Thought of the Day: What Defines Us

https://mailchi.mp/79ecc69aca80/the-weekly-gist-december-15-2023?e=d1e747d2d8

Last week, the Food and Drug Administration (FDA) approved two gene therapy treatments for sickle cell disease, Casgevy and Lyfgenia.

Casgevy, jointly developed by Boston, MA-based Vertex Pharmaceuticals and Switzerland-based CRISPR Therapeutics, is the first approved treatment of any kind available to US patients that uses CRISPR’s gene-editing capabilities.

Lyfgenia, made by Somerville, MA-based Bluebird Bio, uses a more common retrovirus technique for genetic modification. The FDA estimates that about 20K Americans with sickle cell disease will be eligible for the therapies, limited to those patients 12 and older who have had episodes of debilitating pain.

Both treatments will only be available at a small number of facilities nationwide, priced between $2-3M, and require a patient to endure months of hospitalization as well as intensive chemotherapy. Around 100K mostly Black Americans suffer from sickle cell disease, which causes intense pain, organ damage, and reduced life expectancy. Previously, the only curative treatment was a bone marrow transplant.

The Gist: The approval of these drugs represents a milestone moment for those suffering from sickle cell disease, while Casgevy also fulfills the revolutionary promise scientists have seen in CRISPR since it first received broad attention in 2005.

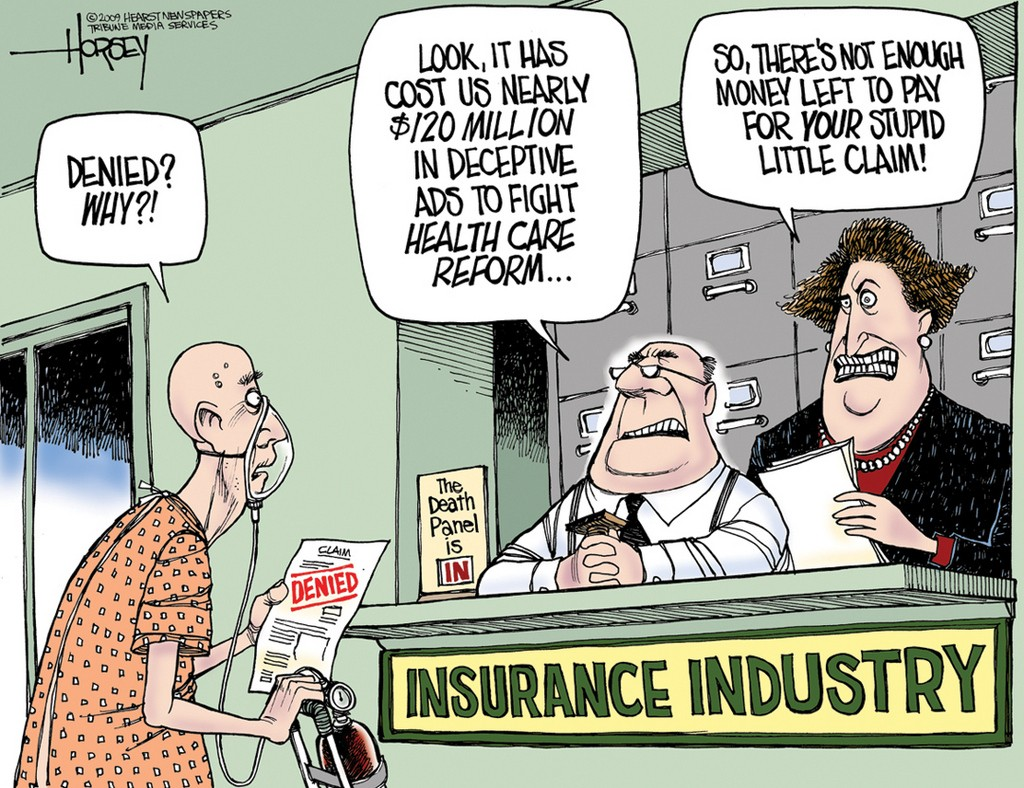

However, now that gene-editing therapies have graduated from the domain of scientific possibility into the realities of our healthcare delivery system, the new challenge becomes ensuring accessibility and equity, as many Americans who most stand to benefit from it also experience barriers in access to care and insurance coverage. (We’d expect insurer pushback similar to that seen when the first highly effective, but extremely costly, hepatitis C treatments like Solvaldi hit the market a decade ago this month.)

While the clinical trial patients who received Casgevy report having “a new lease on life”, sky–high costs, questions of insurance coverage, and the arduous, time-intensive nature of the procedure stand in the way of a population-wide cure for sickle cell disease.

https://mailchi.mp/79ecc69aca80/the-weekly-gist-december-15-2023?e=d1e747d2d8

After a presentation this week, a senior physician from the audience of our member health systems reached out to discuss a well-trod topic, the future of health reform legislation. But his question led to a more forward-looking concern:

“You talked very little about politics, even though we have an election coming up next year. Are you anticipating that Medicare for All will come up again? And what would the impact be on doctors?”

As we’ve discussed before, we think it’s unlikely that sweeping health reform legislation like Medicare for All (M4A) would make its way through Congress, even if Democrats sweep the 2024 elections—and it’s far too early for health systems to dedicate energy to a M4A strategy.

Healthcare is not shaping up to be a campaign priority for either party, and given the levels of partisan division and expectations that slim majorities will continue, passing significant reform would be highly unlikely.

Although there is bipartisan consensus around a limited set of issues like increasing transparency and limiting the power of PBMs, greater impact in the near term will come from regulatory, rather than legislative, action.

For instance, health systems are much more exposed by the push toward site-neutral payments. How large is the potential hit? One mid-sized regional health system we work with estimated they stand to lose nearly $80M of annual revenue if site-neutral payments are fully implemented—catastrophic to their already slim system margins.

Preparing for this inevitable payment change or the long-term possibility of M4A both require the same strategy: serious and relentless focus on cost reduction.

This still leaves a giant elephant in the room: the long-term impact on the physician enterprise.

As referral-based economics continue to erode, health systems will find it increasingly difficult to maintain current physician salaries, further driving the need to move beyond fee-for-service toward a health system economic model based on total cost of care and consumer value, while building physician compensation around those shared goals.

https://mailchi.mp/79ecc69aca80/the-weekly-gist-december-15-2023?e=d1e747d2d8

This week’s graphic highlights increasing tensions between health systems and Medicare Advantage (MA) plans as they battle over what providers see as unsatisfactory payment rates and insurer business practices.

On paper, many providers have negotiated rates with MA plans that are similar to traditional fee-for-service Medicare, but find MA patients are subject to more prior authorizations and denials, as well as delayed discharges to postacute care, which increases inpatient length of stay and hospital costs.

A number of health system leaders have reported their revenue capture for MA patients dropped to roughly 80 percent of fee-for-service Medicare rates due to an increase in the mean length of stay for MA patients, caused by carriers narrowing postacute provider networks.

As a result, a growing number of health systems and medical groups have either already exited, or plan to exit, MA networks due to what they see as insufficient reimbursement.

Health systems with a strong regional presence may be able to leverage their market share to get MA payers to play ball. But for health systems in more competitive markets, these hardline negotiation tactics run the risk of payers merely directing their patients elsewhere.

Regardless of market dynamics, providers exiting insurance plans is extremely disruptive for patients, who won’t understand the dynamics of payer-provider negotiations—but will feel frustrated when they can’t see their preferred physicians.

https://mailchi.mp/79ecc69aca80/the-weekly-gist-december-15-2023?e=d1e747d2d8

Published last week in the Wall Street Journal, this piece predicts that the era of immense profitability for Medicare Advantage (MA) insurers may be drawing to a close.

MA has experienced rapid growth over the past decade, due both to the pace of Baby Boomers aging into Medicare, and the increasing numbers of beneficiaries choosing MA plans. In 2023, MA surpassed 50 percent of total Medicare enrollment.

Payers readily embraced the MA market because they found they could earn gross margins two to three times higher than from a commercial life.

However, as the rate of enrollment growth begins to slow (the last of the Boomers will turn 65 in 2030), competition between payers increases, and government payments become less generous, the MA business—while still profitable—is poised to become less of a jackpot.

The Gist: While MA has been an outsized driver of profits for insurance companies in recent years, the nation’s two largest MA payers, UnitedHealth Group (UHG) and Humana, have been signaling growing concerns to the market.

UHG announced late last month that its 2024 MA enrollment growth will be less than half of its 2023 rate, and Humana has been engaged in merger talks with Cigna.

As the “gold rush” period ends, MA payers will have to earn their keep by better integrating their various care and data assets, and more carefully managing spending for an aging cohort of seniors with increasingly complex needs, both much harder than riding a demographic wave to easy profits.