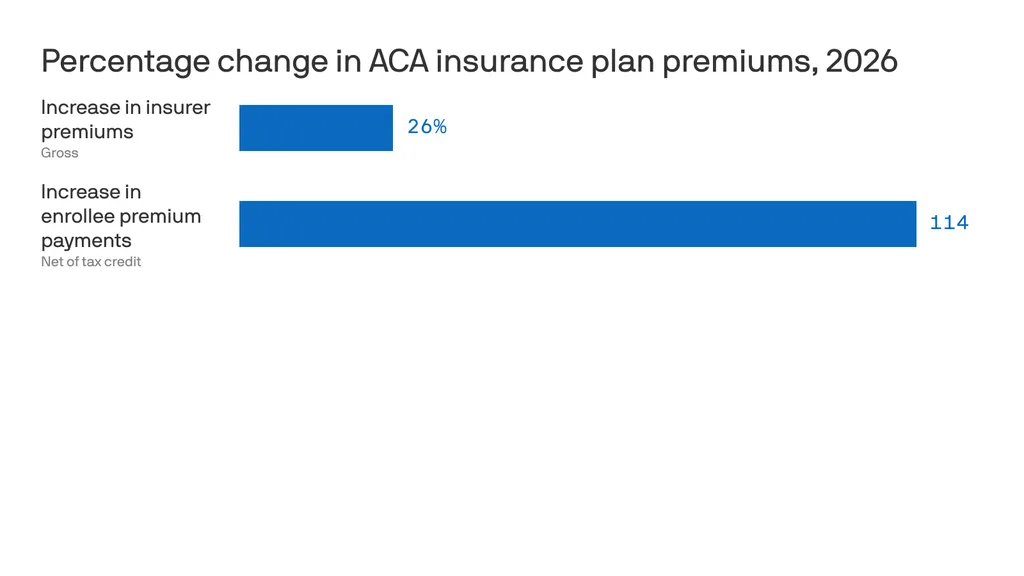

The 119th Congress headed into the holidays no doubt looking forward to quality time with their loved ones and a fat goose on the dinner table—or whatever the privileged stewards of the People eat at Christmas—with what seemed like little concern for the mess and panic they left behind. Messy panic like what the nearly 25 million Americans getting their health insurance through the ACA are facing as their monthly premiums increase at astronomical rates. (Assuming they stick with the devil they know.) Now they’re back, surely refreshed with all engines blazing on their New Year’s resolution to make health care more affordable. It is, after all, what the People want.

But while what to do with the ACA gets fought over like an unloved middle child in a divorce, another form of health care dupery will continue to operate like a mob-run casino.

Many of us navigate our health care thinking that if we can land a full-time job at a company offering benefits, we—and our families—will be covered for most physical and mental health issues without complete disruption to our financial health. And in many cases, sure, that tracks. What we’re not seeing is the financial fleecing that those companies are experiencing at the hands of third-party administrators (TPAs). What’s more is that the companies aren’t seeing it either. And that’s not a bug. It’s a feature.

An employer has options when deciding how to provide health benefits to its employees. One is to contract directly with an insurance company and pay fixed premiums. Another is to self-insure. Self-insured employers pay for all enrolled member benefits and claims directly from their own funds instead of paying those aforementioned fixed premiums. It’s an attractive option for employers because even though the company assumes the financial risk, it offers control over costs, plan design and claims-related data, all of which can help the company run more efficiently and with greater fiduciary understanding. They’re popular, too, with approximately 57% of private sector workers enrolled in these self-funded plans, according to KFF. To facilitate the company’s coverage, employers contract with a TPA to broker plan details, manage claims, pay providers, assist plan members and ensure the benefit program remains compliant with state and federal regulations.

This is theoretical.

TPAs say they’re looking after the company, but they don’t. They’re looking after themselves and their parent companies. And just who are these parents? Blue Cross Blue Shield, UnitedHealthcare, Cigna, and Aetna. Or, as they’re collectively called, the BUCAs. The usual suspects in the web of health care greed and deception.

It’s like taking a pregnancy test then being told the results can’t be shared with you because the results belong to the stick with the pee on it.

Skimming the till the TPA way

The Employee Retirement Income Security Act (ERISA) was passed in 1974 to protect patients by requiring transparency, fiduciary standards and fair claims processes for employer-sponsored health (and retirement) plans. TPAs have found clever ways to avoid ERISA accountability in the way they structure the administrative services agreements (ASAs) they sign with employers. One is by enlisting gag clauses in the ASAs to protect TPAs from showing their work to the employer, which obviously defeats the whole purpose of choosing to self-fund and have more oversight of how their money is being spent. The Consolidated Appropriation Act of 2021 prevented these gag clauses. But TPAs are nimble and clever, and when pressed to offer up information, such as any of the data related to claims managed and paid, TPAs argue they don’t have to because the data is proprietary. It’s an odd argument to make. It’s the employer’s money being spent and their employees being treated. It’s like taking a pregnancy test then being told the results can’t be shared with you because the results belong to the stick with the pee on it.

Not sharing crucial plan information with the employer is one thing, tacking on fees under the guise of good stewardship is another. Like the overpayment recoupment fee. Here’s how this could play out:

- The TPA discovers a provider was overpaid due to an error made by duplicating payments, incorrect coding, or any other administrative whoopsie

- The TPA recoups the overpaid amount, say, $5,000, then takes a percentage of the recouped money—typically 30% — as a fee for cleaning up the mess they made

- They recover the extra $5,000 the employer paid, the employer gets back $3,500 while the TPA banks $1,500

- This means that the employer paid a total of $6,500 on a $5,000 claim, making carelessness an incentive for TPAs

Shared savings fees are put in play when someone enrolled in a health plan uses an out-of-network (OON) provider. As we know, OON claims are often hefty bills. Seemingly, in good faith, the TPA will negotiate a discounted rate with the provider. It could look like this:

- The OON provider bills the employer $50,000

- The TPA negotiates the provider down to $20,000 then takes their shared savings fee out of the $30,000 savings

- Again, this fee rate is often around 30%. That puts $9,000 in the TPA’s pocket

The TPA is incentivized here to push members to go OON, and why not? A $30,000 savings sounds real good. But employers aren’t getting the opportunity to weigh in on these negotiations because they are, you know, “proprietary.”

Putting it honestly, TPAs are the neighborhood mafioso.

TPAs also have skip lists, which are providers they do not apply oversight to when looking for billing errors, which they rarely do anyway, but these lists make it more, um, official. In May 2024, W.W. Grainger, Inc., a product distribution company with 20,000-plus employees (and their family members) filed a lawsuit against Aetna claiming Aetna took money paid by Grainger intended to pay for claims, paying providers only a portion of the money, keeping the rest for itself. The suit claims, “Aetna did not use the fraud prevention techniques it regularly employs when administrating claims for its own fully insured plans. Aetna never refunded or credited the difference to the Plans.” The suit further states, “Aetna also engaged in active deception to conceal its breaches of its duties to the Plans. Aetna prevented Grainger from discovering Aetna’s improper conduct, including by limiting audit rights, providing false or inaccurate claims reports, and preventing Grainger from obtaining or accessing data about the actual financial transactions between Aetna and the health care providers.”

Many other similar suits have been filed against TPAs but are either dismissed or held up in the court’s web of confusion and legal ballet.

The uphill battle for Capitol Hill

Putting it kindly, TPAs are middlemen sold as a way to lighten the administrative load for a company. Putting it honestly, TPAs are the neighborhood mafioso. Imagine with me, a neighborhood dry cleaner… One day, a wise guy walks in and tells the owner that he needs to pay 30% of the profits each week in exchange for protection. “Protection from what?” the dry cleaner asks. “From, you know, trouble. And you don’t want any trouble. Not at a nice establishment such as this.” There’s no way the dry cleaner can win. Either pay the guy or risk going to open the door one morning only to discover the door is the only thing left standing after the place mysteriously burned down overnight.

A bill introduced last year by Senators John Hickenlooper (D-Colo.) and Roger Marshall (R-Kan.) called the Patients Deserve Price Tags Act (PDPTA) is designed to make health costs more transparent and provide employers with better tools to hold TPAs accountable as well as to strengthen and expand existing transparency measures like requiring TPAs to disclose compensation practices truthfully, completely and upfront instead of leaving the burden to employers. The bill would make void any provisions in ASAs that support limiting access to employers. Furthermore, it would empower the Department of Labor (DOL) to fine TPAs $10,000 for each day a violation continues. TPAs would also be required to make quarterly reports detailing pricing and compensation practices and report the total they have been paid in rebates, fees, discounts and other forms of payment. Failure to provide this information would be a violation of ERISA, and the DOL could fine the TPA $100,000 per day until the report is provided.

But will it pass? And if so, how much of it will get hacked away thanks to BUCA lobbying efforts? And is another bill even the answer? Legislation has been passed to defend against these practices, and yet, they persist. Apparently, doing the same thing over and over again and expecting a different result is not insanity, but progress for Congress. Another bill may just add to the complexity of things. And the big question remains: Will it save self-insured employers money? Doubtful. TPAs can simply raise the price of doing business. That’s BUCA forecasting 101—everything can always be more expensive.

Perhaps Washington needs to begin thinking of TPAs and BUCAs like the organized criminals they are and bring a RICO case against them.