There’s a good chance your health insurance premiums are going up next year, regardless of where you get coverage.

Why it matters:

The spike in what millions of Affordable Care Act plan enrollees pay will be acute, but workplace insurance is getting more expensive, too — and all at a time when affordability is prominently on Americans’ minds.

ACA premiums have dominated the political discourse in Congress for weeks, but there’s no real sign that any relief is coming from Washington.

Even extending the Biden-era enhanced ACA subsidies — which most Republicans don’t want to do — would do nothing to address what’s driving the surging cost of care or employer insurance affordability issues.

And all signs point to Democrats hammering Republicans for high costs in all forms of health insurance leading up to next year’s midterm elections.

The big picture:

Health insurance gets more expensive almost every year, keeping up with increases in the costs of procedures, tests, drugs and more. But some years see bigger jumps than others, and 2026 is looking like one of those years.

That means tough choices for families, employers and workers all faced with shouldering higher premiums or out-of-pocket spending. Some will conclude it’s prohibitively expensive and go uninsured.

Another thing that’s different about this year is that the white-hot political rancor around ACA premiums is putting health insurance back centerstage politically.

By the numbers:

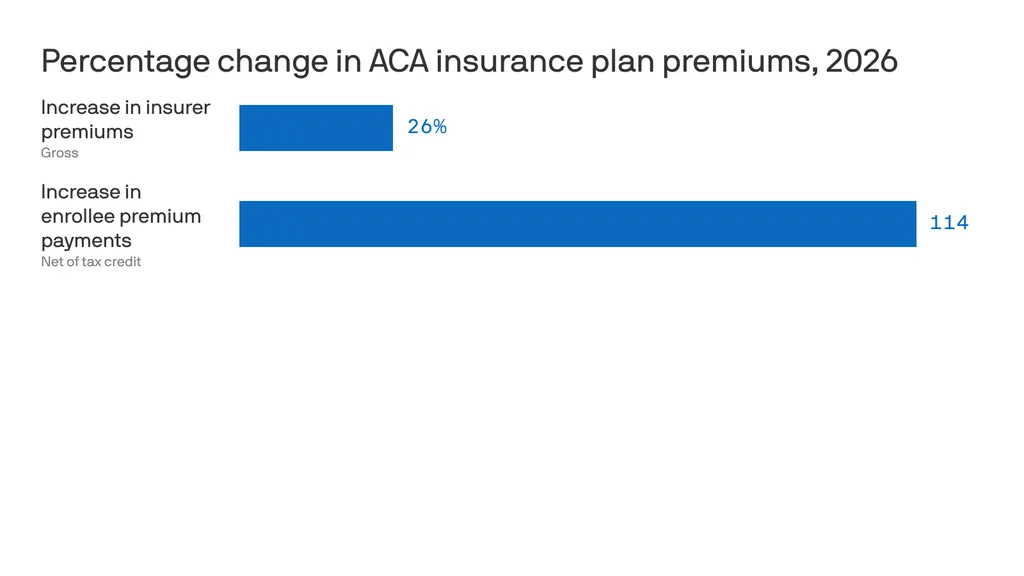

ACA insurers themselves are raising premiums by an estimated 26%, in part due to rising hospital costs, higher demand for pricey GLP-1 drugs like Ozempic, and the threat of tariffs.

But add in the loss of federal subsidies, and the increase is 114% — or more than double what they currently pay, according to KFF. 22 million out of 24 million marketplace enrollees now receive subsidies.

Premiums in the small group employer market will go up by a median of 11%, also per KFF, due to some of the same reasons insurers cite in ACA markets.

For employer health insurance, there’s no comprehensive data yet for 2026, but estimates from earlier this year put the increases in the high single digits.

For example, according to Mercer, health benefit costs are expected to increase 6.5% per employee in 2026, and many employers are planning to limit premium increases by raising out-of-pocket costs for employees.

One factor driving these increases is advances in medicines, like new cancer treatments, that are more expensive, according to Mercer.

But people are also using health care more, per Mercer. That’s possibly because they missed or delayed care during the pandemic — but also because the use of AI in doctors’ offices gives them more capacity and allows them to work faster.

Between the lines:

Just this month, Gallup polling found that approval of the ACA has hit an all-time high of 57%, including more than 6 in 10 independents but only 15% of Republicans.

Another recent Gallup poll found that 29% of Americans say that cost is the “most urgent health problem” facing the country, up from 23% a year ago.

The bottom line:

Get ready to hear a lot more about health care costs over the next year — while potentially also experiencing your own premium increase.

Next year, seniors and families will have more stringent and more unaffordable health coverage thanks to new AI-driven prior authorizations in Medicare and loss of subsidies in the ACA.

The New Year is just two weeks away, and when Americans wake after clinking champagne and kissing at midnight, the health care landscape in the United States will be in worse shape than it was in 2025. There is a growing list of why that’s true, but here are a couple of developments that will make it harder for many of us to get the care we need:

The December 31 expiration of the Affordable Care Act enhanced subsidies, which will lead to millions of Americans losing coverage and make premiums barely affordable for millions of others; and

CMS’s January 1 implementation of a new pilot project that will put private, for-profit contractors using AI-powered prior authorization in traditional Medicare.

Unless policymakers change course, many Americans will be ringing in 2026 with higher costs, less access and a nasty health care hangover.

WISeR strikes at 12

As we’ve reported, the implementation of the Wasteful and Inappropriate Service Reduction (WISeR) model’s will mark the first time in traditional Medicare’s 60-year history that for-profit companies will decide whether seniors receive certain medical services their doctors recommend. Six companies — many with deep ties to Big Insurance and insurer-backed venture capital — will suddenly have the power to say yes or no to 17 procedures that never required prior authorization before. And for these companies, the more the denials, the bigger the profits.

As Dr. Seth Glickman documented after sitting through CMS’s own WISeR webinar, the rollout has been vague on details and confusing to providers and patients. CMS even admitted during the webinar that the vendors chosen to administer the model were selected in part based on their “success” of using prior authorization in the private Medicare Advantage program, which is notorious for denials, delays and life altering decisions.

Some lawmakers in Washington have taken notice. A coalition of Democrats introduced the Seniors Deserve SMARTER Care Act, warning that WISeR creates “a dangerous incentive to put profits ahead of patients’ health.” Imposing prior authorization in traditional Medicare “will kill seniors,” said Rep. Mark Pocan, one of the bill’s sponsors.

Kiss subsidies goodbye

While WISeR threatens seniors’ access to care, millions of working families are facing a different New Year’s surprise: the expiration of enhanced ACA marketplace subsidies, which Congress has (so far) failed to extend or replace. As Rachel Madley, PhD wrote in October, families will have to gamble when they pick a health insurance plan. She added:

The enhanced premium subsidies being debated in Congress right now are a lifeline for so many of us and must continue in the short term, but they don’t fix the underlying problem: Private insurers extract value rather than control costs or provide access to necessary and affordable care. Decades of experience show that when profits rule health insurance, families face financial ruin no matter which plan they pick during open enrollment.

But as we’ve noted before, this isn’t an existential crisis for Big Insurance. ACA marketplace plans are not where insurers make their real money. Their profits flow increasingly from taxpayer-funded programs like Medicare Advantage and Medicaid managed care — the same universe WISeR is quietly expanding.

One proposal to “solve” the subsidy issue, endorsed by President Donald Trump and HELP Chairman Bill Cassidy, would not extend the tax credits but put $1000 to $1500 into government-sponsored health savings accounts (HSAs). HSAs can be helpful if you you have crappy insurance – or are rich and need an additional place to put your money to avoid taxes – but not a meaningful solution to the millions of Americans facing a 75% hike in premiums or finding themselves priced out of coverage altogether in 2026. The supporters of this approach claim it would somehow take money away from health insurers, but it would just reroute federal dollars to those same companies. For instance, UnitedHealth Group, which owns the nation’s biggest HSA custodian, could grab even more of our tax dollars than they already do. Meanwhile, families would still be exposed to unaffordable premiums and massive out-of-pocket costs. Champagne dreams.

Thanks to these changes in health care: The hangover on January 1, 2026, won’t only be from the previous night’s festivities – and it won’t be cured with some water and Advil. Cheers.

There’s likely to be one more round of health care votes in the House next week after the Senate votes down two rival Affordable Care Act subsidy proposals Thursday — but they won’t get any closer to extending the enhanced subsidies.

Why it matters:

Those subsidies now appear certain to expire at the end of the year, short of a last-minute breakthrough — and out-of-pocket premium costs will more than double on average for roughly 20 million ACA enrollees.

Driving the news:

The Democratic proposal that will get a Senate vote Thursday would extend the enhanced subsidies for three years, while the Senate GOP proposal would not extend the subsidies but instead provide money for health savings accounts.

Both will fail to get the needed 60 votes.

Senate Majority Leader John Thune (R-S.D.) has left the door open for further bipartisan talks after both votes fail, but there is deep skepticism in both parties that any such deal is possible.

Sen. Tim Kaine (D-Va.) said it’s possible there is “additional discussion” after the failed votes, but said the issue also might end up in a “political solution in November when people pick the side that’s for them.”

The latest:

House GOP leaders outlined a range of possible health care options on Wednesday morning, but they have little to do with the subsidies, which weren’t included in their plans.

GOP leaders will bring “consensus” bills to the floor next weekthat aim to lower health care costs, a source who attended House Republicans’ Wednesday morning conference meeting told Axios.

Those could include expanding health savings accounts and association health plans, which allow employers to band together to purchase coverage.

Overhauling pharmacy benefit managers with the goal of lowering drug costs was also discussed, along with funding ACA payments known as cost-sharing reductions (CSRs).

The intrigue:

On the House side, a bipartisan group of moderates including Reps. Brian Fitzpatrick (R-Pa.) and Jared Golden (D-Maine) filed a discharge petition, a procedural move to force a vote on a compromise extension plan.

But that effort to go around House GOP leadership faces long odds against getting the required majority of the chamber to sign on.

Modifications to the subsidies in that plan designed to win over GOP votes, like a crackdown on zero premium plans that backers say fuel fraud, could lose Democratic support due to concerns about coverage loss.

Democratic leaders havebeen focused on a clean three-year extension, saying that is the clearest way to address the issue with little time remaining to implement changes before the new coverage year starts Jan. 1.

House Democratic Leader Hakeem Jeffries (N.Y.) told reporters Wednesday he has no position on the discharge petition.

The bottom line:

There is also deep resistance to a subsidy extension among many Republicans.

Thune has said he thinks Democratic leadership is more interested in a “political messaging” vote this week than in entertaining reforms to the subsidies that Republicans point to.

Even if members in either chamber are able to make progress on a consensus compromise subsidy plan, which in theory could be attached to a government funding bill needed before Jan. 30, the divisive issue of abortion hangs over all of the discussions.

Many Republicans insist on new limits preventing the subsidies from going to insurance plans that cover abortion. Democrats say that is a dangerous expansion of safeguards that already require taxpayer funds to be segregated and not pay for abortion coverage.

Yesterday aboard Air Force One, President Trump was asked by a reporter if he supported Senators Bill Cassidy (R-LA) and Mike Crapo’s (R-IN) new health care proposal, which would authorize $1,500 deposits in Health Saving Accounts (HSAs) for lower-income individuals to replace the expiring Affordable Care Act (ACA) subsidies. The president’s response to the question was telling. And it shows just how much Big Insurance has fallen from grace in recent months.

For decades, merely expressing disenchantment with private health insurers could get you labeled as a socialist. Now we are seeing daily criticism of health insurance companies from people across the political spectrum, leading one to not know if a quote like “Americans are getting crushed by health insurance with monthly payments” is coming from a progressive, like AOC, or a conservative like MTG. (Hint: that quote was from MTG). Trump’s response was in the same vein and could lead one to believe there is a chance of the left and right finding common ground in holding insurance companies accountable for their greed.

Where Trump is right. Where Trump is wrong.

Below we will dissect the president’s response and explain where he’s right and wrong.

“I like the concept [of the Cassidy-Crapo legislation]. I don’t want to give the insurance companies any money. They’ve been ripping off the public for years.“

This is true. Big Insurance has been ripping us off for years. And almost all of insurers’ growth in recent years has come from us as taxpayers. Most big insurers now make far more money on the lucrative Medicare Advantage business and managing state Medicaid programs than from their commercial health insurance plans. And they’ve even figured out how to bilk the VA.UnitedHealthcare, the biggest insurer, now gets more than 75% of its revenues from taxpayer-funded programs. And yes, insurers are getting hundreds of billions of dollars every year from the ACA subsidies that are at the center of debate in Washington.

Here are a couple of examples. Private health insurers took in over $500 billion in tax dollars to administer Medicaid in 2023. And this year alone, they will be overpaid – yes overpaid – $85 billion as a consequence of how they’ve rigged the Medicare Advantage program.

Insurers also take in massive amounts of money in the form of premiums that people pay thinking that money goes to care. Much of that money ends up going toward things (and people) that do nothing to get us well or keep us well. Since 2014, the seven largest insurers have made over $500 billion in profits, and they used $146 billion to buy back their own stock. So yes, Trump is correct, health insurance companies have been ripping people off for years.

“Obamacare is a scam to make the insurance companies rich.”

No, Mr. President, the ACA is not a scam and most Americans now know that it has done a lot of good for a lot of people. Among other things, it made it possible for millions of people who previously had been blackballed by insurers because of a preexisting condition to finally get coverage. It brought us many long-overdue consumer protections, outlawed junk insurance, enabled young people to stay on their parents policies until they turned 26, alleviated job-lock through the creation of the ACA (Obamacare) marketplaces, and it made millions more low-income families eligible for Medicaid.

But, the president is right to say that Big Insurance has gotten rich since the passage of the ACA. Between 2014 (the year the entirety of the ACA was implemented) and 2024, just seven for-profit health insurers amassed $543.4 billion in profits and took in a staggering $10.192 trillion in revenues.

“And they have made, I mean, you look, $1,400 to $1,700 increase, 100 percent increase over the last number of years. There’s really few things that have gone up like insurance companies.”

The president is kind of right. As KFF reports, the cost of a family policy has increased 60% since 2014 – a rate of increase much higher than general inflation and also higher than medical inflation. And as we’ve published previously, not only has the total cost of an employer-sponsored plan skyrocketed, so has the share of premiums workers must pay. This year, employers deducted an average of $6,850 from their workers’ paychecks for family coverage, up from $4,823 in 2014. And keep in mind, all that money our employers are having to send to insurance companies is not money that’s available to give raises to workers or hire more people.

“They’re getting numbers and money like nobody’s ever seen before. Billions and billions of dollars is paid directly to insurance companies. We’re not going to do that anymore.”

The president is right. Several Big Insurance companies have ballooned in size over the past decade to become some of the world’s biggest corporate conglomerates. UnitedHealth Group, CVS/Aetna and Cigna are now numbers 3, 5 and 13 on the Fortune 500 list. The only American companies that take in more revenue than UnitedHealth are Walmart and Amazon.

“I believe Obamacare was set up to take care of insurance companies, not to take care of the American public.”

The president has his history wrong here. While there are plenty of Monday-morning-quarterbacking you can do for the ACA – the law was not passed to “take care of insurance companies.” While the ACA didn’t fix everything – not by a long shot – it did stop some of the insurance industry’s worst abuses, like refusing to sell policies to people with preexisting conditions – even acne – and “rescinding” policies to avoid paying for life-saving care. Some insurers were found to be paying employees bonuses to find policies to rescind, including the policies of women almost immediately after being diagnosed with breast cancer.

It prohibited health insurers from charging people more because of a preexisting condition and from dumping the sick so they could reward their shareholders more generously. Keep in mind that insurers consider every claim they pay as a loss, hence the term “medical loss ratio” (MLR), which the ACA addressed by requiring insurers to spend at least 80%-85% of our premiums on our health care.

And it’s not like Big Insurance wanted the ACA to pass. Back in 2010, America’s Health Insurance Plans (AHIP), the PR and lobbying group for health insurers, quietly funneled $100 million to the U.S. Chamber of Commerce to orchestrate a PR, advertising and lobbying blitz to keep the ACA from being passed.

While big health insurance companies have only grown since the passage of the ACA, it has been Big Insurance’s corporate maneuvers and work on Capitol Hill (not the law itself) that has allowed these companies to flout some of the ACA’s regulations and bend the law to do their will.

“I love the idea of money going directly to the people, not to the insurance companies. Going directly to the people. It could be in the health savings account. It could be a number of different ways.”

While that is a compelling sound bite, it’s disingenuous. The money proposed by Cassidy and Crapo to go to HSAs would then be used by enrollees to buy insurance, thus still giving money to the insurance companies. Even worse, the proposed amount of money to go to people’s HSAs to help them pay for health insurance and care is $1,000-$1,500. This is money that would be used to purchase a bronze or copper plan with a high deductible (with many of those plans having deductibles north of $5,000). That means under this plan people would still need to come up with thousands to meet their deductible on top of paying their premiums every month. $1,000 wouldn’t come close to even covering the premiums for a decent policy, much less the out-of-pocket costs.

Replacing ACA subsidies with HSAs would still keep Americans tied to the same private health insurers that Trump calls “big, bad” and “money-sucking.”Most families would still be exposed to crippling medical bills, and even more tax dollars would flow to insurance conglomerates that own HSA custodian businesses (like UnitedHealth’s Optum Bank).

“And the people go out and buy their own insurance, which can be really much better health insurance, health care.”

That’s wishful thinking far removed from reality. The health insurance plans available to people who get money for their HSAs under the Cassidy-Crapo proposal – rather than getting subsidies – are the same as those currently available. Worse, without the subsidies, people will not be able to afford the gold or silver plans that have lower out-of-pocket costs. In reality the plans that people buy under the proposed Cassidy-Crapo plan would have less value than the plans they previously bought with subsidies.

Trump’s comments are coming ahead of tomorrow’s scheduled vote in the Senate on dueling Democratic and Republican proposals to deal with the enhanced subsidies for ACA plans that will expire in three weeks. Without those subsidies, premiums will spike for many of the 24 million American enrolled in “Obamacare” plans. Democrats want to extend the subsidies for three years. Republicans, led by Senate Majority Leader John Thune, will push a plan replacing those subsidies with direct payments into individuals’ Health Savings Accounts (HSAs), as the president is suggesting. Neither plan is expected to get the 60 votes required for passage. What happens next is anybody’s guess.

The Senate will vote tomorrow on dueling health care plans: Democrats’ proposal to extend enhanced Affordable Care Act subsidies for three years, and a plan from two Republican chairmen that would instead give enrollees funds in health savings accounts.

Why it matters:

The move gives the GOP an alternative to point to if the ACA subsidies expire at the end of the year and health care costs spike for millions of people.

But neither plan is expected to get the 60 votes to advance.

Driving the news:

The plan from Finance Committee chair Mike Crapo (R-Idaho) and health committee Chair Bill Cassidy (R-La.) wouldn’t extend the tax credits past their year-end expiration, instead providing $1,000 to $1,500 in health savings accounts to help certain marketplace enrollees with out-of-pocket costs.

It’s drawn sharp criticism from some Democrats for leaving working-class Americans saddled with high health costs.

Senate Majority Leader John Thune (S.D.) left open the possibility of talks after both votes fail on Thursday, though there is deep skepticism about the chances of reaching a bipartisan agreement.

“If neither proposal gets 60 then we’ll see where it goes from there,” Thune said.

President Trump, asked later about the Crapo-Cassidy bill and whether Republicans should vote for it, told reporters, “I like the concept. … I love the idea of money going directly to the people.”

Between the lines:

On the House side, GOP leadership, committee chairs and leaders of House GOP factions met yesterday to discuss health proposals, with an eye toward a possible House vote this year.

Members left the meeting tight-lipped, saying discussions are ongoing.

The full House Republican conference is expected to discuss health proposals in its meeting this morning ahead of potential votes next week.

Over 17 million nonelderly Californians (55%) received health benefits through an employer in 2023. The California Health Benefits Survey (CHBS) tracks trends in these workers’ coverage, including premiums, employee premium contributions, cost sharing, offer rates, and employer benefit strategies. In 2025, the survey also included questions about provider networks, coverage for GLP-1 agonists, premium cost drivers, and employee concerns about utilization management. The CHBS is jointly sponsored by the California Health Care Foundation and KFF.

KEY FINDINGS INCLUDE:

Premiums for covered workers in California are higher than premiums nationally. The average annual single coverage premium in California is $10,033, higher than the national average of $9,325. The average annual family premium in California is $28,397, higher than the national average of $26,993.

Overall, the average family premium has increased annually by 7% in California and 6% nationally. The average single premium has increased 8% annually in California and 6% nationally. Since 2022, the average premium for family coverage has risen 24% in California, higher than national measures of inflation (12.2%) and wage growth (14.4%).

Workers are typically required to contribute directly to the cost of coverage, usually through a payroll deduction. On average, covered workers in California directly contribute 14% of the premium for single coverage and 27% for family coverage in 2025. These shares vary considerably, and some workers face much higher premium contributions, especially for family coverage.

A lower share of covered workers in California face a general annual deductible for single coverage than covered workers nationally (75% vs. 88%), and the average deductible is lower ($1,620 vs. $1,886). The share of California covered workers with a deductible has increased since 2022 (68% to 75%).

Employers in California are significantly less likely than employers across the nation to say there were sufficient mental health providers in their plans’ networks to provide timely access to services.

Many employers report concerns about out-of-pocket costs: 47% of firms offering health benefits indicate that their employees have a “high” or “moderate” level of concern about the affordability of cost sharing in their plans. About one in 10 covered workers in California faces a general annual deductible of $3,000 or more for single coverage.

Large California employers view drug prices as a major driver of rising premiums. Thirty-six percent of large firms report that prescription drug prices contributed “a great deal” to premium increases.

Over one-quarter of large firms (28%) offering health benefits in California say they cover GLP-1 agonists when prescribed primarily for weight loss. Nearly one-third of these firms report higher-than-expected utilization of this benefit.

Read the full report on the KFF website or download it below.

Structural, regulatory and competitive changes will alter the landscape.

10 areas will likely be the foci.

Last week…

the stock market took a dive largely due to tech company volatility resurrecting fears of an A.I. bubble.

reports from the Departments of Labor and Commerce confirmed mixed signals about the economy: job growth was relatively strong but inflation (3%) remained stubbornly above its 2% target and consumer confidence slid.

Target warned Black Friday sales later this week will likely signal softness in consumer spending, and

Congress returned to DC after its 43-day shutdown that ended with no agreement on extension of insurance tax credits that expire at year end.

This week, Thanksgiving will likely slow down things on the U.S. domestic front but not for healthcare. Unlike just about every other industry in the economy, we operate 24/7/365. And like some industries, demand for our services is hard to predict– acts of God, accidents, court decisions, regulatory policy changes, social media “experts” et al. make predictions educated guesses at best. New technologies, clinical innovations, A.I. and private capital keep planners off-balance. Short-terms plans are more defensible; longer-term plans more challenging.

Thus, the industry is understandably focused on 2026. Here are assumptions:

Affordability for groceries, transportation, housing and healthcare (premiums and out-of-pocket) will drive media attention, public opinion and voting November 3, 2026.

Congress will not extend tax credits that expire at year-end prompting a spike in the uninsured and under-insured populations. In tandem, large private insurers will raise premiums and increase leverage with providers to reduce competitive threats.

Media coverage of healthcare will feature sensationalism, soundbites and hyper-simplification: costs (affordability), prices, disparities, executive compensation, outcomes, community benefits, workforce dissatisfaction, profitability and business practices will be foci.

Warfare between hospitals, insurers, and drug manufacturers will intensify. Each will assert their systemic reform proposals serve the greater good best by protecting themselves against unwelcome threats.

States will be the epicenters of health system transformation. Federal changes will be paralyzed by partisan-brinksmanship and posturing for 2026 and 2028 elections.

Trust and confidence in the health system will decrease (further) to record levels of discontent.

And, reflecting on the current state of affairs in U.S. healthcare, here are 10 healthcare headlines you MIGHT see next year:

Employed physicians win class action challenge to hospital employment agreements citing clinical independence, excessive administrative costs concerns

IRS cuts not for profit health systems tax exemptions. Private investments, community benefits, executive compensation cited

UnitedHealth Group completes acquisition of HCA: sets stage for new era of competition in U.S. healthcare

EPIC completes interoperability agreement with CMS: public-private oversight board named

Congress passes most favored nation pricing for biologics, specialty drugs as states enact price controls

Large employers drop employee coverage due to costs, systemic flaws in system

Health and wellbeing services consolidated under HHS to integrate social services and health

Primary care physicians, nurse practitioners, community pharmacists launch national society to advance primary and preventive health services

CMS capitates, expands primary care services in restructured MSSP program

National coalition launched to design transformed system of health that’s accessible, affordable, comprehensive, efficient and effective

And, I’m confident, many others.

2026 is a mid-term election year. In 2016 (Trump 45 Year One), Republicans controlled 31 governorships and 68 legislative chambers. This January, the GOP will control 26 governorships and 57 legislative chambers– a 15% reduction on both. Politics is divided, affordability matters most to voters and healthcare is a high-profile target for campaigns so humility, thoughtful messaging backed by demonstrable actions will be an imperative for every healthcare organization.

2026 is a HUGE year for U.S. healthcare. The outcome is unknown.

As lawmakers debate ACA subsidy extensions and HSAs tied to banks and insurers, the public’s appetite for a health care overhaul is stronger than at any time since the 2020 Democratic primaries.

Washington is running out of hours to address the health care crisis of their own making. There are just 23 days before the Affordable Care Act’s (ACA) enhanced subsidies expire and congressional leaders are still trading barbs and floating half-baked ideas as millions of Americans brace for punishing premium spikes.

Meanwhile, the public has grown frustrated with both congressional dysfunction, and private health insurance companies that continue to raise premiums and out-of-pocket costs at a dizzying pace. According to new KFF data, 6 in 10 ACA enrollees already struggle to afford deductibles and co-pays, and most say they couldn’t absorb even a $300 annual increase without financial pain.

And even as Congress flails, Americans are coalescing around a solution party leaders rarely mention: Medicare for All.

A dramatic rebound in popularity

After Senator Bernie Sanders bowed out of the presidential race in April 2020, Medicare for All faded to the background following political infighting, industry fearmongering and the lack of a national champion. But nearly six years later, the proposed policy solution has re-emerged as a top choice among frustrated voters.

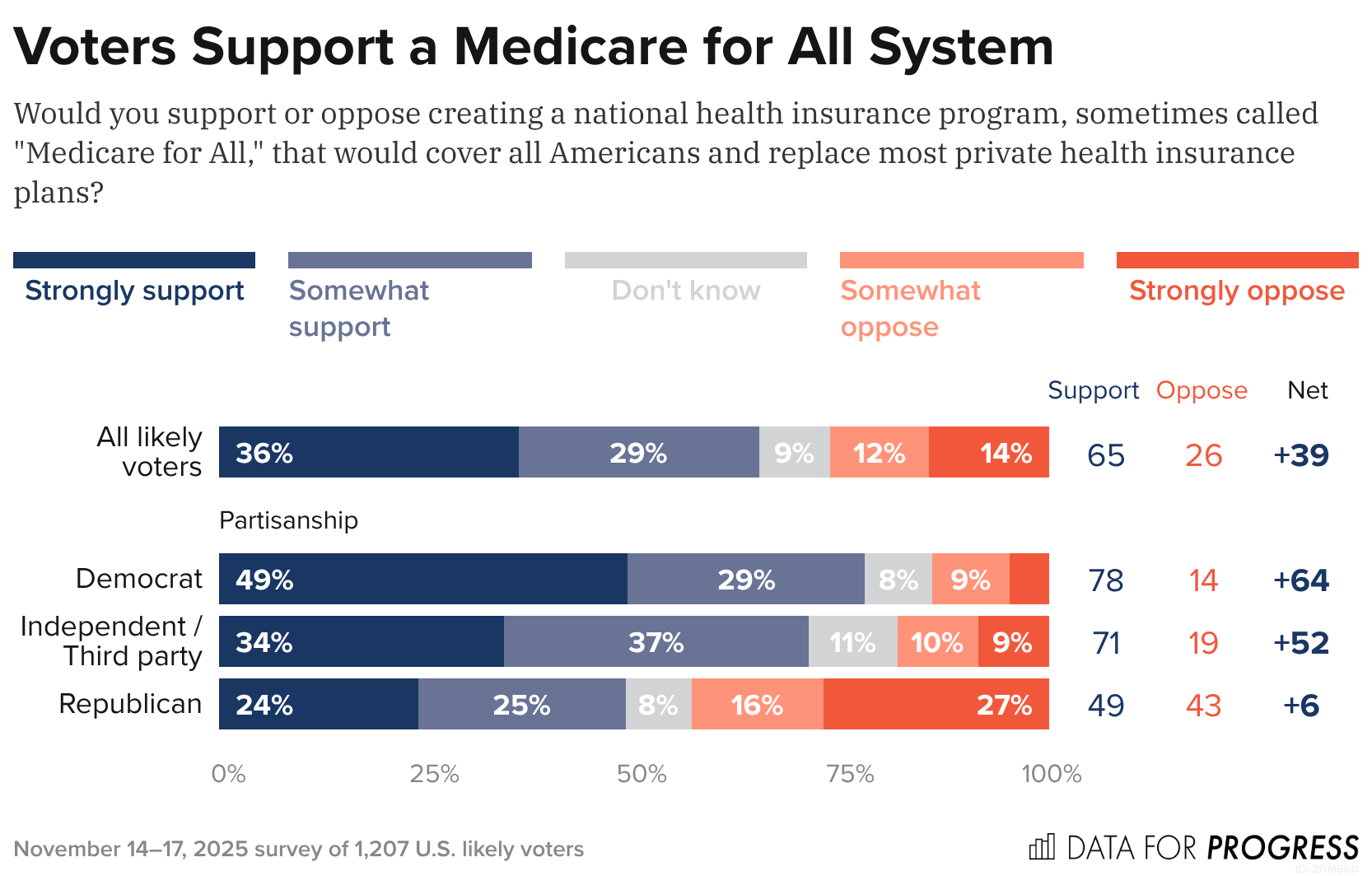

A new Data for Progress poll found that65% of likely voters (including 71% of independents and nearly half of Republicans) support creating a national health insurance program that would replace most private plans. What’s notable is that the poll shows that support barely budges – holding at 63% – even when voters are told Medicare for All would eliminate private insurance and replace premiums with taxes, a dramatic shift from years past when just 13% supported such a plan under those conditions.

The KFF poll shows that ACA enrollees lack confidence that President Trump or congressional Republicans will handle the crisis, with almost half of ACA enrollees saying a $1,000 cost spike would “majorly impact” their vote in 2026. Morethan half of ACA enrollees are in Republican congressional districts, which explains why Republicans representing swing districts are desperately trying to persuade their Republican colleagues — so far without success — to extend the subsidies.

Of course, Medicare for All still faces steep odds in Congress. Industry opposition remains powerful, Democrats are divided and Republicans are openly hostile. But the polling shift is significant and suggests the political terrain is changing faster than Washington is acknowledging — and that voters, squeezed by soaring premiums and dwindling subsidies, are being nudged toward policies previously attacked as too ambitious to pass.

And against this backdrop, Medicare for All’s revival feels less like a left-wing wet dream and more like a window into the public’s thinning patience. Americans are looking past the Affordable Care Act’s limits and past Big Insurance’s promises – and towards a solution that decouples Americans health from profit-hungry, Wall Street-driven corporate monsters. While Washington has met this moment with inaction, Americans seem ready to act.

The software monopoly that powers American hospitals wasn’t built for the data, speed, or intelligence the future of medicine demands.

Epic Systems is an American privately held healthcare software company, founded by Judy Faulkner in 1979, and has grown into the largest electronic health record (EHR) vendor by market share, covering over half of all hospital patients in the U.S.

Epic dominates American healthcare today. But so did Kodak in photography and GE in industry. Its software runs the country’s hospitals, determines the workflows clinicians, nurses and clinical support staff use, and shapes what data gets captured (or more often, what gets lost). It also serves as the front door for healthcare data for the patients it serves. Dominance has never guaranteed a future. Epic’s position reflects the architecture of the past, not the one emerging now.

More importantly, the sheer volume of activity occurring in these hospitals means they are collectively running thousands of experiments, mini clinical trials, and critical observations daily. The stakes are enormous: billions of dollars in drug discovery, the efficiency of clinical trials (currently plagued by poor recruitment and high costs), and the potential for better, personalized care. The data generated in these environments is the single most valuable, untapped resource in all of medicine.

However, this monumental source of value is being throttled by outdated infrastructure, and it shows. It’s hard to imagine a world where AI is used to its full potential in healthcare while Epic is still running the show. The ideas are oppositional at their core.

The Massive Data Problem

Technology is accelerating faster than any legacy system can keep up with. AI is reshaping every major industry, and healthcare will be forced to catch up. However, this essential transformation is structurally incompatible with the dominant system of record.

To put it bluntly: Epic has a data problem. A massive data problem. Not just imperfect data — structurally flawed data. What Epic captures is fragmented, delayed, and riddled with inconsistencies. Diagnoses become billing codes that distort reality. Interventions like intubations, pressor starts, and ventilator changes appear hours late, if at all. Outcomes are incomplete or missing. What remains isn’t a clinical record in any meaningful sense but a billing ledger dressed up as documentation. No model can learn reliably from that.

But the deeper problem is the data Epic never sees. Some of the most valuable information in modern medicine: continuous monitoring streams, ventilator logs, infusion pump data… never enters the EHR in a structured or analyzable form. In many cases, it isn’t captured at all.

I recently brought Roon (a well-known engineer at OpenAI) and Richard Hanania(a public intellectual/cultural critic)—both advisors in my new venture, in full disclosure—to one of the largest academic medical centers in the country. Both watched torrents of millisecond-scale data spill off monitors. Streams that could reveal what’s happening in the brain, heart, and vasculature. Valuable data… all vanished instantly. None of it logged. None of it stored. None of it correlated with outcomes. Roon captured this shock in a viral post on X/Twitter, essentially describing how hospitals are filled with catastrophic events like sudden cardiac death, yet we save none of the time-series data that could teach us how to prevent the next one. His shock distilled what people in technology grasp immediately and what healthcare has normalized: industries where human life isn’t exactly top of mind record everything; hospitals, where the stakes are life and death, learn almost nothing from themselves.

In Silicon Valley, losing data like this is unthinkable. In healthcare, it barely registers.

Epic was never built to ingest or learn from this scale of data. It was built to satisfy billing requirements, regulatory checklists, and documentation workflows. That is the beginning and end of its architecture. It is not a learning system, much less an AI system. It is not even a modern data system. And that is the root of Epic’s downfall.

The Cultural and Financial Moat

Epic is famous for its internal commandments — principles Judy Faulkner wrote decades ago:

Do not acquire.

Do not be acquired.

Do not raise outside capital.

(If you haven’t heard it, the latest Acquired podcast episode on Epic is essential listening)

But the same rules that built its empire now limit what it can become. What was once a strategic strength is now its ceiling.

The next era of healthcare software demands investments that were unnecessary when the EHR was the center of gravity. Building AI-native infrastructure: real-time data pipelines, device integrations, large-scale compute, continuous model training, semantic normalization — requires not millions but tens of billions of dollars. Most companies facing that kind of leap can raise capital, acquire talent, or merge with partners. Epic has ruled all of those options out.

Epic’s formidable market share is anchored by a massive customer sunk cost. With implementation fees often exceeding a billion dollars for large systems, the financial and political inertia makes replacing the EHR functionally unthinkable. However, this commitment only forces customers to defend an obsolete data architecture. By preventing them from adopting novel solutions, this inertia doesn’t protect Epic’s long-term viability, it simply guarantees a widening technical gap between the EHR and the transformative potential of AI.

A company optimized for slow, controlled expansion cannot transform itself into an AI-scale enterprise without violating the principles that define it. The culture that kept Epic dominant is the culture that prevents it from catching the next wave. Epic will continue to excel at documentation, billing, and compliance — but those strengths are anchored in the past. The future belongs to systems that learn, and Epic was never designed to learn.

The Shift to Middleware

Meanwhile, the broader economy is being held up by AI. The world’s largest tech companies are pouring staggering sums into compute, data centers, and model training. And all that compute needs rich, complex, high-value data to train on.

Healthcare is the only remaining frontier of that scale.

No other industry generates so much information while analyzing so little of it. No other sector represents nearly 20% of U.S. GDP yet still runs on fragmented workflows and manual processes. And the incentives here are unmatched: improving patient outcomes, reducing costs, eliminating inefficiency, accelerating drug development, modeling disease trajectories, and eventually automating the more repetitive layers of care. There’s even an irony: the very infrastructure needed to enable learning health systems would also finally make billing more accurate.

I’m not writing this to showcase some utopian vision of AI curing all disease. It’s the practical use of technology we already possess. Our limitation isn’t the models; it’s the missing data.

A handful of companies have bet their trillion-dollar valuations on this: OpenAI, Google, Amazon, Nvidia, Apple, Oracle. They are spending hundreds of billions a year on AI infrastructure and need high-volume, high-quality datasets to justify that investment. Healthcare produces oceans of exactly that kind of data, and most of it evaporates. The companies that learn to capture and structure it will define the next layer of healthcare infrastructure. Whether they integrate with Epic, build around it, or replace it is almost secondary.

What matters is that none of them are waiting for Epic.

Clinicians won’t either. Once tools exist that unify the data hospitals already generate, reduce workload, eliminate administrative drag, and answer the questions clinicians actually ask — What happened? Why did it happen? What should we do now? — the center of gravity will shift. Clinicians will live inside those tools, not inside an interface built for billing.

Epic can still exist, but it doesn’t need to function as healthcare’s operating system. There’s precedent for this in every major industry: the core orchestration/data layer eventually recedes into the background while workflow and data intelligence move up the stack. At that point, the EHR becomes background infrastructure or middleware. The intelligence/workflow layer becomes the real operating system. Epic will undoubtedly resist this shift, yet its attempts to maintain total control of the clinician interface will ultimately collide with the utility and data gravity of AI-native systems.

Epic becomes the backend: essential, invisible, and no longer the place where the practice of medicine occurs.

Regulatory modernization around HIPAA, interoperability, and data liquidity will be essential, but that is a conversation for another essay.

Epic isn’t vanishing tomorrow. Large institutions rarely do. But its relevance is eroding in the only domain that will matter over the next decade: the ability to harness data at a scale and fidelity that makes AI transformative. It can keep its commandments, preserve its culture, and reject outside capital — it just can’t do all that and remain the central platform of hospital data in an AI-native future.

I know plenty of people who are politically right-of-center – and they want to rein in Big Insurance just as much as people to the left.

Some of my closest family and friends have nearly polar opposite political beliefs than mine. And these are not family members I’m only with on holidays (like during Thanksgiving dinner later this week) or friends I only see on Facebook. These are people I love and communicate with weekly — sometimes daily. They’re my people.

And I’d say that my people largely fall into two distinct right-of-center sub groups:

The first group:

USDA grass-fed Trump supporters who like Jeanine Pirro and Blue Lives Matter bumper stickers.

And the second group:

Nonpolitical and anti-establishment 20-30 somethings who make their own beef-tallow.

(And both groups are patient enough to keep a Bernie-t-shirt-owning-lib, who listens to The Daily (like myself) in their lives.)

We don’t all agree on vaccines. We don’t all agree on the Gulf of America. And none of them agree with my mullet. But what we all do agree on is that through backroom deals and moneyed influence, big corporations pull Washington’s levers and squeeze American families at every chance they get – all to make their Wall Street investors and executives richer. And, as readers of HEALTH CARE un-covered undoubtedly know, Big Insurance may be the perfect example of those deals and influence.

That’s where my people and I meet in our venn diagram. While we have many sticking points, Big Insurance is not one of them.

And this is not just qualitative on my end. Poll after poll proves that my people are not the exception to the rule. An October KFF poll showed that a majority of Republicans who align with the MAGA movement (57%) said Congress should have extended the enhanced premium tax credits for Affordable Care Act (ACA) plans, and a new study by Undue Medical Debt found that 62% of Republicans blame health insurance companies the most for the medical debt crisis in the country.

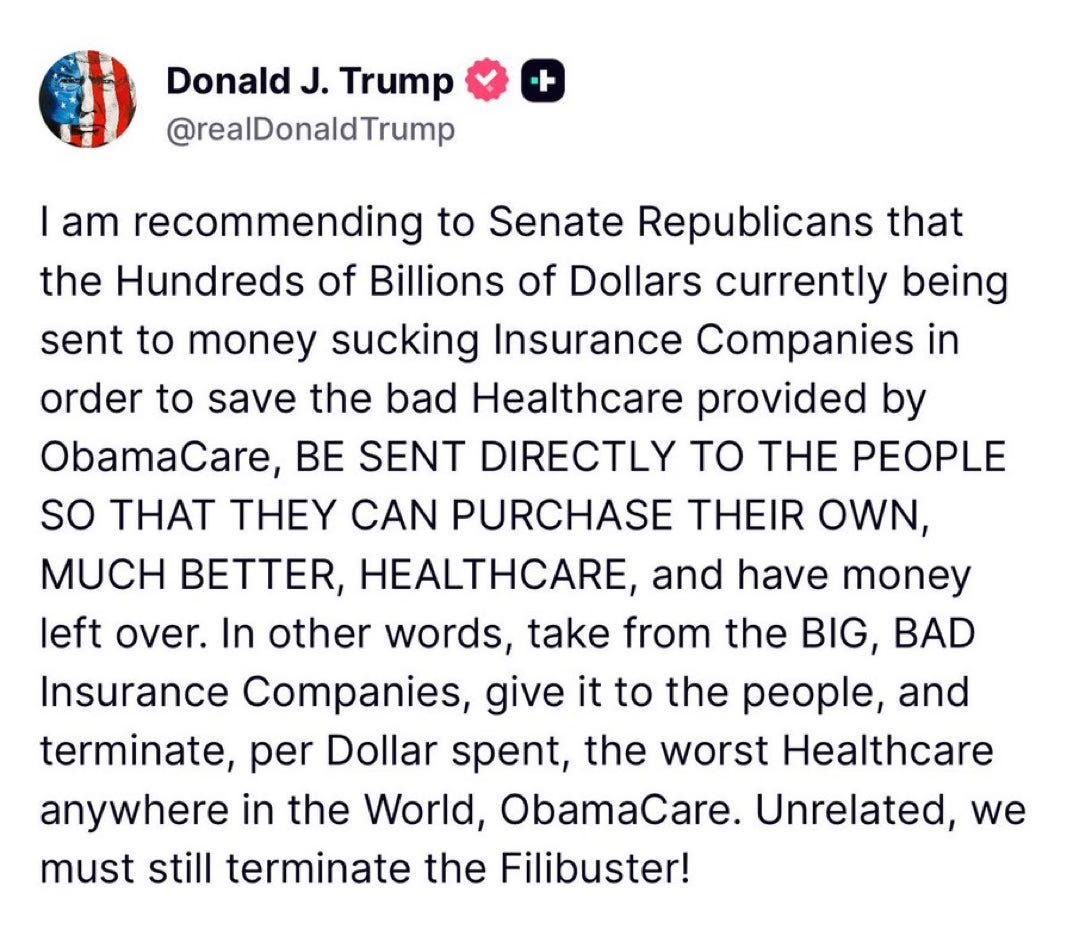

The deeds of the health insurance industry have grown so rotten and their stench so unavoidable that even the President has caught a whiff. On Truth Social last month, President Trump posted about “BIG,” “BAD” and “Money sucking” health insurance companies. His message reverberated in the media and on Wall Street and helped bring this issue even more to the forefront.

President Trump’s post on Truth Social attacking the health insurance industry.

But here’s the thing: Trump’s post isn’t the tip of the spear but rather the caboose following a long train of Republicans (and their voters) who as of late have begun to focus on Big Insurance. In the last six months, we’ve seen Representative Marjorie Taylor Green call on Republicans to take on Big Insurance, former Representative Mark Green (R-TN) introduce legislation to crack down on Big Insurance’s prior authorization tactics, and Pam Bondi’s Department of Justice open a criminal investigation into UnitedHealth Group’s Medicare Advantage business – all moves that have been historically uncharacteristic of their political bents but nonetheless are, in one way or another, raising the heat on Big Insurance.

If the latest news out of Washington tells us anything, it’s that conservatives are largely on the same side as many of the most liberal voices when it comes to health insurance reforms.

While my people may not speak the same health care language or advocate the exact same solutions that many health care reform advocates or left-of-center folks would raise, the differences are largely just in the terminology used. For instance, my people are not going to mention Medicare for All or a public option as an answer to our country’s health care woes. Those phrases have been carefully tarred and feathered by the insurance industry as “socialism” to hold back both centrist and Republican voters and policymakers from putting guardrails in place that would cut into the industry’s immense profits. But again, it’s the terminologies that have been discredited – not the sentiment behind them.

On more than one occasion, when talking with my people about health insurers, they have straight-up volunteered that they think “insurance companies should be outlawed.” That belief, last time I checked, was to the left of even Senators Elizabeth Warren and Bernie Sander’s proposals to finally establish universal coverage for every American by expanding Medicare to cover all of us.

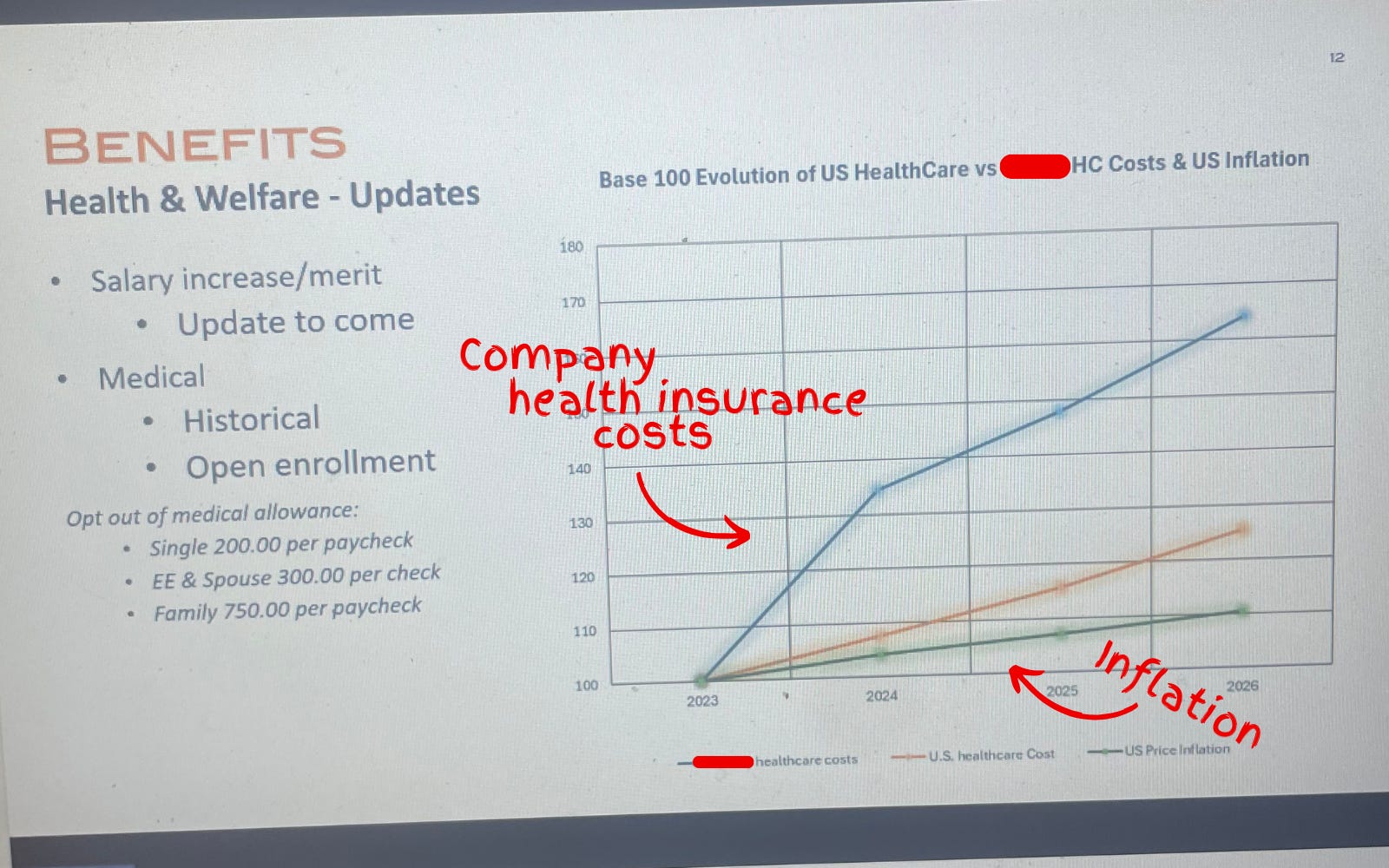

Another one of my people, who handles financials for the North American-sector of a sizable global company in the home-technology space, FaceTimed me last week to show me his computer screen while he was crunching the companies’ health care costs.

Photograph of a slide used during the company town hall showing the company’s health care costs vastly outpacing the rate of inflation.

In anticipation for a company-wide town hall, he had to make a slide showing that the health insurance costs for his company’s U.S.-side had increased (on average) 20% over the past several years – including a projected 25% jump in 2026. He couldn’t believe it. “Show this to Wendell,” he said.

And that’s the thing:

Nobody can believe how out-of-control Big Insurance has become.

Where my people and I meet

It’s fair to say that I think more about health care policy than the average bear. And it’s true that my people have had me in their ear talking about these issues for nearly a decade. But as I noted above, polling shows that while certain solutions may not be as popular, the desire for action is clear and exists sans my yapping.

Over years of conversations, there have been some major themes that have stuck. I will list them below:

Big Insurance is the villain in health care: With its army of slick lobbyists and spokesmen on TV, Big Insurance is the epitome of the D.C.-swamp monster that so many Americans disdain. Between 2014 and 2024, just seven for-profit health insurers amassed $543.4 billion in profits (of which they spent $618 million on lobbying during that time) all while 100 million Americans owe $220 billion in medical debt and Americans’ life expectancy is ranked 48th in the world.

Big Insurance and it’s cushy government handouts: Nearly all of Big Insurance’s growth has come from contracts it engineers with the federal and state governments in the form of managing Medicaid, Medicare Advantage and some Veteran health services. These contracts are not the invisible hand of the free market but rather cushy government handouts that have allowed just seven for-profit health insurance conglomerates to capture $10.192 trillion in revenues between 2014 and 2024.

Big Insurance has grown too big: Big Insurance companies are buying up the entire health care landscape – from physician practices to pharmacies. That is why independent physicians are an endangered species and why an independent pharmacy closes nearly every day in this country.

Big Insurance hurts the little guy: American small businesses often see double-digit yearly increases in health insurance costs that stifle Main Street America’s growth and stop Americans from being entrepreneurs altogether. And, not to mention, if businesses weren’t being raked over the coals for more premium dollars year after year, more money could be paid to workers.

I included this list because I think we are at a watershed moment in the health care debate and reforming Big Insurance is no longer a wedge issue. It’s a bridge issue.

I don’t know what comes next

Because the long standoff between Republicans and Democrats to open the government finally came to an end this month – without the ACA subsidy extensions – Big Insurance reform (and health care reform broadly) has become an unaddressed priority in American politics.

In the current moment, if Republican electeds were smart, they’d read the writing on the wall and focus on rooting out an actual source of widespread waste, fraud and abuse found in health insurance companies’ private Medicare Advantage, Medicaid and military businesses. That’s an issue that polls incredibly well with conservatives. Just tackling Medicare Advantage, for example, could save taxpayers somewhere between $80 and $140 billion annually.For reference, the DOGE website claims it has only clawed back $214 billion in total since January.

Republicans could also work with their political opposites (and fulfill a campaign promise) to pass a worthwhile health insurance reform package that builds on (or possibly replace) the consumer protections of ACA and fills the loopholes of well-intended rules that have been exploited and manipulated by Big Insurance.

And it wouldn’t be a one-party trick. For what it’s worth, I think most Democrats in Washington would be on board with anything that lessens the corporate grip Big Insurance has on our country’s public programs and improves the ACA. In the last year, we’ve already seen Democrats link with the country’s current controlling party to introduce bills that would bring meaningful change to Big Insurance:

Senators Elizabeth Warren (D-MA) and Josh Hawley (R-MO) introduced legislation that would stop health insurance companies from owning pharmacy benefit managers (PBMs);

Senators Jeff Merkley (D-OR) and Bill Cassidy, M.D. (R-LA) introduced the No UPCODE Act to curb taxpayer-sponsored overpayments to health insurers; and

These unlikely partnerships in Washington are happening because what my people (and all people) want is a health insurance system that guarantees comprehensive coverage for all of us, without forcing folks to choose between biopsies or groceries. Everybody I know – left, right and in between – wants a health care system that doesn’t bury families under mountains of medical bills or force them to attend unnecessary funerals. And all rational people want an insurance system that doesn’t buy off its buddies in Washington to serve their Wall Street daddies.

I want to scream from the mountaintops that health insurance reform is not just a moral or economic issue. It’s a winning issue.

Americans have had it. Most of Washington seems motivated. And now is the time for health care, patient and consumer advocates to change their tune and stop (just) preaching to the choir. Advocates for reform need to get their message to the corners of the country that they may have written off — or found too difficult to bridge — because the ground for health care reform is fertilefor change. And I think all people are ready.

Thanksgiving is in a few days. And in times of heightened political polarization, the dinner table – filled with folks sharing a myriad of different opinions – can become a battleground between courses of mashed potatoes and pumpkin pie. But if I can gleam anything from what I see as a bi-partisan kumbaya against Big Insurance, it’s that even with all the reported divisiveness, we have one less thing to argue about.

And because of that – I don’t know what comes next – but what I do know is that the 2026 midterms and the 2028 presidential election will be about health insurance reform. And whichever political party takes that seriously is going to seize the day.