Also from Health Affairs: The level of competition among insurance companies has affected Affordable Care Act premiums more than any other factor.

By the numbers: Premiums are 50% higher this year in areas with just one insurer than in areas with two insurers.

“The presence of a monopolist insurer was the strongest, and most precise, predictor of 2018 premiums,” the study says.

Other factors commonly associated with higher premiums — like hospital concentration and the health of the people who live there — showed significantly smaller effects.

How it works: Jessica Van Parys, the Hunter College economics professor who conducted the study, suggests that insurers underpriced their ACA offerings in the first few years to capture market share, then raised their prices over the years.

Costs and regulatory uncertainty largely kept new competitors from entering those monopolized markets.

Stability has long been an issue for the individual health insurance market, even before the Affordable Care Act. While reforms adopted under the ACA initially succeeded in addressing some of these market issues, market conditions substantially worsened in 2016.

Insurers exited the individual market, both on and off the subsidized exchanges, leaving many areas with only a single insurer, and threatening to leave some areas (mostly rural) with no insurer on the exchange. Most insurers suffered significant losses in the individual market the first three years under the ACA, leading to very substantial increases in premiums a couple of years in a row.

For a time, it appeared that rate increases in 2016 and 2017 would be sufficient to stabilize the market by returning insurers to profitability, which would bring future increases in line with normal medical cost trends. However, Congress’s decision to repeal the individual mandate and the Trump Administration’s decision to halt “cost-sharing reduction” payments to insurers, along with other measures that were seen as destabilizing, created substantial new uncertainty for market conditions in 2018.

This uncertainty continues into 2019, owing both to lack of clarity on the actual effects of last year’s statutory and regulatory changes, and to pending regulatory changes that would expand the availability of “non-compliant” plans sold outside of the ACA-regulated market. These uncertainties further complicate insurers’ decisions about whether to remain in the individual market and how much to increase premiums.

In the states studied—Alaska, Arizona, Colorado, Florida, Iowa, Maine, Minnesota, Nevada, Ohio, and Texas—opinions about market stability vary widely across states and stakeholders.

While enrollment has remained remarkably strong in the ACA’s subsidized exchanges, enrollment by people not receiving subsidies has dropped sharply.

States that operate their own exchanges have had somewhat stronger enrollment (both on and off the exchanges), and lower premiums, than states using the federal exchange.

A core of insurers remain committed to the individual market because enrollment remains substantial, and most insurers have been able to increase prices enough to become profitable. Some insurers that previously left or stayed out of markets now appear to be (re)entering.

Political uncertainty

Premiums have increased sharply over the past two to three years, initially because insurers had underpriced relative to the actual claims costs that ACA enrollees generated. However, political uncertainty in recent years caused some insurers to leave the market and those who stayed raised their rates.

Insurers were able to cope with the Trump administration’s halt to CSR payments by increasing their rates for 2018 while the dominant view in most states is that the adverse effects of the repeal of the individual mandate will be less than originally thought. Even if the mandate is not essential, many subjects viewed it as helpful to market stability. Thus, there is some interest in replacing the federal mandate with alternative measures.

Because most insurers have become profitable in the individual market, future rate increases are likely to be closer to general medical cost trends (which are in the single digits). But this moderation may not hold if additional adverse regulatory or policy changes are made, and some such changes have been recently announced.

Many subjects viewed reinsurance as potentially helpful to market conditions, but only modestly so because funding levels typically proposed produce just a one-time lessening of rate increases in the range of 10-20 percent. Some subjects thought that a better use of additional funding would be to expand the range of people who are eligible for premium subsidies.Actions to restore stability

Concerns were expressed about coverage options that do not comply with ACA regulations, such as sharing ministries, association health plans, and short-term plans. However, some thought this outweighed harms to the ACA-compliant market; thus, there was some support for allowing separate markets (ACA and non-ACA) to develop, especially in states where unsubsidized prices are already particularly high.

Other federal measures, such as tightening up special enrollment, more flexibility in covered benefits, and lower medical loss ratios, were not seen as having a notable effect on market stability.

Measures that states might consider (in addition to those noted above) include: Medicaid buy-in as a “public option”; assessing non-complying plans to fund expanded ACA subsidies; investing more in marketing and outreach; “auto-enrollment” in “zero premium” Bronze plans; and allowing insurers to make mid-year rate corrections to account for major new regulatory changes.

Conclusion

The ACA’s individual market is in generally the same shape now as it was at the end of 2016. Prices are high and insurer participation is down, but these conditions are not fundamentally worse than they were at the end of the Obama administration. For a variety of reasons, the ACA’s core market has withstood remarkably well the various body blows it absorbed during 2017, including repeal of the individual mandate, and halting payments to insurers for reduced cost sharing by low-income subscribers.

The measures currently available to states are unlikely, however, to improve the individual market to the extent that is needed. Although the ACA market is likely to survive in its basic current form, the future health of the market—especially for unsubsidized people—depends on the willingness and ability of federal lawmakers to muster the political determination to make substantial improvements.

From 2000 to 2017, the percentage of employers offering health insurance coverage has declined from 69% to 56%. At the same time, workers are shouldering more of the costs for their health care with increasing premiums and higher deductibles and copays.

California Employer Health Benefits: Workers Shoulder More Costs presents data compiled from the 2017 California Employer Health Benefits Survey.

Key findings include:

From 2016 to 2017, health insurance premiums for family coverage increased by 4.6%, slightly higher than the 3.0% inflation rate.

Average monthly premiums, including the employer portion, were significantly higher in California than the national average. In 2017, the average premium was $604 for single coverage and $1,643 for family coverage.

California workers paid an average of 17% of the total premium for single coverage and 27% for family coverage.

One in 4 workers had an annual deductible of at least $1,000 for single coverage. Large deductibles were more common among workers in small firms (3 to 199 workers) than larger firms. Nearly 60% of workers had no deductible.

In 2017, 25% of California firms reported increasing cost sharing for workers in the past year, and 37% reported that they are very or somewhat likely to increase their workers’ share of premiums in the next year.

The full report, all of the charts found in the report, and the data files are available under Related Materials. These materials are part of CHCF’s California Health Care Almanac, an online clearinghouse for key data and analyses describing the state’s health care landscape.

The California Employer Health Benefits Survey is a joint product of CHCF and the National Opinion Research Center (NORC) at the University of Chicago. The survey was designed and analyzed by researchers at NORC and administered by National Research.

Enrollment in the individual health insurance market — the market for people who don’t get coverage through work — has declined 12 percent in the first quarter of 2018, compared to the same period last year, according to a new analysis released Tuesday.

The analysis from the Kaiser Family Foundation showed enrollment in the individual market grew substantially after the implementation of the Affordable Care Act (ACA) and remained steady in 2016, before dropping by 12 percent in 2017.

There were 17.4 million people enrolled in the individual market in 2015, compared to 15.2 million in 2017 and 14.4 million in the first quarter of 2018.

The study notes that much of the decline is concentrated in the off-exchange market, where a number of enrollees are not eligible for ObamaCare subsidies and therefore not protected from significant premium increases in 2017 and 2018.

In this market, enrollment numbers dropped by 38 percent from the first quarter of 2017 to the first quarter of 2018.

The Trump administration last year canceled key ObamaCare subsidies for insurers, leading insurers to increase premiums substantially.

The anticipation of the repeal of ObamaCare’s individual mandate has also contributed to premium increases.

While ObamaCare enrollees who receive subsidies are mostly shielded from these increases, those who don’t are left to pay the full price.

“While the vast majority of exchange consumers receive subsidies that protect them from premium increases, off-exchange consumers bear the full cost of premium increases each year,” the analysis notes.

“In 2017, states that had larger premium increases saw larger declines in unsubsidized ACA-compliant enrollment, suggesting a relationship between premium hikes and enrollment drops.”

Despite the rises in premiums, enrollment in the ObamaCare exchanges has remained stable. There were 10.6 million people on the exchanges in the first quarter of this year, compared to 10.3 million in the first quarter of last year.

The reinsurance program, which the state operated in 2012 and 2013, before the ACA’s transitional reinsurance took effect, is expected to reduce insurance costs in Maine’s individual insurance market.

The federal government approved another waiver application Monday under the Affordable Care Act, giving Maine the go-ahead to reinstate a reinsurance program it had operated briefly before the ACA took effect.

Maine is the fifth state to secure a Section 1332 waiver to establish a state-run reinsurance program, following closely on the heels of Wisconsin’s waiver request being granted Sunday. Alaska, Minnesota, and Oregon won their waivers last year, and two other states—Maryland and New Jersey—have similar applications pending.

Although the Trump administration has taken a number of actions that would appear to harm the individual market, approving these waivers seems to be a positive step in the opposite direction, says Matthew Fiedler, PhD, a fellow with the Brookings Institution Center for Health Policy who served as chief economist of the Council of Economic Advisers during the Obama administration.

“Reinsurance waivers will reduce premiums in the individual market in these states and will result in more people being covered. I think they’re a reasonable way for states to spend money,” Fiedler tells HealthLeaders Media. “There may be better ways to spend money to improve the individual market, but this is certainly an actionable one and one that states can implement more or less on their own.”

Maine projects that premiums will be 9% lower in 2019 than they would be without reinsurance. Those lower premiums are expected to encourage more people to sign up for coverage, reducing Maine’s uninsured population by 1.7%, according to independent actuarial projections cited by the state and federal governments.

A modest gain in enrollment could translate to a slight benefit for insurers and could reduce the burden of uncompensated care on hospitals, Fiedler says.

‘INVISIBLE HIGH-RISK POOL’

In a letter submitted last May to Health and Human Services Secretary Alex Azar, Maine Bureau of Insurance Senior Staff Attorney Thomas M. Record said the program, which is known formally as the Main Guaranteed Access Reinsurance Association (MGARA), had “become popularly known as Maine’s ‘ invisible high risk pool.'”

Record described the program as a key feature of health reform legislation Maine lawmakers passed in 2011. The program, which was active in 2012 and 2013, successfully reduced premiums in the individual market by about 20%, he said.

Despite that success, MGARA was suspended at the beginning of 2014, when the ACA’s transitional reinsurance program rendered it redundant, according to Maine’s waiver application. The federal reinsurance program ended as scheduled on the final day of 2016.

Material released by the Centers for Medicare & Medicaid Services describe MGARA as operating a hybrid-model reinsurance program that includes traditional and conditions-based components. High-risk patients with any of eight conditions will be ceded automatically. Other high-risk enrollees will be ceded voluntarily. The program will offer 90% coinsurance for claims in the $47,000-77,000 range and 100% coinsurance for higher claims up to $1 million.

For claims above $1 million, the program will cover the amount left uncovered by the federal government’s high-cost risk-adjustment program.

Maine estimates that its program will result in a net spending reduce of more than $33 million per year, for 2019 through 2023, with that federal savings to be passed along to the state to fund the program.

The program’s total expenses are projected to cost $90-104 million annually during the five-year waiver period.

Insurers and providers have responded positively to the prospect of state-run reinsurance programs, seeing the development as good news for business and patients alike. But the benefits should not be overstated.

“The one downside of these programs is that because tax credits fall dollar-for-dollar when premiums fall, they don’t really do anything to make coverage more affordable for people with incomes below 400% of the poverty line,” Fiedler says.

“That doesn’t mean they’re a bad thing. But they can only be one part of an overall strategy for making individual market insurance affordable.”

As high health costs squeeze employers, managed care is making a comeback.

Nineties throwbacks have swept through music, television and fashion. Some startups want to bring a bit of that vintage feel to your workplace health insurance plan.

Health maintenance organizations drove down costs but were painted as villains in that decade for limiting patient choice, rationing care and leaving consumers to grapple with high bills for out-of-network services. But some features of the plans are regaining currency. Companies reviving the model say that new technology and better customer service will help avoid the mistakes of the past.

Rising health-care costs and dissatisfaction with high-deductible plans that ask workers to shoulder more of the burden are pushing employers to consider new ways of controlling spending—and to rethink the trade-offs they’re willing to make to save money.

Medical costs have increased roughly 6 percent a year for the past half-decade, according to PwC’s Health Research Institute, outpacing U.S. economic growth and eroding workers’ wage gains. Some employers, such as Amazon.com Inc., Berkshire Hathaway Inc. and JPMorgan Chase & Co.—wary of asking workers to pay even more—are trying to rebuild their health programs.

Barry Rose, superintendent of the Cumberland School District in northern Wisconsin, went shopping recently for a new health plan for the district’s 290 employees and family members after its annual coverage costs threatened to top $2 million.

“How do we provide quality, affordable and usable health care for employees,” said Rose. “I can’t keep taking money out of their paychecks to spend on health insurance.”

The company he picked, called Bind, is part of a new generation of health plans putting a tech-savvy spin on cost controls pioneered by HMOs.

Bind, started in 2016, ditches deductibles in favor of fixed copays that consumers can look up on a mobile app or online before heading to the doctor. Another upstart, Centivo, founded in 2017, uses rewards and penalties to nudge workers to get most of their care and referrals for specialists from primary-care doctors.

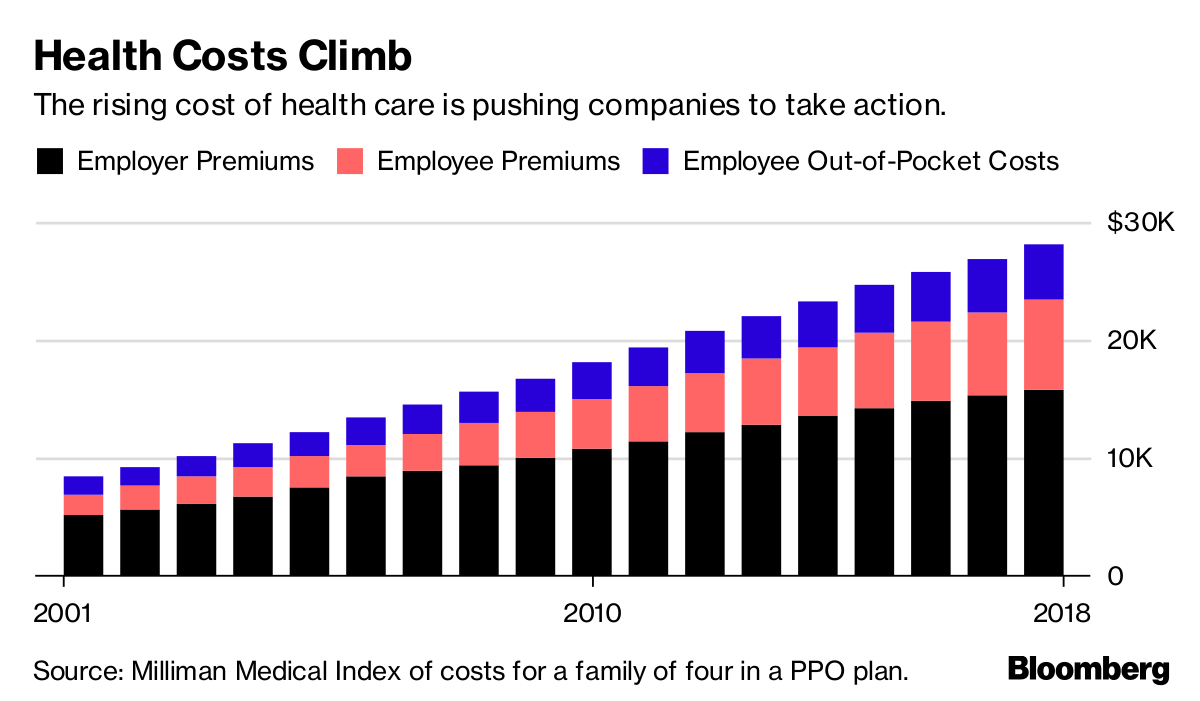

Health Costs Climb

The rising cost of health care is pushing companies to take action.

For many years, employers offered health plans that paid the bills when workers went to see just about any doctor, imposing few limits on care. The companies themselves usually paid much or all of the premiums.

Confronted with rising costs in the 1990s, many employers switched to HMOs or other forms of what became known as managed care. The switch worked, helping hold health costs down for much of the decade.

Soon, however, consumer and physician opposition grew amid horror stories of mothers pushed out of the hospital soon after childbirth, or patients denied cancer treatments. States and the federal government passed laws to protect consumers, and, in 1997, then-President Bill Clinton appointed a panel to create a health consumers’ Bill of Rights.

“The causes of the backlash are much deeper than the specific irritations or grievances we hear about,” Alain Enthoven, the Stanford health economist who helped pioneer the idea of managed care, said in a 1999 lecture. “They are first, that the large insured employed American middle class rejects the very idea of limits on health care because they don’t see themselves as paying for the cost.”

Workers would soon bear the cost, though. By the end of the decade, employers had moved away from these limited health plans. In their wake, costs skyrocketed, giving rise to a new cost-containment tool: high deductibles.

Centivo co-founder Ashok Subramanian spent the past decade trying to figure out how to offer better health insurance at work. His first startup, Liazon, helped workers pick from a big menu of coverage options. He sold it for some $215 million to Towers Watson in 2013, but he said it didn’t fix the bigger problem: Workers had lots of options, but none of them were very good.

“Yes, we were increasing choice, yes we were enabling personalization, but the choices themselves were not that good,” Subramanian said in an interview. “The choices themselves were predicated on a system in which the fundamental incentives in health care are broken.”

Tony Miller, Bind’s founder, helped give rise to health plans with high out-of-pocket costs. He sold a company called Definity Health that combined health plans with savings accounts to UnitedHealth Group Inc. for $300 million in 2004. He now says high-deductible plans failed to deliver on their promises.

“There’s a fever pitch of frustration at employers,” he said. “They’re tired of using the same levers that they’ve been using for the past 20 years.”

UnitedHealth, the biggest U.S. health insurer, helped create Bind with Miller’s venture capital firm and is an investor in the company, which has raised a total of $82 million. Bind is also using UnitedHealth’s network of doctors and hospitals as well as some of its technology.

Centivo has raised $34 million from investors including Bain Capital Ventures.

Centivo and Bind both promise to reduce costs for patients and employers while making it easier to find doctors and check coverage. They say they’ll reduce costs by making sure patients get the care they need, keeping them healthy and avoiding emergencies or unnecessary treatment.

Covered?

The proportion of Americans under 65 in health plans with high deductibles continues to increase.

In most cases, workers who follow the rules of Centivo’s plans won’t face a deductible. When signing up, employees pick a primary-care doctor, who’s responsible for managing their care and making decisions on whether they need to see a specialist. Care provided or directed by that primary physician is free, as is some treatment for chronic diseases such as diabetes, depending on how employers choose to set up the coverage.

The goal is to ensure workers get the care they need, while avoiding low-value treatments. Those who go to an emergency department in cases that aren’t true emergencies, for example, could face high costs.

“The big question is: Is the market ready for it?” said Mike Turpin, who advises employers on their health benefits as an executive vice president at USI Insurance Services. “The American consumer just has it built into their head that access equals quality.”

Bind bundles its coverage so consumers don’t get billed for lots of charges for services that are part of the same treatment. In Rose’s district, the copay for an emergency room visit is $250, while the cost of a hospital stay is capped at $1,000. Office visits are $35; preventive care is free.

Bind also offers what it calls on-demand insurance. Coverage for planned procedures such as knee surgery, tonsil removal or bariatric surgery must be purchased before the operation. That gives Bind a chance to push customers toward a menu of lower-cost alternatives or cheaper providers.

A patient who looks up knee arthroscopy, for instance, would also be offered physical therapy. The patient’s cost for the surgery ranges from $800 at an outpatient center to more than $6,000, in an example used by Miller. Surgeries in hospitals are typically more costly. Bind also charges more for providers who tend to be less efficient or have worse outcomes.

The ability to view costs upfront is part of what appealed to Rose, the Wisconsin superintendent. “Each of my employees knows exactly what they’re paying for, and they have choice in it,” he said.

Rose said the switch to Bind will save his district several hundred thousand dollars, depending on how much health care his workers need over the next year.

Lawton R. Burns, director of the Wharton Center for Health Management and Economics at the University of Pennsylvania, recently authored a paper with his colleague Mark Pauly arguing that it’s probably impossible to simultaneously improve quality, lower costs and achieve better health outcomes. The ideas now being pushed forward, he writes, are similar to ideas tested in the 1990s.

“It’s deja vu all over again,” he said. “It’s not clear to me, this is just me talking, that people have learned the lessons of the 1990s.”

The House Ways and Means Committee on Thursday approved legislation that would chip away at ObamaCare, including a measure that would temporarily repeal the law’s employer mandate.

The bill sponsored by GOP Reps. Devin Nunes (Calif.) and Mike Kelly (R-Pa.) would suspend penalties for the employer mandate for 2015 through 2019 and delay implementation of the tax on high-cost employer-sponsored health plans for another year, pushing it back to 2022.

Congress repealed the penalty associated with the individual mandate last year, but it doesn’t take effect until 2019.

“I think it’s fair, if we relieve the burden for individuals, that we stand with our small and mid-sized companies,” Kelly said.

Powerful lobbying groups like the U.S. Chamber of Commerce have pushed for a repeal of the employer mandate.

The other measure, sponsored by Reps. Peter Roskam (R-Ill.) and Michael Burgess (R-Texas), would allow the use of ObamaCare’s tax credits for plans outside of the exchanges in the individual market. It would also allow anyone to purchase a catastrophic plan — plans that are cheaper but cover fewer services and are currently only available for those under the age of 30.

The bill “provides a much needed offramp for pressure people are feeling right no in terms of premiums increases and limited choices,” Roskam said.

Both measures advanced on party-line votes.

Democrats opposed the bills, saying they would cost too much and destabilize ObamaCare.

Employers across the board saw health plan costs rise for a variety of reasons, but employers with less than 500 workers were especially vulnerable to cost effects, according to a national survey from last year.

Most small employers have faced increasing costs associated with their health plans, while suffering from a lack of leverage and resources to manage the costs.

Though health benefit cost growth has remained steady at 3% annually, a survey of employer-sponsored health plans conducted by Mercer, a healthcare consulting firm, found that employers of varying sizes faced a wide range of health plan cost increases during 2017.

EMPLOYERS WITH 10-499 EMPLOYEES:

34% saw costs increase by more than 10%

29% saw no change

19% saw costs increase 5% or less

18% saw costs increase 6 to 10%

EMPLOYERS WITH MORE THAN 500 EMPLOYEES:

31% saw no change

28% saw costs increase 5% or less

22% saw costs increase 6 to 10%

19% saw costs increase more than 10%

EMPLOYERS WITH MORE THAN 20,000 EMPLOYEES:

50% saw costs increase 5% or less

36% saw no change

14% saw costs increase 6 to 10%

11% saw costs increase more than 10%

The survey attributed the cost increases to a number of factors, namely expensive new treatment options and a rapidly aging population. A new cost driver is the slow rise of uninsured patients, which ticked up in 2017 and is likely to lead to providers shifting the costs of uncompensated care onto employer health plans, according to Mercer. The firm highlighted the importance of maintaining a vibrant workforce in order to counter the effects of rising costs associated with uninsured populations.

“Employers need to manage benefit cost and help employees thrive,” the study read. “These two goals may sound as if they are in opposition – but they don’t have to be. Employers can slow cost growth while helping their employees to receive better care and a better patient experience.”

Health insurers warned that a move by the Trump administration on Saturday to temporarily suspend a program that was set to pay out $10.4 billion to insurers for covering high-risk individuals last year could drive up premium costs and create marketplace uncertainty.

The Affordable Care Act’s (ACA) “risk adjustment” program is intended to incentivize health insurers to cover individuals with pre-existing and chronic conditions by collecting money from insurers with relatively healthy enrollees to offset the costs of other insurers with sicker ones.

President Donald Trump’s administration has used its regulatory powers to undermine the ACA on multiple fronts after the Republican-controlled Congress last year failed to repeal and replace the law propelled by Democratic President Barack Obama. About 20 million Americans have received health insurance coverage through the program known as Obamacare.

America’s Health Insurance Plans (AHIP), a trade group representing insurers offering plans via employers, through government programs and in the individual marketplace, said the CMS suspension would create a “new market disruption” at a “critical time” when insurers are setting premiums for next year.

“It will create more market uncertainty and increase premiums for many health plans – putting a heavier burden on small businesses and consumers, and reducing coverage options. And costs for taxpayers will rise as the federal government spends more on premium subsidies,” AHIP said in a statement.

It could also encourage more insurers to bow out of Obamacare.

“This is occurring right at the time of year that people (insurers) are making decisions about whether to participate in the exchanges and what premiums to charge if they do,” said Eric Hillenbrand, a managing director at consultancy AlixPartners. “This will affect their thinking on both of those decisions.”

The Centers for Medicare and Medicaid Services (CMS), which administers ACA programs, said on Saturday that months-old conflicting court rulings related to the risk adjustment formula prevent them from making payments.

CMS was referring to a February ruling from a federal court in New Mexico that invalidated the risk adjustment formula, and a January ruling from a federal court in Massachusetts that upheld it.

CMS administrator Seema Verma said in a statement the administration was “disappointed” in the February ruling and that CMS has asked the court to reconsider and “hopes for a prompt resolution that allows CMS to prevent more adverse impacts on Americans.”

But supporters of the ACA criticized the CMS announcement as the latest move by the Trump administration to undermine Obamacare.

“We urge the Trump administration to back off of this dangerous and destabilizing plan, and instead begin working on bipartisan solutions to make coverage more affordable,” said Brad Woodhouse, the executive director of Protect Our Care, a progressive group that supports Obamacare.

The administration has made several other moves in recent years to scale back or halt implementation of certain aspects of the ACA.

Late last year, it said it would halt so-called cost-sharing payments, which offset some out-of-pocket healthcare costs for low-income patients.

It has also scaled back the advertising budget for Obamacare healthcare plans during the open-enrollment period by about 90 percent.

“What you are effectively doing is dismantling pieces of [the ACA] without replacing them,” Hillenbrand said. “It moves us back to some extent to the status quo where people with pre-existing conditions found it very difficult to get insurance.”