GOP leaders cited data from a Trump-aligned think tank to argue the ACA is “unaffordable”. Health economists say the numbers were spun and the full story tells the opposite.

In December, when Capitol Hill was consumed by a debate over whether to extend the subsidies that had held down premiums for individual health insurance under the Affordable Care Act since the COVID-19 crisis, Senate Majority Leader John Thune took to the floor to make his case against any extension.

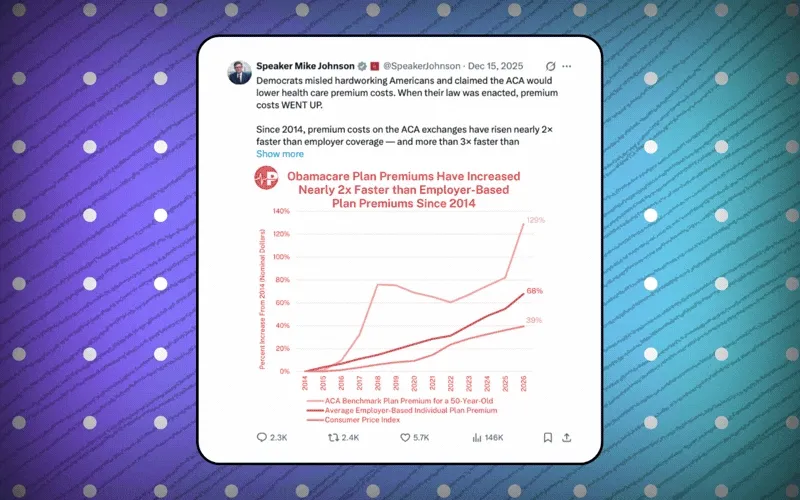

“Obamacare has utterly failed to control health care costs,” argued the South Dakota Republican, who also claimed the government-backed health plan is riddled with what he called “waste, fraud and abuse.” As Thune spoke, he stood before a supersized chart that he said clinched the case for ending the subsidies.

“This graph illustrates that, and it understates the problem,” the GOP leader said, pointing to the chart where a red line symbolizing the costs of ACA insurance jutted skyward. It made a case that since 2014 the premiums for Obamacare coverage have not just outstripped inflation but have increased more than double the rate of employer-based health plans.

In the days that followed, Thune’s GOP caucus held the line and successfully resisted a Democratic push to save the subsidies, even as many of their constituents were getting notices in the mail that their ACA-plan premiums for 2026 would increase sharply – doubling, or more, in some cases.

But some health care experts who looked at the large chart that was so central to Thune’s argument said they could not disagree more with the senator’s claim of an Obamacare affordability crisis. They note that while there was indeed a spike in ACA premium costs in 2017 and 2018 – largely the result of political decisions made by Thune’s fellow Republicans – in the years from 2019 through 2025 the ACA increases were actually lower than in employer-based insurance.

“This is being used as evidence that the individual market is, in some way, particularly inefficient – and I just don’t think there’s any reason for that,” said Matthew Fiedler, senior fellow at the Center for Health Policy at the Brookings Institute. He added: “There has been research that has compared individual-market to employer-market premiums. And what it actually finds is that individual-market premiums” – those offered under ACA – “seem to be a little bit lower than employer-market premiums.”

Thune wasn’t the only top Republican who offered the questionable statistics as a central argument for ending the Obamacare subsidies. House Speaker Mike Johnson tweeted out the same chart on the social-media site X on Dec. 15, lashing out at what he dubbed “the Unaffordable Care Act.”

But where did top Republicans get their arguably misleading information? The answer can be found in the small logo at the top of the controversial chart – that of a small and, until recently, fairly obscure Trump-aligned policy think tank called the Paragon Health Institute. It is led by Brian Blase, who was a member of Trump’s National Economic Council during the president’s first term.

Just a few years old, Paragon under Blase has positioned itself as the leading voice for a Trump-led health care overhaul that has promoted the belief that ACA-supported health insurance is both riddled with fraud and wildly inefficient for taxpayers. And its latest chart on ACA costs isn’t the first time Paragon has been accused of pushing misleading statistics to make its case.

In August, Blase and Paragon claimed that Obamacare is overrun with “phantom enrollees” – insisting that millions of ACA enrollees who’d filed no insurance claims was evidence that unscrupulous brokers had profited by signing up people without their knowledge. But Paragon’s report, which also was cited repeatedly by Republicans seeking to block the extended subsidies, was blasted by groups such as the American Hospital Association.

An AHA vice president, Aaron Wesolowski, wrote in a blog post “that Paragon developed these allegations using inaccurate data, dubious assumptions, and an apparent lack of understanding of how health insurance actually works.” He and other experts explained that while there was a real problem with 200,000 of the more than 25 million people who had signed up for coverage in the ACA marketplace, the vast number of zero-claims patients were not “phantoms” but young people who didn’t see a doctor, people who were only in Obamacare plans for months before getting a new job, or plan-switchers who were double-counted.

The story of Paragon is the health care version of a much bigger story that anyone who’s followed American politics over the last decade will recognize: How misinformation and distortions are amplified in a media and social media ecosystem.

Andrew Sprung, a health care writer who picked apart the Paragon chart on ACA costs in his Substack newsletter, said this type of propaganda “goes straight onto Fox News and into the mouth of Trump allies who deter the Republicans from cutting a deal” that might save the Obamacare subsidies and thus make health coverage more affordable for middle-class families, including their own constituents.

To Sprung and other health watchdogs, the statistical jiu-jitsu that Paragon performed in its analysis of ACA premiums versus employer-based plans is typical of how it helps ultra-conservatives win the PR wars against publicly supported health care in America. The spin helps leaders like Thune and Johnson keep their more moderate members in line.

In fact, Thune, again citing Paragon statistics, noted in his Senate floor speech that if you extend the chart back to 2013, Obamacare premiums appear to have risen some 221% – before he quickly acknowledged that this number is skewed by the difficulties insurers faced in setting rates in the first year of open enrollment.

But health care analysts note that other factors – most of them tied to Republican hostility toward any type of public health care – fundamentally undercut the argument from Paragon and its allies on Capitol Hill that Obamacare is a failure because inflation is baked into the program.

In a post headlined “Lies, damned lies, statistics, and Republican talking points about the ACA,” Sprung notes that the first spike in ACA premiums occurred in 2017 because a three-year, federally funded reinsurance program included in the original 2010 law had expired and insurers recalculated their costs based on a risk pool that was older and sicker than anticipated. As a result, premiums in the benchmark Silver plans under the ACA rose that year by 20%.

But that didn’t end the turmoil for Obamacare, because when Trump took office in 2017 and – with Blase in the White House as a policy adviser – Republicans pushed hard to repeal the ACA. That didn’t happen, of course, but the new administration did make changes like shortening the enrollment period and scaling back recruitment and marketing, as well as reducing cost-sharing payments to insurers.

The chaos the changes caused spooked insurers, who raised premiums a second time in 2018, by an average of 34%. But the failure of the ACA repeal effort in the Senate that same year ushered in a period of stability in which – contrary to Paragon’s argument about the inefficiency of Obamacare – ACA premiums actually outperformed health plans offered by employers. Sprung cited government statistics that premiums for individual plans rose from 2018-23 by 13%, compared to 29% for employer plans.

Brookings’ Fiedler agreed. “You’ll see there’s this period where premiums are actually declining in the individual market,” he said, noting that not only did insurers overshoot with the Obamacare premium hikes of the mid-2010s but that the enhanced subsidies that began under COVID-19 brought in younger, healthier enrollees while encouraging increased competition for new customers.

None of the non-fiction narrative around what has really happened in the marketplace since the passage of Obamacare supports the GOP’s core argument that health care backed by the ACA is riddled with “waste, fraud and abuse.” Instead, Paragon looks to be spinning its own storyline that is to the liking of its donors, like the billionaire libertarians of the Koch family, which supported the think tank in 2021 with a $2 million donation from the aligned organization, Stand Together. Groups aligned with Leonard Leo, the former Federalist Society officer who was the architect of the right-wing takeover of the Supreme Court, have also donated.

The failure by Congress to extend the ACA subsidies ahead of their expiration shows that the right’s deceptive spin-doctoring is working, for now.

That zeitgeist may change once the voodoo economics of a misleading line chart is swamped by the tide of horror stories about soaring out-of-pocket costs for regular folks who can no longer afford the care they need.