Currently there is a resolution HR 7995 in the U.S. House of Representatives, introduced late last week, that will decrease prior authorization delays for patients awaiting care.

The very manual, time-consuming processes, for prior authorization, burden physicians, physician practices, and hospitals while diverting valuable resources away from direct patient care. HR 7995 was referred to the Committee on Ways and Means in addition to the Committee on Energy and Commerce.

Now that the framework of this bill is still being worked, it is crucial to get in front of legislators and let them know that you support this legislation that will decrease prior authorization delays ensuring continuity of care to patients because it:

Exempts qualifying physicians from prior authorization requirements under Medicare Advantage (MA) (providing for a “Gold Card” status for physicians that consistently meet prior authorization requirements).

Allows physicians to appeal “Gold Card” revocation from insurers that are wrongly decided.

Requires Secretary of HHS to issue rules on MA plans.

Medicare currently pays for Hospital at Home using a top-down (hospital-centered) payment—the payment is made to hospitals, and the amount is based on Medicare’s payment system for acute inpatient admissions. An alternative, bottom-up approach could generate a payment amount on the basis of existing home-based care payment systems, with additions for the expanded services needed for the more acute patients in a Hospital at Home model. Because home care providers are typically reimbursed at lower rates, this approach to payment would be less expensive and could capitalize on the existing in-home care expertise these providers have, while expanding their reach to a higher-acuity patient population. The co-authors have compared payment options for home hospitalization programs under both the top-down and bottom-up approaches.

Transformation Challenges

The Hospital at Home delivery model faces three significant and related challenges to expansion—generating a sufficient volume of patients to keep local programs in business, achieving cost efficiencies, and defining appropriate patients (not so sick that the patients will fail to heal or be in danger but not so healthy that they don’t need Hospital at Home).

Any health care innovation needs patient volume to be viable. A Hospital at Home program requires teams that can immediately access and deliver all needed care, including diagnostics, monitoring, pharmaceuticals, and nursing services. It also requires physicians adept at working with home-based patients while coordinating all aspects of care. Patient intake and discharge must be handled promptly, including care plans for the patient during their Hospital at Home “stay” and transitioning the patient to their regular providers after the acute phase. Much, but not all, of this infrastructure exists in home health agencies, but Hospital at Home patients typically have more time-sensitive and intense needs than the usual home health patient, which will require some staff expansion by a home health agency seeking to run a Hospital at Home program. A few patients a day will not likely generate enough revenue to maintain the staff expertise or the infrastructure needed to deliver all the different services Hospital at Home patients need.

While it might seem logical that Hospital at Home programs would be sponsored and operated by individual hospitals, many hospitals would not generate sufficient volume to support their own program. In 2019, the national average discharge rate per hospital bed was about 33 per year, and about half were Medicare beneficiaries. A large hospital with 1,000 beds might have 15,000 Medicare discharges per year. On average, we found about 5 percent of Medicare discharges would be eligible for Hospital at Home—only about 15 per week for a 1,000-bed hospital. A program sponsored by a particular hospital might not receive referral patients from competing hospitals because the competing hospitals would be losing patient volume and revenue, and except for extremely large hospital systems, most hospitals would not generate sufficient volume to support the program. A program that serves multiple hospitals will likely have advantages of scale.

When it comes to cost, hospital-based services are well-known to bear facility overhead expenses, which can make hospital-based services more expensive than services delivered from other sites. Medicare pays for hospital inpatient services mostly using diagnosis-related groups. Medicare pays a pre-set amount for each kind of admission, regardless of the actual cost accrued by the provider for a particular patient. But as our analysis shows, starting with Medicare’s home care reimbursement saves the payer more than 50 percent of an acute patient stay, when considering all facility, professional, and ancillary services. Of course, the lower price is appealing to a payer, such as a Medicare Advantage plan, but it could also save a patient money in reduced cost sharing.

Identifying the right patients for medical interventions has been a challenge for decades.The goal is to strike the right balance: avoiding unnecessary care but not skimping on needed care. To promote efficiency and outcomes, private payers and Medicare apply utilization management reviews and quality monitoring. Even for patients appropriate for Hospital at Home, hospitals may dislike the programs, as they fail to see the value of home-based care delivery in the face of many unfilled inpatient beds. On the other hand, home health agency-based Hospital at Home programs could see financial gains and tend to over-use such programs. All of this must be balanced with patient perceptions and acceptance of such programs. Participants who have piloted both top-down and bottom-up models have found substantially higher patient acceptance in models that allow entry to a Hospital at Home admission without an emergency department visit, which is typically required of top-down models. Clearly, use and quality management programs will be needed to achieve the right balance of these competing interests, and value based programs can help align incentives as well.

Bottom Line

Most research and proposals for implementing home hospitalization programs assume they are an extension of hospital operations and assume hospital costs and reimbursement. But there are cost and other advantages to building home hospitalization on the foundation of home-based care providers, whose expertise includes keeping patients safe and healthy at home. Policy makers who design reimbursement for home hospitalization programs and set conditions for providers to participate in them should consider whether home-based care providers should be eligible to manage, or play a foundational role in, these programs. This could simultaneously save payers money, create operational efficiencies, and increase patient access. Physicians and hospitals sponsoring these programs should similarly consider the roles home-based care providers could play within current home hospitalization programs. Simply extending the reach of hospitals into patients’ homes is unlikely to allow the promising scale or cost savings stakeholders hope for from home hospitalization programs. Each year, hundreds of thousands of Medicare patients could benefit.

The for-profit, 39-hospital Steward system manages 171K lives across the Medicare Advantage, Medicare shared savings, and Medicare direct contracting programs. This deal will allow Miami-based CareMax, a publicly-traded, value-based care company with 42 senior centers (mostly in Florida) and 34K lives under management, to expand across Steward’s footprint, which includes Texas and Arizona, states with rapidly growing Medicare populations.

The Gist:This deal is an example of the rise of venture-funded MSO (medical services organization) services that aim to subsume and scale value-based care functions from hospitals and medical groups. Steward wagers it can find greater success in managing risk in partnership with CareMax, moving a greater share of its Medicare population into risk, and outsourcing care management and patient engagement functions.

Many health systems have spent substantial resources building out accountable care organizations and risk-based Medicare businesses over the last decade. While selling these assets to a company like CareMax may be one way to generate a return, particularly for those frustrated by lower-than-anticipated gains from moving to value-based care, it also requires relinquishing control of functions likely central to the future health system business model.

The momentum behind Medicare Advantage is only growing as more baby boomers age into eligibility, and experts don’t expect the energy around the program to slow down any time soon.

A recent analysis from the Kaiser Family Foundation found that a record 3,834 plans were available for the 2022 plan year in MA, which represents an 8% increase over 2021 and the largest number on the market in a decade.

Open enrollment for Medicare ended Dec. 7, and enrollment numbers will begin trickling out as the year winds down. In 2021, 26 million Medicare beneficiaries, or about 42% of those eligible for the program, were enrolled in an MA plan.

“As Medicare Advantage enrollment continues to grow, insurers seem to be responding by offering more plans and choices to the people on Medicare,” the KFF analysts said.

Part of the appeal of MA to an increasingly savvy consumer base is that it offers additional benefits beyond those afforded people in traditional Medicare, such as vision and dental coverage as well as supports for members’ social needs.

Sachin Jain, M.D., CEO of SCAN Health Plan, told Fierce Healthcare that people are increasingly shopping around for plans, building greater awareness of MA as a whole as well as of the different types of benefits beneficiaries could select.

“We’re seeing that consumers are more sophisticated today than they were a decade ago,” he said. “I think people are realizing that fee-for-service Medicare doesn’t cover a lot of things.”

The KFF report shows that more than 90% of non-group MA plans offer some kind of vision, hearing, telehealth or dental benefits and that most (89%) include prescription drug coverage as well.

Elena McFann, president of Medicare at Anthem, told Fierce Healthcare that throughout the open enrollment period, plans built with benefits that target the social determinants of health and promote whole-person care resonated strongly with members.

Anthem, for example, offers plans that include a slate of essential extra benefits that members can choose from based on what they need the most. Options include grocery cards, transportation benefits and in-home supports.

She said that the grocery benefits and flex cards that allow members to purchase additional hearing, vision and dental coverage have proven particularly popular in this enrollment season.

“What those all point to is the concept of flexibility and helping them lead healthier lives where they really need the help where they are in their journey,” McFann said.

As these benefits prove popular, an increasing number of plans are offering them in tandem. The Better Medicare Alliance released a survey late last month that found the number of plans including supplemental benefits grew by 43% for the 2022 plan year.

The Centers for Medicare & Medicaid Services (CMS) has issued additional flexibilities that allow MA plans to address members’ social determinants of health as the program’s enrollment continues to swell.

Jain said SCAN has seen similar interest in supplemental benefits, and that flexibility afforded to MA plans to adapt to seniors’ needs and expectations is a critical factor in the program’s success.

“When you’re in the business of serving seniors, a lot of what you have to do is anticipate needs that those seniors may not anticipate that they have, give them things they didn’t know they needed,” he said.

McFann said that beneficiaries value plans like these that unite brands they trust and recognize and that partners like Kroger enable insurers to more effectively meet seniors where they are. In its co-branded plans, members can access benefits like Healthy Grocery Cards and stipends to purchase over-the-counter health items.

She said that there has been significant “excitement” around those plans, which are available in four states, during the current enrollment period.

“It gives the Medicare eligibles a sense of familiarity and a sense of comfort, again meeting them on their terms,” McFann said.

However, while many established insurers have set ambitious growth targets in this market and new startups enter the space regularly, they still have plenty of work to do if they want to catch up with the market’s dominant forces: UnitedHealthcare, Humana and Blues plans.

UHC and Humana together account for 45% of the MA market in 2021, according to the KFF analysis. Humana offers plans in 85% of counties and UHC in 74% for 2022.

That means, 89% of Medicare eligibles have access to a Humana plan and 90% have access to a UHC MA plan if they choose, according to the report.

Competition is continuing to grow, though, and both McFann and Jain said they don’t feel the momentum around MA slowing down anytime soon.

“It is those extras and social drivers of health solutions that really have caught on with the Medicare-eligible segment and we expect to see that expand even further,” McFann said.

A recent piece in JAMA argues that policymakers need to be proactive in addressing how the rise of MA enrollment will affect the Medicare program as a whole, including its role in national quality and utilization measurement, rural healthcare access, and graduate medical education. The ability to monitor care delivered to the traditional, fee-for-service Medicare beneficiary population has been critical for assessing cost growth and shifting care patterns, distributing subsidies, and basing MA payments—all things that will become increasingly difficult as traditional Medicare becomes both smaller and less representative of the entire Medicare population.

The Gist: Traditional Medicare has been a springboard for national healthcare policy goals and industry-wide innovations. However, consumers’ preference for, and policy shifts supporting, the growth of Medicare Advantage are proving to be unstoppable.

Providers must prepare for a future in which a shrinking minority of beneficiaries are enrolled in traditional Medicare. If current trends continue, Medicare policymakers must bolster ongoing support for medical education, and build a higher standard of transparency and quality reporting for MA carriers and providers to maintain the sustainability of one of the country’s greatest healthcare data resources.

Medicare Advantage (MA) is the private insurance alternative to traditional Medicare. MA organizations contract with Centers for Medicare and Medicaid Services (CMS) to offer eligible beneficiaries residing in a defined geographic service area (a collection of counties) a selection of private plans. Insurers may offer multiple plans across different plan types under one contract. The service area is defined at the contract-level, and for most MA plans, service areas can include a single county or a collection of multiple counties. (There are other types of plans for which there are constraints on the boundaries of the service area, but these don’t account for very much of MA enrollment.)

As MA-offering insurers contract with CMS, they establish networks that govern patient liability for seeing in- and out-of-network providers. Consequently, plans will vary in their cost-sharing structures and benefit designs as they assume different levels of liability for the cost of out-of-network providers. Overall, plans will cover the cost of care (less copays and deductibles) for patients seeing providers in-network, and certain plan types may require that patients pay more for out-of-network services or receive referrals/prior authorization from primary care providers (PCP) to see specialists.

Preferred Provider Organizations (PPOs) are considered the most flexible type of plan in providing access to care and covering it out-of-network. PPO enrollees can use out-of-network providers for covered services without a referral from a PCP, albeit at greater cost to them than in-network providers.

Health Maintenance Organizations (HMOs), in comparison to PPOs, are more restrictive plans that provide less access to care and less coverage for out-of-network providers, with the exception of emergency, urgent, and dialysis care. HMO members are required to select a PCP and must get authorization for most specialty services. For any out-of-network services received, the patient bears the full cost, up to the traditional Medicare rate.

Health Maintenance Organization Point-of- Service (HMO-POS) are a hybrid plan between PPOs and HMOs. Like an HMO, members must select a PCP for care coordination, but they do not need a referral for specialty services. (However, some services may require prior authorization for coverage.) Like a PPO, this plan does provide some coverage for out-of-network providers.

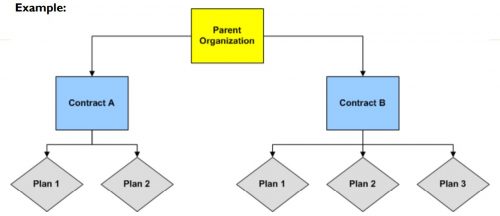

The differences across plan types in access to and cost sharing for out-of-network providers leads to the important question, do MA networks vary by plan within contract? For example, in Figure 1 below, do the beneficiaries enrolled in Plan 1 or 2 under Contract A have the same set of in- and out-of-network providers (likewise for the beneficiaries in Plans 1-3 under contract B)? More specifically, what if Plan 1 is an HMO and Plan 2 is a HMO-POS plan, do they share the same network?

The simple answer seems to be: not necessarily, though more recent regulations attempt to push insurers toward having the same networks across plans within contracts.

For instance, prior to 2019, CMS only reviewed the adequacy of an MA organization’s contracted network under a “triggering event,”like if an organization were to operate a new plan, expand coverage to additional service areas, or in a response to inadequate network complaints. The scope of CMS’ review varied depending on the triggering event that occurred. In some cases, CMS could only conduct partial reviews of a contract’s network, looking at a select set of specialties or counties. A study by the US Government Accountability Office found that between 2013 and 2015, CMS had reviewed less than 1% of all networks. Without regular scrutiny by regulators, it seems likely that networks varied across plans within contracts.

Under the current MA Network Adequacy Criteria Guidance, CMS assesses network adequacy requirements both under triggering events (as explained above) and, separate from that, on a triennial-basis at the contract-level. CMS has previously commented in the 2021 Final Rule that this approach allows them to assess the adequacy of organizations’ networks across all of their plan types (HMOs, PPOs, SNPs) and consider the broadest availability of providers and facilities for an organization. Again, this suggests that insurers may vary networks across plans within contracts.

There are at least two scenarios for which we know certain plans can and likely do have different networks compared with other plans in the contract.

Special Needs Plans (SNPs) are plans designed for individuals with specific diseases or characteristics, such as those who are dual-eligible, have institutional care needs, or have a chronic condition. SNPs can be allowed by regulators to augment the contract’s network to integrate care management teams and specialty providers to accommodate beneficiaries’ complex care needs under the plan’s Model of Care. While SNPs may be granted additional flexibility to alter the contract-level networks established, CMS does not allow SNPs to narrow or shrink that network. They can only expand it.

Provider Specific Plan (PSPs) are plans often found under large, integrated medical groups or provider groups that are the primary bearers of risk. PSP enrollees have access to a smaller subset of in-network providers. Since this plan type has a network of fewer providers than the overall contracted network, organizations must request to offer a PSP from CMS and attest that these plans are in compliance with network adequacy requirements.

Future work with Vericred provider-network data could be one approach to exploring variations in networks among plans under the same contract and service area, beyond the cases listed above. If networks are varying across HMO, PPO, and HMO-POS plans within contracts, it would be interesting to explore just how different they are from one another. Moreover, as CMS reviews continues to review network adequacy requirements at the contract-level (and if networks do differ by plan), one should consider the breadth of the network that organizations are submitting for evaluation. To what extent all plans in a contract are in compliance with network adequacy rules warrants future investigation.

The American Hospital Association, on behalf of its nearly 5,000 healthcare organizations, is urging the Justice Department to probe routine denials from commercial health insurance companies.

Specifically, the AHA is asking the Justice Department to establish a task force to conduct False Claims Act investigations into the insurers that routinely deny payments to providers, according to a May 19 letter to the department.

The request from the AHA comes after HHS’ Office of Inspector General released a report April 27 that found Medicare Advantage Organizations sometimes delayed or denied enrollees’ access to services although the provider’s prior authorization request met Medicare coverage rules.

“It is time for the Department of Justice to exercise its False Claims Act authority to both punish those MAOs that have denied Medicare beneficiaries and their providers their rightful coverage and to deter future misdeeds,” the AHA said in a letter to the Justice Department. “This problem has grown so large — and has lasted for so long — that only the prospect of civil and criminal penalties can adequately prevent the widespread fraud certain MAOs are perpetrating against sick and elderly patients across the country.”

On Thursday CMS announced it will replace all versions of its Global and Professional Direct Contracting (GPDC) model, which allowed primary care providers to take full or partial risk on managing cost of care for traditional Medicare beneficiaries, after progressive Democrats raised concerns about whether a growing presence of Medicare Advantage insurers and private equity-backed groups in the model might compromise patient care and access in the traditional Medicare program. GPDC will be replaced with a new three-year demonstration called Accountable Care Organization Realizing Equity, Access and Community Health (ACO REACH), to start enrollment in 2023. The 51 current participants in the GPDC model can move into ACO REACH as long as they meet new requirements, which include developing plans to identify and address health disparities, and ensuring providers control three quarters of governing boards (as compared to a quarter in the GPDC model). Private equity and insurer applicants can still apply, but must demonstrate a track record of direct patient care, delivering quality outcomes, and serving vulnerable populations.

The Gist: ACO REACH is largely a “re-skinning” of the Direct Contracting program, rather than a significant overhaul. Physician, health system, and ACO groups, who were concerned that the program would be canceled altogether, were pleased with the announced changes to the model, although debate continues on whether the new guardrails will effectively address concerns around for-profit insurer and investor participation.

Like Direct Contracting before it, ACO REACH will be an important vehicle for risk-ready providers to move more extensively into full-risk contracting, without launching a plan or partnering directly with a MA insurer.

The Mayo Clinic in Minnesota is no longer scheduling appointments for patients in most Medicare Advantage plans, and has been gradually notifying patients throughout the year, in a move that could have consequences for insurers operating plans in the area, according to a Mayo Clinic spokesperson.

Some insurers, such as UnitedHealthcare, have been negotiating with the Mayo Clinic to bring them in-network for Medicare Advantage, in some cases asking them to outline their requested terms, but Mayo to date has yet to send out proposals.

Mayo has long been out of network for most Medicare Advantage plans, but has historically treated out-of-network MA patients and accepted their benefits, according to Mayo Clinic spokesperson Karl Oestreich.

According to the Star Tribune, the change occurred because Mayo saw a significant increase in patients covered by “non-contract” MA insurers. That increase, officials said, threatens to crowd out patients covered by in-network insurers.

Non-contract MA plans are those in which insurance companies have not negotiated payment rates for services with Mayo.

UnitedHealthcare, which has been out of network, is negotiating to bring Mayo in-network for MA members, according to Dustin Clark, vice president for communications at UHC.

“We have asked Mayo Clinic to outline requested terms to join our network for Medicare Advantage and haven’t received a proposal,” he told Healthcare Finance News. “We are committed to reaching an agreement at an affordable cost for the people we serve. We stand at the ready to work with Mayo to end this disruption.”

For UHC, it’s especially important that MA patients who traditionally received care at Mayo can continue to do so in the future.

“Although Mayo Clinic does not participate in our network for Medicare Advantage, many of our members have received treatment from its physicians as part of their out-of-network benefits,” said Clark. “We understand how difficult this situation is for some of our members, which is why we are working with Mayo to ensure our Medicare Advantage members who are currently undergoing treatment or have an established relationship with the clinic can continue to see their physician.”

Mayo Clinic spokesperson Karl Oestreich said that medical need is the primary criteria for obtaining an appointment.

“In situations where medical need does not apply and to ensure appointments remain available for our Mayo Clinic patients, we no longer schedule routine visits for those whose coverage does not include Mayo Clinic,” he said. “Continuity of care and relationships with existing local and regional patients won’t be compromised.”

The primary issue, said Oestreich, is capacity, not reimbursement. He said Mayo doesn’t have the capacity to serve an ever-increasing number of patients, and needs to remain a good steward with its contracted plans.

“There was not a policy change, but a shift in enforcement to ensure Mayo has access for our contracted plans (not just Medicare) and those who truly need Mayo’s medical expertise,” he said. “This long-standing policy applies to all payers, not just Medicare Advantage.”

“The impact is to non-contract Medicare Advantage plans,” said Oestrich. “Mayo does not have contracts with these plans. Mayo is open to entering new contracts, but also must keep in mind the impact on capacity to ensure that we can continue to see those patients (regardless of payer) who are in the greatest need of the care Mayo provides.

“We understand that affected patients may be disappointed and frustrated. Patients should always ask their brokers and insurers whether their plans specifically have in-network coverage at Mayo Clinic.”

THE LARGER TREND

UnitedHealthcare, which already has significant market control with its MA plans, said it will strengthen its foothold in the space by expanding its MA plans in 2022, adding a potential 3.1 million members and reaching 94% of Medicare-eligible consumers in the U.S.

While UnitedHealthcare has a massive foothold in the Medicare Advantage space, it underwent scrutiny from the federal government earlier this month, when the Centers for Medicare and Medicaid Services blocked four Medicare Advantage plans from enrolling new members in 2022 because they didn’t spend the minimum threshold on medical benefits. Three UnitedHealthcare plans and one Anthem plan failed to hit the required 85% mark three years in a row.

Medicare Advantage plans are required to spend a minimum of 85% of premium dollars on medical expenses. Failure to do so for three consecutive years triggers the sanctions.

For UHC, the penalties apply to its MA plans in Arkansas, New Mexico and the Midwest, which encompasses Missouri, Kansas, Nebraska and Iowa. UHC plans cover about 83,000 members, and the Anthem plan covers about 1,200 members. They cannot offer select plans to members until 2023, assuming they hit the 85% threshold next year – what’s called the medical loss ratio. If they fail to hit the threshold for five years in a row, the government will terminate the contracts.

UHC representatives told Bloomberg that it missed the 85% benchmark in certain markets in part because of patients deferring medical care due to the COVID-19 pandemic.

Last week, we examined how the fast-growing Medicare Advantage (MA) market remains heavily concentrated among a handful of large carriers. But amid this concentration, consumers have more options than ever before, both in terms of carriers and plans, as shown in the graphic below.

The average MA enrollee can now choose from among 39 health plans offered by nine different payers, the majority of which feature $0 insurance premiums. An increasing number of plans also now offer a variety of non-medical benefits.

Landing an MA consumer soon after they become eligible is critical for carriers, as more than seven in 10 Medicare beneficiaries stick with the plan they have year after year. While this “stickiness” may suggest enrollees are satisfied with their current coverage, it also calls into question whether the MA marketplace is actually working as intended.

With another revenue boost to MA plans proposed for 2023, competition between plans—as well as consolidation among carriers—will continue to heat up, especially as the number of Medicare-eligible Americans will increase by nearly 50 percent over the next three decades.