays for outpatient services that could reduce hospital spending by nearly $11 billion over the next decade, including paying less for chemotherapy.

Hospitals have the rest of this year to boost their balance sheets, invest in technology including AI, and even consider merger plans before the biggest changes take effect in 2027, Fitch Ratings wrote in its annual outlook for the nonprofit hospital sector. The financial outlook remains stable for the sector overall next year, the report predicts.

“People are already very proactively looking at those out years and saying, if that’s the worst-case scenario that I’ve got to deal with, what can I do today to make that impact less,” said Kevin Holloran, a senior director at Fitch.

Threat level:

Hospitals in some instances have started closing unprofitable services like maternity care and behavioral health care in the face of financial pressures.

More than 300 rural hospitals are at immediate risk of closing their operations entirely, according to a December report.

Safety net providers also are going to court to fight an administration effort to make them pay full price for medicines they currently get at a steep discount and reimburse them later if they’re found to qualify under the government’s 340B discount drug program.

“Those hospitals that have been underperforming … they are going to continue to struggle,” said Erik Swanson, managing director at consulting firm Kaufman Hall. “Those who are doing really, really well may continue to see growth in their performance.”

Private equity firms will likely continue buying up and building new businesses in outpatient service areas like ambulatory surgery, labs and imaging, he said.

“Hospitals and health systems should continue to expect quite a bit of challenge and disruption in those spaces.”

Congress still could extend the industry some lifelines, though any effort to delay or roll back some of the biggest Medicaid cuts face tough odds this year.

Sen. Josh Hawley (R-Mo.) introduced a bill to repeal parts of the GOP budget law that would slash hospitals’ Medicaid dollars.

Lawmakers are debating whether to renew enhanced ACA subsidies that expired at the end of 2025 and could result in millions more uninsured patients, but that effort would also have to overcome significant GOP opposition.

“Our job is to make sure that we create a predicate that, as these provisions come online, they may very well need to be revisited,” said Stacey Hughes, the American Hospital Association’s executive vice president for government relations and public policy.

What’s ahead:

Beyond policy changes, hospitals also are dealing with inflationary pressures, including rising medical supply costs, and administrative overhead from insurer pre-treatment reviews.

Those trying to pad their margins may ramp up their use of artificial intelligence to code patient visits in a way that increases reimbursements from public and private payers, Raymond James managing director Chris Meekins wrote in an analyst note.

While hospitals have historically been able to navigate big policy challenges, if things don’t go their way, it could turn into a “tornado of trouble,” Meekins wrote.

Over the last few years, I have written for the Rockefeller Institute about trends in healthcare. In 2023, I chose ten trends, including staffing challenges, the increasing role of non-traditional players in health, such as Walmart and CVS, as well as the increasing role of private equity in healthcare, the movement toward value-based care, and the growing use of digital health—all trends that I expect to continue. In 2024, I highlighted a mega trend specific to the provider community, in which a number of factors had combined to lead to the segmentation of the industry into three different categories of entities. Those included what I categorized broadly as “today” entities (i.e., those that we know as traditional providers, many of whom are fighting for their sustainability), “tomorrow” entities (i.e., non-traditional entities that are not necessarily healthcare entities but are in the healthcare space and are typically part of a larger conglomerate or backed with private equity), and “striving survivors” (i.e., today entities that are adapting radically or partnering with tomorrow entities to exist in the future).

The following January, I picked five issues to watch in healthcare in 2025. They were (1) the continued expansion of computational data technologies, especially artificial intelligence (AI); (2) insurance coverage shifts; (3) consolidation in the overall industry; (4) payment, costs, and coverage for pharmaceuticals; and (5) exponential advancements in life sciences.

This blog reviews the status of those 2025 trends and suggests one additional issue that may garner more attention in 2026: the overall cost, pricing, and affordability of healthcare. I discuss the factors pushing this issue into the spotlight and potential options for policymakers to counteract this trend.

A Status Review of the Five 2025 Trends

Before delving into the newly highlighted trend of the cost, price, and affordability of healthcare, it is worth briefly reviewing the status of the five trends that were identified in 2025, since all of them will continue to be important in 2026.

The continued expansion of computational data technologies, especially AIIssue Updates. There has been no slowdown in the use of computational data technologies and AI in healthcare since I wrote about it in 2023, and as part of the trends last year. In April 2025, the healthcare AI company Innovacer did a survey of AI use in the sector. The company’s report noted that adoption of AI is expected to continue its growth as more tools become available for a variety of purposes, including quicker and more effective disease diagnosis, administrative process improvement, and electronic health record management. JP Morgan likewise reported in December 2025 that AI-focused deals now make up 75% of health tech funding. Some of the more interesting areas of advancement are in genomics, remote patient monitoring, medical imaging, and improved documentation. And the use of ambient products that help capture health data from conversation saw some of the biggest growth yet in 2025. On the consumer side, more and more patients (an estimated 40 million people) are using chatbots to help them with making decisions about their own care, while the integration of AI with robotics is increasingly being used to assist physicians with surgery. And very recently, in January 2026, OpenAI released a chatbot specifically for health care.Policy Responses and Options. In terms of policy, there have been different federal actions designed to accelerate AI adoption and use, including a handful of executive orders in 2025. In healthcare specifically, the Department of Health and Human Services issued its AI strategy on December 5, 2025. And there have been federal investments announced that support the use of AI to advance research and cancer treatment. In addition, on December 19, 2025, the Trump administration asked for public input on how technology adoption in healthcare—especially AI—could be accelerated. At the state level over the last year, 47 states issued more than 250 bills to regulate AI in healthcare (with at least 30 bills signed into law). The bills ranged from ones protecting minors from mental health AI-enabled chatbots to bills barring AI from making therapeutic decisions or interacting with patients without licensed oversight. And states like New York are incentivizing more use of AI in healthcare through the use of partners that improve care and strengthen operations, as well as evaluating best-in-class AI tools.

Insurance coverage shifts Issue Updates. In January 2025, I noted the possibility that insurance coverage was likely to shift, in part, because of the possible expiration of the Enhanced Premium Tax Credits (EPTCs) at the end of 2025. The EPTCs were enhanced in 2021 under the American Rescue Plan Act and are sometimes referred to as the “Obamacare subsidies.” They were intended to reduce the cost that people pay when they obtain coverage from qualified health plans on the health exchanges. Although some proposals were made by both Democrats and Republicans at the end of 2025 to help mitigate the impact of the loss of the EPTCs, none of the proposals were able to gain enough bipartisan support to be signed into legislation in 2025, resulting in a spike in costs for premiums starting January 1, 2026. As this blog was being written, Congress was debating the possible partial extension of these credits in some form, although passage was not certain. Either way, it is likely that healthcare coverage will continue to be a topic of much debate in Congress in 2026.In addition, in 2025, changes made to Medicaid coverage in the One Big Beautiful Bill Act (otherwise known as HR1) are also likely to impact insurance costs and coverage in 2026. The changes to health insurance coverage in HR1 were outlined in a paper by the Institute in mid-2025 and will have varying impacts on both funding and coverage over the coming months and years. As I later wrote about with colleagues, additional federal rule changes in 2025 will also impact public insurance coverage in the future. The Urban Institute estimates that close to five million people may lose coverage in 2026, although the exact number who lose coverage versus those who choose cheaper and less expansive coverage options with fewer benefits has yet to be fully analyzed.Policy Responses and Options. With the expiration of the EPTCs and changes in federal reimbursement for coverage of immigrant populations, state policymakers will need to make decisions in 2026 about who and what may be covered with state-only dollars. States appear to be taking different approaches. By mid-2025, the Kaiser Family Foundation reported that of the 14 states that offer health coverage to at least some immigrants, at least three had proposed limits on coverage (some ending it altogether and others restricting it). For example, on January 1, 2026, Medi-Cal, which is California’s Medicaid program, will freeze any new enrollments for certain undocumented adults who receive state-funded full-scope services. In June 2025, the Minnesota legislature voted to limit eligibility for persons over age 18 who are undocumented. New York has applied to federal regulators seeking to change the authorization for its successful Essential Plan—that provides coverage to some 1.7 million New Yorkers, including certain legally present immigrants—from a revocable federal waiver to the Affordable Care Act (ACA) specified Basic Health Program. Expect to see many other states taking actions to either drop or preserve health insurance coverage in 2026. What impact these changes have on the extent of coverage and the number of newly uninsured people this year remains to be seen.

Consolidation in the overall industry Issue Updates. Consolidations in healthcare, both vertical and horizontal, continue. In January 2025, we highlighted mergers, such as the one that created Risant Health. We also examined the continued integration of various companies with United Health Group under Optum Rx (a pharmacy business), Optum Insight (a health analytics company), and Optum Health (care management), as well as the integration of United Health Group and Change Healthcare in early 2024. The consolidation of the insurance industry continued in 2025, with the top 7 companies garnering 75% of the market. The Government Accountability Office also reported on the continued acquisition of physician groups by insurers, hospitals, and private equity firms. Overall, mergers and acquisitions (M&A) transactions among healthcare entities increased steadily from 2021-2024, and, in 2025, healthcare M&A was experiencing its most active M&A cycle in over a decade. Full-year trends were not yet fully assessed by the time of printing this blog, but Pitchbook, which tracks M&A deals across industries, expected that healthcare services M&A levels in 2025 would slightly exceed 2024 levels. This also includes the divestiture of assets from national chains like Ascension and CommonSpirit Health.Policy Responses and Options. At the federal level, shortly after last year’s blog on this trend was published, the federal HHS released a report on how consolidation in the industry continues. For the most part, the Trump administration has kept in place stricter guidelines for reviewing corporate mergers in healthcare, but that hasn’t stopped consolidation from happening. At the state level, we previously highlighted that state policymakers had proposed over 34 bills in 22 states designed to address such consolidations. As this blog was being written, the governor of New York indicated in her State of the State speech that the state planned to expand its monitoring of transactions by healthcare entities that increase revenues by over $25 million. Yet, market forces seem to be allowing such consolidations to continue, and financial and operational strains allow the continuation of mergers and acquisitions that are forcing some systems to divest in hospitals, while regional systems acquire those smaller assets that enable them to expand. Unless states can play a role in propping up financially challenged providers, prevent large insurers from becoming larger, or better regulate nontraditional actors in healthcare, consolidation appears likely to continue in the coming year.

Payment, costs, and coverage for pharmaceuticals Issue Updates. By late 2025, it was reported that pharmaceutical companies were expected to raise prices on at least 350 drugs in 2026. That is higher than at the same time last year. Generally, many of the regulatory actions to control prices come from the federal level. Although states may feel somewhat constrained by the Commerce Clause on their ability to regulate pharmaceuticals across state lines, there are still ways for them to address cost issues, such as through rebate programs, limits on Pharmacy Benefit Managers (PBMs), or price negotiations for drugs purchased under the Medicaid program or for state employee benefit programs.Policy Responses and Options. At the federal level, the Trump administration issued an executive order in the spring of 2025 with suggested actions to lower drug prices. The administration also announced agreements to lower the cost of two of the most used drugs in the country, Ozempic and Wegovy. Then, at the end of 2025, the Centers for Medicare and Medicaid Innovation (CMMI) released a proposed model for controlling prescription costs called the Global Benchmark for Efficient Drug Pricing (GLOBE) Model, which is a mandatory model that would assess a rebate for certain drugs under Medicare Part B if the prices exceed those paid in economically comparable countries. It also released the Guarding US Medicare Against Drug Costs (GUARD) Model, which calculates international reference pricing benchmarks and requires manufacturers to pay a rebate if the Medicare net price is greater than the Model benchmark. Congress introduced bipartisan legislation in mid-2025 to lower drug prices by barring drug companies in the US from charging higher prices. State governments were also very active in 2025, passing legislation to lower drug prices, with 31 states passing nearly 70 bills by the end of the third quarter with the goal of lowering prices. I expect to see additional legislation in more states in 2026, including state efforts that mirror some of the federal actions that took place in 2025. As mentioned, such efforts might include building on existing state efforts, such as drug review boards, expanded rebates under Medicaid, and/or reducing administrative costs through third parties, like PBMs.

Exponential advancements in life sciences Issue Updates. Although AI has transformed medicine in different ways, in the case of life sciences, AI accelerated advancements especially for genomics, precision medicine, and medical imaging. In particular, as noted by MedEdge, life science based medicine like gene editing and CRISPR were better able to move out of the trial phase and into the treatment phase. AI is also augmenting drug discovery by making it easier to observe the interaction of drugs and understand how they fight disease. Molecular editing, lab-grown 3D bioprinting, mRNA vaccine use for cancer, and robotic surgery are all areas that MedEdge saw continued expansion in 2025. Private funding continued to pour into biotechnology in 2025, as tracked by Fierce Healthcare. The Fierce Healthcare tracker shows that many companies, such as Hemab Therapeutics, Electra Therapeutics, or Tubulis (an antibody drug conjugate), raised well over $100 million in venture capital and related funding in 2025.Policy Responses and Options. In contrast to the growing investments of private funding in life sciences, funding from the federal government specifically for life science research—especially from the NIH—was targeted for cuts in 2025 with disproportionate impacts across states depending on where that research was occurring. According to tracking done by The Sciences & Community Impacts Mapping Project, proposed federal funding cuts showed a potential economic loss of an estimated $16 billion. At the state level, policymakers in the Midwest, California, North Carolina, and a few other states are competing to advance major life sciences projects. The investments include supporting the workforce, developing shovel-ready sites or ones adjacent to major universities, and/or providing expedited permitting. Given the growing advancements and potential of life sciences, in the coming year, I expect to see state policymakers implementing more policy strategies that help grow the life sciences sector in their respective states under both the auspices of life sciences and economic development.

An additional trend to watch in 2026Issue Background. Of the trends I noted in 2025, only one (efforts to control the costs of pharmaceuticals) is specifically targeted at addressing the cost and affordability of healthcare. The impact of the actions of state and federal policymakers to improve the affordability of drugs, however, does not seem to be enough yet to curb the overall cost growth in the industry. In fact, of the other trends noted in 2025, some might even be considered cost drivers. For example, mergers and acquisitions and overall consolidation can at times increase costs in some markets, depending on what those mergers include, and for some healthcare consumers who rely on insurance coverage, the loss of the subsidies to pay for healthcare makes that cost increase much more apparent. Although there is some optimism that AI, through process improvement, quicker diagnostics, and disease prevention, could make certain things more efficient, so far, there are mixed results as to whether AI is making healthcare more affordable. With costs for other basic necessities like housing being less affordable, the focus on healthcare affordability is likely to continue in 2026. This is because some consumers will more directly feel the cost of healthcare in 2026, but also because providers have experienced increasing challenges with expenses that contribute to affordability. Examples of areas of expense growth cited by providers include staffing and benefits, supplies, pharmacy, and technology.Industry Responses and Options. Although I previously noted the policy responses of federal and state governments as they relate to these trends, in the case of lowering costs, industry is also responding in new and creative ways. One of the new ways that health systems and providers are attempting to tackle rising prices and costs is through non-traditional partnerships that deliver care, treatments, and services more directly to patients. An example of this is a potential partnership between Humana, an insurance company, and Mark Cuban, co-founder of Cost Plus Drugs. The potential partnership would focus on direct-to-employer programs that cut out companies in the middle, such as PBMs. Another example was the launch of Northwell Direct, a provider system offering direct care to employers without an insurance company. This arrangement is the largest of its kind and recently added a partnership with the influential 32BJ Health Fund, which allows 170,000 participants in the 32BJ Health Fund in the general Northwell service area to have access to the full spectrum of health care services available through Northwell Direct, which is expected to produce significant administrative savings.Policy Responses and Options. One way government policy makers at both the federal and state levels can respond to the affordability crisis is to allow the industry itself to find creative solutions, such as those outlined above. A second way policymakers can respond is by using the authority granted under the ACA for the CMMI to create and experiment with new models of care delivery that could improve care and lower costs. In 2025, CMMI issued at least 6 new payment models, all designed to lower the costs of healthcare. They include some of the ones mentioned above on pharmaceutical cost control, like the GUARD and GLOBE models, but also ones specifically targeting chronic disease, such as the Advancing Chronic Care with Effective Scalable Solutions (ACCESS model), and healthier lifestyles, for example, the Better Approaches to Lifestyle and Nutrition for Comprehensive Health (BALANCE model).

Meanwhile, state governments and officials are proposing various ways to control costs, with over 750 related bills introduced in 2024 alone. Some states are more focused on particular strategies, such as pricing—including hospitals with reference-based pricing. In Indiana, the legislature passed a bill that does not allow hospital systems to exceed prices set before January 1, 2025, for two years. The hospitals would then have to lower prices by a certain percentage each year to reach a goal set by the state’s Office of Management and Budget. For several years now, states have been implementing price transparency policies with the aim of reducing costs. It is, of course, possible that some states will use a combination of these efforts (e.g., promoting industry-initiated efforts through incentives or less regulation to lower costs while also more closely monitoring prices).

Conclusion

The six trends to watch in 2026 noted in this blog are by no means all-encompassing, but they do highlight areas that are likely to garner a lot of attention from policymakers in the near term. As has been true throughout the country’s history, the Federalist system of government allows state and federal governments to develop varied policy approaches to improve how healthcare is funded and delivered. The Rockefeller Institute will be tracking these six trends and will report on any interesting findings, particularly as they relate to the additional trend of the cost and affordability of care in the coming year.

It is a somber year for health care in America. While we commemorate both the 60th anniversary of Medicare and Medicaid and the 15th anniversary of the Affordable Care Act (ACA), we’re watching health-care costs soar to unaffordable levels and millions of Americans lose access to these very programs. Of the many devastating consequences we can anticipate from these policy choices, we should expect to see the crisis of medical debt in America worsen.

But the immediate harms of medical debt, or money owed for past medical care, are solvable problems—and solving them can point us toward bolder solutions to the crisis of unaffordable health care.

During my time as director of policy in the Office of Cook County Board President Toni Preckwinkle, I and my colleague Nish Dittakavi helped launch the Cook County Medical Debt Relief Initiative using federal funding from the American Rescue Plan Act. This established the first publicly funded program in the United States to buy and cancel residents’ medical debt. In June 2025, President Preckwinkle announced that since its launch in 2022, the program has successfully abolished over $664 million in medical debt so far, benefiting 556,815 residents of Cook County, Illinois.

Cook County’s innovative program also catalyzed a movement across state and local governments.1 As my colleagues at the New School’s Institute on Race, Power and Political Economy have found, since Cook County announced its program, 29 state and local governments across 19 states have collectively pledged to eliminate $15.8 billion in debt for more than 6.3 million Americans. As of October 25, 2022, these programs have abolished nearly $11 billion in medical debt on behalf of more than 6 million residents.

We have shown that erasing medical debt like this can transform people’s lives. Now, we must leverage the momentum of debt cancellation to meet our current moment. Rather than leaving us satisfied with the short-term aid we can provide through medical debt cancellation, the popularity and success of these programs must push us to ask bigger questions about the upstream interventions we need to fix a broken health-care system that forces people to accrue this debt in the first place.

Our Medical Debt Crisis Is Bad, and Will Likely Get Worse

Amid rising health-care costs and increasingly stretched household budgets, medical debt has become a frequent focus of policy attention in the US. And with good reason: According to a 2021 KFF analysis, 20 million people, or nearly 1 in 12 adults, owe medical debt, totaling more than $220 billion. The Consumer Financial Protection Bureau (CFPB) found that medical debt accounted for 58 percent of debt in collections that same year.2

This economic burden can quickly spiral, as the Roosevelt Institute’s Stephen Nuñez examined in a May issue brief. Patients may be denied medical care due to unpaid bills or struggle to afford other basic needs like food. As emergency physician and historian Dr. Luke Messac details in Your Money or Your Life: Debt Collection in American Medicine, owing medical debt can impact your credit score and thus your ability to access loans, land you in court, result in wage garnishment (withholding earnings to pay off a debt), and even lead to arrest.3

Sadly, we should expect these numbers to rise thanks to the Trump administration’s gutting of our public health insurance system. Under the administration’s so-called signature legislative achievement, HR 1, an estimated 12 million people will lose health insurance by 2034, and hospitals and community health centers across the country will face severe threats to their solvency. Even sooner, without congressional action by December an additional 24 million people who purchase ACA plans will simultaneously face steep insurance premium increases and cuts to the tax credits that help subsidize these costs—a key focus of the federal government shutdown this fall.

An estimated 12 million people will lose health insurance by 2034, and hospitals and community health centers across the country will face severe threats to their solvency.

By decreasing eligibility for public insurance and increasing the cost many Americans must pay for non-employer-sponsored private insurance, these policy choices will increase medical debt.4

How Myths About Our Health-Care System Perpetuate Medical Debt

Myths that have dominated decades of health policy can trick us into believing medical debt is an unfortunate bug in an otherwise well-designed system.5

Many proponents of the current system claim that cost-sharing (when patients pay for a portion of their care through copayments, coinsurance, and deductibles) benefits the system by making patients more responsible and frugal when they seek care. But this myth conveniently ignores the vast body of evidence that shows cost-sharing decreases adherence to treatment, leads to worse health outcomes, and, importantly, does not lead to decreased total costs across the system.

The myth that health care can function like a traditional market, with the burden on us as consumers to just make more informed choices, hides the reality that we are patients whose access to needed care is determined by factors beyond our control—what insurance, if any, our job provides, what that insurance chooses to cover, the cost-sharing that insurance chooses to require, and the covered medicines set by the pharmacy benefit manager (PBM) that insurer works with (and increasingly owns). The myth that our health-care system is a functioning market that can and will course-correct any problems on its own also leaves us looking for solutions from the very stakeholders who benefit from the structure as it is currently.

The myth that our health-care system is a functioning market that can and will course-correct any problems on its own also leaves us looking for solutions from the very stakeholders who benefit from the structure as it is currently.

The reality is that medical debt is the logical outcome of core characteristics of the American health-care system, which include

high prices set by hospitals, health-care organizations, pharmaceutical companies, and PBMs;

a costly maze created by insurance companies that exclude, deny, and burden people in need;

a system ultimately designed to place the financial burden of care on patients; and

decades of policy that has failed to rectify the cruel and unsustainable harms these choices have created.

Medical Debt Is a Symptom of a Broken System, Not a Solution to Its Troubles

In the constrained environment under which so much of our health-care system operates, it might seem that collecting on medical debt is unfortunate but essential to keeping the system afloat. Yet even the most aggressive debt collection practices do not generate substantial revenue for hospitals and health-care organizations, as evidenced by a 2017 study in Virginia that found suing patients and garnishing their wages comprised only 0.1 percent of hospital revenue on average. Dr. Marty Makary, a coauthor of the study and the current commissioner of the Food and Drug Administration under the Trump administration, put the implications bluntly: “The argument that we have to do something this ugly in order to stay afloat is not supported by the data.”

Hospitals and health systems know this too, and recognize that most patients with debt simply cannot afford to pay. Precisely because the prospect of collecting full payment is so low, many choose instead to sell this debt cheaply—for pennies on the dollar—and write it off as a loss on their taxes. The cheapness of this debt is what allows cancellation programs like Cook County’s to achieve the high return on investment that is part of their popularity and success.6

This alone should point us to a fundamental question: If we can buy medical debt so cheaply and cancel it so easily, is this debt really necessary in the first place?

Of course, our health-care system needs significant resources to function. But if we are serious about finding sustainable revenue streams to stabilize it, we must acknowledge the needed money will not come from medical debt collection, nor from any other solution that increases the already heavy burden on individuals and maintains the power of the private sector.

Even as CMS documents improper denials, ghost networks and unlawful out-of-pocket charges, enforcement remains weak with just $3 million in fines levied in early 2025 against billion-dollar insurers.

Enrolling in Traditional Medicare means paying more upfront to protect against catastrophic costs because Traditional Medicare lacks an out-of-pocket cap, but in return, you get the care your treating physicians recommend you need. In stark contrast, enrolling in Medicare Advantage typically means allowing a for-profit insurer to second-guess your treating physician and inappropriately delay or deny the care you need, forcing you to gamble with your health and, sometimes, your life. What’s worse is that our federal government is rarely willing or able to punish Medicare Advantage insurers for their bad acts. Consequently, Medicare Advantage insurers too often can get away with restricting access to specialists and specialty hospitals and not covering the treatments their enrollees are entitled to.

Penalties on Medicare Advantage insurers that deprive their enrollees of the care they need are few and far between. In the first four months of 2025, the Trump administration imposed more penalties on the insurers in Medicare Advantage than they faced during the entire four years of the Biden administration. Still, it only imposed about $3 million in penalties, reports Rebecca Pifer Parduhn for HealthcareDive. That is tiny relative to the billions in profits of the big insurers.

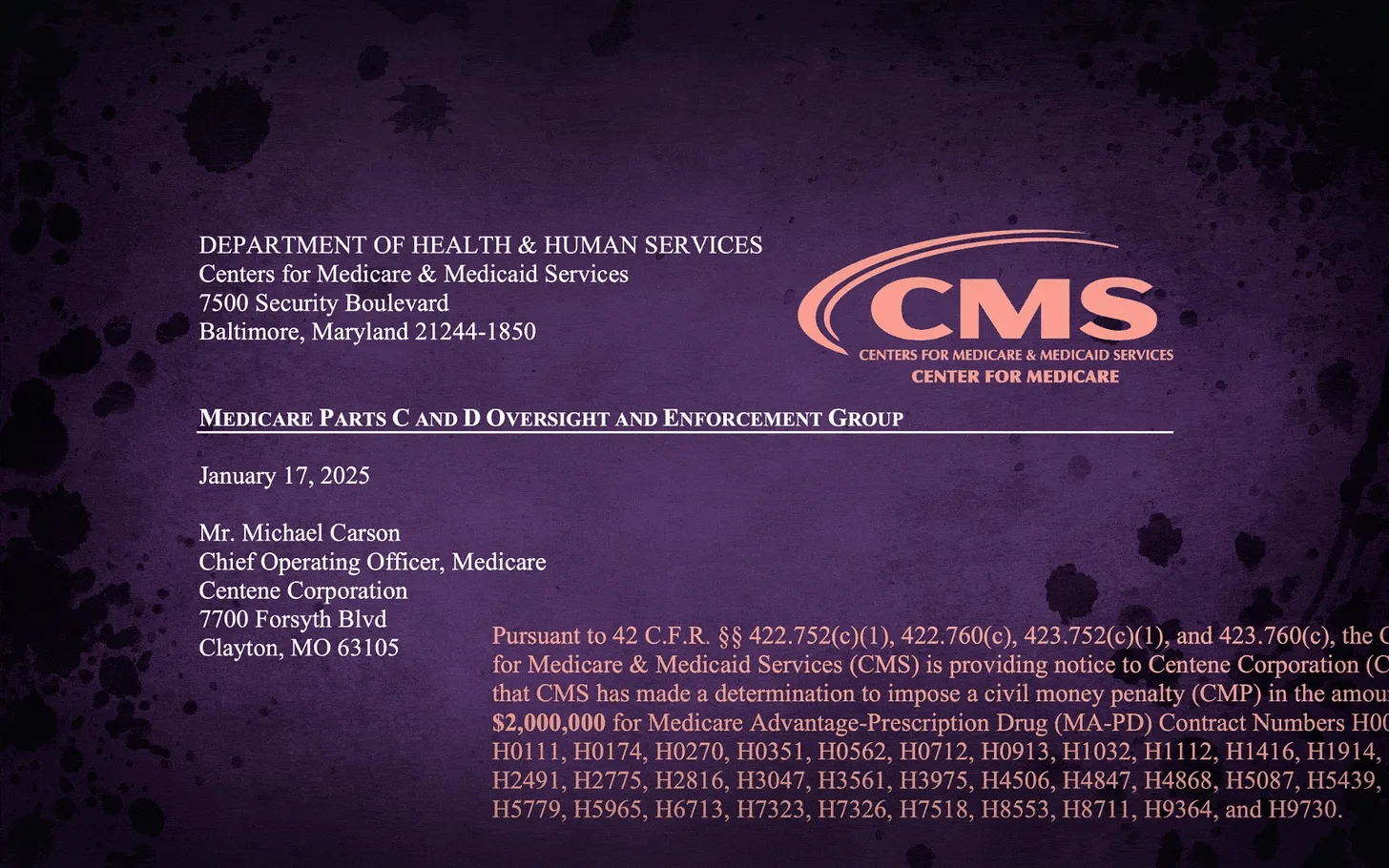

Most of the penalties the Centers for Medicare & Medicaid Services (CMS) has imposed in the last few years for Medicare Advantage insurer violations are under $50,000. Penalties imposed were for serious offenses, including improper insurer delays and denials of care and insurers requiring people to spend more out of their own pockets than allowed under the law. Centene was hit with the largest penalty of $2 million for charging its enrollees above the out-of-pocket maximum permitted to be charged, in violation of 42 C.F.R. Part 422, Subpart C.

Molina received the second largest penalty of just over $285,000 for its failure to comply with prescription drug coverage requirements. CMS said that Molina’s failure was “systemic and adversely affected, or had the substantial likelihood of adversely affecting, enrollees because the enrollees experienced delayed access to medications, paid out-of-pocket costs for medications, or never received medications.” It’s hard to believe that Molina didn’t substantially benefit financially from its violations even after paying the $285,000 fine.

Susan Jaffe reports for KFF News that over a seven-year stretch between 2016 and 2022, CMS, under both Trump and Biden, did almost nothing to ensure network adequacy for Medicare Advantage enrollees. Moreover, it did very little to penalize the Medicare Advantage insurers CMS identified as operating Medicare Advantage plans with inadequate networks.

After KFF made a Freedom of Information Act request regarding enforcement actions against Medicare Advantage insurers with inadequate networks, CMS turned over just five letters to insurers regarding seven MA plans with inadequate provider networks. Given the widespread reporting of network inadequacy in Medicare Advantage, it’s inconceivable that only seven MA plans had inadequate networks. When questioned as to why CMS took action in so few instances, the agency explained that it is not overseeing all of the more than 3,000 Medicare Advantage plans but conducting “targeted” reviews of Medicare Advantage plan provider networks.

What’s clear is that CMS does not begin to have the resources to oversee more than 3,000 Medicare Advantage plans to ensure they are in compliance with their contractual obligations and delivering the care they are required to. As a result, Medicare Advantage enrollees are left unprotected. Too often, Medicare Advantage plans have “ghost networks,” networks that look good in the provider directory but turn out to include physicians who are out of network. These MA plans might not have enough primary care physicians, mental health providers, specialists, hospitals, nursing homes, rehab facilities or mental health professionals in their networks.

Technically, CMS can prevent insurers with inadequate networks from marketing their Medicare Advantage plans, freeze enrollment, fine them or even terminate the Medicare Advantage plans. But it never has. In its June 2024 report, the Medicare Payment Advisory Commission (MedPAC) wrote: “CMS has the authority to impose sanctions for noncompliance with network adequacy standards but has never done so.” CMS often doesn’t even let Medicare Advantage enrollees know about the inadequacy of the provider network or allow enrollees the ability to disenroll.

For CMS to oversee Medicare Advantage plans effectively and impose sanctions where appropriate it would need far more resources than it currently has. Moreover, penalties would likely need to be non-discretionary or they would be subject to political interference. In addition, to simplify the process and reduce costs, insurers likely would need to be required to offer the same network for all their Medicare Advantage plans in a given community.

As media attention focused on Minneapolis, Greenland and Venezuela last week, the Center for Medicaid and Medicare Services (CMS) released its 2024 Health Expenditures report Thursday: the headline was “Health care spending in the US reached $5.3 trillion and increased 7.2% in 2024, similar to growth of 7.4% in 2023, as increased demand for health care influenced this two-year trend. “

Less media attention was given two Labor Department reports released the Tuesday before:

Prices: The consumer-price index (CPI) for December came in somewhat higher than expected with an increase of 0.3% and 2.7% over the past 12 months. Overall inflation isn’t rising, but it also isn’t coming down.

Wages: The Labor Department reported average hourly earnings after inflation in the last year rose 0.7% during the first five months of this year, but real hourly earnings have declined 0.2% since May. They’re stuck.

Prices are increasing but wages for most hourly workers aren’t keeping pace. That’s why affordability is the top concern for voters.

Meanwhile, the health economy continues to grow—no surprise. It’s a concern to voters only to the extent it’s impacting their ability to pay their household bills. They don’t care or comprehend a health economy that’s complex and global; they care about their out-of-pocket obligations and surprise bills that could wipe them out.

As Michael Chernow, MedPAC chair and respected Harvard Health Policy professor wrote:

“The headline number, 7.2% growth in 2024, is concerning but hardly a surprise. It follows 7.4% growth in 2023. This rate of NHE growth is not sustainable. It exceeds general inflation and growth in the gross domestic product (GDP), pushing the share if GDP devoted to health care spending to 18% in 2024; the share of GDP devoted to health care is projected to rise to 20.3% by 2033. In fact, these figures may be an underestimate of the fiscal burden of the health care system because spending on some things, such as employer administrative costs, are not captured… Given all the attention to prices and insurer profits, it is important to note that those factors are not the main drivers of spending growth—this time, it’s not the prices, stupid. There was virtually no excess medical inflation (medical inflation above general inflation) for 2023 or 2024. In fact, prices for retail drugs (net of rebates) rose at a rate below inflation. There will certainly be cases of rising prices driving spending, but on average, price growth is not the problem. This does not mean high-priced products and services are not an important component of spending growth, but instead it implies that their contribution to spending growth on average stems from their greater use, not rising prices. The main driver of spending growth is greater volume and intensity of care…”

My take:

Since 2000 to 2024, total healthcare spending in the U.S. has been volatile:

2000–2007: High growth, typically 6–8% per year (driven by rising utilization and prices).

2008–2013: Growth slowed to 3–4% during and after the Great Recession.

2014–2016: Growth ticked up to 4.5–5.8% with ACA coverage expansion.

2017–2019: Moderation around 4.5%.

2020: COVID‑19 shock—growth slowed to ~2% due to deferred care.

2021: Rebound to ~4%.

2022: 4.8%, close to pre‑pandemic norms.

2023: 7.4%, fastest since 1991–92.

2024: 7.2%, reaching $5.3 trillion (18% of GDP)

Between 2000 and 2024, total health spending in the U.S. increased $3.9 trillion (279%) while the U.S. population grew by 58 million (20.4%). 2025 spending is expected to follow suit. The underlying reason for the disconnect between health spending and population growth is more complicated than placing blame on any one sector or trend: it’s true in the U.S. and every other developed system in the world. Healthcare is expensive and it’s costing more.

This is good news if you’ve made smart bets as an investor in the health industry but it’s problematic for just about everyone else including many in the industry who’ve benefited from its aversion to spending controls and cost cutting.

The current environment for the healthcare economy is increasingly hostile to the status quo. Voters think the system is wasteful, needlessly complicated and profitable. Lawmakers think it’s no man’s land for substantive change, defaulting to price transparency, increased competition and state regulation in response. Private employers, who’ve bear the brunt of the system’s ineffectiveness, are timid and reformers are impractical about the role of private capital in the health economy’s financing.

The healthcare economy will be an issue in Campaign 2026 not because aggregate spending increased 7-8% in 2025 per CMS, but because it’s no longer justifiable to a majority of Americans for whom it’s simply not affordable. Regrettably, as noted in Corporate Board Member’s director surveys, only one in five healthcare Boards is doing scenario planning with this possibility in mind.

P.S. The President released his Great Healthcare Plan last Thursday featuring his familiar themes—price transparency for hospitals and insurers, most favored pricing and elimination of PBMs to reduce prescription drug costs—along with health savings accounts for consumers in lieu of insurance subsidies. The 2-page White House release provided no additional details.

Last Tuesday, HCA, the largest investor-owned hospital system, released their Q4 2025 and year-end earnings and they’re impressive. The 190-hospital system reported:

Net income of $6.8 billion in 2025, a 17.8% increase year over year.

Revenue of $75.6 billion, a 7.1% increase year over year.

On a same facility basis, growth in revenue of 6.6%, equivalent admissions of 2.4% and net revenue per equivalent admission of 4.1% versus prior year.

For 2026, projected a net income between $6.5 billion and $7 billion and adjusted EBITDA between $15.6 and $16.5 billion on revenue between $76.5 billion and $80 billion.

CFO Mike Marks told the 16 analysts on the investor call “Consolidated adjusted EBITDA increased 12.1% over prior year, and we delivered a 90-basis point improvement in adjusted EBITDA margin. Cash flow from operations was $2.4 billion in the (4th) quarter and $12.6 billion for the year. This represents a 20% increase in operating cash flow in 2025 over full year 2024.”

And CEO Sam Hazen added “Let me add to just the whole resiliency agenda. This is not an episodic event for us. It just happens to be a maturation of what in my estimation is cultural within HCA, and that is being cost effective in finding ways to leverage scale, utilize best practices. Now we have tools… that are in front of us as opportunities to create even more consistency, efficiencies and transparency in the company’s overall cost. And that’s why the program is lining up in a well-timed manner with some of the enhanced premium tax credit challenges.

But we see this program continuing to mature. And as we get more capable at using these tools, it’s going to help us find even more opportunities. But this is not a onetime event. It’s a cultural dynamic in our company around being cost effective, being high quality and finding ways to improve from a process standpoint and a leverage standpoint with our overall scale.”

Shares of HCA closed at $488.27 last week, down from its peak at $527.55 (January27). Per MarketWatch, “shares of HCA Healthcare Inc rose $1.19% to $488.27 Friday on what proved to be an around grim trading session for the stock market, with the S&P Index falling 0.43% to 6939.03 and Dow (DJIA) falling 0.36% to 48,892.47. The stock demonstrated a mixed performance when compared to some of its competitors Friday, as Community Health Systems (CYH) rose 1.26% to $3.21 and Tenet (THC) fell 0.11% to $189.28.”

Hospital stock market analysts are keen to gauge how companies like these are navigating choppy waters for healthcare. It’s understandable: Healthcare is one of the 11 sectors that comprises the overall S&P 500 and is 9.6% of its weighting. Historically, the healthcare index had beaten the S&P (30-year average 9% vs. 8% overall) but in recent years, it has lagged largely because regulatory policy changes and healthcare budget volatility dampened investor confidence.

Investors are increasingly hedging their bets in healthcare services reasoning even market bell-weathers like HCA face headwinds. And that sentiment has profound impact on operators in not-for-profit health sectors like community and rural hospitals, nursing and home care and ancillary services like EMS, hospice care and others that see their credit-worthiness slipping and costs for debt capital increasing.

My take

HCA is not an exception. It is culturally geared to the business of running hospitals and amassing scale in its markets vis a vis outpatient services and physician relationships. It follows a playbook geared to earnings per share and strategic deployment of capital to optimize its ROC, and it rewards its leaders accordingly. These are not unique to HCA.

And, like other systems, HCA is a lightning rod for critics. Studies have shown for-profit hospitals lean on staffing, aggressive on procurement, concerning to physicians and increasingly problematic to private insurers. Those same studies have shown quality of care to be comparable and charity care to be at or above same-market competitors. But this discipline also enables a higher price to cost ratio, a better payer mix and pruning of clinical services where margins are thin. Again, leverage in payer contracts and high pricing are not unique to the HCA playbook. Some not-for-profit systems have done the same or better.

What’s unique for each system like HCA are 1-the markets in which they enjoy leverage by virtue of scale and 2-the aggressiveness whereby they use their leverage. Ownership status—not for profit vs. investor-owned—matters in some markets and organizations more than others. But market dominance by any system, and how it’s leveraged, is a differentiator.

Case in point: In Asheville NC, HCA’s Mission Health dominates. HCA paid $1.5 billion for the legacy Mission-St. Joseph’s system in 2019. Despite, difficult media coverage and 3 warnings from CMS about quality shortcomings, it’s profitable.

On December 10, 2025, I had quadruple by-pass surgery there. Over the course 2 ED visits in November, the 5-day inpatient stay and post-surgical interactions since, I had the opportunity to see its operations firsthand. The bottom line for me is this: HCA Healthcare is a successful business. It operates Mission aggressively and profitably. Every employee knows it. Staffing is lean. There are no frills. Coordination of care is a crap shoot: connectivity between offices, services, and physicians is limited; price transparency is a joke and care navigation for patients like me is haphazard. But all say patient care is not compromised as my surgical experience confirmed. Every hospital aspires for the same. All are trying to do more with less.

HCA’s financial success is not the exception in acute care, but it’s certain to draw attention to business practices that enable results like it enjoyed last year across the spectrum of hospital care. And it’s certain to intensify competition between hospitals to get the upper hand.

References in addition to citations in the sections that follow:

Most industries enjoy a luxury that U.S. healthcare does not. In professional services, retail, logistics and software, leaders can respond quickly when conditions change. Companies can shrink or expand the workforce, adopt innovative technologies or reconfigure operations within months.

Healthcare lacks that flexibility. Training new physicians takes a decade, making it difficult to adjust workforce supply to meet changing demand. And unlike other industries, hospitals cannot rapidly cut services or reduce capacity. In fact, most clinical service changes require regulatory approval, turning cost reduction into a multiyear process.

With timelines like these, course correction in healthcare is inherently slow. Problems that might have been manageable persist. And by the time leaders act, threats frequently become too large to reverse.

Three of the nation’s most pressing healthcare problems now face this reality:

Threat 1: The affordability cliff

Over the past 25 years, the nation’s total healthcare spending has climbed from $2 trillion to $5.3 trillion.

Businesses and the government have played “hot potato” in response to these rising costs. Employers slowed wage growth and switched to high-deductible health plans to offset ever-higher premiums. In parallel, Medicare and Medicaid set payment increases below the rising cost of delivering care, driving hospitals and physicians to make up the difference through higher charges in the private market.

The financial impact on families has been devastating. With healthcare costs rising faster than wages, half of Americans say they cannot afford their out-of-pocket expenses should they experienced a major illness.

For businesses, the government and families, these financial challenges are mounting with no relief in sight. In 2024, U.S. medical costs rose more than 7% for the second consecutive year, pushing healthcare’s share of the economy to roughly 18%. Out-of-pocket spending by consumers climbed 7.2%, exceeding $500 billion, as demand for hospital care, prescription drugs and physician services outpaced insurer projections. Moreover, insurance premiums are projected to rise by roughly 9% this year.

Congressional action (and inaction) is amplifying these pressures. The expiration of enhanced subsidies on the insurance exchanges is driving double- and even triple-digit percentage premium increases for roughly 20 million enrollees. And beginning this year, another 8 to 10 million Americans could lose Medicaid coverage as new eligibility restrictions take effect.

Absent major intervention, healthcare spending is projected to exceed $7 trillion by the end of the decade, consuming more than one-fifth of the U.S. economy. At that point, small businesses will have dropped coverage for millions of employees, and a growing share of federal spending will be diverted to interest payments on the national debt, squeezing Medicare, Medicaid and other healthcare programs as demand for medical care rises.

As long as the economy stays strong, businesses and policymakers will respond with incremental changes that dull the pain but fail to address the cause. Consequently, when the next recession begins (perhaps sooner than later, according to historical analyses), the economic crisis will become so large that solutions dependent on improving patients’ health will be too small and take too long to succeed. That brings up the second major challenge.

Threat 2: The chronic disease epidemic

Since the final decade of the 21st century, the United States has experienced a sustained and worsening epidemic of chronic disease.

According to the Centers for Disease Control and Prevention, roughly 194 million U.S. adults now live with at least one chronic condition. About 130 million report multiple chronic diseases.

You might assume that if the healthcare system could prevent younger generations from developing these conditions, total costs would fall. But prevention alone cannot offset the cumulative burden of chronic disease already embedded in the American population.

To understand why, consider a single condition: diabetes.

A patient newly diagnosed with diabetes can usually control it and avoid serious, costly complications through lifestyle changes and relatively low-cost medications.

But when diabetes remains poorly controlled for a decade, biological damage accumulates. Each year, the risk of kidney failure or heart attack rises significantly. As a result, the cost of caring for a single patient with long-standing diabetes outweighs the savings that result from preventing diabetes in multiple newly diagnosed patients.

The math: On average, people with diabetes incur medical costs about 2.6 times higher than those without the disease (around $25,000 more per patient each year).

But when diabetes progresses to kidney failure, spending jumps into an entirely different category. Medicare costs for one patient’s hemodialysis treatment is approximately $100,000 annually. That’s not accounting for the cost of treating a patient’s likely cardiovascular disease, the leading cause of death among people with diabetes.

As such, to offset the medical care costs for a patient with a history of diabetes, our nation would need to prevent four new cases.

Add all these pieces together and diabetes alone accounts for more than $300 billion in direct medical costs each year, plus another $100 billion in indirect costs from disability and lost productivity.

Furthermore, effective chronic disease control requires large upfront investment, while the financial returns arrive years later. Act now, and the returns will be substantial. Based on CDC estimates, better prevention and control of chronic disease could avert up to half of all heart attacks, strokes, cancers and kidney failures, reducing national healthcare spending by $1 to $1.5 trillion each year. But if policymakers wait (while healthcare spending rises 7% or more annually), by the time they confront the crisis, they won’t be able to proceed financially since the required investment will be far more expensive than the payoff, at least in the short run.

Finally, if the U.S, wants to effectively prevent and control chronic disease as the means to reduce healthcare costs, there’s a third challenge our nation will need to address.

Threat 3: Training doctors for the wrong future

Ask medical leaders what they view as the greatest threat to high-quality care in the United States, and most will point to the growing physician shortage.

The Association of American Medical Colleges projects a shortfall of up to 86,000 physicians by 2036, with nearly half of that deficit in primary care. But those projections rest on a false assumption: the way doctors deliver care will be the same in 2036 as it is today.

If the United States has any hope of containing healthcare costs and reversing the chronic disease epidemic, it won’t happen by simply training more physicians.

Instead, countering those threats will require a transformation in how care is delivered. And generative AI will play a central role. But how?

Today, advances in medical knowledge allow physicians to effectively follow well-defined, evidence-based pathways for managing chronic disease in all but the most complex cases. As a result, most routine management tasks (monitoring, medication adjustments and decision support) are primed for generative AI. This transition has already begun.

A San Francisco startup, Mercor, recently earned a $10 billion valuation after recruiting more than 30,000 clinicians to help train AI systems to perform specialized medical tasks. Meanwhile, Utah just became the first state to launch a pilot allowing an AI system to renew prescriptions for 250 commonly used, non-controlled medications under physician oversight.

The implications for medical practice are clear. We can expect that generative AI will take on more routine chronic disease management, leaving primary care physicians more time to focus on complex clinical tasks. With AI support, they will increasingly care for patients who today are referred to specialists.

Specialists, in turn, will spend less time on evaluation and follow-up visits and more time performing procedures and advanced interventions that require human judgment and technical skill.

The combination of healthier patients and the redistribution of work (enabled by generative AI) will ease the physician-shortage problem. To prepare for this outcome, medical schools and residency programs will need to quickly integrate generative AI into every aspect of training. If not, physicians in many specialties will find themselves trained for the roles of the past, not the skills they will require a decade from now.

When Systems Fail, They Fail Together

When chronic disease becomes widespread and clinicians are overwhelmed, America’s health deteriorates, complications ensue and healthcare costs surge.

When chronic disease is managed effectively, the opposite occurs: hospitalizations fall, costly complications become rarer and the demand for specialty care declines.

For decades, healthcare has consumed an ever-larger share of GDP, while clinicians practiced medicine much as their mentors have for generations.

That era is ending. With costs accelerating and incremental fixes exhausted, healthcare is approaching a breaking point. Act aggressively, now, and the nation can prevent and better control chronic disease, avert hundreds of thousands of heart attacks, strokes and kidney failures, and flatten healthcare inflation.

By contrast, wait another decade and there will be no way to rein in spending or chronic disease. And if workforce adaptation is delayed, as many as 30% of physicians will find themselves trained for a version of medicine that no longer exists.