The Trump administration is shaking up how health systems are paid for outpatient care with a plan that could reduce Medicare hospital spending by nearly $11 billion over the next decade.

Why it matters:

It’s a big step forward for “site-neutral” payment policies that have been touted as a way to save taxpayers and patients money, but that hospitals say will lead to service cuts, especially in rural areas.

Driving the news:

Medicare administrators on Friday finalized a proposal to reduce what the government pays hospitals to administer outpatient drugs, including chemotherapy, at off-campus sites.

The move would equalize payment rates to hospitals and physician practices for the same services — an idea that Congress debated last year but didn’t act on in the face of aggressive hospital lobbying.

Medicare now pays about $341 for chemotherapy administration in hospital outpatient facilities, compared with $119 for the same service delivered in a doctor’s office.

Medicare next year will also start to phase out a list of more than 1,700 procedures and services only covered when they’re delivered in an inpatient setting.

What they’re saying:

The policy changes will give seniors more choices on where to get a procedure and potentially lower out-of-pocket costs at an outpatient site, the Centers for Medicare and Medicaid Services said.

Some health policy experts said the change will help make Medicare more affordable.

“We hope the administration will continue its efforts and adopt site neutrality for other services in future rules,” Mark Miller, executive vice president of health care at Arnold Ventures, said in a statement.

The other side:

“Both policies ignore the important differences between hospital outpatient departments and other sites of care,” Ashley Thompson, a senior vice president at the American Hospital Association, said in a statement.

“The reality is that hospital outpatient departments serve Medicare patients who are sicker, more clinically complex, and more often disabled or residing in rural or low-income areas than the patients seen in independent physician offices.”

Hospital outpatient departments still will see an $8 billion overall increase in their Medicare payments in 2026.

But the Trump administration contends that new technologies and other factors are shortening recovery times for procedures done on an outpatient basis.

Between the lines:

Health systems still scored a small win when CMS dropped a plan to speed up the repayment of $7.8 billion in improper cuts the first Trump administration made to safety-net providers’ reimbursements in the federal discount drug program.

The policy would have clawed back the money from hospitals’ Medicare reimbursements. Scrapping the idea “helps preserve critical resources for patient care during an already challenging time,” Soumi Saha, senior vice president of government affairs at Premier, said in a statement.

Still, CMS said it may try again in 2027. And law firm Hooper Lundy Bookman is already sending out feelers to hospitals willing to challenge the version of the repayment plan that will go into effect next year, per an alert sent Friday night.

What we’re watching:

Whether health systems challenge the site-neutral payment changes. The hospital payment plan came weeks later than expected and will make it harder for facilities to update billing, revise their budgets and train staff, Saha said.

The administration is also launching a survey of hospitals’ outpatient drug acquisition costs next year, which is seen as a prelude for cutting reimbursements under the discount drug program.

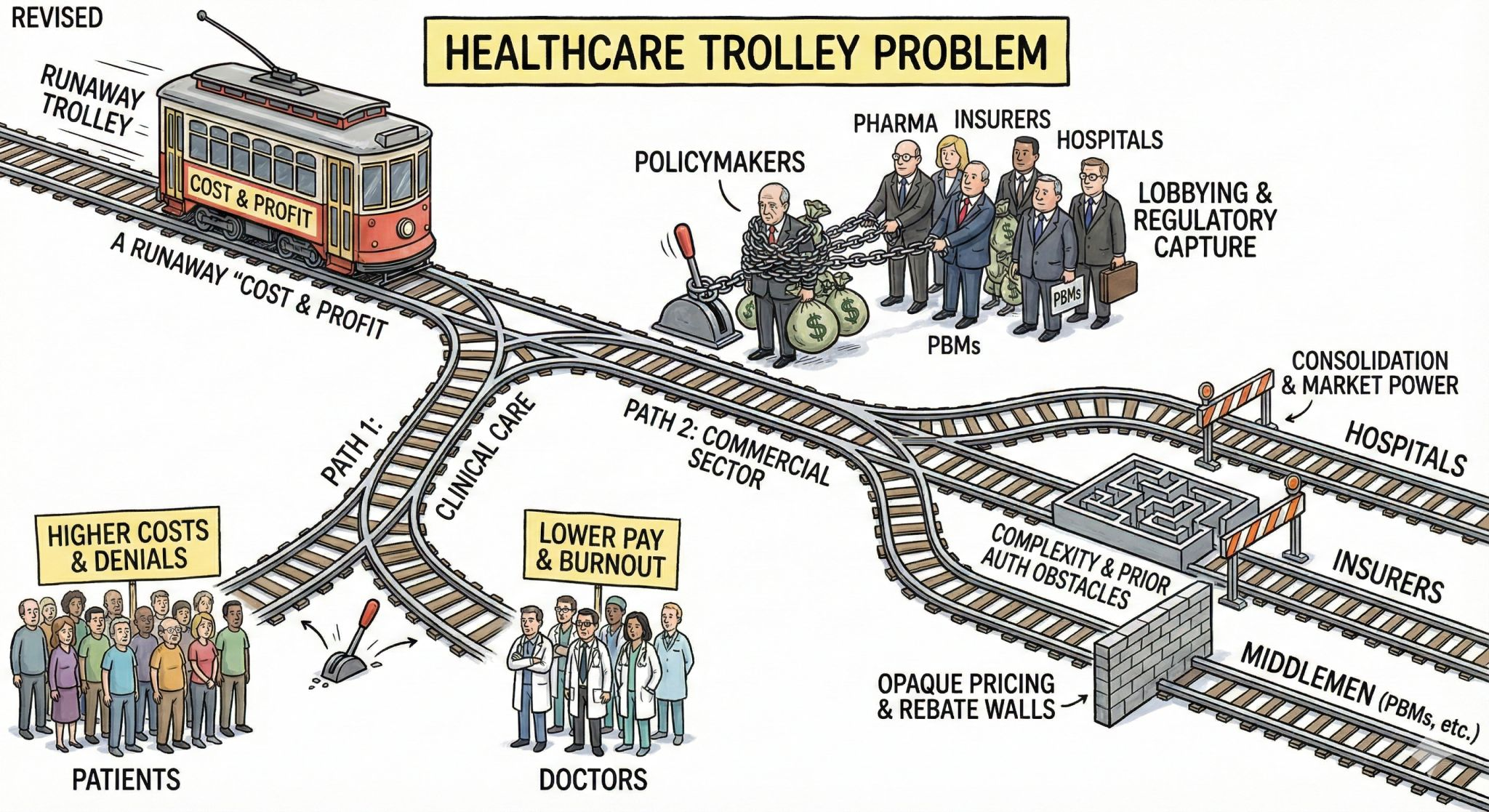

Harvard psychologists Daniel Simons and Christopher Chabris ran a now-famous experiment in the late 1990s. They showed students a short video of six people passing basketballs and told them to count the number of passes made by the three players in white.

Halfway through the film, a person in a gorilla suit walks into the frame, beats its chest and exits. Amazingly, half of viewers — both then and in multiple recreations of the study — never notice the gorilla. They’re so focused on counting passes that they miss the obvious event happening right in front of them.

The authors call this “inattentional blindness.” And you don’t need to visit a research lab to see it. It’s everywhere in American healthcare.

Policymakers, business leaders and medical societies are all busy counting their own pass equivalents: metrics like insurance subsidies, premiums and enrollment numbers.

As a country, we need to stop counting passes long enough to observe how the gorilla negatively affects people everywhere: in Washington, in boardrooms, in workplaces and in rural communities. Only then can we confront the gorilla head on.

1. The gorilla in Washington

In Congress, lawmakers spent 43 days debating how to reopen the government. The fight centered on whether to continue funding the enhanced premium tax credits that have made coverage more affordable for roughly 20 million lower-income Americans who purchase health insurance through the Affordable Care Act’s online exchanges.

Democrats argued that ending those payments in 2026 would cause premiums to spike and make care unaffordable. Republicans warned that continuing them would add nearly $400 billion to the federal deficit over the next decade. Both believed they were protecting Americans from financial harm. And both were right. If the cost of providing medical care isn’t reduced, neither the federal government nor the average family will be able to afford it.

The United States spends $14,885 per person each year on medical care while the next highest-paying nation, Switzerland, spends $9,963 per person with far better clinical outcomes, according to the Peterson Center, .

If the U.S. could cut the spending gap between American and Swiss healthcare in half, our nation would save $700 billion annually. Those savings could help maintain ACA subsidies, lower out-of-pocket costs for families and reduce federal deficits.

But the gorilla inflicts financial damage far beyond just the ACA exchanges. Between federal funding cuts and eligibility changes, analysts warn that millions of Americans enrolled in Medicaid will become uninsured starting in 2026. Meanwhile, because federal law limits Medicare payment growth to the rate of inflation, hospitals make up lost revenue by charging private insurers and their enrollees more (already about 250% of Medicare rates). Ultimately, employers and workers will pay the price.

2. The gorilla in corporate America

America’s C-suite leaders are conducting the business equivalent of counting passes. Instead of confronting the cost of medical care itself, they’re focused on comparing premiums, raising deductibles and choosing plans with narrower physician networks.

But without major changes in how care is delivered, no plan will remain affordable.

The average cost of family health coverage premiums will approach $30,000 next year, with employers paying about $24,000 and workers responsible for the rest, according to an October KFF survey of 1,862 non-federal public and private firms. A projected 9% premium increase means employers and employees together will spend roughly $2,500 more next year per worker — limiting wage growth, hiring and investments in innovation.

America doesn’t have an insurance problem. It has a medical cost crisis.

3. The gorilla in the workplace

While workers focus on wages, benefits and job security, the same cost crisis threatening businesses and government is about to hit them hard.

More than half of U.S. adults receive health insurance through an employer. But as medical costs rise, companies are turning to automation and generative AI to reduce their expenses.

Amazon offers a vivid example: the company eliminated 14,000 office and professional roles and announced plans to combine robotics with generative AI to replace as many as three-quarters of its warehouse workforce. The company plans to create new, higher-skill jobs to maintain the robots, but far fewer (and not for the same people who were displaced).

When workers lose employer-based insurance, they don’t stop getting sick. They turn to Medicaid or subsidized exchange plans. That strains government budgets, lowers hospital reimbursements and pushes insurers to raise commercial premiums even higher.

Unless the cost of medical care drops dramatically, the gorilla’s impact will reverberate throughout society.

4. The gorilla in rural hospitals

The cost crisis is devastating people everywhere, but perhaps nowhere more than in rural America. Over the past two decades, 150 rural hospitals have closed or stopped offering inpatient services. Another 700 facilities (nearly one-third of those remaining) are at risk of shutting down.

With small patient populations and high fixed costs, many rural hospitals can no longer provide inpatient care. But instead of reducing the high cost of care delivery, most communities pursue short-term relief: emergency grants, temporary bailouts and added Congressional funding.

These efforts can delay closure, but they don’t change the math. Even when hospital beds are empty, the buildings must be staffed, heated, insured and maintained, turning every day into a financial loss.

To survive, the model will have to change, and painful sacrifices will be necessary.

Addressing the gorilla everywhere

The United States can dramatically reduce healthcare spending while improving quality. But doing so will require a structural overhaul, not incremental tweaks. Three major opportunities already exist.

1. Shrink our hospital footprint

America maintains far more hospitals than it needs, with many offering duplicate services at high fixed costs. A more sustainable system would:

Eliminate overlapping specialty programs in crowded markets.

Small rural hospitals could transition into 24-hour emergency and urgent-care hubs supported by telemedicine and reliable, low-cost transportation to larger facilities.

2. Prevent diseases before they happen

According to the CDC, more effective control of chronic diseases would reduce medical costs up to $1.8 trillion by preventing as many as half of all heart attacks, strokes, cancers and kidney failures. Three pragmatic opportunities include:

Every complication avoided is a hospital admission, ICU stay or surgery that never happens and is never billed.

Pay for value, not volume

Healthcare’s fee-for-service payment system rewards doing more, not doing better. Capitation — fixed monthly payments to physician groups and hospitals — flips the incentive structure, rewarding improved health, not just disease treatment.

Under capitation, prevention becomes financially rewarded, chronic diseases are managed earlier and more effectively, and care shifts to high-quality, cost-efficient settings, including outpatient facilities and virtual platforms.

The result is a virtuous cycle: healthier patients, fewer complications and significantly lower cost.

No single group — government, employers, patients or clinicians — can solve this crisis alone. Success will require all stakeholders to overcome their inattentional blindness and confront the gorilla together. The only question is how much worse things must become before we do.

A Florida retirement haven is thrown into chaos as a $360 million Medicare overbilling scandal and a Humana–UnitedHealth standoff leave seniors scrambling to keep their doctors.

Behind the gates of The Villages (the pastel Shangri-La of Florida retirement lore) is a place where American seniors zoom around on golf carts like 1977 Thunderbirds and keep wrist stabilizers on the ready for impromptu pickleball matches. It’s a community built on the promise that retirement is a time for sunshine, camaraderie and — most importantly — a health system that doesn’t leave you out in the cold.

HEALTH CARE un-covered has published stories about The Villages in the past – and how the retirement community is rife with Medicare Advantage shenanigans. And today, many Villagers have been blindsided by these shenanigans like they’re part of a Big Insurance hostage crisis straight out of an episode of Days of Our Lives or General Hospital.

A TVH / UnitedHealth dispute leaving seniors “duped”

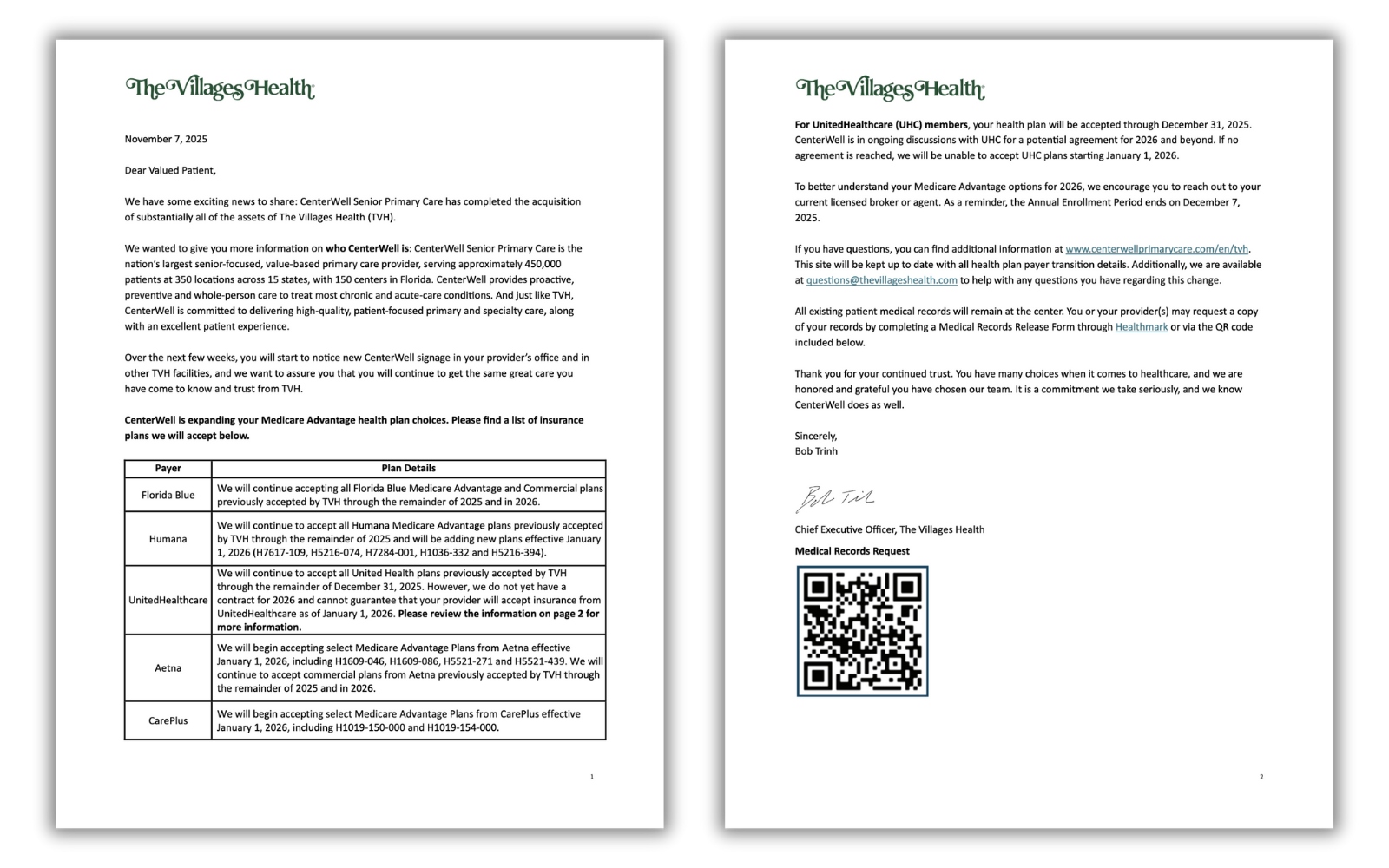

Earlier this year, The Villages Health (TVH) — the health system serving more than 55,000 retirees — promised a smooth handoff as it prepared to sell itself to CenterWell, Humana’s senior-focused primary-care chain. TVH’s CEO assured residents that “no change in care” was coming, according to News 6.

But then came the bankruptcy filing. And then the revelation that TVH owed more than $360 million to the federal government for “Medicare overbilling.” And then the sale. And, according to Village-News, then a bankruptcy judge confirming that, yes, TVH was indeed being swallowed by CenterWell for $68 million.

In other words: the health care version of a soap-opera plot twist. Only with fewer glamorous outfits and more Chapter 11 filings.

On November 7, the very day the sale of TVH closed, patients received a message warning them that their UnitedHealthcare Medicare Advantage plan — the plan they were nudged toward back in 2016 when TVH tried to push all patients into UnitedHealth’s grasp — might not be accepted after Dec. 31, 2025. If negotiations fail, residents must switch doctors or switch insurers.

Message from The Villages Health to their “Valued Patient(s)”.

“Not to be notified until basically the last minute that there isn’t a contract between CenterWell and United at this time is very alarming,” Villager Phyllis McElveen told Spectrum News. “We had already gone out and selected our UnitedHealthcare plan for 2026. We had already done everything. And now to know we might have to make a change is just not a pleasant feeling.”

At The Villages, you can imagine that picking the right Medicare plan is akin to competitive sport — one step removed from a pickleball tournament. The residents do their homework and many reportedly attend “Medicare prep presentations.” So for Villagers, being blindsided is a big deal.

Longtime patient Nancy Devlin told News 6 that she dug through Humana’s and Aetna’s plans to find a plan that might allow her to stay with the physicians she’s seen for six years. But for Devlin, her digging was to no avail. None of the plans matched what she currently had with UnitedHealthcare. Not the same covered medications. Not the same premiums. Not the same out-of-pocket costs. Not the same networks.

“They duped us,” she said. “It’s more expensive and doesn’t have my medications, or I have to pay for them, and I don’t pay for my medications now.”

For retirees on limited incomes, doubling drug costs is a gut punch that can mean one less trip to visit their grandkids or postponing that cruise to the Bahamas. Or for some, putting enough food on the table.

A deal gone sour

To understand how this crisis happened, go back to 2016, when TVH urged residents to switch into UnitedHealthcare Medicare Advantage or lose access to their doctors. Fast-forward to today. TVH is bankrupt, Humana now owns the centers, and UnitedHealth, the world’s largest health conglomerate (and the once-preferred partner for Villagers) is persona non grata unless a deal is reached.

The timing could not be worse. Open enrollment ends December 7, which means that tens of thousands of retirees have just around two weeks to decide whether to switch insurers or switch doctors.

What’s happening here is not simply a contract negotiation gone awry, but a symptom of something deeper. TVH didn’t just owe “some money” to Medicare. It owed about $360 million because of what Humana and The Villages described as a gigantic “Medicare coding error.”

UnitedHealthcare, in turn, accused The Villages’ controlling Morse family of quietly pulling out $183 million between 2022 and 2024 – funds UnitedHealth argued were siphoned off just before the bankruptcy filing.

If that allegation sounds familiar, it’s because we’ve seen versions of this story across the health care industry: private companies treating Medicare Advantage plans like piñatas stuffed with taxpayer dollars. Sometimes, the bat misses the piñata and smacks a whole village of seniors.

Here’s what happens next

The Villages, for all its mid-century charm and retirement-resort quirks, is a microcosm of a national problem that Medicare Advantage is, too often, run for Big Insurance’s advantage with seniors just an afterthought. Corporate acquisitions, bankruptcies, risk-coding schemes, contract disputes and Wall Street demands that lead to fewer and fewer in-network doctors and hospitals and covered drugs. Meanwhile, billions in taxpayer dollars flow through this system with relatively no accountability. Medicare Advantage is corporate welfare on steroids, with the “invisible hand” of the market misleading and then slapping the hell out of vulnerable American seniors to enrich the big guys in control with cushy government handouts.

For Villagers, it’s either/or:

Either CenterWell and UHC strike a deal: The crisis cools, residents keep their current doctors in 2026.

Or no deal is reached: Tens of thousands will either change doctors, change plans or risk being turned away at medical appointments starting Jan. 1, 2026.

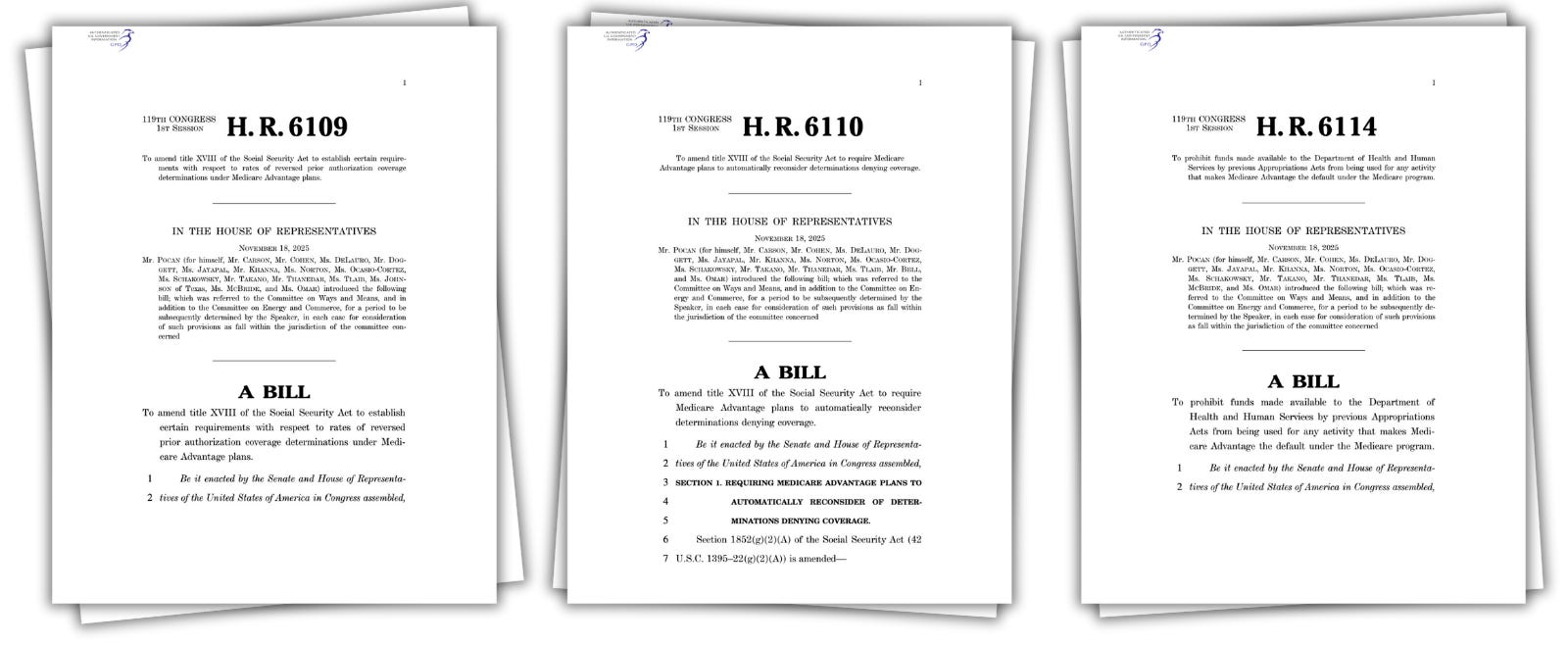

Representative Mark Pocan (D-WI) yesterday introduced eight bills aimed at strengthening traditional Medicare and reining in some of the worst practices in the privately-run Medicare Advantage business. For years, lawmakers have danced around the mounting evidence that private Medicare Advantage plans overbill taxpayers between $80 and $140 billion annually and quietly impose barriers to seniors’ care to boost profits.

Traditional Medicare remains one of the most successful public programs in American history. It was built around a simple promise: If your doctor says you need care, you get it. But as Medicare Advantage has grown, that promise has eroded for millions of people. MA plans are largely run by big insurance conglomerates – like UnitedHealthcare, Elevance and CVS/Aetna – and those insurers decide what care is covered, which doctors you can see and how long you can stay in a hospital. Each cent they have to shell out for your care is a cent they can’t keep in their pockets or split with their shareholders. Wall Street’s relentless demand for more and more of that money incentivizes them to deny or delay care that mean life-and-death for millions of American seniors.

And it’s not just health care policy nerds like me that have been focused on this issue – even the U.S. Department of Justice (DOJ) has taken aim at Medicare Advantage. In February, news broke that the DOJ had launched a civil fraud investigation into UnitedHealth Group, the largest MA insurer, for the company’s alleged use of diagnoses that trigger higher Medicare Advantage payments. And in July, the company confirmed it is the subject of a DOJ criminal investigation. The DOJ reportedly questioned former UnitedHealth Group employees about the company’s business practices.

You can see the entire package of bills on Pocan’s website. They include the Denials Don’t Pay Act, which would force Medicare Advantage plans to face real consequences if too many of their prior-authorization denials are overturned; The Right to Appeal Patient Insurance Denials (RAPID) Act, which would ensure every denial is automatically appealed, sparing sick and elderly patients from navigating a process many never even know exists; and the Protect Medicare Choice Act which would stop insurers and brokers from pushing seniors into Medicare Advantage by default.

Pocan and his co-sponsors understand that Medicare Advantage’s prior authorization hurdles and widespread denials are just Wall Street-directed obstacles that second-guess physicians and delay care. Patients pay the price. Doctors pay the price. And taxpayers pay the price.

More Perfect Union has just posted a video breaking down a truth that Big Insurance hopes you never hear: rising “health care costs” are really rising health insurance profits.

As I explained in the video, UnitedHealth, Cigna, CVS/Aetna are part of a cartel of corporate conglomerates that have built a business model that relies on overpayments in Medicare Advantage, shrinking doctor networks and a sprawling web of vertically integrated subsidiaries that vacuum up our premiums, deductibles and tax dollars — and turn them into shareholder returns as Wall Street relentlessly demands.

Here’s a bit of what I said:

“Your premiums, deductibles and pharmacy bills are all going up. We’re told it’s because medical costs are rising, but the bigger story is who’s capturing the money. In just three months, UnitedHealth Group made $4.3 billion in profits on revenues of $113 billion.

Over the past five years, the cost of a family premium has increased 26%. This year, the average cost of a family policy was almost $27,000.

Just about everybody with private insurance will be paying a lot more than that next year, regardless of whether you get it from your employer or buy it on your own. That’s because UnitedHealth and other big insurance companies cannot control rising health care costs.

In fact, insurance companies benefit from medical inflation. They just jack up their premiums enough to cover the additional cost and guarantee them a tidy profit.”

The video points out the real drivers of cost growth — from UnitedHealth’s nearly 2,700 acquisitions to Medicare Advantage overpayments that funnel billions from taxpayers into corporate profits.

If you haven’t watched it yet, I hope you will and share it with everybody else you know. It’s clear that Congress must pass common sense guardrails to stop Big Insurance from writing the rules of American health care and squeezing Americans.

The average costof covering a U.S. worker will exceed $18,500 next year, underscoring concerns about health care affordability and prompting benefit changes, according to a new Mercer survey.

Why it matters:

The added costs will force tough tradeoffs for employers who’ve tried to maintain generous benefits in tight labor markets and be passed on to workers already reeling from inflationary pressure.

The corporations are likely to offer more plan options, take steps to guide workers to high-performing providers and provide specialized health programs in areas like diabetes and fertility.

By the numbers:

Higher drug spending, including on GLP-1 weight-loss medications, will drive up total health benefit costs an expected 6.7% in 2026, accounting for the highest increase in 15 years,Mercer said.

The survey found that this year, the average cost of employer-sponsored coverage reached $17,496 per employee, a 6% increase that’s well above the rate of inflation and wage growth.

A factor behind the increase was sharp growth in prescription drug spending, which rose 9.4% on average for large employers with 500 or more employees.

49% of large employers covered costly GLP-1 weight-loss drugs in 2025 — up from 44% in 2024.

What’s ahead:

Corporations already are increasing the number of medical plans to pick from.

More are pushing plans with smaller networks of providers, along with stand-alone programs designed to help employees better manage specific health conditions, Mercer said.