As lawmakers debate ACA subsidy extensions and HSAs tied to banks and insurers, the public’s appetite for a health care overhaul is stronger than at any time since the 2020 Democratic primaries.

Washington is running out of hours to address the health care crisis of their own making. There are just 23 days before the Affordable Care Act’s (ACA) enhanced subsidies expire and congressional leaders are still trading barbs and floating half-baked ideas as millions of Americans brace for punishing premium spikes.

Meanwhile, the public has grown frustrated with both congressional dysfunction, and private health insurance companies that continue to raise premiums and out-of-pocket costs at a dizzying pace. According to new KFF data, 6 in 10 ACA enrollees already struggle to afford deductibles and co-pays, and most say they couldn’t absorb even a $300 annual increase without financial pain.

And even as Congress flails, Americans are coalescing around a solution party leaders rarely mention: Medicare for All.

A dramatic rebound in popularity

After Senator Bernie Sanders bowed out of the presidential race in April 2020, Medicare for All faded to the background following political infighting, industry fearmongering and the lack of a national champion. But nearly six years later, the proposed policy solution has re-emerged as a top choice among frustrated voters.

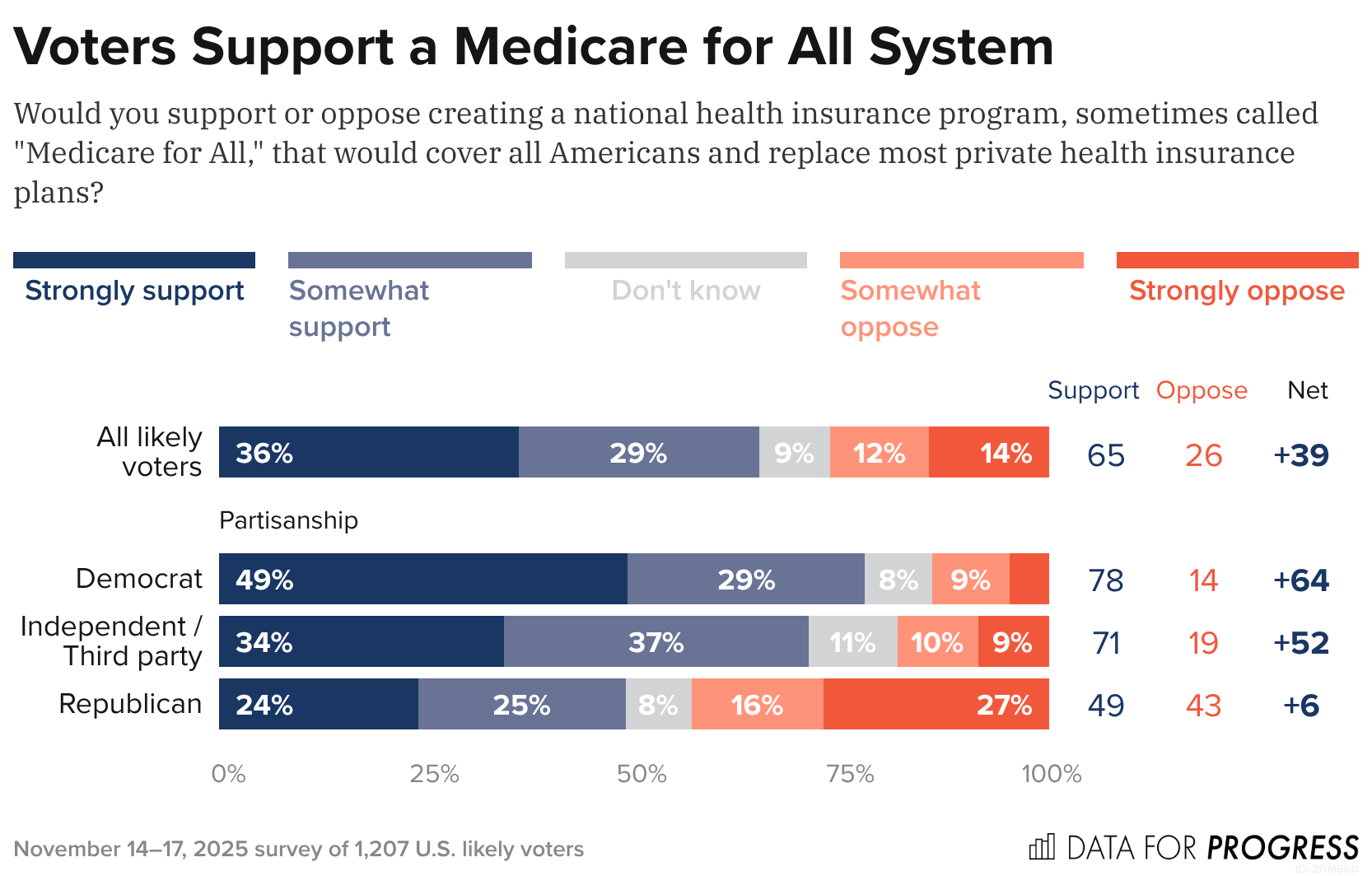

A new Data for Progress poll found that65% of likely voters (including 71% of independents and nearly half of Republicans) support creating a national health insurance program that would replace most private plans. What’s notable is that the poll shows that support barely budges – holding at 63% – even when voters are told Medicare for All would eliminate private insurance and replace premiums with taxes, a dramatic shift from years past when just 13% supported such a plan under those conditions.

The KFF poll shows that ACA enrollees lack confidence that President Trump or congressional Republicans will handle the crisis, with almost half of ACA enrollees saying a $1,000 cost spike would “majorly impact” their vote in 2026. Morethan half of ACA enrollees are in Republican congressional districts, which explains why Republicans representing swing districts are desperately trying to persuade their Republican colleagues — so far without success — to extend the subsidies.

Of course, Medicare for All still faces steep odds in Congress. Industry opposition remains powerful, Democrats are divided and Republicans are openly hostile. But the polling shift is significant and suggests the political terrain is changing faster than Washington is acknowledging — and that voters, squeezed by soaring premiums and dwindling subsidies, are being nudged toward policies previously attacked as too ambitious to pass.

And against this backdrop, Medicare for All’s revival feels less like a left-wing wet dream and more like a window into the public’s thinning patience. Americans are looking past the Affordable Care Act’s limits and past Big Insurance’s promises – and towards a solution that decouples Americans health from profit-hungry, Wall Street-driven corporate monsters. While Washington has met this moment with inaction, Americans seem ready to act.

The software monopoly that powers American hospitals wasn’t built for the data, speed, or intelligence the future of medicine demands.

Epic Systems is an American privately held healthcare software company, founded by Judy Faulkner in 1979, and has grown into the largest electronic health record (EHR) vendor by market share, covering over half of all hospital patients in the U.S.

Epic dominates American healthcare today. But so did Kodak in photography and GE in industry. Its software runs the country’s hospitals, determines the workflows clinicians, nurses and clinical support staff use, and shapes what data gets captured (or more often, what gets lost). It also serves as the front door for healthcare data for the patients it serves. Dominance has never guaranteed a future. Epic’s position reflects the architecture of the past, not the one emerging now.

More importantly, the sheer volume of activity occurring in these hospitals means they are collectively running thousands of experiments, mini clinical trials, and critical observations daily. The stakes are enormous: billions of dollars in drug discovery, the efficiency of clinical trials (currently plagued by poor recruitment and high costs), and the potential for better, personalized care. The data generated in these environments is the single most valuable, untapped resource in all of medicine.

However, this monumental source of value is being throttled by outdated infrastructure, and it shows. It’s hard to imagine a world where AI is used to its full potential in healthcare while Epic is still running the show. The ideas are oppositional at their core.

The Massive Data Problem

Technology is accelerating faster than any legacy system can keep up with. AI is reshaping every major industry, and healthcare will be forced to catch up. However, this essential transformation is structurally incompatible with the dominant system of record.

To put it bluntly: Epic has a data problem. A massive data problem. Not just imperfect data — structurally flawed data. What Epic captures is fragmented, delayed, and riddled with inconsistencies. Diagnoses become billing codes that distort reality. Interventions like intubations, pressor starts, and ventilator changes appear hours late, if at all. Outcomes are incomplete or missing. What remains isn’t a clinical record in any meaningful sense but a billing ledger dressed up as documentation. No model can learn reliably from that.

But the deeper problem is the data Epic never sees. Some of the most valuable information in modern medicine: continuous monitoring streams, ventilator logs, infusion pump data… never enters the EHR in a structured or analyzable form. In many cases, it isn’t captured at all.

I recently brought Roon (a well-known engineer at OpenAI) and Richard Hanania(a public intellectual/cultural critic)—both advisors in my new venture, in full disclosure—to one of the largest academic medical centers in the country. Both watched torrents of millisecond-scale data spill off monitors. Streams that could reveal what’s happening in the brain, heart, and vasculature. Valuable data… all vanished instantly. None of it logged. None of it stored. None of it correlated with outcomes. Roon captured this shock in a viral post on X/Twitter, essentially describing how hospitals are filled with catastrophic events like sudden cardiac death, yet we save none of the time-series data that could teach us how to prevent the next one. His shock distilled what people in technology grasp immediately and what healthcare has normalized: industries where human life isn’t exactly top of mind record everything; hospitals, where the stakes are life and death, learn almost nothing from themselves.

In Silicon Valley, losing data like this is unthinkable. In healthcare, it barely registers.

Epic was never built to ingest or learn from this scale of data. It was built to satisfy billing requirements, regulatory checklists, and documentation workflows. That is the beginning and end of its architecture. It is not a learning system, much less an AI system. It is not even a modern data system. And that is the root of Epic’s downfall.

The Cultural and Financial Moat

Epic is famous for its internal commandments — principles Judy Faulkner wrote decades ago:

Do not acquire.

Do not be acquired.

Do not raise outside capital.

(If you haven’t heard it, the latest Acquired podcast episode on Epic is essential listening)

But the same rules that built its empire now limit what it can become. What was once a strategic strength is now its ceiling.

The next era of healthcare software demands investments that were unnecessary when the EHR was the center of gravity. Building AI-native infrastructure: real-time data pipelines, device integrations, large-scale compute, continuous model training, semantic normalization — requires not millions but tens of billions of dollars. Most companies facing that kind of leap can raise capital, acquire talent, or merge with partners. Epic has ruled all of those options out.

Epic’s formidable market share is anchored by a massive customer sunk cost. With implementation fees often exceeding a billion dollars for large systems, the financial and political inertia makes replacing the EHR functionally unthinkable. However, this commitment only forces customers to defend an obsolete data architecture. By preventing them from adopting novel solutions, this inertia doesn’t protect Epic’s long-term viability, it simply guarantees a widening technical gap between the EHR and the transformative potential of AI.

A company optimized for slow, controlled expansion cannot transform itself into an AI-scale enterprise without violating the principles that define it. The culture that kept Epic dominant is the culture that prevents it from catching the next wave. Epic will continue to excel at documentation, billing, and compliance — but those strengths are anchored in the past. The future belongs to systems that learn, and Epic was never designed to learn.

The Shift to Middleware

Meanwhile, the broader economy is being held up by AI. The world’s largest tech companies are pouring staggering sums into compute, data centers, and model training. And all that compute needs rich, complex, high-value data to train on.

Healthcare is the only remaining frontier of that scale.

No other industry generates so much information while analyzing so little of it. No other sector represents nearly 20% of U.S. GDP yet still runs on fragmented workflows and manual processes. And the incentives here are unmatched: improving patient outcomes, reducing costs, eliminating inefficiency, accelerating drug development, modeling disease trajectories, and eventually automating the more repetitive layers of care. There’s even an irony: the very infrastructure needed to enable learning health systems would also finally make billing more accurate.

I’m not writing this to showcase some utopian vision of AI curing all disease. It’s the practical use of technology we already possess. Our limitation isn’t the models; it’s the missing data.

A handful of companies have bet their trillion-dollar valuations on this: OpenAI, Google, Amazon, Nvidia, Apple, Oracle. They are spending hundreds of billions a year on AI infrastructure and need high-volume, high-quality datasets to justify that investment. Healthcare produces oceans of exactly that kind of data, and most of it evaporates. The companies that learn to capture and structure it will define the next layer of healthcare infrastructure. Whether they integrate with Epic, build around it, or replace it is almost secondary.

What matters is that none of them are waiting for Epic.

Clinicians won’t either. Once tools exist that unify the data hospitals already generate, reduce workload, eliminate administrative drag, and answer the questions clinicians actually ask — What happened? Why did it happen? What should we do now? — the center of gravity will shift. Clinicians will live inside those tools, not inside an interface built for billing.

Epic can still exist, but it doesn’t need to function as healthcare’s operating system. There’s precedent for this in every major industry: the core orchestration/data layer eventually recedes into the background while workflow and data intelligence move up the stack. At that point, the EHR becomes background infrastructure or middleware. The intelligence/workflow layer becomes the real operating system. Epic will undoubtedly resist this shift, yet its attempts to maintain total control of the clinician interface will ultimately collide with the utility and data gravity of AI-native systems.

Epic becomes the backend: essential, invisible, and no longer the place where the practice of medicine occurs.

Regulatory modernization around HIPAA, interoperability, and data liquidity will be essential, but that is a conversation for another essay.

Epic isn’t vanishing tomorrow. Large institutions rarely do. But its relevance is eroding in the only domain that will matter over the next decade: the ability to harness data at a scale and fidelity that makes AI transformative. It can keep its commandments, preserve its culture, and reject outside capital — it just can’t do all that and remain the central platform of hospital data in an AI-native future.

I know plenty of people who are politically right-of-center – and they want to rein in Big Insurance just as much as people to the left.

Some of my closest family and friends have nearly polar opposite political beliefs than mine. And these are not family members I’m only with on holidays (like during Thanksgiving dinner later this week) or friends I only see on Facebook. These are people I love and communicate with weekly — sometimes daily. They’re my people.

And I’d say that my people largely fall into two distinct right-of-center sub groups:

The first group:

USDA grass-fed Trump supporters who like Jeanine Pirro and Blue Lives Matter bumper stickers.

And the second group:

Nonpolitical and anti-establishment 20-30 somethings who make their own beef-tallow.

(And both groups are patient enough to keep a Bernie-t-shirt-owning-lib, who listens to The Daily (like myself) in their lives.)

We don’t all agree on vaccines. We don’t all agree on the Gulf of America. And none of them agree with my mullet. But what we all do agree on is that through backroom deals and moneyed influence, big corporations pull Washington’s levers and squeeze American families at every chance they get – all to make their Wall Street investors and executives richer. And, as readers of HEALTH CARE un-covered undoubtedly know, Big Insurance may be the perfect example of those deals and influence.

That’s where my people and I meet in our venn diagram. While we have many sticking points, Big Insurance is not one of them.

And this is not just qualitative on my end. Poll after poll proves that my people are not the exception to the rule. An October KFF poll showed that a majority of Republicans who align with the MAGA movement (57%) said Congress should have extended the enhanced premium tax credits for Affordable Care Act (ACA) plans, and a new study by Undue Medical Debt found that 62% of Republicans blame health insurance companies the most for the medical debt crisis in the country.

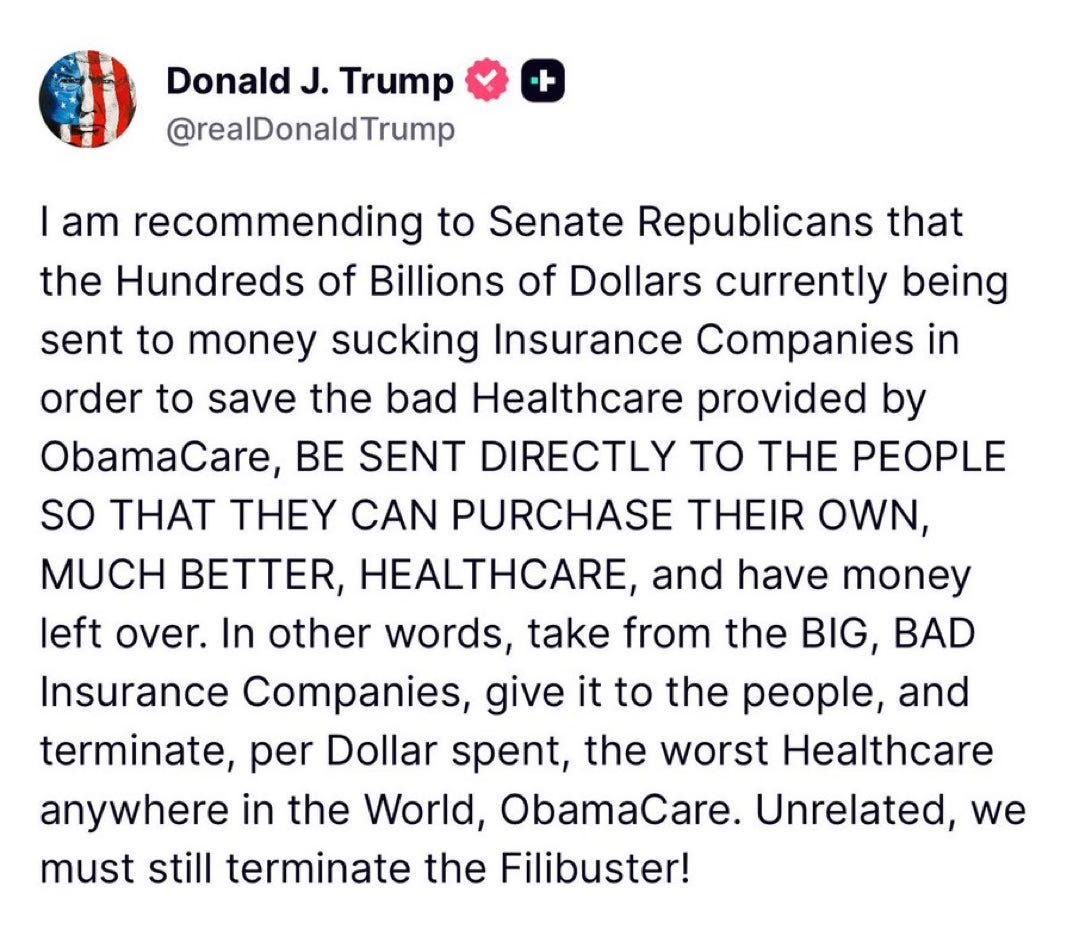

The deeds of the health insurance industry have grown so rotten and their stench so unavoidable that even the President has caught a whiff. On Truth Social last month, President Trump posted about “BIG,” “BAD” and “Money sucking” health insurance companies. His message reverberated in the media and on Wall Street and helped bring this issue even more to the forefront.

President Trump’s post on Truth Social attacking the health insurance industry.

But here’s the thing: Trump’s post isn’t the tip of the spear but rather the caboose following a long train of Republicans (and their voters) who as of late have begun to focus on Big Insurance. In the last six months, we’ve seen Representative Marjorie Taylor Green call on Republicans to take on Big Insurance, former Representative Mark Green (R-TN) introduce legislation to crack down on Big Insurance’s prior authorization tactics, and Pam Bondi’s Department of Justice open a criminal investigation into UnitedHealth Group’s Medicare Advantage business – all moves that have been historically uncharacteristic of their political bents but nonetheless are, in one way or another, raising the heat on Big Insurance.

If the latest news out of Washington tells us anything, it’s that conservatives are largely on the same side as many of the most liberal voices when it comes to health insurance reforms.

While my people may not speak the same health care language or advocate the exact same solutions that many health care reform advocates or left-of-center folks would raise, the differences are largely just in the terminology used. For instance, my people are not going to mention Medicare for All or a public option as an answer to our country’s health care woes. Those phrases have been carefully tarred and feathered by the insurance industry as “socialism” to hold back both centrist and Republican voters and policymakers from putting guardrails in place that would cut into the industry’s immense profits. But again, it’s the terminologies that have been discredited – not the sentiment behind them.

On more than one occasion, when talking with my people about health insurers, they have straight-up volunteered that they think “insurance companies should be outlawed.” That belief, last time I checked, was to the left of even Senators Elizabeth Warren and Bernie Sander’s proposals to finally establish universal coverage for every American by expanding Medicare to cover all of us.

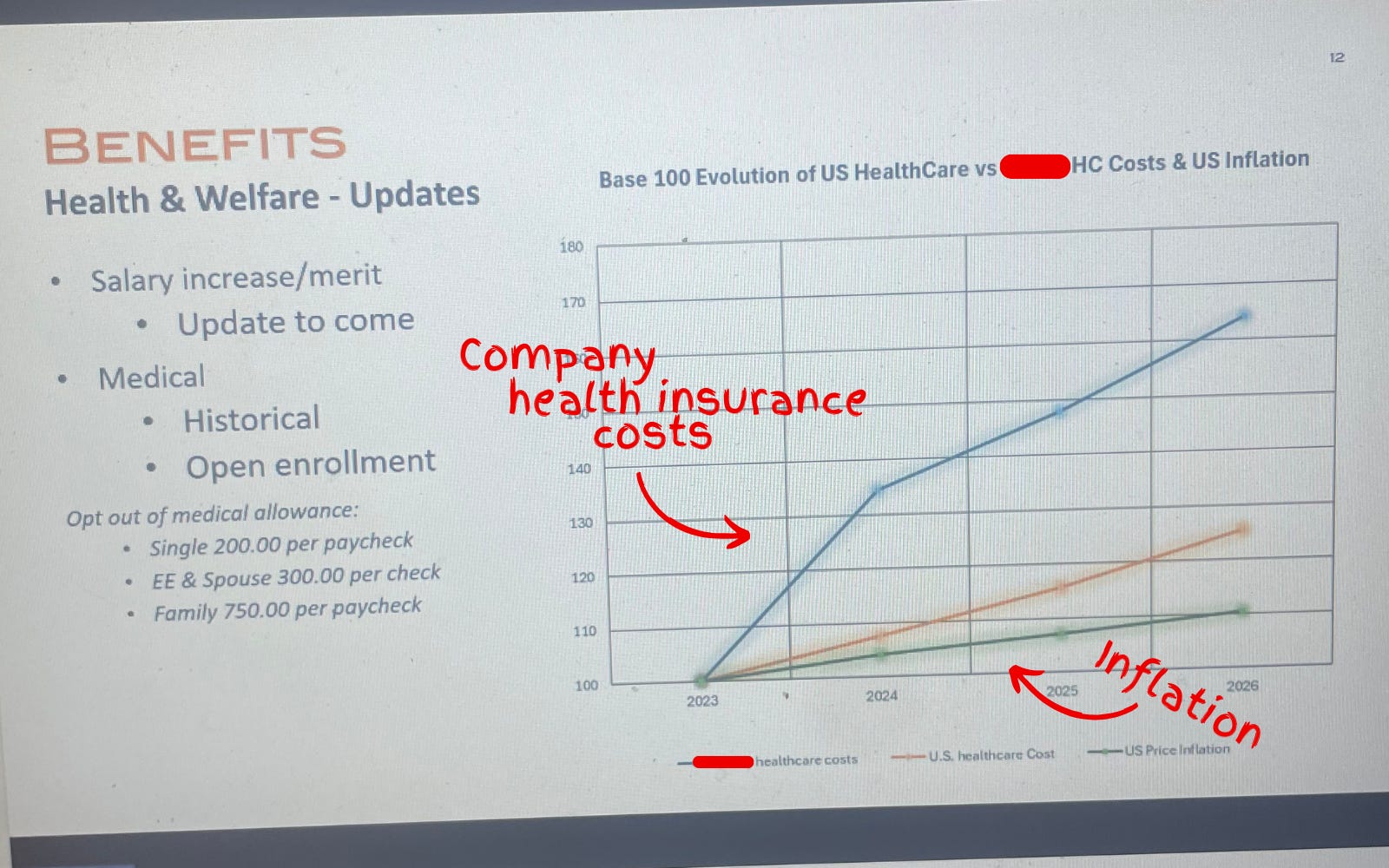

Another one of my people, who handles financials for the North American-sector of a sizable global company in the home-technology space, FaceTimed me last week to show me his computer screen while he was crunching the companies’ health care costs.

Photograph of a slide used during the company town hall showing the company’s health care costs vastly outpacing the rate of inflation.

In anticipation for a company-wide town hall, he had to make a slide showing that the health insurance costs for his company’s U.S.-side had increased (on average) 20% over the past several years – including a projected 25% jump in 2026. He couldn’t believe it. “Show this to Wendell,” he said.

And that’s the thing:

Nobody can believe how out-of-control Big Insurance has become.

Where my people and I meet

It’s fair to say that I think more about health care policy than the average bear. And it’s true that my people have had me in their ear talking about these issues for nearly a decade. But as I noted above, polling shows that while certain solutions may not be as popular, the desire for action is clear and exists sans my yapping.

Over years of conversations, there have been some major themes that have stuck. I will list them below:

Big Insurance is the villain in health care: With its army of slick lobbyists and spokesmen on TV, Big Insurance is the epitome of the D.C.-swamp monster that so many Americans disdain. Between 2014 and 2024, just seven for-profit health insurers amassed $543.4 billion in profits (of which they spent $618 million on lobbying during that time) all while 100 million Americans owe $220 billion in medical debt and Americans’ life expectancy is ranked 48th in the world.

Big Insurance and it’s cushy government handouts: Nearly all of Big Insurance’s growth has come from contracts it engineers with the federal and state governments in the form of managing Medicaid, Medicare Advantage and some Veteran health services. These contracts are not the invisible hand of the free market but rather cushy government handouts that have allowed just seven for-profit health insurance conglomerates to capture $10.192 trillion in revenues between 2014 and 2024.

Big Insurance has grown too big: Big Insurance companies are buying up the entire health care landscape – from physician practices to pharmacies. That is why independent physicians are an endangered species and why an independent pharmacy closes nearly every day in this country.

Big Insurance hurts the little guy: American small businesses often see double-digit yearly increases in health insurance costs that stifle Main Street America’s growth and stop Americans from being entrepreneurs altogether. And, not to mention, if businesses weren’t being raked over the coals for more premium dollars year after year, more money could be paid to workers.

I included this list because I think we are at a watershed moment in the health care debate and reforming Big Insurance is no longer a wedge issue. It’s a bridge issue.

I don’t know what comes next

Because the long standoff between Republicans and Democrats to open the government finally came to an end this month – without the ACA subsidy extensions – Big Insurance reform (and health care reform broadly) has become an unaddressed priority in American politics.

In the current moment, if Republican electeds were smart, they’d read the writing on the wall and focus on rooting out an actual source of widespread waste, fraud and abuse found in health insurance companies’ private Medicare Advantage, Medicaid and military businesses. That’s an issue that polls incredibly well with conservatives. Just tackling Medicare Advantage, for example, could save taxpayers somewhere between $80 and $140 billion annually.For reference, the DOGE website claims it has only clawed back $214 billion in total since January.

Republicans could also work with their political opposites (and fulfill a campaign promise) to pass a worthwhile health insurance reform package that builds on (or possibly replace) the consumer protections of ACA and fills the loopholes of well-intended rules that have been exploited and manipulated by Big Insurance.

And it wouldn’t be a one-party trick. For what it’s worth, I think most Democrats in Washington would be on board with anything that lessens the corporate grip Big Insurance has on our country’s public programs and improves the ACA. In the last year, we’ve already seen Democrats link with the country’s current controlling party to introduce bills that would bring meaningful change to Big Insurance:

Senators Elizabeth Warren (D-MA) and Josh Hawley (R-MO) introduced legislation that would stop health insurance companies from owning pharmacy benefit managers (PBMs);

Senators Jeff Merkley (D-OR) and Bill Cassidy, M.D. (R-LA) introduced the No UPCODE Act to curb taxpayer-sponsored overpayments to health insurers; and

These unlikely partnerships in Washington are happening because what my people (and all people) want is a health insurance system that guarantees comprehensive coverage for all of us, without forcing folks to choose between biopsies or groceries. Everybody I know – left, right and in between – wants a health care system that doesn’t bury families under mountains of medical bills or force them to attend unnecessary funerals. And all rational people want an insurance system that doesn’t buy off its buddies in Washington to serve their Wall Street daddies.

I want to scream from the mountaintops that health insurance reform is not just a moral or economic issue. It’s a winning issue.

Americans have had it. Most of Washington seems motivated. And now is the time for health care, patient and consumer advocates to change their tune and stop (just) preaching to the choir. Advocates for reform need to get their message to the corners of the country that they may have written off — or found too difficult to bridge — because the ground for health care reform is fertilefor change. And I think all people are ready.

Thanksgiving is in a few days. And in times of heightened political polarization, the dinner table – filled with folks sharing a myriad of different opinions – can become a battleground between courses of mashed potatoes and pumpkin pie. But if I can gleam anything from what I see as a bi-partisan kumbaya against Big Insurance, it’s that even with all the reported divisiveness, we have one less thing to argue about.

And because of that – I don’t know what comes next – but what I do know is that the 2026 midterms and the 2028 presidential election will be about health insurance reform. And whichever political party takes that seriously is going to seize the day.

The Trump administration is shaking up how health systems are paid for outpatient care with a plan that could reduce Medicare hospital spending by nearly $11 billion over the next decade.

Why it matters:

It’s a big step forward for “site-neutral” payment policies that have been touted as a way to save taxpayers and patients money, but that hospitals say will lead to service cuts, especially in rural areas.

Driving the news:

Medicare administrators on Friday finalized a proposal to reduce what the government pays hospitals to administer outpatient drugs, including chemotherapy, at off-campus sites.

The move would equalize payment rates to hospitals and physician practices for the same services — an idea that Congress debated last year but didn’t act on in the face of aggressive hospital lobbying.

Medicare now pays about $341 for chemotherapy administration in hospital outpatient facilities, compared with $119 for the same service delivered in a doctor’s office.

Medicare next year will also start to phase out a list of more than 1,700 procedures and services only covered when they’re delivered in an inpatient setting.

What they’re saying:

The policy changes will give seniors more choices on where to get a procedure and potentially lower out-of-pocket costs at an outpatient site, the Centers for Medicare and Medicaid Services said.

Some health policy experts said the change will help make Medicare more affordable.

“We hope the administration will continue its efforts and adopt site neutrality for other services in future rules,” Mark Miller, executive vice president of health care at Arnold Ventures, said in a statement.

The other side:

“Both policies ignore the important differences between hospital outpatient departments and other sites of care,” Ashley Thompson, a senior vice president at the American Hospital Association, said in a statement.

“The reality is that hospital outpatient departments serve Medicare patients who are sicker, more clinically complex, and more often disabled or residing in rural or low-income areas than the patients seen in independent physician offices.”

Hospital outpatient departments still will see an $8 billion overall increase in their Medicare payments in 2026.

But the Trump administration contends that new technologies and other factors are shortening recovery times for procedures done on an outpatient basis.

Between the lines:

Health systems still scored a small win when CMS dropped a plan to speed up the repayment of $7.8 billion in improper cuts the first Trump administration made to safety-net providers’ reimbursements in the federal discount drug program.

The policy would have clawed back the money from hospitals’ Medicare reimbursements. Scrapping the idea “helps preserve critical resources for patient care during an already challenging time,” Soumi Saha, senior vice president of government affairs at Premier, said in a statement.

Still, CMS said it may try again in 2027. And law firm Hooper Lundy Bookman is already sending out feelers to hospitals willing to challenge the version of the repayment plan that will go into effect next year, per an alert sent Friday night.

What we’re watching:

Whether health systems challenge the site-neutral payment changes. The hospital payment plan came weeks later than expected and will make it harder for facilities to update billing, revise their budgets and train staff, Saha said.

The administration is also launching a survey of hospitals’ outpatient drug acquisition costs next year, which is seen as a prelude for cutting reimbursements under the discount drug program.

Harvard psychologists Daniel Simons and Christopher Chabris ran a now-famous experiment in the late 1990s. They showed students a short video of six people passing basketballs and told them to count the number of passes made by the three players in white.

Halfway through the film, a person in a gorilla suit walks into the frame, beats its chest and exits. Amazingly, half of viewers — both then and in multiple recreations of the study — never notice the gorilla. They’re so focused on counting passes that they miss the obvious event happening right in front of them.

The authors call this “inattentional blindness.” And you don’t need to visit a research lab to see it. It’s everywhere in American healthcare.

Policymakers, business leaders and medical societies are all busy counting their own pass equivalents: metrics like insurance subsidies, premiums and enrollment numbers.

As a country, we need to stop counting passes long enough to observe how the gorilla negatively affects people everywhere: in Washington, in boardrooms, in workplaces and in rural communities. Only then can we confront the gorilla head on.

1. The gorilla in Washington

In Congress, lawmakers spent 43 days debating how to reopen the government. The fight centered on whether to continue funding the enhanced premium tax credits that have made coverage more affordable for roughly 20 million lower-income Americans who purchase health insurance through the Affordable Care Act’s online exchanges.

Democrats argued that ending those payments in 2026 would cause premiums to spike and make care unaffordable. Republicans warned that continuing them would add nearly $400 billion to the federal deficit over the next decade. Both believed they were protecting Americans from financial harm. And both were right. If the cost of providing medical care isn’t reduced, neither the federal government nor the average family will be able to afford it.

The United States spends $14,885 per person each year on medical care while the next highest-paying nation, Switzerland, spends $9,963 per person with far better clinical outcomes, according to the Peterson Center, .

If the U.S. could cut the spending gap between American and Swiss healthcare in half, our nation would save $700 billion annually. Those savings could help maintain ACA subsidies, lower out-of-pocket costs for families and reduce federal deficits.

But the gorilla inflicts financial damage far beyond just the ACA exchanges. Between federal funding cuts and eligibility changes, analysts warn that millions of Americans enrolled in Medicaid will become uninsured starting in 2026. Meanwhile, because federal law limits Medicare payment growth to the rate of inflation, hospitals make up lost revenue by charging private insurers and their enrollees more (already about 250% of Medicare rates). Ultimately, employers and workers will pay the price.

2. The gorilla in corporate America

America’s C-suite leaders are conducting the business equivalent of counting passes. Instead of confronting the cost of medical care itself, they’re focused on comparing premiums, raising deductibles and choosing plans with narrower physician networks.

But without major changes in how care is delivered, no plan will remain affordable.

The average cost of family health coverage premiums will approach $30,000 next year, with employers paying about $24,000 and workers responsible for the rest, according to an October KFF survey of 1,862 non-federal public and private firms. A projected 9% premium increase means employers and employees together will spend roughly $2,500 more next year per worker — limiting wage growth, hiring and investments in innovation.

America doesn’t have an insurance problem. It has a medical cost crisis.

3. The gorilla in the workplace

While workers focus on wages, benefits and job security, the same cost crisis threatening businesses and government is about to hit them hard.

More than half of U.S. adults receive health insurance through an employer. But as medical costs rise, companies are turning to automation and generative AI to reduce their expenses.

Amazon offers a vivid example: the company eliminated 14,000 office and professional roles and announced plans to combine robotics with generative AI to replace as many as three-quarters of its warehouse workforce. The company plans to create new, higher-skill jobs to maintain the robots, but far fewer (and not for the same people who were displaced).

When workers lose employer-based insurance, they don’t stop getting sick. They turn to Medicaid or subsidized exchange plans. That strains government budgets, lowers hospital reimbursements and pushes insurers to raise commercial premiums even higher.

Unless the cost of medical care drops dramatically, the gorilla’s impact will reverberate throughout society.

4. The gorilla in rural hospitals

The cost crisis is devastating people everywhere, but perhaps nowhere more than in rural America. Over the past two decades, 150 rural hospitals have closed or stopped offering inpatient services. Another 700 facilities (nearly one-third of those remaining) are at risk of shutting down.

With small patient populations and high fixed costs, many rural hospitals can no longer provide inpatient care. But instead of reducing the high cost of care delivery, most communities pursue short-term relief: emergency grants, temporary bailouts and added Congressional funding.

These efforts can delay closure, but they don’t change the math. Even when hospital beds are empty, the buildings must be staffed, heated, insured and maintained, turning every day into a financial loss.

To survive, the model will have to change, and painful sacrifices will be necessary.

Addressing the gorilla everywhere

The United States can dramatically reduce healthcare spending while improving quality. But doing so will require a structural overhaul, not incremental tweaks. Three major opportunities already exist.

1. Shrink our hospital footprint

America maintains far more hospitals than it needs, with many offering duplicate services at high fixed costs. A more sustainable system would:

Eliminate overlapping specialty programs in crowded markets.

Small rural hospitals could transition into 24-hour emergency and urgent-care hubs supported by telemedicine and reliable, low-cost transportation to larger facilities.

2. Prevent diseases before they happen

According to the CDC, more effective control of chronic diseases would reduce medical costs up to $1.8 trillion by preventing as many as half of all heart attacks, strokes, cancers and kidney failures. Three pragmatic opportunities include:

Every complication avoided is a hospital admission, ICU stay or surgery that never happens and is never billed.

Pay for value, not volume

Healthcare’s fee-for-service payment system rewards doing more, not doing better. Capitation — fixed monthly payments to physician groups and hospitals — flips the incentive structure, rewarding improved health, not just disease treatment.

Under capitation, prevention becomes financially rewarded, chronic diseases are managed earlier and more effectively, and care shifts to high-quality, cost-efficient settings, including outpatient facilities and virtual platforms.

The result is a virtuous cycle: healthier patients, fewer complications and significantly lower cost.

No single group — government, employers, patients or clinicians — can solve this crisis alone. Success will require all stakeholders to overcome their inattentional blindness and confront the gorilla together. The only question is how much worse things must become before we do.

A Florida retirement haven is thrown into chaos as a $360 million Medicare overbilling scandal and a Humana–UnitedHealth standoff leave seniors scrambling to keep their doctors.

Behind the gates of The Villages (the pastel Shangri-La of Florida retirement lore) is a place where American seniors zoom around on golf carts like 1977 Thunderbirds and keep wrist stabilizers on the ready for impromptu pickleball matches. It’s a community built on the promise that retirement is a time for sunshine, camaraderie and — most importantly — a health system that doesn’t leave you out in the cold.

HEALTH CARE un-covered has published stories about The Villages in the past – and how the retirement community is rife with Medicare Advantage shenanigans. And today, many Villagers have been blindsided by these shenanigans like they’re part of a Big Insurance hostage crisis straight out of an episode of Days of Our Lives or General Hospital.

A TVH / UnitedHealth dispute leaving seniors “duped”

Earlier this year, The Villages Health (TVH) — the health system serving more than 55,000 retirees — promised a smooth handoff as it prepared to sell itself to CenterWell, Humana’s senior-focused primary-care chain. TVH’s CEO assured residents that “no change in care” was coming, according to News 6.

But then came the bankruptcy filing. And then the revelation that TVH owed more than $360 million to the federal government for “Medicare overbilling.” And then the sale. And, according to Village-News, then a bankruptcy judge confirming that, yes, TVH was indeed being swallowed by CenterWell for $68 million.

In other words: the health care version of a soap-opera plot twist. Only with fewer glamorous outfits and more Chapter 11 filings.

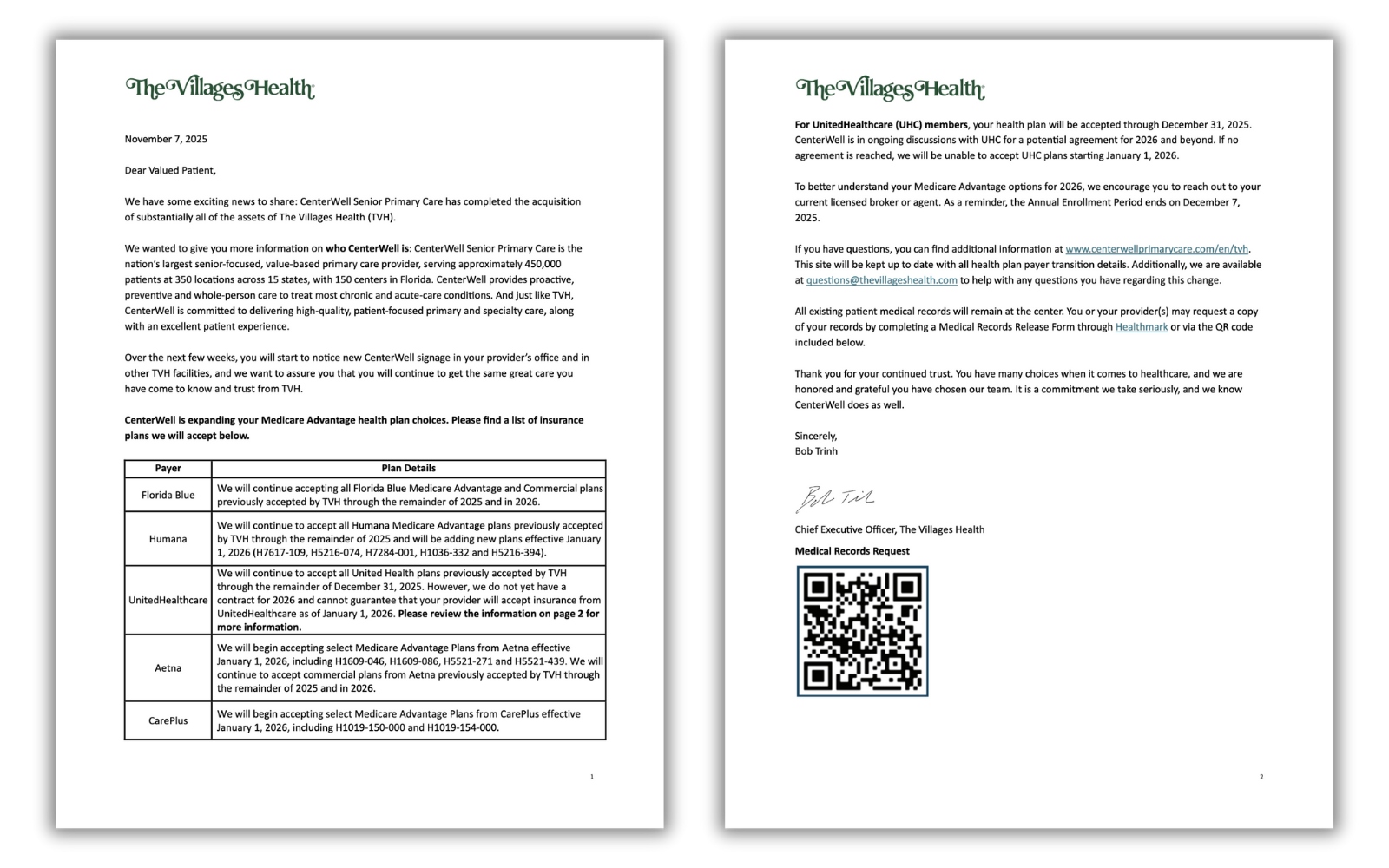

On November 7, the very day the sale of TVH closed, patients received a message warning them that their UnitedHealthcare Medicare Advantage plan — the plan they were nudged toward back in 2016 when TVH tried to push all patients into UnitedHealth’s grasp — might not be accepted after Dec. 31, 2025. If negotiations fail, residents must switch doctors or switch insurers.

Message from The Villages Health to their “Valued Patient(s)”.

“Not to be notified until basically the last minute that there isn’t a contract between CenterWell and United at this time is very alarming,” Villager Phyllis McElveen told Spectrum News. “We had already gone out and selected our UnitedHealthcare plan for 2026. We had already done everything. And now to know we might have to make a change is just not a pleasant feeling.”

At The Villages, you can imagine that picking the right Medicare plan is akin to competitive sport — one step removed from a pickleball tournament. The residents do their homework and many reportedly attend “Medicare prep presentations.” So for Villagers, being blindsided is a big deal.

Longtime patient Nancy Devlin told News 6 that she dug through Humana’s and Aetna’s plans to find a plan that might allow her to stay with the physicians she’s seen for six years. But for Devlin, her digging was to no avail. None of the plans matched what she currently had with UnitedHealthcare. Not the same covered medications. Not the same premiums. Not the same out-of-pocket costs. Not the same networks.

“They duped us,” she said. “It’s more expensive and doesn’t have my medications, or I have to pay for them, and I don’t pay for my medications now.”

For retirees on limited incomes, doubling drug costs is a gut punch that can mean one less trip to visit their grandkids or postponing that cruise to the Bahamas. Or for some, putting enough food on the table.

A deal gone sour

To understand how this crisis happened, go back to 2016, when TVH urged residents to switch into UnitedHealthcare Medicare Advantage or lose access to their doctors. Fast-forward to today. TVH is bankrupt, Humana now owns the centers, and UnitedHealth, the world’s largest health conglomerate (and the once-preferred partner for Villagers) is persona non grata unless a deal is reached.

The timing could not be worse. Open enrollment ends December 7, which means that tens of thousands of retirees have just around two weeks to decide whether to switch insurers or switch doctors.

What’s happening here is not simply a contract negotiation gone awry, but a symptom of something deeper. TVH didn’t just owe “some money” to Medicare. It owed about $360 million because of what Humana and The Villages described as a gigantic “Medicare coding error.”

UnitedHealthcare, in turn, accused The Villages’ controlling Morse family of quietly pulling out $183 million between 2022 and 2024 – funds UnitedHealth argued were siphoned off just before the bankruptcy filing.

If that allegation sounds familiar, it’s because we’ve seen versions of this story across the health care industry: private companies treating Medicare Advantage plans like piñatas stuffed with taxpayer dollars. Sometimes, the bat misses the piñata and smacks a whole village of seniors.

Here’s what happens next

The Villages, for all its mid-century charm and retirement-resort quirks, is a microcosm of a national problem that Medicare Advantage is, too often, run for Big Insurance’s advantage with seniors just an afterthought. Corporate acquisitions, bankruptcies, risk-coding schemes, contract disputes and Wall Street demands that lead to fewer and fewer in-network doctors and hospitals and covered drugs. Meanwhile, billions in taxpayer dollars flow through this system with relatively no accountability. Medicare Advantage is corporate welfare on steroids, with the “invisible hand” of the market misleading and then slapping the hell out of vulnerable American seniors to enrich the big guys in control with cushy government handouts.

For Villagers, it’s either/or:

Either CenterWell and UHC strike a deal: The crisis cools, residents keep their current doctors in 2026.

Or no deal is reached: Tens of thousands will either change doctors, change plans or risk being turned away at medical appointments starting Jan. 1, 2026.

Representative Mark Pocan (D-WI) yesterday introduced eight bills aimed at strengthening traditional Medicare and reining in some of the worst practices in the privately-run Medicare Advantage business. For years, lawmakers have danced around the mounting evidence that private Medicare Advantage plans overbill taxpayers between $80 and $140 billion annually and quietly impose barriers to seniors’ care to boost profits.

Traditional Medicare remains one of the most successful public programs in American history. It was built around a simple promise: If your doctor says you need care, you get it. But as Medicare Advantage has grown, that promise has eroded for millions of people. MA plans are largely run by big insurance conglomerates – like UnitedHealthcare, Elevance and CVS/Aetna – and those insurers decide what care is covered, which doctors you can see and how long you can stay in a hospital. Each cent they have to shell out for your care is a cent they can’t keep in their pockets or split with their shareholders. Wall Street’s relentless demand for more and more of that money incentivizes them to deny or delay care that mean life-and-death for millions of American seniors.

And it’s not just health care policy nerds like me that have been focused on this issue – even the U.S. Department of Justice (DOJ) has taken aim at Medicare Advantage. In February, news broke that the DOJ had launched a civil fraud investigation into UnitedHealth Group, the largest MA insurer, for the company’s alleged use of diagnoses that trigger higher Medicare Advantage payments. And in July, the company confirmed it is the subject of a DOJ criminal investigation. The DOJ reportedly questioned former UnitedHealth Group employees about the company’s business practices.

You can see the entire package of bills on Pocan’s website. They include the Denials Don’t Pay Act, which would force Medicare Advantage plans to face real consequences if too many of their prior-authorization denials are overturned; The Right to Appeal Patient Insurance Denials (RAPID) Act, which would ensure every denial is automatically appealed, sparing sick and elderly patients from navigating a process many never even know exists; and the Protect Medicare Choice Act which would stop insurers and brokers from pushing seniors into Medicare Advantage by default.

Pocan and his co-sponsors understand that Medicare Advantage’s prior authorization hurdles and widespread denials are just Wall Street-directed obstacles that second-guess physicians and delay care. Patients pay the price. Doctors pay the price. And taxpayers pay the price.

More Perfect Union has just posted a video breaking down a truth that Big Insurance hopes you never hear: rising “health care costs” are really rising health insurance profits.

As I explained in the video, UnitedHealth, Cigna, CVS/Aetna are part of a cartel of corporate conglomerates that have built a business model that relies on overpayments in Medicare Advantage, shrinking doctor networks and a sprawling web of vertically integrated subsidiaries that vacuum up our premiums, deductibles and tax dollars — and turn them into shareholder returns as Wall Street relentlessly demands.

Here’s a bit of what I said:

“Your premiums, deductibles and pharmacy bills are all going up. We’re told it’s because medical costs are rising, but the bigger story is who’s capturing the money. In just three months, UnitedHealth Group made $4.3 billion in profits on revenues of $113 billion.

Over the past five years, the cost of a family premium has increased 26%. This year, the average cost of a family policy was almost $27,000.

Just about everybody with private insurance will be paying a lot more than that next year, regardless of whether you get it from your employer or buy it on your own. That’s because UnitedHealth and other big insurance companies cannot control rising health care costs.

In fact, insurance companies benefit from medical inflation. They just jack up their premiums enough to cover the additional cost and guarantee them a tidy profit.”

The video points out the real drivers of cost growth — from UnitedHealth’s nearly 2,700 acquisitions to Medicare Advantage overpayments that funnel billions from taxpayers into corporate profits.

If you haven’t watched it yet, I hope you will and share it with everybody else you know. It’s clear that Congress must pass common sense guardrails to stop Big Insurance from writing the rules of American health care and squeezing Americans.

Republicans are taking a harder line against extending enhanced Affordable Care Act subsidies — and doubling down on an alternative plan that would send the money directly to consumers.

Why it matters:

President Trump’s opposition to an extension makes it increasingly unlikely that Republicans will agree to renew the tax credits, even though it’s not clear how the GOP alternative would work or whether the party can reach a consensus.

Driving the news:

Trump wrote on Truth Social on Tuesday that the “only” plan he will support is “sending the money directly back to the people,” and that Congress should not “waste your time” on anything else, like a subsidy extension.

Trump didn’t elaborate on how his plan would work. The ACA already gives people financial help in buying insurance.

Some GOP proposals envision giving people money for a health savings account on top of existing ACA coverage, mitigating concerns about healthy people leaving the market.

Senate health committee Chair Bill Cassidy (R-La.) outlined a plan on Monday that would redirect the enhanced subsidy money to an HSA to help pay out-of-pocket costs for people who chose bronze-level ACA plans, which tend to have high deductibles.

He argued the move would direct money away from insurance companies and to consumers, and empower them to shop for health services.

Anotherpossible outcome would be allowing people to buy cheaper, skimpier coverage that doesn’t comply with the ACA’s benefit requirements. Some policy experts warn that would destabilize the ACA markets, by prompting an exodus of healthier people.

That would leave a sicker risk pool and prompt insurers to raise premiums, resulting in a “death spiral,” said Larry Levitt, executive vice president for health policy at KFF.

By contrast, “I don’t think there’s any risk of, you know, a collapse or death spiral, from what Senator Cassidy is talking about,” Levitt said, though without the enhanced subsidies there would still be “potentially millions of people who just won’t be able to afford insurance at all.”

Between the lines:

Senate Majority Leader John Thune (R-S.D.) wouldn’t rule out a bipartisan solution when asked about Trump’s comments on Tuesday, saying “we’ll see” how negotiations go and that “there’s an openness” to a deal on the GOP side.

He said the biggest obstacle, though, could be whether Democrats agree to apply the Hyde Amendment to the subsidies and add restrictions on using the funds for abortions.

The intrigue:

Cassidy is framing his plan as the most realistic option, given White House and House GOP leadership resistance to the subsidies.

“The president is not going to sign a straightforward extension of premium tax credits,” Cassidy said. “So if you actually want something which can pass and get a vote on the House floor, then what the president is proposing is actually a better way.”

Yes, but:

Democrats believe mounting public concern about rising health costs gives them the upper hand pushing for a subsidy extension.

“Sending people a few thousand dollars while doing nothing to lower health care costs is a scheme to help the ultra-wealthy at the expense of working people with cancer or pre-existing conditions,” Senate Democratic Leader Chuck Schumer said in response to Trump’s comments.

“Americans want Congress to extend the ACA tax credits to keep health insurance premiums from skyrocketing on January 1,” he added.

The big picture:

The war of words is further diminishing the chances that a group of moderates in both parties can find a bipartisan agreement to extend the subsidies with some modifications favored by Republicans, like an income cap and anti-fraud measures.

House GOP leaders have also been criticizing the subsidies. House Majority Leader Steve Scalise (R-La.) said on Fox News on Sunday that the party would be bringing forward legislation in the coming weeks on other ways to lower costs, like expanding HSAs or cracking down on pharmacy benefit managers.

The Senate Finance Committee will hold a hearing Wednesday morning on health care costs, giving senators a chance to stake out their positions further in public.

The bottom line:

It’s unlikely that Trump’s plan would gain the necessary 60 Senate votes to advance. But it could give Republican senators political cover if they oppose a subsidy extension.

Republicans could still opt to use the reconciliation process to pass a bill with a simple majority. Though the White House floated the idea on Tuesday, it’s not clear if any GOP-only plan has the votes to pass.

The Trump administration is expected to spell out its intentions for Medicare Advantage soon — a program that enrolls about half of U.S. seniors but has drawn intensifying criticism for costing the government too much.

Why it matters:

Centers for Medicare and Medicaid Services chief Mehmet Oz called the system “upside down” during his confirmation hearings, hinting at possible changes to the way the federal government pays and regulates plans.

Any big changes would be a departure from a history of friendly treatment from Republican administrations.

Those could become apparent in the proposed 2027 Medicare Advantage rule, which may come out before the end of this year.

How it works:

Many privately run Medicare plans charge no monthly premium and provide supplemental benefits that traditional Medicare doesn’t cover,like dental coverage and help paying for over-the-counter drugs.

The program was created on the premise that private insurers could manage care better and at a lower price point than the federal government.

But some insurers have since drawn fire for categorizing patients as sicker than they are to get higher payments, and for overly complicated pretreatment reviews.

Advisors to Congress projected the federal government would spend about $84 billion more on Medicare Advantage enrollees this year than for people in traditional Medicare. (Insurers say the advisors’ methodology is flawed.)

Oz has a history of promoting Medicare Advantage plans on his popular television show and advocating for an “MA for All” policy.

But he’s been more openly skeptical since joining the administration, as a growing cadre of GOP policymakers ask questions about the program’s finances and insurers’ role in driving up costs.

“I came both to celebrate what you’re trying to do, but also be honest about some of the issues that we’re seeing at CMS,” Oz said at the industry lobby’s conference last month.

Oz believes choice and competition are needed for a strong Medicare program, but also that CMS has a responsibility to keep “program payments fair, transparent, and grounded in data,” Catherine Howden, the agency’s director of media relations, told Axios in response to a request for comment.

This is an opportunity for Medicare Advantage insurers to have some strategic conversations with CMS about Oz’s vision for the program, said Daniel Fellenbaum, senior director at Penta Group.

UnitedHealthcare, Humana and Aetna are the three biggest Medicare Advantage insurers and cover more than 20 million seniors combined.

Where it stands:

This year CMS announced what it termed an “aggressive” strategy to increase audits of the diagnoses Medicare Advantage plans document for enrollees, which could claw back money from insurers.

Medicare’s Innovation Center said it’s working on pilot programs that could change the way thegovernment pays the plans.

Industry onlookers are also expecting the administration to propose changes to the star ratings system, which measures Medicare Advantage plan quality and dictates bonus payments to plans.

What they’re saying:

Insurers and advocates of private Medicare plans remain optimistic that Oz has their best interests at heart.

“He seems to stress good oversight and holding the program to high standards without losing sight of what’s working for seniors,” said Susan Reilly, vice president of communications at Better Medicare Alliance.

Insurance trade group AHIP welcomes “constructive, data-driven conversations with policymakers on actions that strengthen Medicare Advantage,” CEO Mike Tuffin said in a statement to Axios.

AHIP wants a focus on stability in the program after several years of medical costs increasing faster than Medicare Advantage payment, it said.

Reality check:

The 2026 update to plan payment, the first of this administration, is better than anticipated for insurers, giving them more than $25 billion increase in federal payments.

The Trump administration also struck voluntary agreements with insurers to simplify the rules for authorizing procedures and treatments ahead of time, rather than using its regulatory authority to require changes.

“We hear rhetoric talking tough on MA, but we’ve not seen them put that into actual reality,” said Chris Meekins, managing director at Raymond James.

Any big policy changes next year would also become apparent to seniors right before the midterm elections. Bigger policy swings from the administration might be more likely to go into effect for 2028, Meekins said.

What we’re watching:

President Trump has been vocal about his distaste for health insurance companies on social media lately as Congress debates extending enhanced premium subsidies for Obamacare coverage.

That ire could seep into how he directs his administration to regulate Medicare Advantage.