https://www.thefiscaltimes.com/2017/07/08/Here-s-What-Bipartisan-Health-Care-Deal-Might-Look

Practically overnight, Senate Majority Leader Mitch McConnell (R-KY) placed the once-unthinkable notion of a bipartisan deal with the Democrats to salvage the Affordable Care Act well within the realm of possibility.

For months, McConnell, House Speaker Paul Ryan (R-WI) and President Trump vowed to move with alacrity to repeal and replace Obamacare with a far superior GOP health insurance plan that would bring down premium costs , provide tax relief for wealthier Americans and the health care industry, and phase out expanded Medicaid coverage for millions of poor and disabled people.

But with the Senate’s 52 Republicans still badly divided over how best to proceed and time running out before a long August recess, McConnell said Thursday during a speech in Kentucky that if his party cannot muster at least 50 votes to rewrite the Obamacare law, it would have no choice but to work with the Democrats to produce a more modest bill to support the law’s existing insurance market.

“No action is not an alternative ,” McConnell said during a speech at a Rotary Club lunch in Glasgow, Kentucky. “We’ve got the insurance markets imploding all over the country, including in this state.”

The Republicans have long argued that Obamacare is in a “death spiral,” with premiums going through the roof and more and more major health care insurers pulling out of the market after incurring huge losses on the ACA exchanges. The Trump White House, the Department of Health and Human Services (HHS) and the Internal Revenue Service have also taken executive actions that have undercut enrollment and insurer participation.

But the veteran Senate majority leader has begun facing up to the harsh political reality that as many as a dozen conservative and moderate Republicans currently oppose a bill that McConnell almost single-handedly drafted behind closed door. Now it will take a herculean effort to muster a minimum of 50 votes needed to pass the bill under expedited budget reconciliation rules that were designed to avert a filibuster.

Douglas Holtz-Eakin, a former Congressional Budget Office director and Republican economic adviser, said on Friday that McConnell “has done the [political] arithmetic right” and that there may be no choice but to cut a deal with Senate Minority Leader Chuck Schumer (D-NY).

“We know that the exchanges are melting down under current law,” Holtz-Eakin, president of the American Action Forum, said in an interview. “We know that the cost-sharing money [to subsidize insurers] has to come from somewhere or they will continue to melt down, and insurers will leave, and premiums will continue to skyrocket.”

However, he warned that such an agreement would have serious political ramifications for the GOP and could touch off a conservative backlash, especially in the House. “It’s going to be a really bad deal for Republicans, and House Republicans are going to have to eat it.”

Michael F. Cannon, director of health policy at the libertarian Cato Institute, said McConnell might have raised the idea of working with Democrats to force recalcitrant Republicans into line. However, he said it was high risk for a party that for the past seven years has promised to repeal and replace Obamacare.

“If he does pursue a bill with Democrats to bail out the exchanges, then it will cause a rift in his own party much bigger than the rift he sees right now,” Cannon cautioned.

Schumer on Thursday called McConnell’s comments encouraging, and that his caucus is “eager to work with Republicans to stabilize the markets and improve the law.” The minority leaders have said for weeks that the Democrats were ready to bargain with the GOP and the White House on virtually any issue provided the Republicans abandoned their effort to repeal former President Barack Obama’s signature program.

According to several policy experts, here are five areas where a bipartisan health care compromise might be struck:

- Cost sharing — One of the pillars of the Obamacare markets is the $7 billion a year in federal cost-sharing subsidies to insurance companies that allow them to help offset the cost of the monthly premiums and copayments of low and moderate income Americans who make between $12,000 and $48,000 a year. House Republicans challenged the constitutionality of those subsidies in court, and Congress and the Trump administration have agreed to continue the payments pending a final outcome of the case.

But without more certainty of the future of those subsidies, many major insurance companies have begun pulling out of markets throughout the country. If both parties are concerned about stabilizing the Obamacare insurance markets and making sure they don’t go under, making the cost-sharing subsidies permanent would be a good place to start. - Reviving Risk Corridors –Before the Republicans succeeded in turning off the spigot, an Obamacare reinsurance program or so-called “risk corridors” funneled billions of dollars to insurers to offset the unforeseen costs of their most expensive enrollee.

Republicans led by Sen. Marco Rubio (R-FL) led an effort to kill off the program, arguing that it constituted an unjustifiable “bailout” of the insurance industry. But Republican and Democratic negotiators would likely have to reconsider reviving the program – and tax revenue to pay for it – to further stabilize the insurance market. - Tax Repeal – The Senate GOP plan includes a tax cut of $700 billion over the coming decade, which would be achieved by repealing all the tax hikes in Obamacare passed to help finance the health insurance program. The cost of that massive tax relief for mainly wealthy Americans and the pharmaceutical, health care and insurance industries, would be offset by deep cuts in Medicaid for millions of poor and disabled Americans.

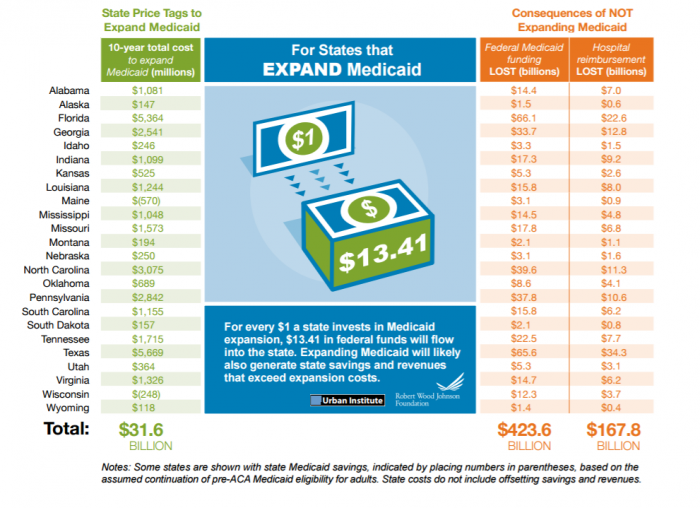

Democrats are adamant about blocking wholesale cuts in Medicaid. However, they might be open to some horse trading to repeal some of the Obamacare taxes while preserving others, in order to prevent massive cuts in Medicaid. - Medicaid Spending– The Senate GOP bill would allow 31 states that expanded Medicaid to millions of childless, able-bodied, low-income adults to continue receiving bonus federal funding through 2013, before beginning to reduce it between 2021 and 2024.

Democrats would be insistent on preserving expanded Medicaid even longer and would have considerable leverage in order to achieve that goal. Moreover, there is virtually no interest on their part in transforming Medicaid from an open-ended entitlement to a per-capita-cap block grant to the states. But amid growing concern about the long-term impact of growing entitlements on the debt, Democratic negotiators might be open to reforms to slow the rate of growth of Medicaid. - Lowering premiums – There is little disagreement between the two parties on the need to bring down premiums and copayments that have literally priced many families out of the market, even with tax subsidies. Yet finding a compromise that satisfies the Democrats demands to preserve Obamacare levels of benefits – including a ban on insurers discriminating against people with preexisting medical conditions — and GOP insistence on allowing skimpier, less expensive policies for younger and healthier people – will be hard to do.

“All of this adds up to huge new spending, but the Democrats would be in charge, and McConnell knows it,” Joe Antos, a health care expert with the conservative-leaning American Enterprise Institute, said. “They won’t get everything, but I don’t expect any compromise to look like a Republican bill. Nonetheless, if the Democrats aren’t too greedy, such a bill could pass in the Senate, but would be rejected in the House.”

{kind=link}