https://www.modernhealthcare.com/article/20190116/NEWS/190119927/medicare-advantage-industry-sees-slower-growth-for-2019

Medicare Advantage insurers added 1.4 million members to their rosters for 2019 coverage, as they looked to grow membership in a market known for being politically safe and predictably lucrative. But Advantage membership is growing at a slower pace compared with previous years.

According to the latest federal data showing enrollment as of this month, 22.4 million people are enrolled in Medicare Advantage for 2019 coverage—an alternative to the traditional Medicare program in which private insurers contract with the federal government to administer program benefits. That’s an increase of 6.8% since January 2018. Health insurers, however, managed to grow their Advantage membership base by more than 1.5 million in both 2016 and 2017.

Some industry experts were expecting more. “The formula was there: Health plans were aggressive, they got nice rate increases, the rules around benefit design relaxed a little bit,” explained Jeff Fox, president of Gorman Health Group, which provides technology and other services to Medicare Advantage plans.

Fox expected Advantage enrollment to increase by double-digits over the past year, as health plans invested heavily in marketing and the federal government provided one of the biggest rate increases for the plans in years at 3.4%. The Trump administration also granted Advantage plans the flexibility to provide more supplemental benefits in 2019, such as transportation and in-home care.

But Fox said distraction from the craziness of the November midterm elections may have kept some seniors from enrolling during the annual open enrollment that lasted from Oct. 15 to Dec. 7, 2018. While the CMS data captures some of the sign-ups from open enrollment, figures out next month are likely to be higher.

Despite the slower pace, many Advantage insurers still experienced big enrollment increases as they picked up more market share. About half of all members are covered by just three companies. UnitedHealth held onto the top spot, adding nearly 500,000 Advantage members in the past year for a total 5.7 million. UnitedHealth holds more than a quarter of the total Medicare Advantage market share.

Humana remained the No. 2 Advantage insurer with 3.9 million members, an increase of 10.4% over January 2018. But thanks to its acquisition of Aetna, CVS Health took the No. 3 spot with 2.2 million Advantage enrollees. Kaiser Foundation Health Plan and Anthem rounded out the top five insurers with the most Advantage members.

On a percentage basis, Anthem and Aetna grew membership the fastest. Anthem’s Medicare Advantage membership spiked 53% to 1.1 million members compared with the same time last year. The Indianapolis-based insurer has long focused on serving employers, but recently turned its sights to growing Medicare Advantage rolls through acquisitions and expansions in places where it already operates.

Anthem bought Florida-based Medicare plans HealthSun in December 2017 and America’s 1st Choice in February 2018, together giving Anthem about 170,000 more Advantage members. Anthem CEO Gail Boudreaux told investment analysts in July that the company would focus on selling group Medicare Advantage plans and serving medically complex dual-eligible members in 2019.

CVS Health, meanwhile, grew its Medicare membership by 26.7% in 2018 to 2.2 million through its acquisition of Aetna. The deal is still technically awaiting a federal judge’s approval. In a research note Monday, Barclays equity analyst Steve Valiquette noted that Aetna’s membership growth was driven by its expansion into about 360 new counties. Valiquette wrote that the growth experienced by some public health insurers during the annual enrollment period for 2019 coverage was driven more by market share gains than by industry growth.

Medicare Advantage enrollment is climbing as the baby boomer generation ages rapidly into Medicare. Those seniors are used to employer-sponsored managed-care plans and are choosing Advantage over traditional Medicare more often than previous generations did. Seniors also often get more benefits, including dental care, eyeglasses and gym memberships, with an Advantage plan.

Medicare Advantage also enjoys support from both political parties and is able to weather swings from one federal administration to the next, whereas insurers that sell plans in the individual market, for example, may have to deal with more volatility.

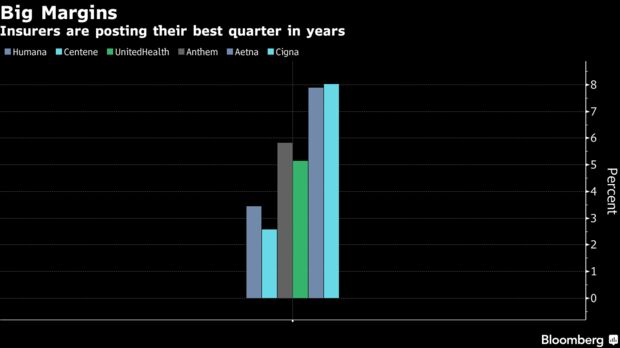

Moreover, Medicare Advantage margins tend to hover between 4% to 5%, whereas Medicaid margins come in at 2% to 3% and the individual market historically has had even lower margins, S&P analyst Deep Banerjee told Modern Healthcare in August. The group employer business has higher margins, but that market isn’t growing like Medicare Advantage is.