Sen. Bernie Sanders (I-Vt.) is urging Senate Democrats to unite behind an expansive health care proposal in the party’s negotiations with Republicans to extend Affordable Care Act tax credits.

Why it matters:

GOP leaders have promised Democrats a vote on the expiring tax credits next month as part of their deal to end the government shutdown.

Sanders wants the Democratic proposal to extend the ACA tax credits, repeal $1 trillion in GOP health care cuts, expand Medicare and lower prescription drug prices, he said in a letter to colleagues late Monday.

Republicans, however, have signaled that any deal to extend the tax credits must be short term and require reforms.

Premiums will more than double for millions of ACA enrollees next year if Congress does not renew enhanced marketplace subsidies by year’s end, according to a new analysis.

The big picture:

Democratic leaders have argued that the government shutdown has made health care a top political issue.

Sanders, the top Democrat on the Senate Health, Education, Labor and Pensions Committee, said Democrats must make proposals that address “systemic deficiencies.”

“We should not be defending a system which is not only, by far, the most expensive in the world, but one which numerous international studies describe as one of the worst,” Sanders wrote to Democratic senators.

Sanders’ HELP committee is expected to be involved in negotiations with Republicans over a potential bipartisan deal to extend the credits next month.

A spokesperson for Senate Minority Leader Chuck Schumer (D-N.Y.) said: “The bill Democrats bring to the floor will be a caucus product.”

Between the lines:

Sanders acknowledged in his letter that his Medicare For All proposal “does not yet have majority support” in the caucus. But he said his latest proposal included “much-needed reforms.”

Sanders also encouraged Democrats to propose investments to expand primary care services, ban stock buybacks and dividends and substantially reduce CEO compensation in the health care industry.

Republicans are taking a harder line against extending enhanced Affordable Care Act subsidies — and doubling down on an alternative plan that would send the money directly to consumers.

Why it matters:

President Trump’s opposition to an extension makes it increasingly unlikely that Republicans will agree to renew the tax credits, even though it’s not clear how the GOP alternative would work or whether the party can reach a consensus.

Driving the news:

Trump wrote on Truth Social on Tuesday that the “only” plan he will support is “sending the money directly back to the people,” and that Congress should not “waste your time” on anything else, like a subsidy extension.

Trump didn’t elaborate on how his plan would work. The ACA already gives people financial help in buying insurance.

Some GOP proposals envision giving people money for a health savings account on top of existing ACA coverage, mitigating concerns about healthy people leaving the market.

Senate health committee Chair Bill Cassidy (R-La.) outlined a plan on Monday that would redirect the enhanced subsidy money to an HSA to help pay out-of-pocket costs for people who chose bronze-level ACA plans, which tend to have high deductibles.

He argued the move would direct money away from insurance companies and to consumers, and empower them to shop for health services.

Anotherpossible outcome would be allowing people to buy cheaper, skimpier coverage that doesn’t comply with the ACA’s benefit requirements. Some policy experts warn that would destabilize the ACA markets, by prompting an exodus of healthier people.

That would leave a sicker risk pool and prompt insurers to raise premiums, resulting in a “death spiral,” said Larry Levitt, executive vice president for health policy at KFF.

By contrast, “I don’t think there’s any risk of, you know, a collapse or death spiral, from what Senator Cassidy is talking about,” Levitt said, though without the enhanced subsidies there would still be “potentially millions of people who just won’t be able to afford insurance at all.”

Between the lines:

Senate Majority Leader John Thune (R-S.D.) wouldn’t rule out a bipartisan solution when asked about Trump’s comments on Tuesday, saying “we’ll see” how negotiations go and that “there’s an openness” to a deal on the GOP side.

He said the biggest obstacle, though, could be whether Democrats agree to apply the Hyde Amendment to the subsidies and add restrictions on using the funds for abortions.

The intrigue:

Cassidy is framing his plan as the most realistic option, given White House and House GOP leadership resistance to the subsidies.

“The president is not going to sign a straightforward extension of premium tax credits,” Cassidy said. “So if you actually want something which can pass and get a vote on the House floor, then what the president is proposing is actually a better way.”

Yes, but:

Democrats believe mounting public concern about rising health costs gives them the upper hand pushing for a subsidy extension.

“Sending people a few thousand dollars while doing nothing to lower health care costs is a scheme to help the ultra-wealthy at the expense of working people with cancer or pre-existing conditions,” Senate Democratic Leader Chuck Schumer said in response to Trump’s comments.

“Americans want Congress to extend the ACA tax credits to keep health insurance premiums from skyrocketing on January 1,” he added.

The big picture:

The war of words is further diminishing the chances that a group of moderates in both parties can find a bipartisan agreement to extend the subsidies with some modifications favored by Republicans, like an income cap and anti-fraud measures.

House GOP leaders have also been criticizing the subsidies. House Majority Leader Steve Scalise (R-La.) said on Fox News on Sunday that the party would be bringing forward legislation in the coming weeks on other ways to lower costs, like expanding HSAs or cracking down on pharmacy benefit managers.

The Senate Finance Committee will hold a hearing Wednesday morning on health care costs, giving senators a chance to stake out their positions further in public.

The bottom line:

It’s unlikely that Trump’s plan would gain the necessary 60 Senate votes to advance. But it could give Republican senators political cover if they oppose a subsidy extension.

Republicans could still opt to use the reconciliation process to pass a bill with a simple majority. Though the White House floated the idea on Tuesday, it’s not clear if any GOP-only plan has the votes to pass.

The Trump administration is expected to spell out its intentions for Medicare Advantage soon — a program that enrolls about half of U.S. seniors but has drawn intensifying criticism for costing the government too much.

Why it matters:

Centers for Medicare and Medicaid Services chief Mehmet Oz called the system “upside down” during his confirmation hearings, hinting at possible changes to the way the federal government pays and regulates plans.

Any big changes would be a departure from a history of friendly treatment from Republican administrations.

Those could become apparent in the proposed 2027 Medicare Advantage rule, which may come out before the end of this year.

How it works:

Many privately run Medicare plans charge no monthly premium and provide supplemental benefits that traditional Medicare doesn’t cover,like dental coverage and help paying for over-the-counter drugs.

The program was created on the premise that private insurers could manage care better and at a lower price point than the federal government.

But some insurers have since drawn fire for categorizing patients as sicker than they are to get higher payments, and for overly complicated pretreatment reviews.

Advisors to Congress projected the federal government would spend about $84 billion more on Medicare Advantage enrollees this year than for people in traditional Medicare. (Insurers say the advisors’ methodology is flawed.)

Oz has a history of promoting Medicare Advantage plans on his popular television show and advocating for an “MA for All” policy.

But he’s been more openly skeptical since joining the administration, as a growing cadre of GOP policymakers ask questions about the program’s finances and insurers’ role in driving up costs.

“I came both to celebrate what you’re trying to do, but also be honest about some of the issues that we’re seeing at CMS,” Oz said at the industry lobby’s conference last month.

Oz believes choice and competition are needed for a strong Medicare program, but also that CMS has a responsibility to keep “program payments fair, transparent, and grounded in data,” Catherine Howden, the agency’s director of media relations, told Axios in response to a request for comment.

This is an opportunity for Medicare Advantage insurers to have some strategic conversations with CMS about Oz’s vision for the program, said Daniel Fellenbaum, senior director at Penta Group.

UnitedHealthcare, Humana and Aetna are the three biggest Medicare Advantage insurers and cover more than 20 million seniors combined.

Where it stands:

This year CMS announced what it termed an “aggressive” strategy to increase audits of the diagnoses Medicare Advantage plans document for enrollees, which could claw back money from insurers.

Medicare’s Innovation Center said it’s working on pilot programs that could change the way thegovernment pays the plans.

Industry onlookers are also expecting the administration to propose changes to the star ratings system, which measures Medicare Advantage plan quality and dictates bonus payments to plans.

What they’re saying:

Insurers and advocates of private Medicare plans remain optimistic that Oz has their best interests at heart.

“He seems to stress good oversight and holding the program to high standards without losing sight of what’s working for seniors,” said Susan Reilly, vice president of communications at Better Medicare Alliance.

Insurance trade group AHIP welcomes “constructive, data-driven conversations with policymakers on actions that strengthen Medicare Advantage,” CEO Mike Tuffin said in a statement to Axios.

AHIP wants a focus on stability in the program after several years of medical costs increasing faster than Medicare Advantage payment, it said.

Reality check:

The 2026 update to plan payment, the first of this administration, is better than anticipated for insurers, giving them more than $25 billion increase in federal payments.

The Trump administration also struck voluntary agreements with insurers to simplify the rules for authorizing procedures and treatments ahead of time, rather than using its regulatory authority to require changes.

“We hear rhetoric talking tough on MA, but we’ve not seen them put that into actual reality,” said Chris Meekins, managing director at Raymond James.

Any big policy changes next year would also become apparent to seniors right before the midterm elections. Bigger policy swings from the administration might be more likely to go into effect for 2028, Meekins said.

What we’re watching:

President Trump has been vocal about his distaste for health insurance companies on social media lately as Congress debates extending enhanced premium subsidies for Obamacare coverage.

That ire could seep into how he directs his administration to regulate Medicare Advantage.

The Trump administration is expected to spell out its intentions for Medicare Advantage soon — a program that enrolls about half of U.S. seniors but has drawn intensifying criticism for costing the government too much.

Why it matters:

Centers for Medicare and Medicaid Services chief Mehmet Oz called the system “upside down” during his confirmation hearings, hinting at possible changes to the way the federal government pays and regulates plans.

Any big changes would be a departure from a history of friendly treatment from Republican administrations.

Those could become apparent in the proposed 2027 Medicare Advantage rule, which may come out before the end of this year.

How it works:

Many privately run Medicare plans charge no monthly premium and provide supplemental benefits that traditional Medicare doesn’t cover,like dental coverage and help paying for over-the-counter drugs.

The program was created on the premise that private insurers could manage care better and at a lower price point than the federal government.

But some insurers have since drawn fire for categorizing patients as sicker than they are to get higher payments, and for overly complicated pretreatment reviews.

Advisors to Congress projected the federal government would spend about $84 billion more on Medicare Advantage enrollees this year than for people in traditional Medicare. (Insurers say the advisors’ methodology is flawed.)

Oz has a history of promoting Medicare Advantage plans on his popular television show and advocating for an “MA for All” policy.

But he’s been more openly skeptical since joining the administration, as a growing cadre of GOP policymakers ask questions about the program’s finances and insurers’ role in driving up costs.

“I came both to celebrate what you’re trying to do, but also be honest about some of the issues that we’re seeing at CMS,” Oz said at the industry lobby’s conference last month.

Oz believes choice and competition are needed for a strong Medicare program, but also that CMS has a responsibility to keep “program payments fair, transparent, and grounded in data,” Catherine Howden, the agency’s director of media relations, told Axios in response to a request for comment.

This is an opportunity for Medicare Advantage insurers to have some strategic conversations with CMS about Oz’s vision for the program, said Daniel Fellenbaum, senior director at Penta Group.

UnitedHealthcare, Humana and Aetna are the three biggest Medicare Advantage insurers and cover more than 20 million seniors combined.

Where it stands:

This year CMS announced what it termed an “aggressive” strategy to increase audits of the diagnoses Medicare Advantage plans document for enrollees, which could claw back money from insurers.

Medicare’s Innovation Center said it’s working on pilot programs that could change the way thegovernment pays the plans.

Industry onlookers are also expecting the administration to propose changes to the star ratings system, which measures Medicare Advantage plan quality and dictates bonus payments to plans.

What they’re saying:

Insurers and advocates of private Medicare plans remain optimistic that Oz has their best interests at heart.

“He seems to stress good oversight and holding the program to high standards without losing sight of what’s working for seniors,” said Susan Reilly, vice president of communications at Better Medicare Alliance.

Insurance trade group AHIP welcomes “constructive, data-driven conversations with policymakers on actions that strengthen Medicare Advantage,” CEO Mike Tuffin said in a statement to Axios.

AHIP wants a focus on stability in the program after several years of medical costs increasing faster than Medicare Advantage payment, it said.

Reality check:

The 2026 update to plan payment, the first of this administration, is better than anticipated for insurers, giving them more than $25 billion increase in federal payments.

The Trump administration also struck voluntary agreements with insurers to simplify the rules for authorizing procedures and treatments ahead of time, rather than using its regulatory authority to require changes.

“We hear rhetoric talking tough on MA, but we’ve not seen them put that into actual reality,” said Chris Meekins, managing director at Raymond James.

Any big policy changes next year would also become apparent to seniors right before the midterm elections. Bigger policy swings from the administration might be more likely to go into effect for 2028, Meekins said.

What we’re watching:

President Trump has been vocal about his distaste for health insurance companies on social media lately as Congress debates extending enhanced premium subsidies for Obamacare coverage.

That ire could seep into how he directs his administration to regulate Medicare Advantage.

Layoff trends in 2025 indicate an increase in job cuts compared to 2024, with US employers announcing nearly 950,000 cuts through September, the highest number since 2020. Key drivers include cost-cutting measures, the strategic implementation of artificial intelligence (AI), and a cooling labor market.

Key Trends

Elevated Numbers: Total US job cuts through October 2025 were over one million, a 65% increase from the same period in 2024. October 2025 had the highest number of layoffs for that month in 22 years.

AI as a Primary Driver: AI adoption is a leading cause for job cuts as companies restructure for efficiency and reallocate resources. Companies like Amazon and Intel have cited AI as a reason for significant workforce reductions.

“Forever Layoffs”: A new trend involves smaller, more regular rounds of layoffs (fewer than 50 people) that create ongoing worker anxiety and impact company culture. These rolling cuts often stay out of headlines but contribute significantly to the overall job cuts.

Method of Notification: The process is becoming more impersonal, with many employees being notified of their termination via email or phone call rather than in-person meetings.

Hiring Slowdown: Alongside the layoffs, there has been a sharp drop in hiring plans, with planned hires for the year at their lowest level since 2011.

Affected Industries

While tech has been significantly impacted since late 2022, other industries are also facing substantial cuts in 2025:

Technology: Remains a leading sector for cuts as companies continue to restructure after pandemic-era overhiring and focus on AI.

Retail and Warehousing: Companies like Target and UPS are cutting thousands of jobs due to changing consumer demands, automation, and a push for efficiency.

Energy and Manufacturing: Oil giants such as Chevron and BP are making cuts as part of cost-reduction strategies and market consolidation.

Finance and Consulting: Firms like PwC and Morgan Stanley are trimming staff, citing factors like low attrition rates and the need to realign resources.

Media and Communications: Companies like CNN and the Washington Post have made cuts to pivot toward digital services and reduce costs.

Economic Context

The overall U.S. labor market remains relatively healthy despite the uptick in layoffs, though it is showing signs of cooling. The unemployment rate has inched up, and consumer sentiment has declined. The Federal Reserve is monitoring the situation and has implemented interest rate cuts to help stabilize the job market.

Wall Street reacts to the failed ACA subsidy extension — and to the president’s swipe at “money sucking insurance companies.”

Wall Street got the jitters yesterday after Donald Trump’s pointed remarks about “money sucking insurance companies” and a Congressional deal that failed to extend the enhanced subsidies under the Affordable Care Act (ACA) marketplace plans. According to one market analysis, shares of Centene (CNC) plunged about 8.15% in pre-opening trade, while competitors such as Molina (MOH) fell 4.6%, Elevance (ELV) dropped 3.7%, UnitedHealth Group (UNH) slipped 1.9% and Humana (HUM) declined 1.45%.

Why the sell-off? Because the enhanced ACA subsidies — which reduce premiums for some marketplace enrollees — expire at the end of the year and without renewal, an estimated 3.8 million people could lose coverage, and premiums would rise significantly for others. Insurers that rely on the stability and growing enrollee base of the ACA marketplace face heightened risk when that funding is in question – especially when the dollars are guaranteed – like when they are shoveled out from the federal government.

Still, it’s worth noting that the ACA marketplace business is not the primary profit engine for most large payers. Their bigger gains typically come from taxpayer-funded programs like Medicare Advantage, Medicaid managed-care contracts and veterans’ / VA contracts.

Here’s how five of the major players fared in 2024 profits:

Centene: $3.2 billion (+590% since 2014)

UnitedHealth Group: $32.2 billion (+214% since 2014)

Elevance: $9.1 billion (+78% since 2014)

Humana: $2.6 billion (+8.3% since 2014)

Molina: $1.18 billion (+780% since 2014)

Because most of their gains have not come from ACA exchange plans (and especially not the thin margin employer market) but through their other government-subsidized businesses, investors can have some certainty their investments in those companies are still largely safe and Big Insurance will be able to weather this storm.

For instance, the industry has always been able to strongarm rough patches in the consumer market – as long as they can stave off any meaningful changes to their bread and butter taxpayer-funded programs. As we reported last month, the industry’s outside PR and lobbying friends – Better Medicare Alliance and Medicare Advantage Majority – have hit the airwaves and the halls of Congress to halt the advancement of the No UPCODE Act. The bipartisan bill, sponsored by Senators Bill Cassidy (R-LA) and Jeff Merkley (D-OR) would end wasteful, fraudulent practices in Big Insurance’s Medicare Advantage businesses that funnel taxpayer money into the pockets of industry executives and Wall Street shareholders and could save taxpayers as much as $124 billion over the next decade and keep the Medicare Trust Fund solvent for years longer.

As of this morning, insurers seem to be fairing better. Centene, UnitedHealth Group, Elevance, Humana and Molina are all back in the green.

Research suggests UnitedHealth may be running a shell game — one that lets insurers flout regulations and obscure the harmful consequences of their vertical integration strategies.

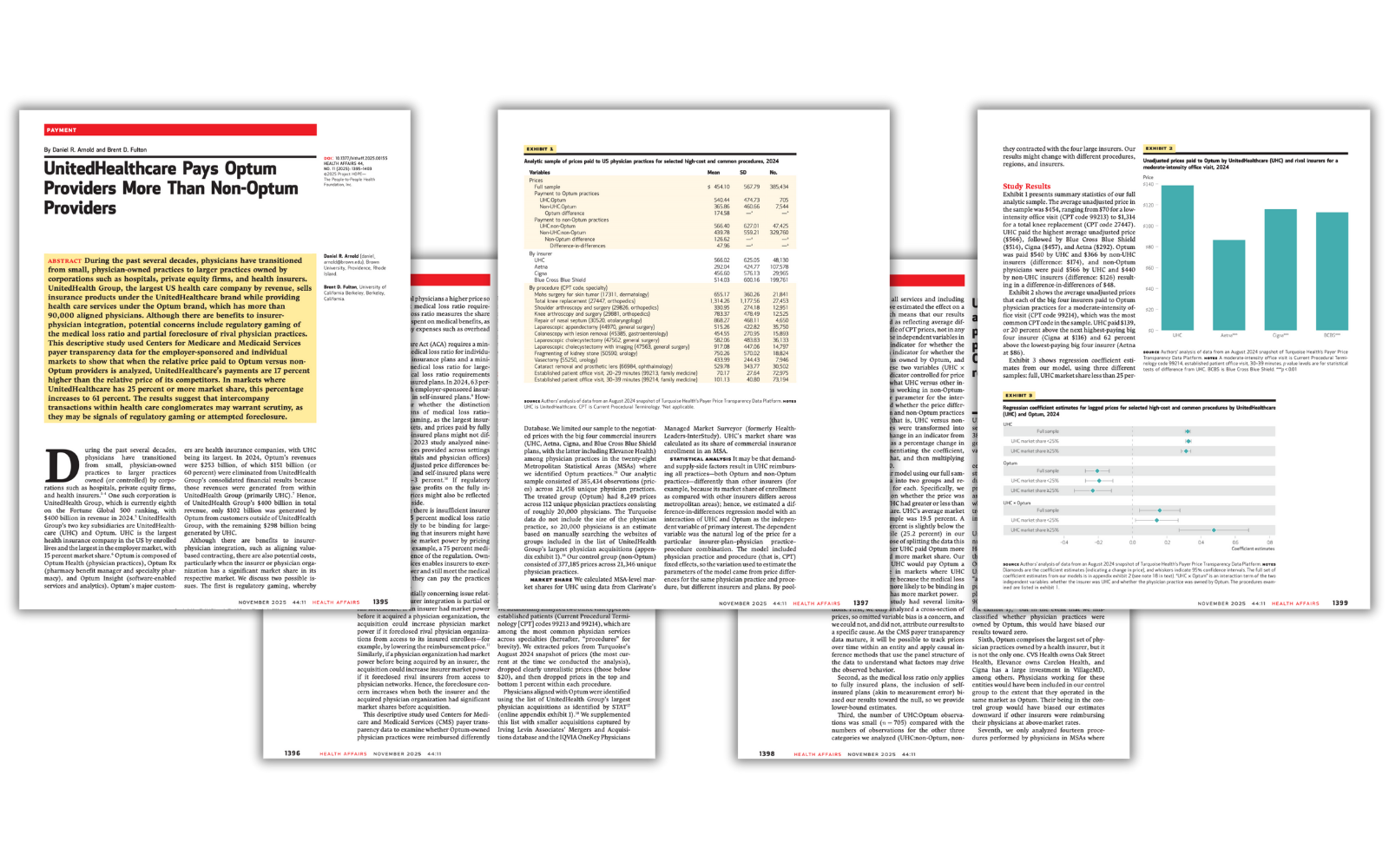

A new Health Affairs study has confirmed that UnitedHealth Group — the nation’s largest health care conglomerate — is doing more than dominating the market; it’s playing by a different set of rules.

Researchers Daniel Arnold of Brown University and Brent Fulton of UC Berkeley analyzed new federal “Transparency in Coverage” data and found that UnitedHealth’s insurance arm, UnitedHealthcare, pays its own Optum physicians 17% more on average than it pays other doctors for the same services. And in markets where UnitedHealthcare holds a large share — 25% or more — that gap explodes to 61%.

The Affordable Care Act’s medical loss ratio (MLR) rule requires insurers to spend at least 80–85% of premium revenue on patient care, rather than on administrative expenses and profits, but if an insurer can funnel “medical spending” to its own subsidiaries — in this case, the thousands of subsidiaries that now comprise Optum — it can appear to comply with the law while actuallyshifting massive amounts of revenue from one pocket to another.

Under the MLR rule, insurers are required to send rebate checks to their customers if they don’t comply with the MLR requirement. The Health Affairs research suggests that UnitedHealth may be flouting that rule by deliberately overpaying the health care delivery operations it owns to comply with the letter of the law if not the intent. Because physician practices and other provider entities are exempt from the MLR rule, regardless of ownership, UnitedHealth can avoid sending its customers the rebates they otherwise would get and pad the conglomerate’s bottom line.

As the researchers put it:

“The results suggest that intercompany transactions within health care conglomerates may warrant scrutiny, as they may be signals of regulatory gaming or attempted foreclosure.”

Another way to game the system

This study also highlights another consequence: independent physician practices are being squeezed out. When UnitedHealth pays Optum doctors more — and non-Optum doctors less — it creates an uneven playing field that could drive small and mid-sized practices out of business.

The authors warn that this pattern “could lead to independent practices closing or joining larger groups such as Optum”. Over the past decade, Optum has quietly amassed more than 90,000 doctors under its control — more than any other private organization in the country.

And it’s not just doctors – UnitedHealth owns nearly 2,700 entities – a pharmacy benefit manager, a data analytics firm, home health companies and even surgery centers. The study notes that in 2024, Optum reported $253 billion in revenue, but 60% of that was simply money moving internally from UnitedHealthcare. In other words, UnitedHealth’s empire is built on being able to feed itself by self-dealing.

The point

This research provides some of the strongestevidence yet that UnitedHealth’s “vertical integration” strategy is distorting the market — not to improve care but to maximize profits under the guise of “compliance.”

For regulators at the Department of Justice, the Department of Labor (which has jurisdiction over employer-sponsored plans administered by UnitedHealth and other insurers) and the Centers for Medicare and Medicaid Services, this should be a wake-up call. As the authors conclude, even a 1% artificial price increase through these internal transfers could significantly reduce the rebates insurers owe consumers under the medical loss ratio rule. That’s billions of dollars that patients, taxpayers and employers are entitled to but that never leave the company’s bank account – except to reward shareholders and top executives. During just the first nine months of this year, UnitedHealth reported making nearly $19 billion in profits on revenues of more than $334 billion. Both revenues and profits likely would have been considerably less if not for the apparent gaming the Health Affairs researchers uncovered.