Cartoon – My Best Leadership Skill

Five major health systems are teaming up with one of North Carolina’s largest insurers to launch a new value-based care program.

Duke University Medical Center, University of North Carolina Health Care, Wake Forest Baptist Health, WakeMed Health and Hospitals, Cone Health and their respective accountable care organizations (ACOs) will join the new program led by Blue Cross and Blue Shield of North Carolina (Blue Cross NC).

Under the new program, called Blue Premier, Blue Cross NC and the health systems will be jointly responsible for better health outcomes and patient experiences while lowering costs. The idea is to make providers share risk for higher costs and inefficiencies in the healthcare system in exchange for reaping the rewards of the savings.

The total payments to the health system under Blue Premier will be based on the health systems’ ability to manage the total cost of care and their overall performance.

“Historically, our healthcare system pays for services that may or may not improve a patient’s health, and our customers simply cannot afford this approach,” said Patrick Conway, M.D., Blue Cross NC president and CEO and the former head of the Center for Medicare and Medicaid Innovation (CMMI), in a statement. “Moving forward, insurers, doctors and hospitals must work together, and hold each other accountable for improving care and reducing costs.”

The news comes just a month after Blue Cross NC announced a partnership with Aledade, a well-funded startup that partners with primary care physicians to build and lead ACOs, to launch a new initiative that will support hundreds of independently owned and operated primary care physician clinics in the state in value-based care.

The insurer has an established history of working with the health systems to find ways to drive down costs. In August, Blue Cross NC worked out a deal with UNC Health in a move that reduced premiums on the ACA exchange. However, at the same time, the insurer cut ties with WakeMed and Duke Health by discontinuing its Blue Local exchange.

Blue Cross NC has said that by 2020, it plans to have at least half of its members with a provider who is working under a value-based contract.

Medicare Advantage insurers added 1.4 million members to their rosters for 2019 coverage, as they looked to grow membership in a market known for being politically safe and predictably lucrative. But Advantage membership is growing at a slower pace compared with previous years.

According to the latest federal data showing enrollment as of this month, 22.4 million people are enrolled in Medicare Advantage for 2019 coverage—an alternative to the traditional Medicare program in which private insurers contract with the federal government to administer program benefits. That’s an increase of 6.8% since January 2018. Health insurers, however, managed to grow their Advantage membership base by more than 1.5 million in both 2016 and 2017.

Some industry experts were expecting more. “The formula was there: Health plans were aggressive, they got nice rate increases, the rules around benefit design relaxed a little bit,” explained Jeff Fox, president of Gorman Health Group, which provides technology and other services to Medicare Advantage plans.

Fox expected Advantage enrollment to increase by double-digits over the past year, as health plans invested heavily in marketing and the federal government provided one of the biggest rate increases for the plans in years at 3.4%. The Trump administration also granted Advantage plans the flexibility to provide more supplemental benefits in 2019, such as transportation and in-home care.

But Fox said distraction from the craziness of the November midterm elections may have kept some seniors from enrolling during the annual open enrollment that lasted from Oct. 15 to Dec. 7, 2018. While the CMS data captures some of the sign-ups from open enrollment, figures out next month are likely to be higher.

Despite the slower pace, many Advantage insurers still experienced big enrollment increases as they picked up more market share. About half of all members are covered by just three companies. UnitedHealth held onto the top spot, adding nearly 500,000 Advantage members in the past year for a total 5.7 million. UnitedHealth holds more than a quarter of the total Medicare Advantage market share.

Humana remained the No. 2 Advantage insurer with 3.9 million members, an increase of 10.4% over January 2018. But thanks to its acquisition of Aetna, CVS Health took the No. 3 spot with 2.2 million Advantage enrollees. Kaiser Foundation Health Plan and Anthem rounded out the top five insurers with the most Advantage members.

On a percentage basis, Anthem and Aetna grew membership the fastest. Anthem’s Medicare Advantage membership spiked 53% to 1.1 million members compared with the same time last year. The Indianapolis-based insurer has long focused on serving employers, but recently turned its sights to growing Medicare Advantage rolls through acquisitions and expansions in places where it already operates.

Anthem bought Florida-based Medicare plans HealthSun in December 2017 and America’s 1st Choice in February 2018, together giving Anthem about 170,000 more Advantage members. Anthem CEO Gail Boudreaux told investment analysts in July that the company would focus on selling group Medicare Advantage plans and serving medically complex dual-eligible members in 2019.

CVS Health, meanwhile, grew its Medicare membership by 26.7% in 2018 to 2.2 million through its acquisition of Aetna. The deal is still technically awaiting a federal judge’s approval. In a research note Monday, Barclays equity analyst Steve Valiquette noted that Aetna’s membership growth was driven by its expansion into about 360 new counties. Valiquette wrote that the growth experienced by some public health insurers during the annual enrollment period for 2019 coverage was driven more by market share gains than by industry growth.

Medicare Advantage enrollment is climbing as the baby boomer generation ages rapidly into Medicare. Those seniors are used to employer-sponsored managed-care plans and are choosing Advantage over traditional Medicare more often than previous generations did. Seniors also often get more benefits, including dental care, eyeglasses and gym memberships, with an Advantage plan.

Medicare Advantage also enjoys support from both political parties and is able to weather swings from one federal administration to the next, whereas insurers that sell plans in the individual market, for example, may have to deal with more volatility.

Moreover, Medicare Advantage margins tend to hover between 4% to 5%, whereas Medicaid margins come in at 2% to 3% and the individual market historically has had even lower margins, S&P analyst Deep Banerjee told Modern Healthcare in August. The group employer business has higher margins, but that market isn’t growing like Medicare Advantage is.

Joseph Daskalakis’ son Oliver was born on New Year’s Eve, a little over a week into the current government shutdown, and about 10 weeks before he was expected.

The prematurely born baby ended up in a specialized neonatal intensive care unit, the only one near the family’s home in Lakeville, Minn., that could care for him.

But Daskalakis, who works as an air traffic controller outside Minneapolis, has an additional worry: The hospital where his newborn son is being treated is not part of his current insurer’s network and the partial government shutdown prevents Daskalakis from filing the paperwork necessary to switch insurers, as he would otherwise be allowed to do.

As a result, he could be on the hook for a hefty bill — all the while not receiving pay. Daskalakis is just one example of federal employees for whom being unable to make changes to their health plans really matters.

Although the estimated 800,000 government workers affected by the shutdown won’t lose their health insurance, an unknown number are in limbo like Daskalakis — unable to add family members such as spouses, newborns or adopted children to an existing health plan; unable to change insurers because of unforeseen circumstances; or unable deal with other issues that might arise.

“With 800,000 employees out there, I imagine that this is not a one-off event,” says Dan Blair, who served as both acting director and deputy director of the federal Office of Personnel Management during the early 2000s and is now senior counselor at the Bipartisan Policy Center. “The longer this goes on, the more we will see these types of occurrences.”

While little Oliver Daskalakis is getting stronger every day — he’s now out of the ICU, according to his father’s local air traffic union representative — it’s unclear how the situation will affect his family’s finances.

That’s because out-of-network charges are generally far higher than being in-network, and NICU care is enormously expensive,no matter what. Those bills could add up, especially as the family’s current insurance plan has an out-of-pocket maximum of $12,000 annually. Because Oliver was born before the new year, the family could face that amount twice — for 2018 and for 2019.

And Daskalakis still isn’t getting paid.

“I don’t know when I’ll be able to change my insurance, or when I’ll get paid again,” Daskalakis wrote to Sen. Tina Smith, D-Minn., who shared the letter on Facebook and before her Senate colleagues last week.

Other families are also worried about paperwork delays, and the financial and medical effects a prolonged shutdown could cause.

Dania Palanker, a health policy researcher at Georgetown’s Center on Health Insurance Reforms, studies what happens when families face insurance difficulties. Now she’s also living it.

After arranging to reduce her work hours because of health problems, Palanker knew her family would not qualify for coverage through her university job. No problem, she thought, as she began the process in December of enrolling her family in coverage offered by her husband’s job with the federal government.

But there was a hitch.

We could not get the paperwork in time to apply for special enrollment through the government and get it processed before the shutdown,” Palanker says.

Georgetown allowed her to boost her work hours this month to keep the family insured through January, but Georgetown’s share of her coverage will end in February.

Palanker’s treatments are expensive, so she is likely to hit or exceed her annual $2,000 deductible in January — then start over with another annual deductible once the family secures new health coverage.

“I’m postponing treatment in hopes that it is just a month and I’m back on the federal plan in February,” says Palanker, who has an autoimmune disease that causes nerve damage. “But I can’t postpone indefinitely, as my condition will get worse.”

Overseeing federal health benefits programs is within the purview of the Office of Personnel Management, whose data hub is operational, according to a spokeswoman. But getting information to that data hub to make the kind of changes Daskalakis, Palanker and others need depends on the individual agencies that employ government workers.

The OPM has told government agencies “that they should have [human resources] staff available during the lapse, specifically to process” such requests, which are called “qualifying life events,” the spokeswoman says.

Workers enrolled in plans under the Blue Cross Blue Shield Association, which covers about 5 million federal workers and retirees in the Federal Employees Health Benefits Program, can make qualifying life event changes directly with the insurer if they can’t get it processed by their workplace, an association spokesman said Friday.

In a written statement Wednesday, Smith said: “Oliver’s story is a powerful reminder that hundreds of thousands of real families have had their financial and personal lives turned upside down by this unnecessary shutdown.” The Minnesota senator called onthe president to come back to the negotiating table.

For Daskalakis, there’s been some recent good news.

His union representative, Tony Walsh, says both the OPM website and Daskalakis’ insurer now indicate that the family’s request to change to an insurance plan that classifies the hospital as “in-network” will be retroactive to Oliver’s birthday — so the out-of-network charges may not play a role.

Just to be safe, “Joe is currently working on an insurance appeal based on no in-network care [being available],” Walsh reports in an emailed statement.

Still, the family has already received an initial $6,000 bill from the hospital, Walsh notes. He says that $6,000 does not include costs associated with Oliver’s birth or his stay in the intensive care unit — those charges likely are still to come.

Walsh says the shutdown is affecting a broad swath of employees in ways many lawmakers never anticipated.

The workers “are essential to the system,” he says, “and it’s unfair they are being treated this way.”

One of the rare market bright spots last year, the U.S. healthcare sector remains a Wall Street darling despite a slow start to 2019.

As 2019 begins, healthcare .SPXHC is the most favored of the 11 main S&P 500 sectors, according to a Reuters review of ratings from 13 large Wall Street research firms, which recommend how to weigh those groups in investment portfolios.

Healthcare shares overall rose 4.7 percent last year, one of only two S&P 500 sectors, along with utilities, to post positive returns in 2018 as the benchmark index fell 6.2 percent.

Proponents cite the healthcare sector’s reasonable valuations, strong balance sheets and dividend payments among many companies, as well as the group’s upbeat outlook for earnings, which are less susceptible to economic cycles than other businesses.

If economic growth is slowing, some investors are wary of being too invested in cyclical sectors that thrive during an upswing, but do not want to be too defensive either.

“We are trying to find things that skirt both of those two categorizations, and healthcare is a really nice diversified earnings stream,” said Noah Weisberger, managing director for U.S. portfolio strategy at Bernstein.

Such diversity stems from the variety of companies comprising the sector: manufacturers of prescription medicines, makers of medical devices, such as heart valves and knee replacements, health insurers, hospitals and providers of tools for scientific research.

From a stock perspective, that means the sector includes potential fast-growing stocks, such as biotechs that can carry more risk and more reward, or large pharmaceutical companies and others that offer steadier, slower growth.

Investment advisory firm Alan B. Lancz & Associates sold some pharmaceutical holdings late last year that had posted big gains, such as Merck & Co (MRK.N), to move into biotech stocks it believed were undervalued, said Alan Lancz, the firm’s president.

“We have maintained our overweighting, which is unusual for us with a sector that has outperformed so dramatically,” Lancz said. “But mainly there are segments within the sector that still offer opportunity.”

For 2019, healthcare companies in the S&P 500 are expected to increase earnings by 7.5 percent, ahead of the 6.3 percent growth estimated for S&P 500 companies overall, according to IBES data from Refinitiv.

Health insurer UnitedHealth Group Inc (UNH.N), the sector’s third-largest company by market value, kicks off fourth-quarter earnings season for healthcare on Tuesday.

“Healthcare is one of the few sectors with high quality, above-market growth and it’s relatively immune to the array of macro headwinds that we see out there,” said Martin Jarzebowski, sector head of healthcare for Federated Investors.

Healthcare shares could also benefit from anticipation of increased dealmaking activity after two large acquisitions of biotechs were already announced this year.

Despite healthcare’s outperformance last year, the sector is trading at the same valuation as the S&P 500 – 14.5 times earnings estimates for the next 12 months – whereas healthcare on average has held a premium over the market for the past 20 years, according to Refinitiv data.

The sector also is valued at a discount, by such price-to-earnings measures, to defensive sectors, including consumer staples .SPLRCS, which trades at 16.6 times forward earnings, and utilities .SPLRCU, which trades at 15.8 times.

According to the Reuters review of sector weightings, healthcare is followed by financials .SPSY, then technology .SPLRCT. Real estate .SPLRCR ranks as the most negatively rated group.

The healthcare sector has lagged in the early days of 2019, rising less than 1 percent against a 3 percent rise for the S&P 500.

Some investors doubt healthcare will maintain its outperformance. JP Morgan strategists downgraded the sector to “underweight” last month, pointing in part to political rhetoric possibly turning “more negative on healthcare leading up to the 2020 presidential elections.”

The healthcare sector struggled ahead of the 2016 election, with the high U.S. cost of prescription medicines a prominent issue during the presidential campaign. With renewed scrutiny on drug pricing, such concerns linger.

The sector could suffer if investors become more optimistic about economic growth and flee defensive stocks, while the popularity of healthcare as an investment could work against it if the trade becomes overly crowded.

“There is risk there,” said Walter Todd, chief investment officer at Greenwood Capital in South Carolina. But given issues affecting other sectors, he said, “when you look around the market…you arrive by default at healthcare, and so I think that’s why a lot of people are interested in the sector.”

The pharmaceutical industry’s 2 leading trade groups both set records for lobbying spending in 2018 — a sign of just how much the industry believes is on the line in the political battle over drug prices.

By the numbers:

Between the lines: PhRMA set its previous lobbying record during the debate over the Affordable Care Act, trying to stop a fully Democratic government from taking a bite out of its bottom line.

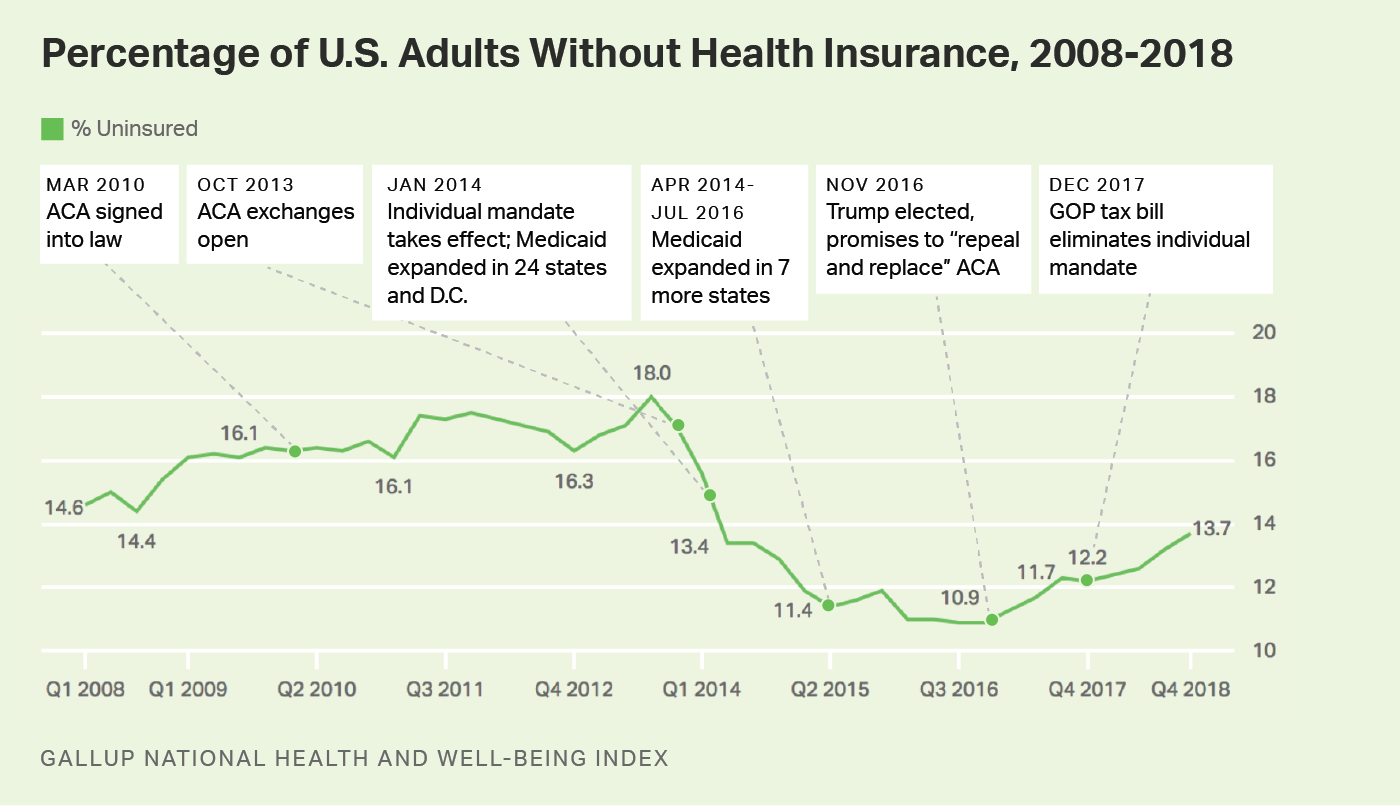

WASHINGTON, D.C. — The U.S. adult uninsured rate stood at 13.7% in the fourth quarter of 2018, according to Americans’ reports of their own health insurance coverage, its highest level since the first quarter of 2014. While still below the 18% high point recorded before implementation of the Affordable Care Act’s individual health insurance mandate in 2014, today’s level is the highest in more than four years, and well above the low point of 10.9% reached in 2016. The 2.8-percentage-point increase since that low represents a net increase of about seven million adults without health insurance.

Nationwide, the uninsured rate climbed from 10.9% in the third and fourth quarters of 2016 to 12.2% by the final quarter of 2017; it has risen steadily each quarter since that time. Since Gallup’s measurement began in 2008, the national uninsured rate reached its highest point in the third quarter of 2013 at 18.0%, and thus, the current rate of 13.7% — although it continues a rising trend — remains well below the peak level.

These data, collected as part of the Gallup National Health and Well-Being Index, are based on Americans’ answers to the question, “Do you have health insurance coverage?” Sample sizes of randomly selected adults in 2018 were around 28,000 per quarter.

The ACA marketplace exchanges opened on Oct. 1, 2013, and most new insurance plans purchased during the last quarter of that year began their coverage on Jan. 1, 2014. Medicaid expansion among 24 states (and the District of Columbia) also began at the beginning of 2014, with 12 more states expanding Medicaid since that time. Expanded Medicaid coverage as a part of the ACA broadens the number of low-income Americans who qualify for it to those earning up to 138% of the federal poverty level. The onset of these two major mechanisms of the ACA at the beginning of 2014 makes the uninsured rate in the third quarter of 2013 the natural benchmark for comparison to measure the effects of that policy.

The uninsured rate rose for most subgroups in the fourth quarter of 2018 compared with the same quarter in 2016, when the uninsured rate was lowest. Women, those living in households with annual incomes of less than $48,000 per year, and young adults under the age of 35 reported the greatest increases. Those younger than 35 reported an uninsured rate of over 21%, a 4.8-point increase from two years earlier. And the rate among women — while still below that of men — is among the fastest rising, increasing from 8.9% in late 2016 to 12.8% at the end of 2018.

At 7.1%, the East region, which has in recent years maintained the lowest uninsured rate in the nation, is the only one of the four regions nationally whose rate is effectively unchanged since the end of 2016. Respondents from the West, Midwest and South regions all reported uninsured rates for the fourth quarter of 2018 that represent increases of over 3.0 points. The South, which has always had the highest uninsured rate in the U.S. but has seen some of the greatest declines at the state level, has had a 3.8-point increase to 19.6%.

A number of factors have likely played a role in the steady increase in the uninsured rate over the past two years. One may be an increase in the rates of insurance premiums in many states for some of the more popular ACA insurance plans in 2018 (although most states saw premiums stabilize for 2019). For enrollees with incomes that do not qualify for government subsidies, the resulting hike in rates could have had the effect of driving them out of the marketplace. Insurers have also increasingly withdrawn from the ACA exchanges altogether, resulting in fewer choices and less competition in many states.

Other factors could be a result of policy decisions. The open enrollment periods since 2018 have been characterized by a significant reduction in public marketing and shortened enrollment periods of under seven weeks, about half of previous periods. Funding for ACA “navigators” who assist consumers in ACA enrollment has also been reduced in 2018 to $10 million, compared with $63 million in 2016. Overall, after open enrollment in the ACA federal insurance marketplace (i.e., healthcare.gov) peaked in 2016 at 9.6 million consumers, it declined by approximately 12.5%, to 8.4 million in 2019, based on recently released figures.

Other potential factors include political forces that may have increased uncertainty surrounding the ACA marketplace. Early in his presidency, for example, President Donald Trump announced, “I want people to know Obamacare is dead; it’s a dead healthcare plan.” Congressional Republicans made numerous high-profile attempts in 2017 to repeal and replace the plan. Although none fully succeeded legislatively, the elimination of the ACA’s individual mandate penalty as part of the December 2017 Republican tax reform law may have reduced participation in the insurance marketplace in the most recent open enrollment period.

Trump’s decision in October 2017 to end cost-sharing reduction could also potentially have affected the uninsured rate. The cost-sharing payments were made to insurers in the marketplace exchanges to offset some of their costs for offering lower-cost plans to lower-income Americans. The Trump administration had previously renewed the payments on a month-by-month basis but later concluded that such payments were unlawful. In April 2018, a federal court granted a request for a class-action lawsuit by health insurers to sue the federal government for failing to make the payments. Such lawsuits continue to be litigated.