With commercial medical costs projected to increase 9.0% in 2027, patients are feeling the financial squeeze from administrative friction generated by the payer-provider AI arms race.

KEY TAKEAWAYS

PwC projects a 9.0% commercial medical cost trend for group plans in 2027, driven by structural inflators like AI-enabled documentation tools, rising specialty pharmacy costs, and IDR payments.

As payers aggressively deploy AI-driven pre-payment reviews to combat rising costs, providers are automating their defenses, creating an expensive administrative arms race that fails to lower systemic costs for the consumer.

To navigate this financial squeeze without alienating their communities, health systems must shift away from back-end collections and prioritize transparent, empathetic pre-service financial clearance.

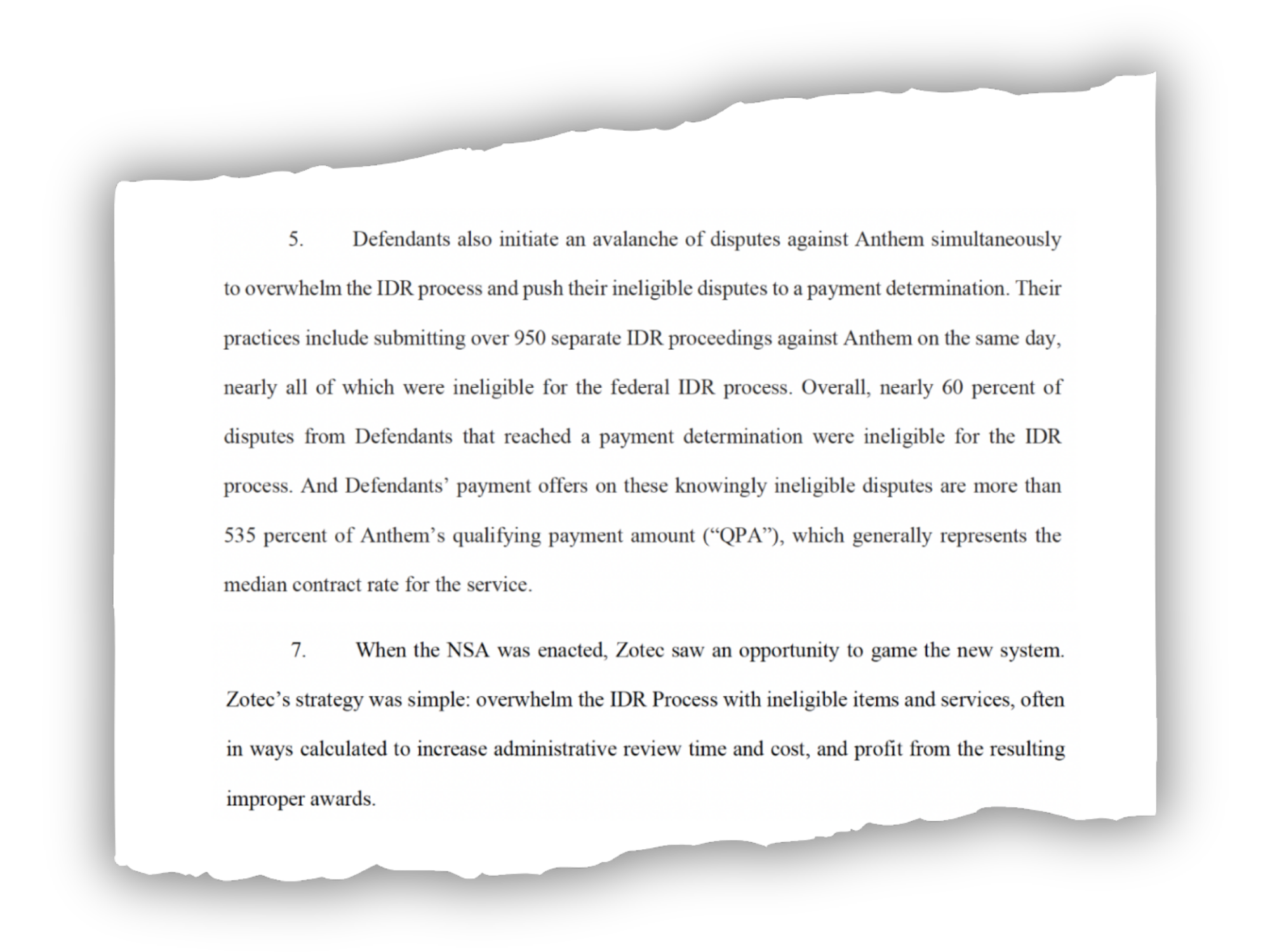

Last year, PwC projected a 8.5% medical cost spike in the commercial group market. Unfortunately, the professional services company’s forecast for the next year does not suggest there will be any relief for rising healthcare costs.

According to PwC’s latest Medical Cost Trend: Behind the Numbers report, the 2026 group cost trend has been retroactively adjusted upward to 9.0%. Looking ahead to 2027, health plan actuaries expect that 9.0% growth rate to sustain in the group market, alongside an 8.5% increase in the individual market.

With historical deflators, like biosimilars and site-of-care shifts now fully embedded into the baseline, the cost environment heading into 2027 represents a structural shift rather than a temporary spike, according to the report.

Five Cost Inflators in 2027

Health plan actuaries point to five distinct inflators driving medical costs higher across the commercial sector.

1. AI-Enabled Revenue Optimization

While revenue cycle leaders may say that payers started the battle of the bots, provider use of AI-powered scribes and ambient documentation tools are leading to higher E/M levels and higher-severity DRG assignments. Consequently, health plans are seeing higher billed allowed amounts and increasing per-member-per-month trends without a corresponding change in actual care utilization or contracted rates.

2. Provider Reimbursement Pressures

Hospitals continue to face elevated labor expenses and rising input costs for drugs and supplies. To offset these structural costs, health systems are leveraging market consolidation to negotiate higher commercial reimbursement rates.

3. Surging Pharmacy Costs

Pharmacy trend continues to outpace overall medical trend. Spending on cancer medicines alone reached $143 billion in 2025. Additionally, high-cost GLP-1 therapies are expanding well beyond obesity treatment, securing FDA approvals for cardiovascular disease and chronic kidney disease.

4. Behavioral Health Utilization

Between 2018 and 2024, behavioral health visit rates increased by 62.6%. Unlike other medical categories that are driven by unit cost, the behavioral health trend is actively fueled by sustained increases in patient utilization.

5. IDR Arbitration

The No Surprises Act’s Independent Dispute Resolution (IDR) process has become a significant revenue driver for providers. Providers won roughly 88% of payment determinations in the first half of 2025. A 2025 report found that IDR had generated $5 billion in costs, including $2.24 billion in direct payments to providers.

Looking at the Bigger Picture

While AI has been sold as a tool to improve efficiency, the technology has so far driven an expensive administrative arms race rather than acting as a systemic cost deflator. On the health systems side, providers are using AI-powered scribes and documentation tools to capture greater complexity and patient acuity. Meanwhile, health plans are deploying their own technology to auto-triage complex claims, detect billing anomalies, and flag provider outliers before funds are ever released.

Administrative friction between providers and payers ultimately causes patients to delay or interrupt necessary clinical care. It is critical that payers and providers work together to prevent this, according to Ryan Thompson, Chief Revenue Cycle Officer at Providence.

“It’s incumbent on both payers and providers to identify what we can do differently to mitigate that friction that causes patients to interrupt or delay care,” Thompson says.

This puts revenue cycle leaders in a tricky position, where they are expected to drive collections from cash-strapped patients without alienating local communities by focusing solely on revenue optimization.

To counteract the 2027 cost trajectory without damaging patient trust, health systems must prioritize transparent, pre-service financial clearance. Ryan Klein, Senior Director of Patient Access and Financial Experience at UW Health, emphasized that leaning into empathy and flexibility ultimately protects both the patient and the bottom line.

“An experience-first approach, I don’t think it undermines revenue goals,” Klein stated. “I think it just simply sets up the patient to contribute to their out-of-pocket liability in the way that best works for them.”

The Federal IDR Operations final rule introduces vital changes to fees, batching, and eligibility, but a lack of federal enforcement leaves providers battling payers for post-decision payments.

KEY TAKEAWAYS

The final rule slashes administrative fees and relaxes batching constraints to make pursuing lower-dollar claims much more financially viable for providers.

Payers must now provide essential claim details upfront to streamline eligibility determinations and reduce administrative friction.

Revenue cycle leaders should advocate for legislative action to hold payers accountable because the new rule lacks mechanisms to enforce post-decision payments.

While there is a significant administrative lift that comes with navigating the Federal Independent Dispute Resolution (IDR) process comes with a heavy administrative lift, the system has proven to be a significant driver of recovered revenue for providers.

To address operational friction for all parties, federal regulators have finalized the Federal IDR Operations rule. This update includes adjustments designed to standardize data, clarify timelines, and streamline the process.

For revenue cycle leaders, understanding these updates is essential to maintaining compliance and optimizing cash flow without adding unnecessary overhead.

Open Negotiation and Communication

The final rule mandates that all parties use the federal open negotiation portal to initiate the dispute process.

This requires providers to submit standardized data elements, creating a uniform communication channel. By centralizing the exchange, regulators aim to move away from the chaotic web of emails and spreadsheets that have often complicated early-stage resolutions.

Clarifying Eligibility

Determining IDR eligibility has been a time-consuming step for revenue cycle teams, but the final rule shifts more responsibility to payers.

Payers must now provide essential claim details at the time of the initial payment or denial. This includes the Qualifying Payment Amount (QPA) and specific remittance codes indicating whether a claim falls under state or federal jurisdiction. This upfront transparency allows providers to accurately assess eligibility before committing resources to a dispute.

Reducing IDR Fees

Perhaps most notably, the final rule reduces the non-refundable administrative fee to just $15 per party, per dispute. This represents an 85% drop from the previous $115 rate.

While the final rule establishes that these fees will now be collected earlier in the workflow to maintain system capacity, the lower financial barrier to entry makes it far more viable for providers to pursue arbitration for lower-dollar claims. Ultimately, this allows revenue cycle teams to seek out-of-network reimbursements without the fear that the administrative cost of the dispute will eclipse the potential recovery.

Revamped Batching Rules

New batching rules will help providers to more efficiently manage IDR costs and consolidate efforts by relaxing previous constraints and offering clearer guidelines for grouping claims.

Providers can now batch items and services billed under the same or similar service codes. To qualify, these claims must involve the same provider and the same payer, and they must have occurred within a specified 30-day window.

Enforcing the Cooling-Off Period

The NSA originally established a 90-day cooling-off period following a final determination to help manage dispute volumes.

The final rule explicitly clarifies how this timeline is triggered and applied. Providers cannot continuously submit the same disputed item or service code for the same payer once a determination is made. Revenue cycle teams will need to refine their internal tracking processes to ensure compliance with the cooling-off window and avoid administrative dismissals.

Will Payers Play Nice?

While the final rule clarifies details of the IDR process, it neglected to address comments from providers calling for an enforcement mechanism. Health systems are increasingly winning their IDR cases, only to find that payers are simply refusing to remit the owed amounts, according to Kathy Stull, manager of revenue cycle and analytics for HFMA.

“Instead of even getting the incorrect payment, they’re not going to pay anything,” Stull noted during the recent HFMA Region 1 Annual Conference.

If payers fail to make post-decision payments, revenue cycle leaders and health system government relations teams should advocate for H.R. 4710, a proposed bill that would impose civil monetary penalties on insurers for every instance they fail to pay following an IDR loss.

Presbyterian Healthcare Services’ decision to exit most Medicare Advantage plans and eliminate 150 positions underscores a growing reality for provider-sponsored health plans.

KEY TAKEAWAYS

Rising utilization, reimbursement pressure and regulatory scrutiny are forcing organizations to reassess participation in Medicare Advantage.

Presbyterian’s move reflects a decision to prioritize care delivery and long-term financial stability over maintaining an unprofitable business line.

Financial flexibility and access to capital increasingly depend on demonstrating disciplined balance-sheet management.

Albuquerque-based Presbyterian Healthcare Services has announced it will discontinue most of its Medicare Advantage (MA) offerings beginning in 2027, affecting roughly 30,000 members, while laying off approximately 150 health plan and administrative employees. The system will continue operating its Dual Plus Special Needs Plan serving Medicare-Medicaid beneficiaries. According to Presbyterian, remaining in the broader MA market would limit its ability to invest in care delivery, workforce development and access initiatives across New Mexico. The move is another indication that provider-sponsored health plans are facing mounting pressure as MA margins tighten nationwide.

Many health systems entered Medicare Advantage to create integrated delivery models, diversify revenue streams and capture greater value from population health initiatives. However, elevated medical utilization, changing reimbursement dynamics and increased regulatory oversight have altered the financial equation. Presbyterian’s decision suggests leadership determined that the returns no longer justified the capital and operational resources required to compete effectively in the market.

The regional implications are significant. Presbyterian is one of New Mexico’s largest healthcare organizations, operating hospitals, clinics, physician practices and a health plan across the state. While the layoffs are concentrated in health plan and administrative roles, the exit removes a major local MA option and will require thousands of seniors to seek alternative coverage. At the same time, Presbyterian argues the move will allow it to redirect resources toward direct patient care and workforce investments, potentially strengthening healthcare delivery capacity over the long term.

There’s a larger lesson centered on strategic focus. Organizations often face pressure to maintain market presence across multiple business lines, even when margins deteriorate. Presbyterian’s action demonstrates the importance of regularly evaluating whether each service line advances the system’s long-term mission and financial objectives. Exiting a business can be difficult, but preserving capital for higher-value investments may ultimately create greater organizational resilience.

The decision also highlights why credit ratings deserve ongoing executive attention. Strong ratings are not simply a borrowing metric; they influence an organization’s ability to finance facilities, technology modernization, workforce initiatives and strategic growth. Rating agencies increasingly scrutinize operating performance, liquidity, leverage, governance and management’s willingness to make difficult strategic decisions when market conditions change. Fitch continues to maintain coverage on Presbyterian Healthcare Services, underscoring the importance of external evaluation of health system financial strength.

Healthcare organizations that delay corrective action risk eroding margins, weakening liquidity and increasing borrowing costs. Conversely, systems that demonstrate disciplined portfolio management often preserve stronger credit profiles and maintain greater access to capital during periods of industry disruption.

Presbyterian’s Medicare Advantage could signal a move towards strategic capital allocation, a growing priority in today’s environment. As reimbursement uncertainty and utilization pressures continue across healthcare, CFOs should view the announcement as a reminder that financial sustainability sometimes requires difficult choices today to preserve organizational strength tomorrow.

Policy momentum continues to shift toward prevention, affordability, and population health, which is increasing the value of physician alignment and care management capabilities.

The biggest risk in price transparency isn’t fines—it’s how increased visibility into payer contracts and pricing structures could affect margins, negotiations, and market position.

One healthcare organization’s restructuring highlights a broader industry shift toward rewarding sustainable cash flow, liquidity, and financial flexibility over leveraged growth models.

Headline: Free primary care for all: Democratic think tank pushes the party on new health policy

Democratic strategists are promoting free primary care for all Americans as a more politically viable alternative to Medicare for All, aiming to address healthcare affordability and access ahead of the 2026 elections.

Why it matters: I do not think this proposal will become federal policy in the near future. However, it reflects a shift in healthcare reform politics. Instead of focusing on comprehensive insurance redesign, policymakers are increasingly exploring targeted affordability initiatives that can be more easily communicated to voters and potentially implemented incrementally. I have little doubt that primary care access, preventive services, and healthcare affordability are likely to remain prominent policy themes heading into the midterm election cycle.

The CFO Takeaway: This headline underscores the idea that primary care is becoming a strategic asset. If policymakers continue moving toward subsidized or universally accessible primary care models, health systems with strong employed physician networks, value-based care capabilities, and population health infrastructure could be positioned to benefit.

On the other hand, organizations that remain heavily dependent on downstream specialty and procedural volumes may feel the heat as policymakers and payers redirect resources toward prevention and early intervention. I say look at this as another signal that future reimbursement models may reward access, chronic disease management, and longitudinal patient engagement rather than episodic acute care. The question is not whether free primary care becomes law, but whether an organization’s capital allocation, physician alignment strategy, and care delivery model are prepared for a healthcare economy that places greater financial value on keeping patients healthy rather than treating them after they become sick.

Headline: Trump administration warns more than 500 hospitals to provide more price information or face fines

The Trump administration has intensified enforcement of hospital price transparency rules, warning more than 500 hospitals over alleged noncompliance. Hospitals that fail to disclose required pricing data could face penalties of up to $2 million annually, with officials signaling that additional enforcement actions are likely as the administration intensifies oversight of transparency requirements originally established during President Trump’s first term.

The CFO Takeaway: While hospitals have been required to publish machine-readable files and consumer-friendly pricing information for years, compliance has been uneven across the industry. Many CFOs have spoken to me about the difficulty in publishing usable pricing information; standardizing the masses of varying data is often just too complex and time consuming. This move is the administration’s latest shift from rulemaking toward active enforcement in this category. CFOs should focus on strengthening pricing governance, contract management, and payer negotiation strategies. The bigger risk is whether increased transparency exposes pricing weaknesses that could undermine future reimbursement, market position, and margins.

Industry POV: This headline is not fundamentally about fines, it’s about margin visibility and negotiating leverage. Price transparency is becoming a strategic financial issue. As payer rates and pricing differences become more visible, hospitals will face greater scrutiny from employers, insurers, competitors, and regulators.

Headline: GoHealth files for Chapter 11 to strengthen its position ahead of AEP 2026

GoHealth has filed a prepackaged Chapter 11 bankruptcy to reduce debt and strengthen its finances. The restructuring has strong backing from lenders and major stakeholders, allowing the company to continue normal operations, pay vendors, and maintain customer and payer relationships while emerging with a healthier balance sheet and lender-led ownership structure. The company expects to continue normal operations throughout the process, pay vendors in full, preserve relationships with health plans and consumers, and emerge from bankruptcy before the critical Medicare enrollment season begins.

Why it matters: While the announcement is framed as a restructuring, it is really the culmination of Medicare Advantage pressures. GoHealth has faced declining revenues, significant debt obligations, higher interest costs, and a challenging MA market with health plans increasingly focused on profitability, member retention, and tighter distribution economics.

The CFO Takeaway: This headline is ultimately unsurprising in today’s market. GoHealth’s restructuring shows how quickly leverage that seemed manageable during periods of growth can become a strategic constraint when industry economics shift.

GoHealth’s restructuring may ultimately be successful, but it highlights that healthcare organizations are increasingly being judged not just on revenue growth, but on their ability to generate sustainable cash flow and withstand prolonged reimbursement pressure. CFOs, is that shift influencing capital allocation decisions today?

Hospitals reduced expenses and improved throughput in March, but rising uncompensated care and worsening payer mix are limiting margins, Kaufman Hall’s latest data reveals.

KEY TAKEAWAYS

Hospital margins improved in March, but year-to-date performance remains below 2025 levels despite operational gains.

Expenses declined month-to-month, potentially signaling short-term stabilization, though drug and supply costs are significantly higher year-over-year.

Health systems are being pushed toward targeted resource allocation and outpatient-focused service-line strategies.

Hospitals are showing signs of stronger operational discipline in early 2026, but those gains have yet to translate into meaningful financial growth.

While margins improved modestly and expenses dipped slightly month-to-month in March, hospitals continue to face persistent pressures like an eroding payor mix and a rise in uncompensated care that are offsetting operational progress, according to Kaufman Hall’s latest National Hospital Flash Report.

The average monthly operating margin, inclusive of health system allocations for the cost of shared services, increased from 1.8% in February to 2.9% in March. That jump pushed the adjusted year-to-date operating margins to 1.7%, up from 1.3% in February. However, Kaufman Hall’s data shows hospitals are well below 2025 levels overall, highlighting that recent gains have not been enough to reverse financial headwinds.

Expenses declined across the board on a month-to-month basis, suggesting some short-term stabilization after earlier increases. Decreases were seen in total daily expenses (4%), daily labor expenses (2%), daily non-labor expenses (5%), daily supply expenses (1%), daily drug expenses (1%), and daily purchased service expenses (8%).

Still, costs remain elevated on a yearly basis, particularly related to drugs (10%) and supplies (11%). Even with the March dip, expense relief has been uneven and not yet sustained enough to materially improve margins.

At the same time, hospitals continue to demonstrate incremental operational improvements. The report found a 2% reduction in average length of stay month-over-month and a 3% drop year-over-year. Meanwhile, daily outpatient revenue stayed flat in March but rose 12% year-over-year, indicating efforts to improve throughput and shift care to lower-cost settings. Adjusted discharges increased 4% year-over-year in March, and equivalent patient days per calendar day fell 3% month-over-month and 2% year-over-year, pointing to gains in capacity management and patient flow efficiency.

Less encouragingly, hospitals are still contending with higher levels of bad debt and charity care, which jumped 18% year-over-year, reflecting a worsening payer mix and ongoing challenges with government payers relative to commercial reimbursement.

“Hospitals continue to see the effects of payor mix erosion and cost pressures,” Erik Swanson, managing director and data and analytics group leader at Kaufman Hall, said in a statement. “Proactive steps to strategically allocate resources and manage spend, through areas such as length of stay, outpatient care and growing expenses, will continue to be key.”

Regional variation is also a defining feature of the current environment. The Northeast posted margin improvement despite historically weaker financial performance, while hospitals in the West saw the most pronounced increases in drug expenses. Those two outliers showcase the uneven cost and revenue forces across markets.

For hospital leaders, the latest data is further evidence that operational improvement alone is unlikely to fully restore margins right now. Many health systems have already spent the past several years striving to improve efficiency in areas like staffing and throughput, meaning future gains may be harder to achieve through traditional cost-cutting alone.

Instead, executives must prioritize more targeted resource allocation and service-line strategy, especially as hospitals invest more in outpatient settings.

Saad Ehtisham says the nonprofit health system is looking beyond typical ROI benchmarks for determining worthwhile investments in AI and digital tools for operational growth.

KEY TAKEAWAYS

Atlantic Health views innovation as an organizational and cultural transformation effort rather than simply a technology initiative.

The system’s AI investments are focused on reducing friction across care delivery, including clinician documentation burden and patient scheduling delays.

CEO Saad Ehtisham sees workforce resilience and consumer access as long-term strategic returns, alongside traditional financial performance metrics.

For many health systems, innovation has become shorthand for digital expansion and AI deployment designed to create a return on investment. At Atlantic Health, president and CEO Saad Ehtisham frames that approach in another way.

“We’re looking at innovation much differently than most systems are and not as a tool, but as a cultural shift,” Ehtisham told HealthLeaders.

That philosophy is driving the New Jersey-based health system’s use of technology to improve workflows for clinicians while simplifying access for patients.

Investment, according to Ehtisham, is flowing into ambient listening tools, workflow automation, digital scheduling capabilities, and AI applications aimed at reducing friction across care delivery.

A Happier Workforce is a Better Workforce

One of Atlantic Health’s biggest strategic priorities involves workforce sustainability.

The system has emphasized upskilling employees and encouraging leaders to think beyond traditional operational silos, Ehtisham highlighted. The organization wants managers and staff members to develop enterprise-level understanding that allows them to grow internally rather than looking for opportunities outside the system.

“What we want to do is make sure our team members don’t stay in the vertical expertise that they’re framed in, but they have the ability to cross-train into a different vertical and be able to grow in their acumen,” Ehtisham said.

Technology investments have become integral to that workforce strategy.

Atlantic Health recently piloted ambient listening tools that document physician-patient conversations during appointments. While many organizations evaluate those platforms through productivity or revenue gains, Ehtisham is more interested in the impact on clinician experience and long-term sustainability.

“How does that make our clinicians’ and physicians’ lives a lot easier and their flow throughout the day?” Ehtisham said. “Does that reduce their pajama time where they can spend more time with their families instead of having to be in their computers?”

Atlantic Health is also exploring agentic AI capabilities that can respond to certain administrative patient questions through Epic’s MyChart platform. The goal is to reduce after-hours inbox management that contributes to physician burnout.

“It is increasing the resilience of our physicians and that will in turn increase their ability to want to practice longer and want to be with the system,” Ehtisham said. “So that’s our ROI. And I don’t think you can put a dollar value on that. You probably could, you get a mathematician, you can quantify that through some algorithm. I would rather not.”

That same mindset has influenced nursing operations.

Atlantic Health has deployed robots capable of retrieving supplies and handling tasks that frequently pull nurses away from bedside care, Ehtisham noted.

“Twenty-five percent of the time our nursing or any nurse in any health system is spending is non-patient facing,” he said.

By supplementing those activities through automation, the system can allow its team members to focus on taking care of the patient and performing at the top of their license.

As Ehtisham puts it, staff are more likely to produce 150% output if they’re working at 90% of their capability from a resource intensity standpoint, and happier in what they do.

Pictured: Saad Ehtisham, president and CEO, Atlantic Health.

Opening the Digital Front Door Wider

Atlantic Health’s innovation strategy extends into consumer access.

One of the earliest operational changes implemented under Ehtisham involved measuring the next available appointment within 30 days across clinics and reducing delays that prevented patients from getting timely care.

“That was one operational lever we pulled early on,” he said.

According to Ehtisham, improving appointment access generated gains in consumer experience while contributing to stronger financial performance.

“We’re beginning to see it from consumer experience,” he said. “They’re much happier being able to get in when they want to be seen.”

The system is now experimenting with on-demand self-scheduling capabilities designed to better connect patients with its ambulatory infrastructure.

Atlantic Health continues to expand outpatient locations anchored around primary care as well. Many of those sites include rotating specialty services, imaging, laboratory capabilities, and physical therapy offerings intended to create centralized outpatient destinations.

The organization’s digital ambitions also include patient-facing AI applications.

Ehtisham said Atlantic Health is looking at developing its own version of Claude or ChatGPT, capable of guiding consumers toward the appropriate level of care based on conversations occurring through the platform. He envisions systems eventually using those interactions to direct patients toward physician appointments or virtual visits while simultaneously transferring relevant information into the clinical workflow before the encounter begins.

“We know consumers are going on those platforms and typing in, ‘I have this, what should I be?’” Ehtisham said. “That’s a platform that’s being engineered by non-healthcare providers systems. We’d rather get into that technology.”

Keeping Financial Discipline in Focus

Even as Atlantic Health expands technology investments, Ehtisham acknowledged the tension many health systems face when balancing the pursuit of innovation with financial realities.

“Healthcare is the only place where you bring in technology, the cost goes up versus going down,” he said. “We’re trying to invert that thinking.”

That influences how Atlantic Health approaches vendor relationships and operational deployment. Ehtisham said the system prefers working more deeply with select partners capable of improving workflows end-to-end, rather than as a one-off.

He pointed to operational throughput as one example. The organization is evaluating how technology can reduce bottlenecks beginning in the emergency department and continuing through inpatient discharge processes. Smoother patient flow can improve experience while generating financial yield through shorter lengths of stay, Ehtisham stressed.

“It starts creating this pipeline of revenue streams and future predicted models that’s going to be coming through market share that you’re going to be gaining over time,” he said. “It doesn’t happen overnight. But you have to commit to what you’re trying to do.”

Innovation can’t happen without resourcing though, which is why Atlantic Health has dedicated annual capital dollars specifically toward technology investments tied to operational improvements.

“It’s more of a derivative,” Ehtisham said. “You’ve got to generate so much operating margin in order to invest in that,” creating a direct link between financial discipline and innovation capacity.

As financial challenges persist and clinical labor remains difficult to replace, many hospitals are turning to restructuring for cost savings.

KEY TAKEAWAYS

Care New England, Washington Regional Medical System, and Intermountain Health all announced layoffs that prominently affected administrative functions.

Hospitals are increasingly embracing “The Great Flattening,” consolidating nonclinical roles to reduce overhead while preserving frontline care capacity.

While leaner organizational structures may improve efficiency and speed decision-making, reducing leadership layers can also create operational strain and place added burden on remaining staff.

Three notable health systems announced layoffs in recent days, and in all three cases, management and leadership roles were largely affected. Even as labor costs continue to climb, clinical talent remains scarce, making administrative jobs often the primary target of workforce reductions.

Healthcare, and hospitals specifically, are not immune to “The Great Flattening” impacting corporate America. Companies across industries have spent recent years trimming down middle management, if not outright eliminating those positions, for the purpose of creating leaner workforce structures and cutting overhead.

In the case of hospitals, many have taken the step to consolidate functions that aren’t directly tied to delivering patient care.

The trend became particularly visible over the past week with Care New England, Washington Regional Medical System, and Intermountain Health all initiating reductions.

Providence, Rhode Island-based Care New England eliminated more than 30 leadership and nonclinical positions as part of a restructuring to address financial pressures and help close an estimated $20 million budget gap for fiscal year 2026. System president and CEO Michael Wagner said in a statement that “current financial conditions have made additional cost-saving measures unavoidable.”

Elsewhere, Washington Regional Medical System announced a restructuring plan that included 86 job cuts through consolidation of management and support functions. “By restructuring our management operations and consolidating roles, Washington Regional will reduce redundancies and optimize efficiency while still providing the high-quality care our community has come to expect,” Lucas Campbell, president and CEO of Washington Regional, said in the announcement.

At Intermountain Health, the 93 positions that were eliminated amid clinic closures and operational changes in Colorado and Montana looked a little different. While clinical roles were affected as part of the restructuring, the organization also pointed to leadership and administrative consolidation to improve efficiency and better align resources.

Though the circumstances surrounding the three systems differed, the overlap across the layoffs was the emphasis on leadership restructuring and administrative streamlining.

The logic behind these restructurings is straightforward: clinical workers are difficult to replace, whereas administrative costs often represent one of the few areas where organizations can still reduce spending relatively quickly.

According to Kaufman Hall’s latest National Hospital Flash Report for March, hospitals are operating more efficiently, but financial performance is still being weighed down by rising expenses. Length of stay, for example, was down 3% year-over-year, indicative of improved throughput. However, that clinical efficiency requires adequate staffing, and that labor is costly, as seen in a 4% rise in labor expense per calendar day year-over-year.

To just maintain their thin margins, hospitals are being forced to cut costs in areas that won’t directly hinder patient flow. That’s why administrative restructuring is often viewed as a less disruptive path toward reducing overhead while sustaining operational efficiency.

The result can also be a faster decision-making structure, allowing organizations to be strategically nimbler during a time when moving slow can leave hospitals behind the curve.

Still, the benefits come at a price. The loss of leadership and management may not be felt in financial performance immediately, but over time, it can create operational strain and place additional burden on remaining leaders and frontline staff.

For hospital executives, the question they must answer is how far their organization can streamline before efficiency gains start to create new organizational pressures.

The diagnosis is simple: “Our health-care system broke in 2020,” says Dr Tom Dolphin, an anaesthetist in London and boss of the British Medical Association. “We like to pretend it didn’t, but it really did.” In the early months of 2020, hospitals paused normal activity to free up beds as they braced for a wave of covid-19 patients. The strategy helped in a moment of crisis. But, several years on, it is becoming clear that those measures did lasting damage to health-care systems. Understanding why is less straightforward.

From admission to discharge, hospital care is now harder to access, takes longer and is of worse quality. The resulting toll includes avoidable deaths. Almost everyone is affected: across 18 rich democracies, satisfaction with health-care quality fell sharply after the pandemic and remains well below the pre-pandemic norm (see chart). Few data sets track hospital performance across countries, so The Economist collected data on health-care systems from all over the world to identify where things are going awry.

Chart: The Economist

The ordeal begins outside the emergency room, or the accident-and-emergency department (A&E).Waiting times have become longer in America, Europe and elsewhere. Hospital entry halls are more crowded and their staff more overstretched than they were before the pandemic, says Dr Alex Janke, an emergency physician at the University of Michigan.

In some parts of Australia almost half of patients arriving by ambulance wait more than 30 minutes outside A&E before space can be found for them. About a quarter of patients experience such delays in Britain, double the level in 2019. In Canada a record number of sick and injured simply give up and leave emergency rooms before they are seen by staff.

Once in A&E, care is slow. More than a quarter of patients in England spend over four hours there, roughly twice the level in 2019. In Massachusetts, a state with good data, more than two in five endure such waits. In Australia, nearly half of patients do so. There has also been a steep rise in “trolley waits”, the time between a doctor’s decision to admit a patient from A&E to the hospital and when a patient gets a bed. Last year nearly one in ten emergency admissions in England, or some 550,000 people, had waited more than 12 hours on a trolley—a 67-fold increase since 2019.

The real trolley problem

The Royal College of Emergency Medicine estimates that trolley waits contributed to almost 5,000 avoidable deaths in Britain’s hospitals last summer (health authorities have disputed such figures in the past).

Millions are stuck on waiting lists. Waits for hip replacements, to take one example, were above pre-pandemic levels in 2024 in nine out of 11 OECD countries, for which data exist. Canada is perhaps the worst hit. The median waiting time for specialist treatment was 29 weeks in 2025, more than a third higher than the 2019 baseline, according to the Fraser Institute, a think-tank in Vancouver. That is the second-worst result since the survey began in 1993; the record of 30 weeks was set in 2024. France’s main hospital union says access to health care in the country is undergoing an “unprecedented deterioration”.

In many countries the challenges of hospitals are viewed as the product of domestic policy choices. Britain’s government, like Giorgia Meloni’s in Italy, was elected in part on a promise to reduce waiting lists; Australian voters have punished politicians for ambulances delayed outside A&E; and in France, where staffing shortages have forced the closure of some clinics, there is talk of déserts médicaux.

But the long-term effects of the pandemic on hospitals are consistent across countries. A paper published in January by Luigi Siciliani of the University of York and his co-authors finds no relationship between a health-care system’s characteristics, be it public or private, and the effect of covid on its function. How much funding a system had, its bed capacity and how many physicians it employed, had little to no relation with big jumps in waiting lists for elective surgeries between 2020 and 2023, which occurred across the board.

Hospitals are jammed up despite being well-resourced. Funding for health care is the highest it has ever been, outside covid. After stabilising in the 2010s, spending in the OECD rose to nearly 10% of GDP following the pandemic. Median spending per person in Europe has risen 13% in constant prices since 2019. There are also more helping hands. Hospitals added nearly 140,000 jobs in America last year, more than the entire rest of the economy. Hiring by England’s National Health Service has increased sharply: its headcount has grown by 25% since 2019 to employ some 1.4m people—or 2% of the population.

All this presents a productivity puzzle. Some hospitals seem to be faring worse with more resources. In Australia, where the hospital workforce grew by almost 20% from 2019-24, elective surgeries are basically flat—the only difference is that the sick are waiting longer to be seen. Though there has been a gradual recovery, “On any measure you want to use in England, productivity is below where it was pre-pandemic,” says Max Warner of the Institute for Fiscal Studies, a think-tank in London.

Hospital productivity is hard to measure, but a good rule of thumb for spotting any decline in productivity is when spending grows faster than output, or revenue. Even in Germany, where the public system is considered to be in good shape, three out of four hospitals lost money in 2024, up from a third in 2019, according to a recent report by Roland Berger, a consultancy. In America operating costs for hospitals increased by 7.5% in 2025, about twice as fast as prices, says Aaron Wesolowski of the American Hospital Association, an industry body. Accordingly operating-profit margins have stagnated since 2019, even as profits in the rest of America’s economy recovered and grew.

Experts differ on the reasons why hospitals, as big, complex systems, have never fully recovered. One explanation lies in the hospital workforce. About half of the growth last year in the operating expenses of American hospitals came from inputs such as labour costs, which grew by 5.6% in nominal terms. Pandemic-era stresses increased churn as doctors and nurses resigned, or retired early. Those who stayed have reduced their “discretionary effort”, voluntary overtime work that helped frail health-care systems surge in peak periods. Burnout remains high, says Dr Margot Burnell of the Canadian Medical Association.

Is there a manager in the house?

Both factors have created an acute need for staff, and spurred a big hiring drive. The knock-on effect is that health-care workers today are less experienced and perhaps less productive. In Britain the share of nurses with less than one year of experience has doubled since 2015, a trend explained also by efforts to improve nurse-to-patient ratios. Moreover, though doctors and nurses have been added quickly, in some countries hiring for other jobs vital to productivity, such as theatre assistants and hospital managers, has not kept pace.

The other half of rapidly rising costs comes from having more, and sicker, patients. Four factors apply across rich countries: longer waits have left patients sicker, sicker patients take longer to treat, longer treatments clog capacity, reduced capacity creates longer waits. It is a doom loop.

First, in many places the queue has never been longer. Across the OECD, a group of mostly rich countries, elective-surgery activity dipped in 2020 by 19%. This has left hospitals with a long to-do list on top of their ordinary flow of new patients. More than 3m missed hospital stays accumulated in France between 2019 and 2024, according to estimates by the country’s health-care unions. In January nearly 40% of those waiting for treatment in Britain—or 2.8m people—had been languishing for more than 18 weeks. That was up from 570,000 in the same month of 2019. Mr Siciliani says that in order to cut those lists, hospitals need not only to return to their pre-pandemic productivity, but also to “support a big surge in activity”.

That task is made harder by a second big change: patients are sicker now. Long waits for treatment have made patients’ conditions more complex. Some diseases, such as cancers, stayed undiagnosed for longer because people avoided hospitals and clinics during the pandemic. (In America this effect was compounded by a rising avoidance of treatment due to expense.) In addition, populations are older than they were a few years ago. All this has seen chronic conditions, such as heart disease, cancer and liver disease rise as a share of hospital workloads. Death rates, not adjusted for age, are higher than before the pandemic. “Patients are staying longer and cost more to treat,” says Dr Richard Leuchter, an acute-medicine specialist at the University of California, Los Angeles.

Patients who stay longer take up precious bed capacity. Bed occupancy is further inflated by poorly performing general-practitioner services and chock-full care homes for the elderly, both of which funnel a growing number of sick and infirm into hospitals. Research by Dr Leuchter shows that prior to the pandemic about 64% of American hospital beds were occupied at any given time; during the pandemic that figure shot up to and remained at 75%. In some states, the average is as high as 88% (85% is considered “safe”).

American hospitals look positively capacious next to public systems, which run much leaner. In Ireland more than 94% of beds were occupied in 2019; that went up to 96% in 2025. In Britain beds are often 90% occupied and delays in discharging patients have grown. That worsens the initial problem, delays at the A&E door.

Hospitals are trying to break free from the cycle. Many are demanding more money and staff. A few are trying novel approaches to make room for the sickest patients. Some American hospitals, such as Dr Leuchter’s, are trying “avoidance” strategies that refer stable A&E patients to clinics without overnight beds. Many countries are trying types of “community care” in which treatment occurs outside hospitals, sometimes in patients’ homes. In ageing societies, it was inevitable that hospital care would change: there would be relatively fewer nails in thumbs, and relatively more chronically ill. The pandemic simply made people sicker, sooner.

A wave of coordinated lawsuits is transforming the No Surprises Act’s arbitration system into a battlefield where insurers seek to intimidate physicians, rewrite the law and consolidate control.

As I have written, Congress passed the No Surprises Act (NSA) to safeguard patients from unforeseen medical expenses and establish a neutral, independent dispute resolution (IDR) process for payment conflicts between insurers and out-of-network providers. That design was meant to replace brinkmanship with an independent referee. What Congress designed as a neutral arbitration system is now being challenged by Big Insurance through coordinated litigation designed to narrow, intimidate, and ultimately reshape the law.

Major insurance conglomerates — including UnitedHealthcare entities, Elevance/Anthem affiliates and Blue Cross Blue Shield plans — have launched a coordinated series of federal lawsuits against providers, hospitals, and revenue-cycle vendors who have used IDR at scale. Employing nearly identical language, legal arguments, and allegations, these lawsuits are not isolated ordinary litigation. It is lawfare.

Narratively, these suits recast lawful engagement in the NSA’s IDR process as “abuse,” but functionally they are designed to intimidate physicians from seeking NSA protection. A Pennsylvania suit from UnitedHealthcare against NorthStar Anesthesia presents the most urgent and perilous threat to independent physicians. If Unitedhealthcare prevails, insurers will be able to obtain judgments of fraud against physicians who incorrectly file NSA disputes. The effects of this will be catastrophic for independent physician practices, who cannot afford to litigate against billion dollar behemoths that have armies of lawyers on staff and retainer.

If successful in these efforts, the insurers will further weaken physician practices and make them ripe for acquisitions, continuing the dangerous path of vertically integrated insurance corporations – and the further decimation of independent physician practices.

The “Flooding” Myth

The lawsuits all start in a similar fashion. Each one claims that the defendant “abused” federal legislation “designed to protect patients from unexpected medical bills” and asserts that “the IDR process has not functioned as intended.” This wording appears verbatim in cases filed months apart, across different jurisdictions, against completely different defendants. Insurers adopt the same basic allegation: providers or billing companies “flooded,” “overwhelmed,” or unleashed an “avalanche” of IDR disputes that insurers assert were ineligible.

Those characterizations are based on bad data. Before the NSA went into effect, the Departments of Health and Human Services, Labor, and Treasury projected that the independent dispute resolution (IDR) process would see roughly 17,000 disputes annually. In reality, the system received nearly hundreds of thousands of disputes in its first year. That mismatch didn’t happen by accident. The departments based their projections on New York’s experience with a state arbitration system, scaling the state’s dispute numbers nationally. But New York’s law relied on an independent benchmark called FAIR Health that sharply reduced disputes. This is a structural feature the federal law does not have.

A more realistic comparison was available at the time: Texas. Unlike New York, Texas operated an arbitration system without an external benchmark making it a better comparison for the federal No Surprises Act. In its first year, the Texas system received nearly 49,000 arbitration requests for a population of just under six million people. That experience should have been a clear signal that arbitration volume would be far higher than federal projections suggested. Insurers have used this modeling error to their rhetorical advantage in their litigation.

Last week, the war in Iran intensified and Kristi Noem’s tenure as DHS Secretary came to an unceremonious close. Perhaps lost in the noise was the February jobs report issued Friday by the U.S. Bureau of Labor Statistics. It showed a surprising decline in job growth prompting speculation the economy might have taken a downward turn. Some headlines….

Payrolls unexpectedly fell by 92,000 in February; unemployment rate rises to 4.4% (CNBC)

Employers Cut Jobs in Sign of a Shakier Economy (New York Times)

Paychecks keep rising for American workers, providing boost to household budgets (Fox Business):

The U.S. economy lost 92,000 jobs in February, stoking labor market worries (NBC News)

The US economy lost 92,000 jobs in February and the unemployment rate rose to 4.4% (CNN)

Anticipation that the jobs report portends bad news for the economy followed the news cycle all day and through the weekend. And a few, like Axios, went further: “The surprise to many was where the biggest since job growth especially in healthcare and social assistance had buoyed the labor market for 3 years.” Others attributed the decline to hangovers from recent nursing strikes (USC Keck, Kaiser Permanente, MarinHealth) and layoffs by many health systems.

To industry insiders, the BLS jobs report’s capture of declines in healthcare hiring was no surprise. Operating cost reduction has been a strategic imperative in every hospital, long-term care, ancillary and medical group since the pandemic (2020). In tandem, investments in workforce productivity enhancements via technology-enabled workforce redesign and performance-based compensation have elevated human resource management to C-suite status in most organizations. It’s understandable:

Healthcare is capital intense: it needs appropriations from government and in-flows from employers and individual taxpayers to pay its bills. Most of that pays for its labor costs. Today, most Board agenda include updates on labor relations, human resource management issues and workforce adequacy—it’s standard fare. And all weigh options to outsource and devour progress reports from HR management on AI-enabled investments anticipated to reduce labor costs.

Healthcare is highly regulated, especially in workforce activities, and labor-management relationships impact organizational performance and reputation. Every sector in healthcare is regulated by combinations of federal, state and local rules, laws and agency directives that define roles, responsibilities, decision-rights and constraints of its workforce. It’s complicated by the politics of healthcare which avoids policy changes that threaten protections sought by each labor cohort in healthcare. Protecting funding and restricting infringement on scope of responsibility by unwanted outsiders is the primary rationale for professional society’ advocacy efforts. In hospital and long-term care settings, the healthcare workforce is a cast-system that keeps doctors at the top of the pyramid, licensed mid-levels in the middle and everyone else below. In other healthcare settings, executive-level designations dominate hierarchies, and in some Boards play roles in workforce structure and compensation schemes. Workforce modernization in most healthcare settings is acknowledged as a critical need but most default to layoffs and fail to enact a comprehensive strategy.

Looking ahead, technology will alter the status quo for workforce modernization efforts in healthcare:

1-Less dependence on physician recommendations. Might patients access customized clinical decision support tools more widely in the future and make more choices themselves (especially if incentives support self-care)? Might other sources of clinical counsel be more accurate, more accessible and less costly in the future, prompting acceptance (trust and confidence) by patients? Physicians and other caregivers will play key roles, but in concert with tools and processes that enable consumer engagement.

2-More access to verifiable cost, price and value information. The underlying costs and prices for healthcare services are unknown to their caregivers at the points of care so the majority of transactions require pre-authorization by a third-party adjudicator with payments that follow. Physicians bear no responsibility for advising patients about costs and prices: theirs is exclusively the domain of clinical counsel. Thus, labor costs in healthcare presume third party payments, middlemen, incapable self-care and work rules that reinforce old ways and torpedo better ways of work. Might the role and scope of insurer activity be integrated with delivery so that “costs and quality” are directly accountable to providers? Might primary and preventive health hubs (physical + behavioral + nutrition + prophylactic dentistry + self-care enablement + insurance) become the centerpieces of community health replacing traditional insurers and hospitals? Where will the workforce choose to work?

Per the Healthcare Workforce Coalition (www.healthcareworkforce.org), healthcare workforce shortages are a near and present danger to the U.S. health system: shortages of physicians, nurses and allied health professionals are significant, especially in rural areas. The 18-million who constitute the healthcare workforce today are being told to work harder with less. It’s no secret.

In the Affordable Care Act (2010), Title 5 (Section 5101), healthcare workforce modernization was authorized: “The purpose of this title is to improve access to and the delivery of health care services for all individuals…” Subtitle B authorized creation of a 15-member National Health Care Workforce Commission to recommend modernization policies. It would have coordinated workforce initiatives across federal agencies (HRSA, CMS, MedPAC, MACPAC, GAO, et al) along with states and private sector operators to address long-term issues and short-term execution challenges. The Commission never met because its funding was not authorized by Congress.

If the overall economy is dependent on healthcare to produce an appropriate share of job growth while reducing overall costs, modernizing its workforce is key. It must include unpaid caregivers, licensed and unlicensed providers and technology-enabled solution providers—not just traditional licensed professional groups and their academic partners. That’s not going to happen in the current political environment where each sector’s primary focus is protecting reimbursement and guarding against scope of practice threats.

The health system needs transformation. Workforce modernization is where to start.

Paul

P.S. My journey as a heart patient continues to teach me just how far we have to go as a “system.” Understanding what I have been billed for, by whom, when and why is like reading Russian. As best I can see, $267,490.30 has been charged by the hospital and 13 different doctors who’ve treated me in some way. How much I end up spending after rehab et al remains a mystery but it’s not remotely close to the hospital’s “price estimator” tool. Little wonder consumers are frustrated about healthcare costs pushing its affordability to the top of their Campaign 2026 concerns.