In second episode of the HEALTH CARE un-covered Show, we walk you through the most recent earnings reports of seven of the largest for-profit health insurance corporations in the country.

Every three months, the nation’s largest health insurers release earnings statements filled with crammed financial tables, investor language and Wall Street jargon. Most people never see them. Even fewer try to understand what they really reveal about how the U.S. health care system works.

In second episode of the HEALTH CARE un-covered Show, we do something no one else does: walk you through the most recent earnings reports of seven of the largest for-profit health insurance corporations in the country — UnitedHealth Group, CVS Health (Aetna), Cigna, Elevance, Humana, Centene and Molina. As you’ll see, the results paint a striking picture of how powerful and profitable Big Insurance has become.

Together, those companies collected nearly $1.7 trillion in revenue in 2025, about $175 billion more than the year before and generated more than $54 billion in profits. Yet despite the record financial performance, the companies covered roughly 10 million fewer people than they did in 2024 – and ever-increasing chunks of their revenues are now coming from Americans’ tax dollars.

We show evidence of a trend reshaping the health care economy: self-dealing through insurers’ vertical integration and their huge government contracts, which accounts for much of the industry’s growth. For example, UnitedHealthcare now gets more than 77% of its revenue from government programs such as Medicare Advantage and Medicaid. As a reminder, Medicare Advantage is not traditional Medicare but a very profitable privatized version of the program that’s funded by taxpayers and that last year overpaid insurers by $84 billion.

We also examine stock buybacks. Between 2015 and 2025,these seven companies spent more than $137 billion buying back their own shares, a move that boosts earnings per share and enriches shareholders and top executives. That’s $137 billion that could have been used to reduce premiums and out-of-pocket expenses but went into the pockets of investors instead.

To put the numbers in perspective, we compare these insurers with some of America’s most recognizable corporations — from Chevron and PepsiCo to Bank of America and Salesforce. Most of the big seven generate more revenue than these household names. And many of the insurance conglomerates are growing faster than companies like Target, Uber, Disney and Starbucks.

We take viewers inside Wendell’s office to make sense of Big Insurance’s dense 2025 earnings reports.

You won’t find an analysis quite like this anywhere else.

This episode has been re-uploaded with corrected numbers. For instance, Disney was listed as having revenues of $274.9B in 2025. The correct number is $94.4B. The percent change used in the original video (+80%) was correct.

In Episode 1 of the HEALTH CARE un-covered Show, we examine what may be an inflection point in the health insurance reform debate. Plus, we’re joined by pollster Madeline Conway of Impact Research.

The volume of claims is treated as proof of misconduct, despite the fact that the statute imposes no limit on IDR submissions and explicitly allows for repeated use when payment disputes continue. Further, insurers base this claim on estimates of IDR submissions that were deeply flawed, forecasting nationwide utilization on the experience of one state.

The message is unmistakable: providers are not accused of breaking the NSA, but rather of utilizing it too effectively. For instance, insurers claim that providers submitted “thousands” of IDR disputes, including nearly “200 overlapping proceedings for the same services” across both the federal and state IDR systems, and batched an average of 66 separate items or services into a single IDR filing: Insurers describe these statistics as “overwhelming,” despite the fact that each dispute is linked to a corresponding payment denial or gross underpayment.

Recasting Physician Disputes as “Fraud”

Each lawsuit hones in on physician NSA disputes and castigates them as some kind of “fraud” or “abuse.” The HaloMD lawsuits are a prime example of the insurer taking an NSA dispute, challenging the disputes eligibility for arbitration and then recasting it as “fraud.” What these lawsuits notably fail to recognize is that the outcomes of IDR are determined by independent arbitrators, called certified IDR entities (IDREs), not by the providers themselves.

According to CMS’s public-use files, 82% of 2024 disputes and 80% of 2025 disputes were found eligible for arbitration. This is orders of magnitude greater than what the government had estimated. What these numbers tell us is that the problem with the volume of disputes is not a conspiracy by doctors to abuse this system, but systemic underpayment by insurers, as we have reported.

In the lawsuits, insurers concede that it was the arbitrators, not the providers, who rendered the final awards in these disputes. Insurers also consistently and publicly voice their concerns that NSA awards surpass the Qualifying Payment Amount (QPA), often describing results that are ‘multiples’ of the median in-network rates or even exceeding billed charges. Insurers assert that IDR awards are excessive, “citing CMS data showing that they are on average slightly over 300% of the QPA” of the QPA.

However, a recent analysis shows that the reported QPAs consistently underestimate the actual median in-network rates, with an average discrepancy of 290% in cases where such discrepancies are present. A pervasive problem reported by providers and evident in the public-use files shows thousands of initial offers for payment that amount to less than a dollar. In one documented case involving high-acuity emergency care, the insurer calculated the QPA at $0.01. The arbitrator ultimately awarded $1,196. The gap was not evidence of an inflated charge; it was evidence that the benchmark itself was flawed.

This underestimation is attributed to calculations controlled by insurers, insufficient oversight, and the omission of market factors that Congress mandated arbitrators to consider.

Simply disagreeing with an IDRE’s assessment does not equate to fraud. Rather than modifying payment practices, enhancing negotiations, or pursuing legislative clarity, insurers have opted for litigation as a tool to crush providers while claiming unfavorable arbitration results as evidence that the system is being “manipulated.” They are both arsonists and firefighters.

The Litigation Boa Constrictor

Across jurisdictions, insurers clearly claim that defendants engaged in “coordinated enterprises,” “strategic partnerships,” or “associations-in-fact,” alleging RICO violations founded on the concurrent use of IDR, common billing vendors, and simultaneous filings, even though there is no statutory restriction against coordinated IDR usage or shared administrative frameworks.

The recurring themes in these filings are hard to overlook. In the last 12 months, there have been 11 lawsuits targeting use of the No Surprises Act, four alleging RICO violations and five seeking treble damages.

So far, this coordinated lawfare effort includes the following suits:

Blue Cross Blue Shield of Texas v. HaloMD et al. (E.D. Tex., Aug. 2025)

Blue Cross Blue Shield of Texas v. Zotec Partners, LLC (E.D. Tex., Dec. 2025)

Anthem Health Plans of Virginia v. AGS Health / SCP Health et al. (W.D. Va., Nov. 2025)

Community Insurance Co. (Anthem Ohio) v. HaloMD et al. (S.D. Ohio, June 2025)

Blue Cross Blue Shield Healthcare Plan of Georgia v. HaloMD et al. (N.D. Ga., May 2025)

Anthem Blue Cross (CA) v. HaloMD et al. (C.D. Cal., July 2025)

Anthem Blue Cross (CA) v. Prime Healthcare entities (C.D. Cal., Jan. 2026)

UnitedHealthcare of Pennsylvania, Inc. v. NorthStar Anesthesia of Pennsylvania, LLC (E.D. Pa., Dec. 2025)

UnitedHealthcare Insurance Co. v. Maui Emergency Care Physicians, LLC (D. Haw., Jan. 2026)

United Healthcare Services, Inc. v. Concord Company of Tennessee, PLLC (W.D. Ky., Jan. 2026)

UnitedHealthcare Ins. Co. v. Radiology Partners, LLC (D. Ariz, Aug. 2025)

These prosecutions follow a distinct pattern of allegations: strategic batching, simultaneous filings, excessive offers, false statements, and an alleged conspiracy to take advantage of IDR. Even when the factual circumstances vary, the narrative remains the same. This consistency indicates not an independent discovery of wrongdoing, but a calculated strategy.

The targets of these lawsuits represent the full spectrum of organizations utilizing the NSA. From revenue cycle management (HaloMD) to large physician staffing organization (SCP) to small physician practice management group (Concord Company), insurers are constricting the entire provider community hoping to alter the NSA through legal outcomes.

Litigation as Press Release

The litigation involving Prime Healthcare highlights this strategy particularly well. In this case, insurers openly admit that hospitals are utilizing IDR instead of balance billing patients, precisely what Congress intended, yet they still label this behavior as abusive because it led to payments that were higher than what insurers were prepared to offer. Lawful reliance on IDR is recast in this complaint as “extractive,” “indiscriminate,” or “profitable abuse,” as if the issue lies not with insurer underpayment but with the presence of an independent referee who has the authority to disagree with them.

The impact on the real world is far from just a theory. These lawsuits aim for treble damages, annulment of arbitration awards, and injunctions intended to completely deny providers future access to IDR. The message from insurers is clear: engage in the IDR process established by Congress, and you will face consequences. Providers who utilize IDR are not seen as legitimate participants in a federal program; instead, they are viewed as targets, labeled as racketeers, pulled into costly litigation, and compelled to defend their right to contest underpayment. These lawsuits serve as a deterrent and act as a warning to discourage providers from engaging in IDR by making the costs of participation excessively burdensome.

Breaking the NSA Balance

No lawsuit will have more far reaching consequences for physicians than UnitedHealthcare v NorthStar Anesthesia (the insurer has filed five similar lawsuits). While this suit follows the usual script of allegations it aims for something more pernicious than unflattering headlines: declaratory judgment of fraud for ineligible disputes. The eligibility of an NSA dispute rests solely with CMS and the independent arbitrator – they are administrative. Physicians have repeatedly shown that insurers withhold critical information needed to determine a claim’s eligibility, the result being that occasionally physicians will dispute a claim that is ineligible for arbitration. According to CMS, with more than 80% of claims sent to arbitration being determined as eligible, these mistakes are the exception, not the rule.

However, if UnitedHealthcare is granted the relief it seeks, insurers will be able to challenge dispute eligibility in court, outside of arbitration, and receive direct judgments of “fraud” against physicians who have filed ineligible claims. A declaratory judgment of fraud would not simply reverse a payment. It would create precedent allowing insurers to relitigate administrative eligibility decisions in federal court and seek damages for disputes that arbitrators have already accepted into the federal process. This elevates an administrative error into reputational and legal risk that no physician practice could withstand.

The NSA’s public policy goal of removing patients from billing disputes, was buttressed by leveling the playing field between physician practices and insurance behemoths. The sweeping effects of this case will fundamentally alter the scales in favor of insurers and not just chill, but shut out doctors from obtaining fair reimbursement.

Shifting the balance of power

This situation should alarm policymakers as well as doctors and their patients. It embodies the risk of extended, multi-faceted litigation initiated by trillion-dollar insurance conglomerates targeting individual physicians, small practices, and safety-net hospitals that do not possess equivalent resources.

This pressure does not safeguard patients. Instead, it discourages providers from contesting underpayment, shifts the balance of power firmly back to insurers, and dissuades the use of the very system intended to resolve disputes and protect patients. In the meantime, insurers leverage extensive financial resources to maintain coordinated litigation efforts while depicting providers, especially those offering emergency care, as wrongdoers for employing the only legal remedy available.

Ultimately, these legal actions are not aimed at preventing misconduct. Instead, they focus on altering market structure. By transforming the routine application of IDR into a significant litigation risk, insurers are indicating that independent providers who challenge payment terms will face penalties instead of negotiations.

The foreseeable outcome is the consolidation of providers: small practices, emergency physician groups, and safety-net hospitals will be compelled to sell, affiliate, or close rather than endure the costs and uncertainties associated with defending against repeated federal lawsuits. As we’ve reported, Optum now employs more than 90,000 clinicians. Simultaneously, this approach accelerates the vertical integration of insurers, directing care toward entities that are either owned or aligned with insurers, which are shielded from payment disputes and arbitration. Within this context, the courts do not serve as a venue for resolving conflicts; they function as a mechanism for enforcing market discipline. This undermines the fundamental objective of the No Surprises Act to balance bargaining power and, in turn, reinforces insurer dominance over pricing, networks, and access to care.

A law meant to protect patients and equalize bargaining power is being weaponized by insurers to suppress those who question insurer payment practices and, in doing so, to silence the underdog.

New data shows the U.S. is moving backward on coverage, not forward—raising a harder question: is the problem affordability, or priorities?

Will the U.S. ever provide health care for all its citizens?

The prospects are dim for enacting a system that provides services for the county’s entire population the way Europeans have done for decades. As the head of the German pharmaceutical association in Berlin once told me in an interview, “In the German system, nothing comes between us and our principle of solidarity.” I asked, “Even your profits?” “Not even our profits,” he replied.” Imagine any health care executive in the U.S., where the bottom line reigns supreme, daring to say a thing like that.

That interview with the German pharmaceutical executive came to mind again as I read the latest study from the Commonwealth Fund, which should be required reading for anyone interested in health policy and the future of the American system. The report by the Fund’s senior scholar, Sara Collins, said the Trump administration has “made it harder than ever for Americans to get good health insurance,” a conclusion that needs to be shared far and wide.

The administration itself predicts these changes will reduce enrollment in the Affordable Care Act marketplaces next year by 1.2 to 2 million people. The U.S. is falling backward in providing health care for all, a project that prompted Dr. Martin Luther King Jr. to observe long ago, “Of all the forms of inequality, injustice in health care is the most shocking and inhumane.”

At the Commonwealth Fund, Collins noted that those losses are on top of other changes expected to leave another 7.5 million people uninsured. Even though members of Congress hostile to the Affordable Care Act failed to repeal the act during Trump’s first term, Collins points out they still inflicted damage by whittling away at some of the law’s provisions. She reports that last year a majority of the public supported the Affordable Care Act’s enhanced premium tax credits, established in 2021. Republicans, however, did not pass legislation to extend those credits that helped millions of Americans, who now face annual premium increases of $750 to more than $4,000.

Does the destruction of the hard-won Affordable Care Act mean that a country as rich as ours cannot afford to pay for medical care like the rest of the world’s developed countries do, or does it mean those with clout don’t want those without to have health care? I am inclined to believe the latter.

That was not the only damage caused by the Trump administration. For example, a new rule for marketplace coverage increased out-of-pocket costs, eliminated special enrollment periods for those with low incomes, and put new restrictions on auto enrollment. In addition insurers raised premiums by 20% or more in many cases, hoping that those people who are healthy would not drop coverage and leave them with sick, and more costly, health plan enrollees. Such a strategy would be unheard of in countries with national health systems, where everyone is entitled to care.

“The Trump administration’s latest actions on the ACA marketplaces continue to make it as difficult and costly as possible for those with low and moderate incomes to get good health insurance and care they need,” Collins reported. “This will lead to more people with low and moderate incomes uninsured, underinsured, less healthy, and saddled with medical debt.”

Is this what Americans want for their health care system?

Last week, the war in Iran intensified and Kristi Noem’s tenure as DHS Secretary came to an unceremonious close. Perhaps lost in the noise was the February jobs report issued Friday by the U.S. Bureau of Labor Statistics. It showed a surprising decline in job growth prompting speculation the economy might have taken a downward turn. Some headlines….

Payrolls unexpectedly fell by 92,000 in February; unemployment rate rises to 4.4% (CNBC)

Employers Cut Jobs in Sign of a Shakier Economy (New York Times)

Paychecks keep rising for American workers, providing boost to household budgets (Fox Business):

The U.S. economy lost 92,000 jobs in February, stoking labor market worries (NBC News)

The US economy lost 92,000 jobs in February and the unemployment rate rose to 4.4% (CNN)

Anticipation that the jobs report portends bad news for the economy followed the news cycle all day and through the weekend. And a few, like Axios, went further: “The surprise to many was where the biggest since job growth especially in healthcare and social assistance had buoyed the labor market for 3 years.” Others attributed the decline to hangovers from recent nursing strikes (USC Keck, Kaiser Permanente, MarinHealth) and layoffs by many health systems.

To industry insiders, the BLS jobs report’s capture of declines in healthcare hiring was no surprise. Operating cost reduction has been a strategic imperative in every hospital, long-term care, ancillary and medical group since the pandemic (2020). In tandem, investments in workforce productivity enhancements via technology-enabled workforce redesign and performance-based compensation have elevated human resource management to C-suite status in most organizations. It’s understandable:

Healthcare is capital intense: it needs appropriations from government and in-flows from employers and individual taxpayers to pay its bills. Most of that pays for its labor costs. Today, most Board agenda include updates on labor relations, human resource management issues and workforce adequacy—it’s standard fare. And all weigh options to outsource and devour progress reports from HR management on AI-enabled investments anticipated to reduce labor costs.

Healthcare is highly regulated, especially in workforce activities, and labor-management relationships impact organizational performance and reputation. Every sector in healthcare is regulated by combinations of federal, state and local rules, laws and agency directives that define roles, responsibilities, decision-rights and constraints of its workforce. It’s complicated by the politics of healthcare which avoids policy changes that threaten protections sought by each labor cohort in healthcare. Protecting funding and restricting infringement on scope of responsibility by unwanted outsiders is the primary rationale for professional society’ advocacy efforts. In hospital and long-term care settings, the healthcare workforce is a cast-system that keeps doctors at the top of the pyramid, licensed mid-levels in the middle and everyone else below. In other healthcare settings, executive-level designations dominate hierarchies, and in some Boards play roles in workforce structure and compensation schemes. Workforce modernization in most healthcare settings is acknowledged as a critical need but most default to layoffs and fail to enact a comprehensive strategy.

Looking ahead, technology will alter the status quo for workforce modernization efforts in healthcare:

1-Less dependence on physician recommendations. Might patients access customized clinical decision support tools more widely in the future and make more choices themselves (especially if incentives support self-care)? Might other sources of clinical counsel be more accurate, more accessible and less costly in the future, prompting acceptance (trust and confidence) by patients? Physicians and other caregivers will play key roles, but in concert with tools and processes that enable consumer engagement.

2-More access to verifiable cost, price and value information. The underlying costs and prices for healthcare services are unknown to their caregivers at the points of care so the majority of transactions require pre-authorization by a third-party adjudicator with payments that follow. Physicians bear no responsibility for advising patients about costs and prices: theirs is exclusively the domain of clinical counsel. Thus, labor costs in healthcare presume third party payments, middlemen, incapable self-care and work rules that reinforce old ways and torpedo better ways of work. Might the role and scope of insurer activity be integrated with delivery so that “costs and quality” are directly accountable to providers? Might primary and preventive health hubs (physical + behavioral + nutrition + prophylactic dentistry + self-care enablement + insurance) become the centerpieces of community health replacing traditional insurers and hospitals? Where will the workforce choose to work?

Per the Healthcare Workforce Coalition (www.healthcareworkforce.org), healthcare workforce shortages are a near and present danger to the U.S. health system: shortages of physicians, nurses and allied health professionals are significant, especially in rural areas. The 18-million who constitute the healthcare workforce today are being told to work harder with less. It’s no secret.

In the Affordable Care Act (2010), Title 5 (Section 5101), healthcare workforce modernization was authorized: “The purpose of this title is to improve access to and the delivery of health care services for all individuals…” Subtitle B authorized creation of a 15-member National Health Care Workforce Commission to recommend modernization policies. It would have coordinated workforce initiatives across federal agencies (HRSA, CMS, MedPAC, MACPAC, GAO, et al) along with states and private sector operators to address long-term issues and short-term execution challenges. The Commission never met because its funding was not authorized by Congress.

If the overall economy is dependent on healthcare to produce an appropriate share of job growth while reducing overall costs, modernizing its workforce is key. It must include unpaid caregivers, licensed and unlicensed providers and technology-enabled solution providers—not just traditional licensed professional groups and their academic partners. That’s not going to happen in the current political environment where each sector’s primary focus is protecting reimbursement and guarding against scope of practice threats.

The health system needs transformation. Workforce modernization is where to start.

Paul

P.S. My journey as a heart patient continues to teach me just how far we have to go as a “system.” Understanding what I have been billed for, by whom, when and why is like reading Russian. As best I can see, $267,490.30 has been charged by the hospital and 13 different doctors who’ve treated me in some way. How much I end up spending after rehab et al remains a mystery but it’s not remotely close to the hospital’s “price estimator” tool. Little wonder consumers are frustrated about healthcare costs pushing its affordability to the top of their Campaign 2026 concerns.

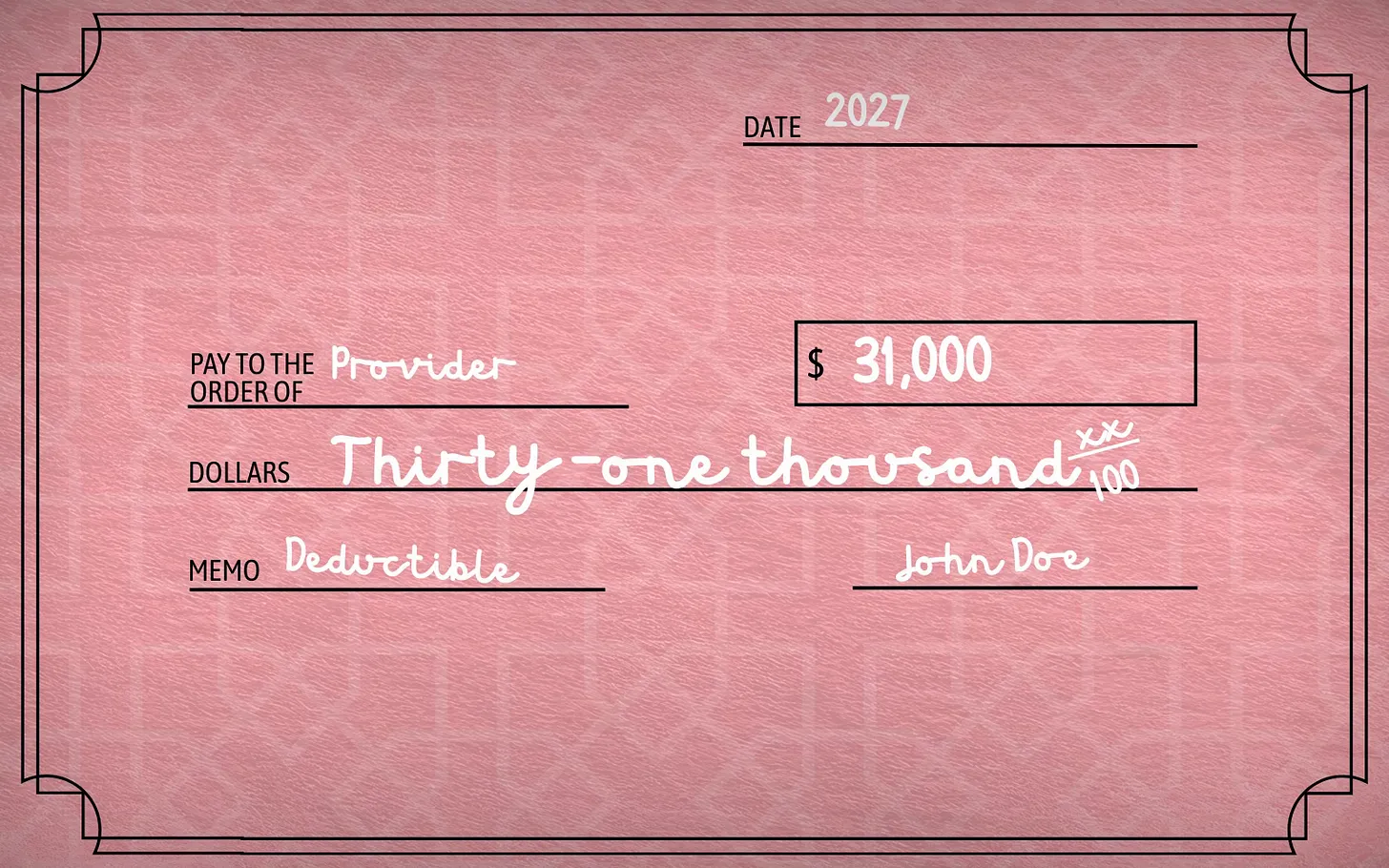

Trump’s proposal would revive “catastrophic” plans with deductibles as high as $31,000 — shifting even more costs onto patients with cancer, chronic illness, and medical emergencies.

On Friday, Erica Bersin – who has two chronic illnesses, including multiple sclerosis – wrote about the challenges of finding a decent and affordable health plan in the ACA marketplace. As a sole proprietor, the only plan with a manageable premium ($330 a month) came with a $10,000 deductible. MS drugs are expensive and many people with the disease have to pay hundreds and sometimes thousands of dollars out of their own pockets before their coverage kicks in. Sadly, the way the ACA plans are structured, Americans with chronic conditions – and others who are diagnosed with cancer or have a heart attack or other acute medical event and have no option for coverage other than the ACA marketplace – are penalized financially far more than the rest of us..

But instead of helping those folks out, the Trump administration is proposing to change the marketplace in ways that will make a $10,000 deductible seem like a bargain. Say hello to a $31,000 family deductible. And even if you’re covered by an employer-sponsored plan and in no imminent danger of being enrolled in a plan like that, know that their reappearance (they were outlawed 16 years ago), will push your premiums even higher than they already are. That’s because hospitals and physician practices know people enrolled in those plans will not be able to pay their bills. They’ll have no option but to increase their prices to cover the additional bad debt.

Health insurance policies with deductibles that high were prevalent before the Affordable Care Act was enacted in 2010. When I was a health insurance executive, I knew some insurers were selling policies with family deductibles north of $50,000. Not only that, many of them had annual and lifetime caps and wouldn’t pay for any care related to a preexisting condition.

They were officially called “catastrophic” plans. Patient and consumer advocates had a more appropriate name for them: junk plans. They were outlawed by the ACA, and I thought they had been buried for good. Unfortunately, the Trump administration is bringing them back to life.

I’m sure my former colleagues in the health insurance business went to work immediately getting those plans ready to sell once again to unsuspecting customers. That’s because they can be very, very profitable. Imagine having to pay $50,000 – or even $31,000 – out of your own pocket every year before your insurer will cover the care your doctor says you need. Cigna, where I worked, as well as Aetna and UnitedHealthcare, the country’s biggest health insurers, sold plans like that and collected billions in premiums every month but paid little if anything out in claims during a given year.

When I first testified before Congress, I was one of three people at the witness table, and all of us knew a lot about those plans – including Nancy Metcalf, who was senior program editor at Consumer Reports at the time. She in particular knew about the many shortcomings of those plans because she had heard horror story after horror story from people who had enrolled in a junk plan. She urged lawmakers to outlaw them – or at least make insurers put warning labels on them so people would know what they were buying and how little protection those plans provided. As Nancy testified:

Consumers need to be told, in big letters, what their policy’s out-of-pocket limit is, and right next to it, in equally big letters, if there are any expenses that don’t count towards that. They need to know approximately what their out-of-pocket costs will be for expensive treatments such as cancer chemotherapy, or heart surgery, or infusions of patented biologic drugs. They need, in other words, a fighting chance not to be ripped off by junk insurance.

As Reed Abelson of The New York Times reported last week, the administration’s proposal “involves a type of plan known as a catastrophic or skinny policy. While they may be appropriate for someone who is young and healthy, a sudden emergency room or unexpected hospital stay could cost thousands of dollars in unforeseen bills. People with chronic medical conditions also might have to pay for much – if not all – of their care out of their own pockets.”

Commonwealth Fund president Joseph Betancourt pointed out in the Times’ story that people are already struggling to pay for their medical care:

There’s no doubt that we have an affordability crisis. As we move forward to shifting more of the burden to patients, there’s a chance to really exacerbate the crisis.

Abelson noted that under the proposed rule change, insurance companies could not only sell the catastrophic plans on a multiyear basis once again, they could also sell plans that do not offer an established network of hospitals and doctors. “Those plans,” she wrote, “would instead pay a fixed amount for a doctor’s visit or procedure, and patients would have to pay any difference in price.”

Abelson also warned of another risk associated with sky-high deductibles: Because their premiums are lower, they “will end up being used as the benchmark for the level of subsidies in a given market. People who want a traditional plan with an established network could end up paying more because they receive a lower subsidy.”

As I mentioned, all of us will likely pay more for our coverage when these plans become legal again next year. As BenefitsPro reported last month – quoting the CEO of Community Health Systems, a big hospital chain – most patients who are currently in ACA plans with lower but still high deductibles and coinsurance requirements can’t pay very much of the “big out-of-pocket bills” hospitals have to send them.

How disappearing ACA subsidies, soaring premiums, and bureaucratic chaos nearly left a consultant with multiple sclerosis uninsured.

The business of health care is not broken; it is working exactly how it was intended. It was designed for people to pay in just in case something happens and then not to pay out when it does. It was intended to “maximize shareholder value.”

About 22 million Americans received enhanced premium subsidies in 2025. According to The Urban Institute and The Commonwealth Fund, it’s estimated that “7.3 million people will leave the ACA marketplace in 2026” due to the loss of the subsidies. About 5 million people will go uninsured, rather than find insurance elsewhere.

Some people have said their premiums and deductibles are doubling or even tripling with tens of thousands in deductibles before coverage kicks in. While absolutely imperfect, we must keep the Affordable Care Act intact for everyone otherwise the cost of Medicare, Medicaid, and private and employer-based insurance will skyrocket, resulting in millions of people losing coverage due to lack of affordability.

Accessible insurance is a huge part of living a healthy life. Because of this, we need to expand coverage and make it fair for everyone. The goal should be for every single person in the U.S. to have head-to-toe health care.

My Story

As a single-person LLC consultant, I have navigated the New York State Exchange (ACA) for years. It is the most expensive Exchange in the country for those who do not qualify for subsidies. If subsidies are received, an increase in income requires repayment via federal tax returns the following year.

For 2025, I resigned myself to a catastrophic plan at $330 per month with a $10,000 deductible, as other options approached $1,000 monthly. While applying in November 2024, my temporarily being in-between projects / contracts was interpreted by the NYS Exchange as being unemployed, which led me to unexpectedly qualify for Medicaid. The state market assured me that this was correct for consultants in my situation, and they “saw it all the time.”

However, during open enrollment in October 2025, I was informed that despite meeting the income threshold, I no longer qualified for either Medicaid or financial assistance / subsidies. The catastrophic plan doesn’t seem to exist now, and the “least expensive” option is $675 with poor / limited coverage. After four months, dozens of phone calls, six people (including an aide in my state assembly member’s office), and about 100 hours of everyone’s time, I have health insurance this year, for now.

Living with two chronic illnesses, including multiple sclerosis, my experience with a “government run” system over the last year has led me to believe that, for the most part, it works. Health care should be a right of birth, not a privilege for the rich.

This is just one person’s story. The rise in health care costs impacts everyone, but especially lower income Americans. You can see some of their fears, here.

The Trump administration is doubling down on efforts to revamp the federal discount drug program — a major flashpoint between Big Pharma and hospitals.

Why it matters:

The so-called 340B program has been mired in litigation, most recently over administration efforts to let drugmakers carry out price reductions through rebates instead of cutting prices at the front end.

After a court halted the attempt on procedural grounds, federal health officials this month laid the groundwork to reintroduce changes that providers say could cost them hundreds of millions of dollars.

Driving the news:

The Health Resources and Services Administration last week issued a notice soliciting feedback on whether and how to make hospitals and clinics in the program pay full price up front for the medications.

Drugmakers would then rebate the price difference later, after verifying that a facility qualifies for a discount.

The agency is asking hospitals for financial data to back up industry claims that such a change would threaten facilities’ cash flows and create administrative hassles as they contend with federal Medicaid cuts.

Context:

A federal court in Maine ruled late last year that the Department of Health and Human Services, which HRSA is part of, didn’t solicit enough stakeholder feedback before proposing its initial rebate model.

HHS “cannot fly the plane before they build it,” Judge Lance Walker wrote in response to a lawsuit from the American Hospital Association and other hospital groups.

HHS scrapped the pilot in January and dropped its appeal of the decision.

The new notice it sent this month “suggests a sense of urgency in advancing a new rebate model proposal,” lawyers at Quarles & Brady wrote in a blog post.

Still, HHS would need to formally propose and gather comment on any future model, and has committed to giving providers at least 90 days’ notice before starting the new system.

Where it stands:

The drug industry trade group PhRMA sees the rebate model as a way to add needed transparency to federal drug discounts, spokesperson Alex Schriver said in a statement to Axios.

“We’re heartened by the administration’s efforts to ensure that the program operates as it’s intended,” CEO Steve Ubl told reporters last week.

Pharmaceutical companies have been trying to move in the direction of rebates themselves over the past couple of years, arguing that many providers are gaming the system and getting 340B program discounts as well as Medicaid rebates for drugs.

Courts have blocked individual companies like Bristol Myers Squibb and Johnson & Johnson from switching to rebates from up-front discounts.

The other side:

Hospitals are planning to respond to the information request, but they’re holding out hope that HHS will drop the rebate idea altogether.

HHS should “recognize that imposing hundreds of millions of dollars in costs on hospitals serving rural and underserved communities is not a sound policy,” Aimee Kuhlman, AHA vice president of advocacy and grassroots, said in a statement.

AHA and other hospital groups last week sent a letter to the administration asking to extend the comment period and potentially laying the groundwork for another legal challenge if that isn’t granted.

Community health centers, meanwhile, are urging Congress to pass a bill that exempts them from rebate experiments.

The bottom line:

The administration isn’t giving up on the rebate idea. That will only add to the controversy over a program that covers more than $81 billion in annual drug purchases.

Last week, the Trump White House released a plan to reduce health care costs that is consistent with its approach to many differing questions. There was a dominant populist impulse, with several provisions targeting corporate interests for supposedly causing most of the problems consumers experience, alongside a more libertarian orientation that emphasizes patient choice and control, although the proposals tied to this theme lacked sufficient detail to be convincing. What the White House did not provide is an actionable legislative plan to lower the cost of health care for most Americans. Instead, the status quo is almost certain to prevail this year and for the foreseeable future.

That might have been the intention, as the White House probably wants to avoid a protracted debate on health care as the midterm election approaches. The administration’s one-page summary of its ideas, called “The Great Healthcare Plan,” seems to have been put together for defensive reasons. The Republican Party has been scrambling for several months to deflect Democratic attacks over the December expiration of enhanced premium credits for Affordable Care Act (ACA) insurance plans that had been approved through 2025 during President Joe Biden’s term. The Trump White House’s plan was developed to provide the Republican Party, or at least key officials in the administration, with something to talk about when opposing a straight extension of the credits.

The administration’s plan contains nine proposals that purport to boost transparency, lower costs, or give consumers more control over their health care choices. The net effect of the plan will be minimal because the causes of high and rapidly rising health costs have deep roots and cannot be addressed with surface changes that leave untouched the basic architecture of the status quo.

Last week, the Federal Government released agency reports that paint a perplexing picture for the health industry entering 2026:

Tuesday, The Bureau of Labor Statistics released the EMPLOYMENT COST INDEX SUMMARY noting “Compensation costs for civilian workers increased 0.7%, seasonally adjusted, for the 3-month period ending in December 2025 and 3.4% for the 12-month period ending December, 2025.” Closer look: it was +3.6% for hospitals and +3.2% for nursing homes.

Wednesday, the Bureau of Labor Statistics released THE EMPLOYMENT SITUATION — JANUARY 2026: “Total nonfarm payroll employment rose by 130,000 in January, and the unemployment rate changed little at 4.3%… Job gains occurred in health care, social assistance, and construction, while federal government and financial activities lost jobs…Health care added 82,000 jobs in January, with gains in ambulatory health care services (+50,000), hospitals (+18,000), and nursing and residential care facilities (+13,000). Job growth in health care averaged 33,000 per month in 2025. Employment in social assistance increased by 42,000 in January, primarily in individual and family services (+38,000).” Closer look: the jobs report is based on employer sampling which is revised as subsequent surveys are added to the sample. Thus, data for any single month is at best only directionally accurate. Reliable federal data about the healthcare workforce remains a work in process.

Friday, BLS released the CONSUMER PRICE INDEX REPORT FOR JANUARY, 2026: “Consumer prices rose 2.4% in January from a year earlier down from 2.7% in December.” Core prices, which exclude volatile food and energy items, rose 2.5% from a year earlier vs. medical care commodities (+.3%), hospital services (+6.6%) and physician services (+2.1%). Closer look: prices for hospitals and physicians vary widely (by ownership, specialty, size and location) but differ in one respect: Medicare rates are used as a proxy for both, but rate setting for physicians disallows inflationary adjustments.

Taken together, they reflect the obvious: The healthcare economy is a big deal in the scheme of the overall economy and the nation’s monetary policy. The CBO’s revised projection shows it increasing from 18% of the GDP today to 20.3% by 2033.

But a closer look exposes worrisome signals in the reports:

Increased housing costs are destabilizing lower-and-middle income household finances resulting in increased medical debt, delayed care and heightened sensitivity to healthcare affordability. It also has direct impact on the availability of the local workforce where home ownership or rental costs are out of reach.

Hospital price increases used to offset escalating labor and supply chain costs are well-above other spending categories; some have healthy margins while others are struggling. Public perception about hospital finances is susceptible to misinformation and executive compensation is a lightning rod for detractors. Per a KFF report last week, hospitals accounted for a third of total health spending increases since 2023 but 40% of the total spending increase—higher than any other factor. That puts added pressure on hospitals to justify costs and account for prices.

The healthcare workforce has become the backbone of the labor market: the majority of its expanded labor pool are skilled and unskilled hourly workers for whom competitive wages and benefits are key. Healthcare delivery is labor intense. Across all settings in healthcare, efforts to increase productivity via data-driven, technology-dependent process improvements have been made. But reimbursements by payers have punished improvements in productivity requiring more work for less money. The result: disenchantment about the future of the system is a tsunami in the healthcare workforce.

In every hospital, medical group nursing home and home care organization, pressure to attract and keep a viable workforce is mission critical. In some, the Human Resource function is effectively aligned with regulatory, clinical and technology changes, in some, compensation plans from executive to support are strategically designed to optimize short and long-term performance and ROI. In some, the Board Compensation committee is well-prepared to adjust policies as talent requirements change. In some, leaders and frontline teams show mutual respect and sincere appreciation. But many fall short.

These reports are public record. But their headline stats don’t tell a complete story. Every healthcare organization is obligated to do the rest.

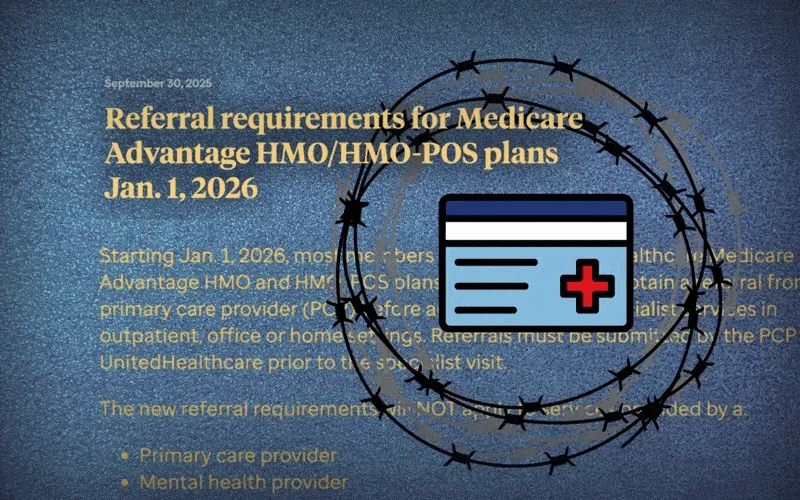

New referral requirement for HMO and HMO-POS plans alarms patients and doctors, who predict bureaucratic delays and reduced access to care.

Theresa Schwartz, a 66-year-old Milwaukee plumber, says she’s one of those people who never went to a doctor before she was 40. That has changed in the second half of her life as she has dealt with major health issues, including lung cancer and rheumatoid arthritis.

In recent years, her regular visits to the Milwaukee Rheumatology Center have been covered, without hassle, by her Medicare Advantage insurance provided through the nation’s largest health insurer, UnitedHealthcare. But Schwartz was surprised and became upset during her most recent visit there when she was told that — because of a new UnitedHealthcare policy — she will now need a referral from a primary care physician to be covered.

Schwartz said she’s never had a primary care physician.

“I’m just spinning the hamster wheel,” said Schwartz, who said in a phone interview that she is already confused and frustrated by the new policy and has little patience or interest in finding a UnitedHealthcare in-network physician. She even offered to pay cash for her visits, which the Milwaukee clinic said it cannot accept for Medicare patients.

Schwartz’s discontent over the new UnitedHealthcare policy — which launched at the beginning of the year, with reimbursements for visits without referrals to certain types of specialists set to stop after April 30 — is hardly unique. Health care advocates say the policy change affects a large pool of senior citizens in the insurer’s HMO and HMO-Point of Service (POS) Medicare Advantage plans. This is a healthy chunk of the estimated 8.5 million seniors who get their Medicare Advantage coverage through UnitedHealthcare — one of every four MA enrollees.

“I have patients in their 90s who are now facing this, if you can imagine,” said Nilsa Cruz, the tireless patient advocate for Milwaukee Rheumatology Center who frequently speaks out at the Wisconsin state capitol and elsewhere about health care issues. “And they don’t understand their insurance cards, anyway.”

Cruz predicted “a total disaster” when the UnitedHealthcare policy, which is currently in a sort of soft-launch mode, takes full effect in May, as both patients — many who’ve been seeing a specialist for 15 or 20 years without ever needing a referral — and their doctors struggle to adapt to an onerous new system.

The change, which is likely to have the effect of reducing specialist visits and thus saving UnitedHealthcare millions if not billions of dollars, isn’t taking place in a vacuum. Rather, it’s one more assault on seamless and efficient health care coverage. Patient inconvenience seems to be a cornerstone of this icon of Big Insurance’s plan for dealing with what its executives claimed last year were $6.5 billion in annual higher costs.

In recent months, UnitedHealthcare has dropped as many as 180,000 enrollees from its Medicare Advantage plans in targeted geographic areas and plans to drop more than a million by the end of this year. It has also “narrowed” its provider networks, relegating certain clinical practices, such as rheumatology clinics, which provide costly infusion therapies, to out-of-network status.

Some analysts had predicted a kinder, gentler UnitedHealth after a tragedy that made national headlines — the murder in New York of UnitedHealthcare CEO Brian Thompson in December 2024 — focused new attention on the company’s aggressive use of prior authorization to deny coverage for medically necessary care. Instead, the giant insurer has doubled down on ways to drive the highest-cost patients and providers from its system, making it necessary for millions of seniors to scramble to find either new MA insurers or new doctors. Many undoubtedly will go untreated.

The unwelcome requirement for many of UnitedHealth’s Medicare Advantage patients to get primary-doctor referral for treatments they’ve often been getting for years from a specialist looks to be one more way the company is nickel-and-diming a path back to higher profits on the backs of patients with chronic health issues.

Needless to say, UnitedHealthcare, whose financial performance has disappointed investors for more than a year, doesn’t portray the change that way. In announcing the move late last year the company hailed it as a way to improve communication between its affiliated providers and prevent unnecessary tests or procedures, or visits to a specialist that aren’t really necessary.

“The goal of this referral process is to help increase primary care provider (PCP) engagement with patients and help foster collaborative partnerships between PCPs and specialists,” is the upbeat jargon UnitedHealthcare used to explain the change on its provider portal.

Since Jan. 1, the change has been in what UnitedHealthcare considers “a trial period,” which means that while it wants patients to begin getting primary-care referrals before seeing certain types of specialists, visits without a referral are still covered for now. That will no longer be the case after April 30.

The policy does exempt more than a dozen specialists or types of visits — most notably oncology, as well as mental health treatment, physical therapy, and some other common medical treatments. It also won’t affect MA enrollees in California, Texas, and Nevada where referrals were already required.

Madelaine Feldman, M.D., the New Orleans-based immediate past president of the Coalition of State Rheumatology Organizations, said she imagines dire scenarios in which a patient with a sudden flare-up cannot get speedy treatment because of the inability to get a speedy referral, or visits that aren’t covered because the referral is mishandled.

“So the fact that UnitedHealthcare has decided that rheumatologists are not capable of deciding when a patient needs to be seen is ludicrous, capricious, and most importantly, dangerous,” Feldman said. She added that situations that are harmful for patient care “will be seen more and more as a result of policies enacted to improve UnitedHealthcare’s bottom line.”

But for people enrolled in the company’s HMO and HMO-POS Medicare Advantage plans, the new policy seems less a way of improving communication than an additional and unwanted barrier to receiving care.

“Today I found out about it, and I don’t think it’s fair,” said Pamela Matias, a 63-year-old infusion-therapy patient at the Milwaukee Rheumatology Center who filmed a video after learning of the change. “I’ve been getting this medication for 20 years and never needed a referral.”

Unlike Schwartz, Matias does see a primary care doctor, but she still worries that the extra hassles of getting a referral — and making sure it goes through properly — have longtime rheumatoid arthritis patient alarmed. “Without my medication, I would not be able to walk,” she said. “I’ll be in 100% pain all day long.”

Cruz, the center’s patient advocate, said that during this trial period, it’s not just patients who are disoriented. An early problem she’s seen with the program is that doctors’ offices are often faxing or attempting to call in patient referrals when UnitedHealthcare is only recognizing those that are made electronically through its online portal. What’s more, she said doctors need to specify how many visits are covered during a six-month window.

Cruz said even one of the largest health care practices in Wisconsin was improperly faxing the referrals. “I think they were faxing up until the other day — you know, a month and a half, almost, into this thing,” she said. “So that tells you something. Andrimary care physicians were not all fully informed.” Even if they are trained, primary-care doctors don’t always know how many specialist visits a patient will need until they are reevaluated by the specialist and begin their treatments.

If doctors don’t understand the new UnitedHealthcare policy, she worries, then how will elderly Medicare patients — including some with major disabilities — be able to follow the rules? Furthermore, if a patient’s current primary-care doctor retires or relocates, it often takes months in today’s frenzied health care environment to get an appointment with a new one, which could delay critical care.

As a rabble-rousing patient advocate, Cruz seems somewhat ahead of the curve in anticipating a crisis. Many specialists are just beginning to absorb the changes and won’t feel a real impact until May, when UnitedHealthcare stops paying specialists for their patients who didn’t obtain referrals.

But Cruz said she is already lobbying the Coalition of State Rheumatology Organizations, where she is a highly active member, to take a stand against UnitedHealthcare’s new policy, noting that it targets only the lowest-cost Medicare Advantage HMO plans and not the higher-end PPO policies, let alone its commercial insurance customers. To her mind, that is discrimination. “They’re doing the HMO — the sickest patients,” she said. “The sickest.”

This and other moves from UnitedHealthcare and its competitors have the effect of pushing the sickest and most expensive patients off their rolls, either by dropping customers outright or making it harder for them to access the medical care they so desperately need. Forcing sick people to make extra doctor visits to get treatment undoubtedly will cause many to delay or even forgo care — which, sadly, seems to be what UnitedHealthcare is going for as it tries to get back into Wall Street’s good graces.